Original Author: @0xJaehaerys, Gelora Research

Original Compilation: EeeVee, SpecialistXBT, BlockBeats

Original Title: Lending Markets Do Not Need the Curator Model

Editor's Note: After the successive blowups of Stream Finance and USDX, the DeFi community is undergoing a painful disenchantment. The "Curator" model introduced by protocols like Morpho and Euler was originally intended to solve liquidity fragmentation but inadvertently reintroduced the moral hazard of "human" factors on-chain. The author of this article points out that current lending protocols mistakenly bundle "risk definition" with "order matching." By drawing on the order book model from traditional finance, this article constructs a new paradigm that eliminates the need for curators and relies on algorithmic automatic routing.

The Evolutionary Logic of Lending Markets

Reviewing the evolution of on-chain trading provides a reference for understanding lending market.

AMMs based on constant functions (like Uniswap) solved a fundamental problem: how to create a market without active market makers? The answer was to use an invariant function to preset the "shape" of liquidity. Liquidity providers pre-agree to a set of strategies, and the protocol handles execution automatically.

This works well in trading because trading is relatively simple: buyers and sellers meet at a price. But lending is much more complex. A loan involves multiple dimensions:

Interest rate

Collateral type

Loan-to-Value ratio (LTV)

Term (fixed vs. demand)

Liquidation mechanism

Matching a loan requires satisfying constraints across all these dimensions simultaneously.

Early DeFi lending directly adopted solutions similar to AMMs. Protocols like Compound and Aave preset interest rate curves, with lenders joining a shared pool. This allowed lending markets to function without active lenders.

But this analogy has a fatal flaw. In DEX trading, the shape of the constant function curve affects execution quality (slippage, depth); in lending, the shape of the interest rate curve directly determines risk. When all lenders share a single pool, they also share the risk of all collateral accepted by the pool. Lenders cannot express their desire to bear only specific types of risk.

In the trading space, order books solved this problem: they allow market makers to define their own "curve shape." Each market maker quotes at their preferred price, the order book aggregates these quotes into a unified market, but each market maker still controls their own risk exposure.

Can lending adopt the same approach? A project named Avon attempts to answer this question.

The Liquidity Fragmentation Problem

To give lenders control, DeFi's first attempt was market isolation.

Protocols like Morpho Blue and Euler allow anyone to create lending markets with specific parameters: designated collateral, borrowed asset, fixed liquidation LTV, and interest rate curve. Lenders deposit into markets that match their risk preferences. Bad debt in one market never spills over to another.

This is perfect for lenders; they get the risk isolation they want.

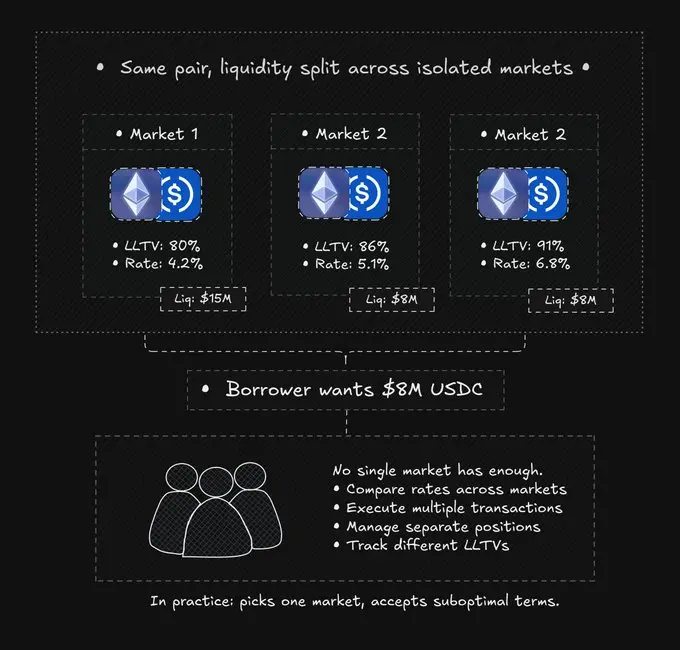

But for borrowers, this creates fragmentation.

Take ETH-USDC lending as an example. There might be a dozen different markets:

Market B: $3M liquidity, 86% LTV, 5.1% interest rate

Market C: $2M liquidity, 91% LTV, 6.8% interest rate

... and 9 other markets with lower liquidity

A user wanting to borrow $8 million cannot be satisfied from a single market. They must manually compare prices, execute multiple transactions, manage分散的头寸, and track different liquidation thresholds. The theoretical optimal solution requires splitting the loan across four or more markets.

In practice, no one does this. Borrowers typically just pick one market. Capital utilization is low in fragmented pools.

Market risk isolation solved the lender's problem but created a borrower's problem.

The Limitations of Curator Vaults

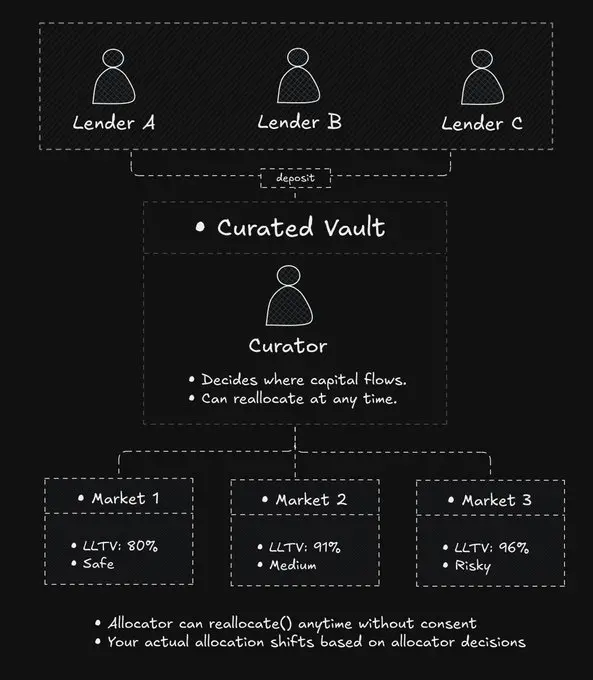

The curator vault model attempts to bridge this gap.

The idea is: professional curators manage capital allocation. Lenders deposit into vaults, and curators allocate funds to underlying markets, optimizing yield and managing risk. Borrowers still face fragmented markets, but at least lenders don't have to manually rebalance.

This helps lenders who want to "set and forget," but it introduces something DeFi aimed to eliminate: discretionary power.

Curators decide which markets get capital and can reallocate at any time. The lender's risk exposure changes with the curator's decisions, unpredictably and uncontrollably. As one Twitter user put it: "The curator is PvPing the borrower, but the borrower doesn't even know they are being farmed."

This asymmetry is not only in strategy but also in the accuracy of the basic interface. Morpho's UI sometimes shows "$3 million available liquidity," but in practice, funds at low interest rates are scarce, with most capital located in higher rate tiers.

When liquidity coordination relies on human decisions, transparency suffers.

Capital allocators adjust market liquidity on their schedule, not based on the market's immediate needs. Vaults try to solve borrower fragmentation through "rebalancing," but rebalancing requires gas fees, depends on the curator's willingness, and often lags. Borrowers still face suboptimal rates.

Separating Risk from Matching

Lending protocols conflate two distinct modules.

User definition of risk: Different lenders have different views on collateral quality, leverage ratios.

The protocol's method of matching loans: This is mechanical. It doesn't require user subjectivity, just efficient routing.

The pooled model bundles these two, lenders lose control.

The isolated pool model separates risk definition but abandons matching, forcing borrowers to manually find the optimal path.

The curator vault model adds matching back through the curator role but introduces a trust assumption in the curator.

Can matching be automated without introducing discretion (human intervention)?

Order books in trading did this. Market makers define quotes, the order book aggregates depth, matching is deterministic (best price first). No one decides where orders go, the mechanism decides everything.

CLOB lending applies the same principle to credit markets:

Lenders define risk through isolated strategies.

Strategies post quotes to a shared order book.

Borrowers interact with unified liquidity.

Matching happens automatically, without curator intervention.

Risk stays with the lender, coordination becomes mechanical. No trust in a third party is needed at any point.

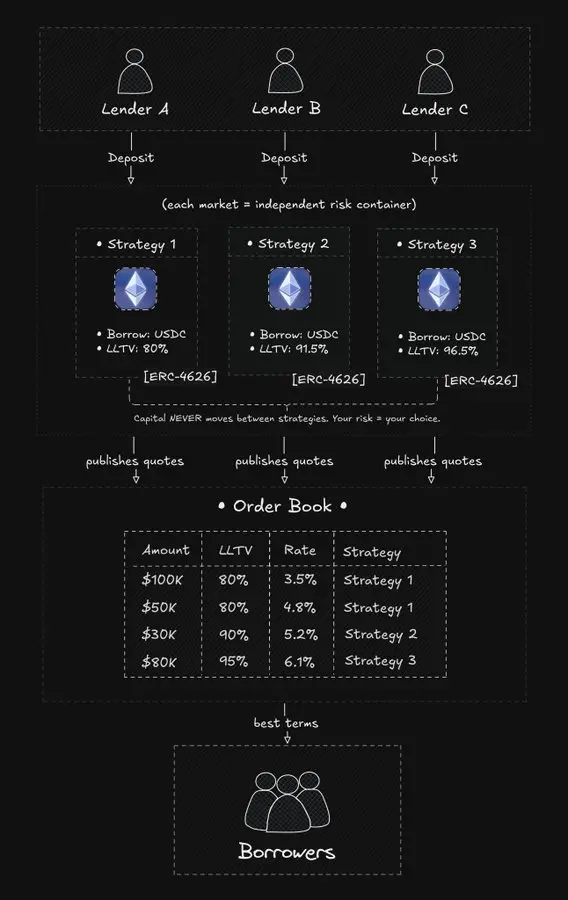

Two-Tier Architecture

Avon implements order book lending through two unique tiers.

Strategy Layer

A "Strategy" is an isolated lending market with fixed parameters.

The strategy creator defines the following parameters: Collateral/Borrowed Asset, Liquidation LTV, Interest Rate Curve, Oracle, Liquidation Mechanism.

Once deployed, the shape of the interest rate curve cannot be changed. Lenders know the rules exactly before depositing.

Funds never move between strategies.

If you deposit into Strategy A, your money stays in Strategy A until you withdraw. No curators, no rebalancing, no sudden changes in risk exposure.

Although someone (the strategy manager) sets the parameters, they are fundamentally different from a curator: Curators are capital allocators (deciding where money goes), strategy managers are true risk managers (defining rules but not moving money), analogous to Aave DAO. The decision-making power for capital allocation always remains with the lender.

How does the system adapt to market changes? Through competition, not parameter modification. If the risk-free rate soars, this forces old strategies to become obsolete (funds flow out), and new strategies are created (funds flow in). "Discretion" shifts from "where should capital go?" (curator's decision) to "which strategy should I choose?" (lender's decision).

Matching Layer

Strategies do not serve borrowers directly; instead, they post quotes to a shared order book.

The order book aggregates quotes from all strategies into a unified view. Borrowers see the combined depth of all strategies that accept their collateral.

When a borrower places an order, the matching engine:

Filters quotes by compatibility (collateral type, LTV requirements).

Sorts by interest rate.

Executes starting from the cheapest.

Settles within an atomic transaction.

If one strategy can fulfill the entire order, it takes it all; if not, the order is automatically split across multiple strategies. The borrower only perceives one transaction.

Important note: The order book only reads strategy states; it cannot modify them. It is only responsible for coordinating access, not allocating capital.

A Boon for RWA

DeFi has always faced a structural contradiction in institutional adoption: compliance requires isolation, but isolation kills liquidity.

Aave Arc tried the "walled garden" model, where compliant participants have their own pool. The result was shallow liquidity and poor rates. Aave Horizon tried a "semi-open" model (RWA issuers require KYC, but lending is permissionless). This is progress, but institutional borrowers still cannot access the $32 billion liquidity in Aave's main pool. Some projects explored permissioned rollups. The KYC process is completed at the infrastructure level. This approach works for some use cases but fragments liquidity at the network layer. Compliant users on Chain A cannot access liquidity on Chain B.

The order book model offers a third way.

The strategy layer can enforce any access control (KYC, geographic restrictions, accredited investor checks). The matching engine is only responsible for matching.

If a compliant strategy and a permissionless strategy both offer compatible terms, they can simultaneously fill the same loan.

Imagine a corporate treasury抵押代币化国债 borrowing $100 million:

$30 million from a strategy requiring institutional KYC (pension fund LPs)

$20 million from a strategy requiring accredited investor certification (family office LPs)

$50 million from a completely permissionless strategy (retail LPs)

Funds are never mixed at the source, institutions remain compliant, but liquidity is unified globally. This breaks the deadlock of "compliance equals isolation."

Mechanisms for Multi-Dimensional Matching

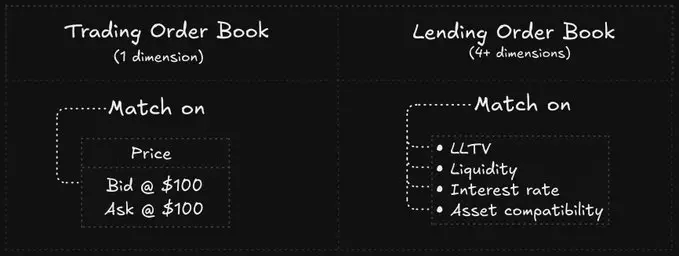

Order books match on only one dimension: price. The highest bid and lowest ask match.

Lending order books must match across multiple dimensions simultaneously:

Interest Rate: Must be below the borrower's acceptable上限.

LTV: The borrower's collateral ratio must meet the strategy's requirements.

Asset Compatibility: Currency match.

Liquidity: Sufficient market liquidity.

Borrowers who provide more collateral (lower LTV) or accept higher interest rates can match with more strategies. The engine finds the cheapest path within this constraint space.

A note for large borrowers. In Aave, $10 billion in liquidity is a monolithic pool. In order book lending, $10 billion might be分散在数百种策略中. A $100 million loan would quickly consume the entire order book, filling from the cheapest strategies first, progressively moving to the most expensive ones. Slippage is visible.

Pool-based systems also have slippage, just manifested differently: a surge in utilization pushes up interest rates. The difference is transparency. In the order book, slippage is visible upfront. In the pool, slippage only becomes apparent after the trade executes.

Floating Rates and Re-quoting

DeFi lending uses floating rates. As utilization changes, so does the interest rate.

This creates a synchronization challenge: if the strategy utilization changes but the quote on the order book isn't updated, the borrower executes at the wrong price.

Solution: Continuous re-quoting.

As soon as the strategy state changes, immediately post a new quote to the order book. This requires extremely high infrastructure performance:

Very fast block times.

Extremely cheap transaction costs.

Atomic state reads.

This is why Avon chose to build on MegaETH. On Ethereum Mainnet, this architecture is prohibitively expensive due to gas fees.

Existing friction:

If market rates move but the strategy's fixed curve doesn't adapt, a "Dead Zone" appears – borrowers find it too expensive to borrow, and lenders earn no yield. In Aave, the curve adjusts automatically, whereas in CLOB mode, this requires lenders to manually withdraw and migrate to new strategies. This is the price paid for control.

Multi-Strategy Position Management

When a loan is filled by multiple strategies, the borrower effectively holds a multi-strategy position.

Although it looks like one loan on the interface, the underlying components are independent:

Independent Interest Rates: Component A's rate might rise due to increased utilization in Strategy A, while Component B remains unchanged.

Independent Health Ratios: When the token price drops, components with stricter LTV limits are liquidated first locally. You don't get liquidated all at once but experience a series of partial liquidations, like being "nibbled away."

To simplify the experience, Avon provides unified position management (one-click add collateral, automatically distributed by weight) and one-click refinancing功能 (automatically borrow new to repay old via flash loans, always locking in the market's best rate).

Conclusion

DeFi lending has gone through several stages:

Pooled Protocols: Gave borrowers depth but剥夺了放贷人的控制权.

Isolated Markets: Gave lenders control but fragmented the borrower experience.

Curator Vaults: Attempted to bridge the two but introduced human decision-making risk.

Order Book Lending (CLOB): Decouples the above models. Risk definition rights return to lenders; matching is achieved through an order book engine.

The design principle is clear: when matching can be achieved through code, human intervention is no longer needed. Markets can self-regulate.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush