Author: Thejaswini M A

Compiler: Saoirse, Foresight News

In Goodfellas, Ray Liotta has a line: "Forget about it. Pay me." This line shatters the romantic filter of mafia morality glorified in works like The Godfather, starkly revealing the cold, parasitic, and profit-driven essence of organized crime. Following this similar logic, let's discuss large tech companies.

You control value by controlling profits. To achieve this, you don't even need to build a public blockchain protocol or a project. This is a profit war with no rules. However, we cannot blame companies like Coinbase, Stripe, or Kraken for making such choices.

From the most fundamental business logic, their operations resemble a shrewd real estate play: securing traffic distribution channels first. Now holding the power of these channels, they look down and ask, "Who really holds the pricing power?"

Coinbase built its own blockchain; Stripe spent $11 billion acquiring infrastructure it could have leased; Kraken spent $15 billion acquiring a derivatives trading platform; Apple built the App Store. The logic of this playbook is: let others explore the market and bear the early-stage risks, then acquire the underlying infrastructure once the profitability of the sector becomes sufficiently attractive. The core question this article explores: when traffic distribution channels no longer hold core value, where will the industry head?

Coinbase has 110 million verified users. For years, its lending products offered to users were built on the open-source protocol Morpho, with all protocol fees going to Morpho. Later, Coinbase launched its own Layer 2 blockchain, Base. Morpho chose to deploy on Base solely because Coinbase's massive user base could bring transaction volume. Now, every transaction on Base generates sequencing fees that flow entirely into Coinbase's pockets, not Morpho's.

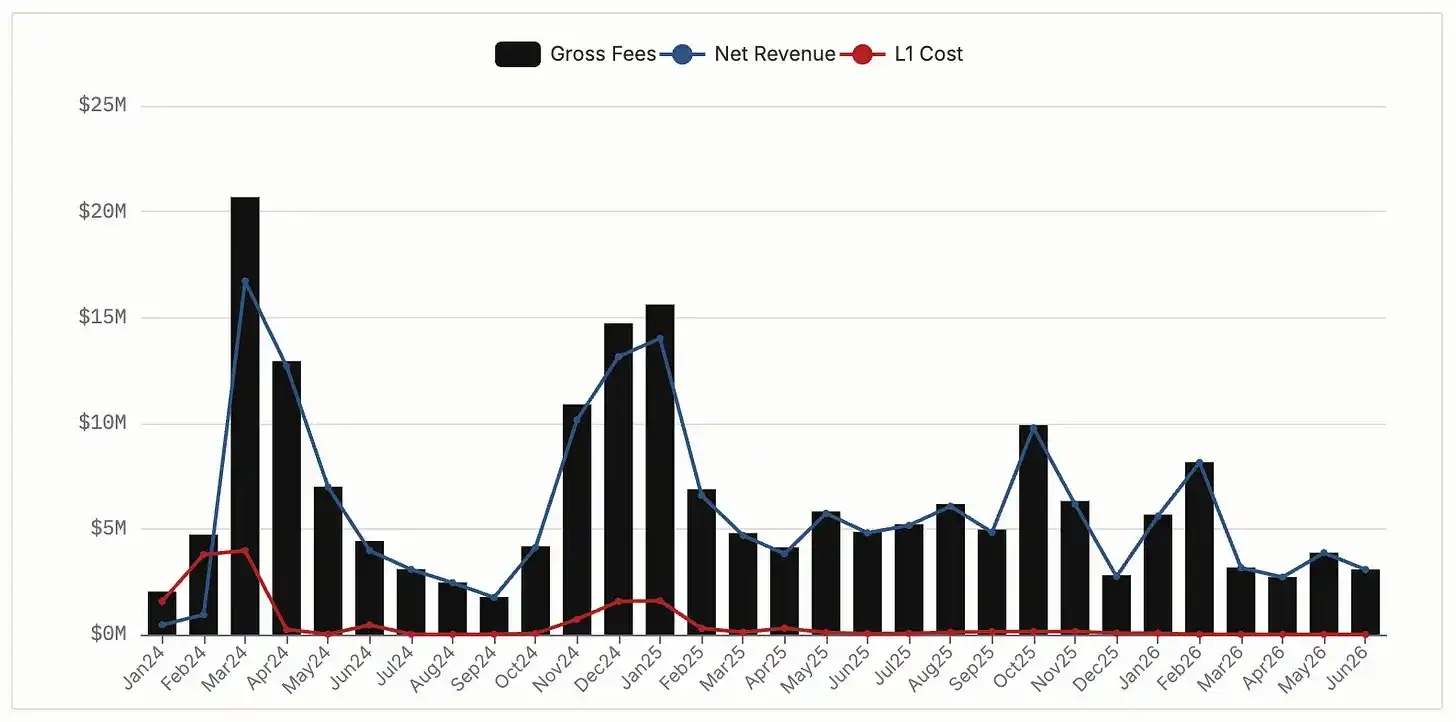

Base generated $76 million in net sequencing fee revenue in 2024, and $74 million in 2025. Before February 2026, according to a licensing agreement, Coinbase needed to share a portion of revenue with Optimism. But eventually, Coinbase severed the partnership, switched to self-developed underlying architecture, and now keeps the entire $64 million revenue stream. Meanwhile, Morpho remains firmly rooted on Base, developing well with a Total Value Locked (TVL) of $2.5 billion. However, every business processed by Morpho now shares a portion with Coinbase.

Base Monthly Sequencing Fee Revenue, Data Source: DeFiLlama

Coinbase, relying on Morpho's underlying architecture, launched a $300 million Bitcoin-backed lending product. Its issued wrapped Bitcoin, cbBTC, is the largest collateral asset within Morpho, accounting for 38% of the protocol's total TVL. This creates a mutual interdependence: Morpho holds the underlying core capability of Coinbase's credit products, while Coinbase can extract a revenue share from all of Morpho's business, making it difficult for either side to easily sever the cooperation.

Consider Stripe's case: in early 2025, it spent $11 billion acquiring Bridge. Before that, Stripe's stablecoin business relied on Circle's infrastructure. Circle held the stablecoin issuance rights and earned the floating interest generated by the reserve collateral assets. At that time, all revenue from Stripe's trillion-level stablecoin transactions flowed to Circle. The acquisition of Bridge completely reversed this situation. Bridge issues its own stablecoin, USDB, collateralized by BlackRock money market funds. After switching to USDB, the sizable interest from these reserves remained entirely within Stripe's ecosystem. Stripe's annual payment transaction volume reaches $1.4 trillion; long-term rental of a competitor's profit-generating foundation meant losing hundreds of millions in annual profit.

Patrick Collison once called stablecoins "the room-temperature superconductors of finance." Spending $11 billion to fully own this underlying tool is far more economical than continuously paying tolls to a competitor.

Pure spot exchanges have a natural growth ceiling, with users only able to trade hundreds of tokens. But Kraken wanted to attract institutional investors and sophisticated retail traders, groups that primarily trade via futures and clearing derivatives. Operating a derivatives business requires registration with the U.S. Commodity Futures Trading Commission (CFTC), membership with the National Futures Association (NFA), and broker-dealer licenses. Building this entire compliance system takes years; even building from scratch, regulators could deny approval for various uncontrollable reasons.

This is why Kraken targeted NinjaTrader. The $1.5 billion acquisition in January 2025 brought not only 1.7 million funded trading accounts but, more crucially, directly provided Kraken with the full set of broker-dealer licenses it would have struggled to quickly develop and obtain on its own.

By acquiring ready-made compliance qualifications, Kraken completely freed itself from dependence on external partners. It now fully owns the entire technological system and licenses, needing to rely on no one else nor spend years awaiting regulatory approval.

Some might say: large enterprises swallowing small protocols, isn't that industry norm? What's new here?

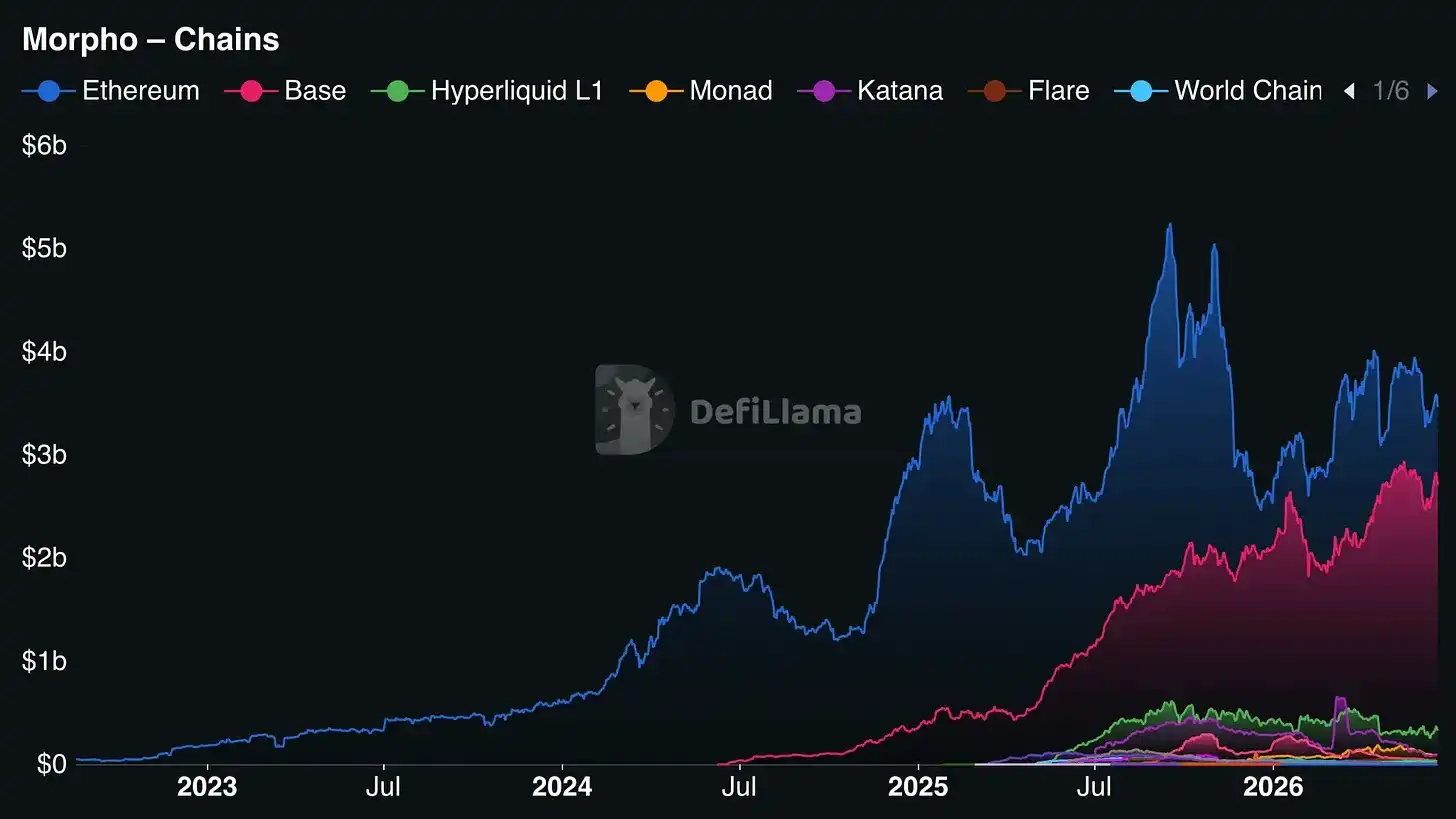

Morpho's total TVL is $6.4 billion, with $3.308 billion deployed on Ethereum and $2.488 billion deployed on Base. If Coinbase decided to delist Morpho and use a self-developed lending protocol instead, Morpho would immediately lose 39% of its TVL; but it would still retain 52% on Ethereum, while continuing to expand across multiple chains like Hyperliquid L1, Monad, and Arbitrum, allowing its overall business to operate stably.

Morpho TVL Distribution Across Chains, Data Source: DeFiLlama

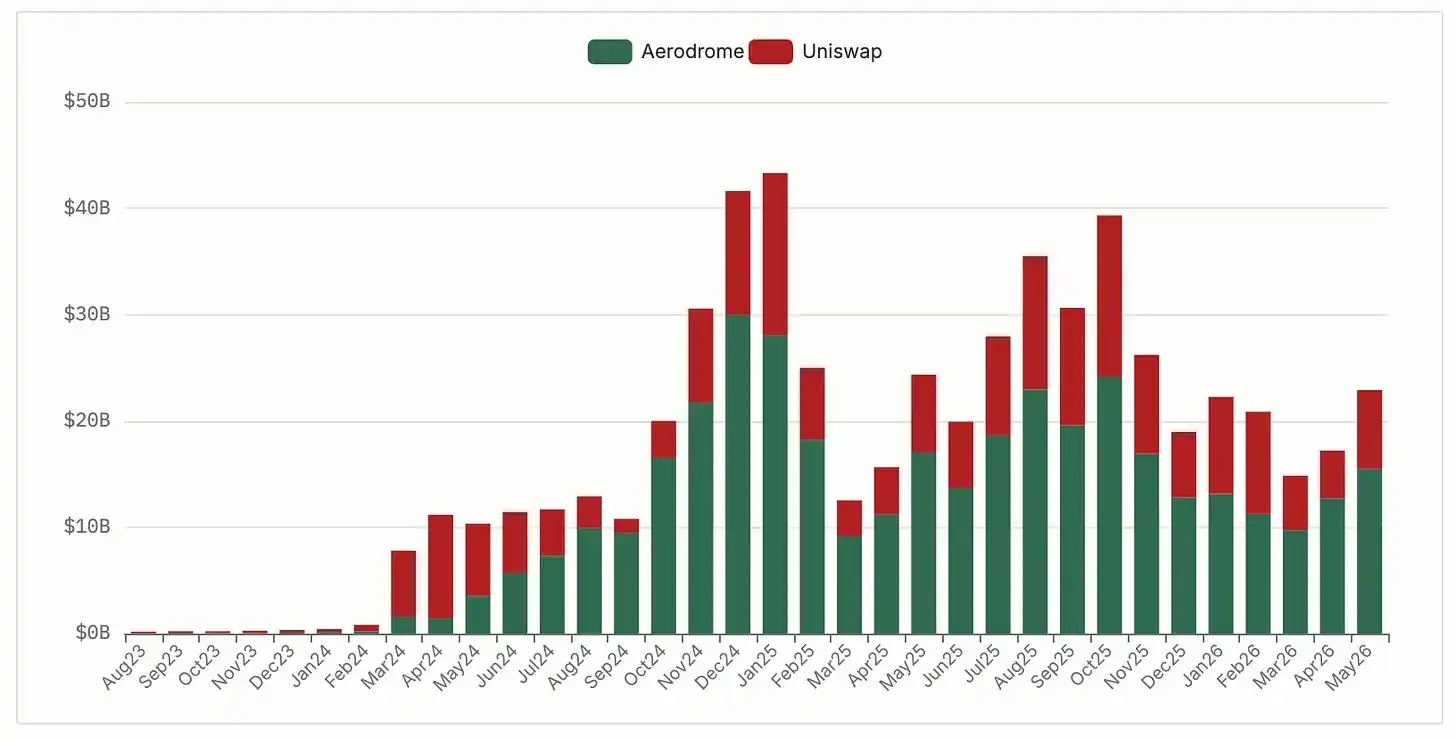

The case of Aerodrome on the Base chain vividly demonstrates the industry impact when a chain operator promotes its own competitor. Aerodrome is Base's native decentralized exchange (DEX), optimized for Base's architecture. Coinbase Ventures holds approximately $20 million worth of AERO tokens, its largest liquidity token investment; meanwhile, the project, through locked AERO token voting, guides liquidity towards Coinbase's products, including cbBTC pools. Aerodrome captures about 51% of Base's DEX trading volume, peaking at 77% in September 2024. Uniswap, deployed across 44 chains, is Base's second-largest DEX, holding 30% trading volume. Even after losing its top position on a single chain, Uniswap did not die: in 2025, it processed $212 billion in volume on Base, with estimated all-chain monthly trading volume around $73 billion.

Base DEX Trading Volume Share, Data Source: DeFiLlama

This case confirms that multi-chain deployment is a protocol's natural moat. A project deployed only on a single chain is entirely at the mercy of the chain operator, who can at any time promote a competitor to squeeze its survival space. Conversely, a multi-chain deployed protocol can continue operating normally across other tracks even if it loses one chain's market. After witnessing Uniswap's traffic diversion on Base by Aerodrome, Morpho rapidly expanded its deployment across multiple chains. Large traffic platforms can vertically integrate downwards into the underlying layer, while open-source protocols can horizontally expand across multiple chains to diversify risk.

If you rely on underlying infrastructure you do not own, you do not truly control your business. The party controlling the underlying layer holds overwhelming pricing power over you, can define your product experience, and ultimately influence your operational stability. For companies of this scale, this dependency relation results in tangible profit loss daily. This business logic is not unique to crypto: Amazon built its moat on AWS; Apple, once constrained by Intel's chip roadmap, spent years developing custom chips to break free.

Everyone can check in real-time how much revenue Coinbase earns from Base sequencing fees and clearly view Morpho's TVL across various chains. This value extraction process is entirely transparent, unlike the internal infrastructure profits of traditional internet giants like Amazon.

One potential industry direction is a future market entirely controlled by giants like Coinbase, Stripe, Kraken, and a few banks. They would control the entire industry chain from underlying protocols to payment cards, with open-source protocols merely filling niche gaps the giants haven't yet addressed. This is a fully plausible development path for fintech. Open-source technology would no longer be a free, vast fertile ground for innovation but merely a patch of tape filling tiny crevices in giant enterprises not yet monetized. Like the joke goes: "Look at this high-quality small open-source protocol; let's just build a commercialization system on top of it to harvest the traffic."

However, I lean towards an optimistic view: considering several current acquisition cases, the probability of such complete monopolistic control is not as high as it seems. Underlying protocols are difficult to be exclusively monopolized by giants like traffic channels. Morpho can complete deployment on a new chain in mere weeks; replacing a battle-tested lending protocol deeply embedded in institutional operations incurs extremely high costs, not easily perceptible to outsiders. Coinbase's $300 million Bitcoin lending product still relies on Morpho because replicating Morpho's security system from scratch would take years and introduce security risks Coinbase is unwilling to bear.

Protocols that can survive this wave of giant consolidation share a core condition: completing full multi-chain deployment before traffic giants build their own ecosystems, deeply embedding themselves into major enterprises' backend systems, making the economic cost of replacement prohibitively high. Even Robinhood, a traffic giant with a massive user base, chose to integrate the third-party zero-knowledge proof perpetual contract exchange Lighter as its trading backend. Robinhood Ventures participated in Lighter's $68 million funding round, and founder Vlad Tenev maintains close communication with the project.

If only traffic channels could build moats, Robinhood could have self-developed the entire backend like Coinbase. But it didn't: combining centralized exchange trading speed with zero-knowledge verifiable matching logic is an extremely difficult niche technical challenge; the Lighter team spent over a year solving it. Robinhood calculated that purchasing the right to use mature technology is far more economical than developing from scratch.

Currently, Morpho occupies this favorable position of mutual deterrence, and Uniswap is the pioneer of this path. The speed of institutional expansion and the speed of open-source protocols' horizontal multi-chain expansion are in a game, the outcome of which will determine the direction of the industry landscape.

For now, the underlying operations of giants like Stripe and Coinbase still rely on open-source technology. In the short term, open-source protocols can still stand firm. In two years, we can re-examine the industry landscape.