Author:Li Dan

Amid recent investor panic fueled by a series of product releases from Anthropic and Citrini's "doomsday report," the AI boom has withstood a direct test. NVIDIA delivered "explosive" earnings, proving that the demand generated by AI remains strong.

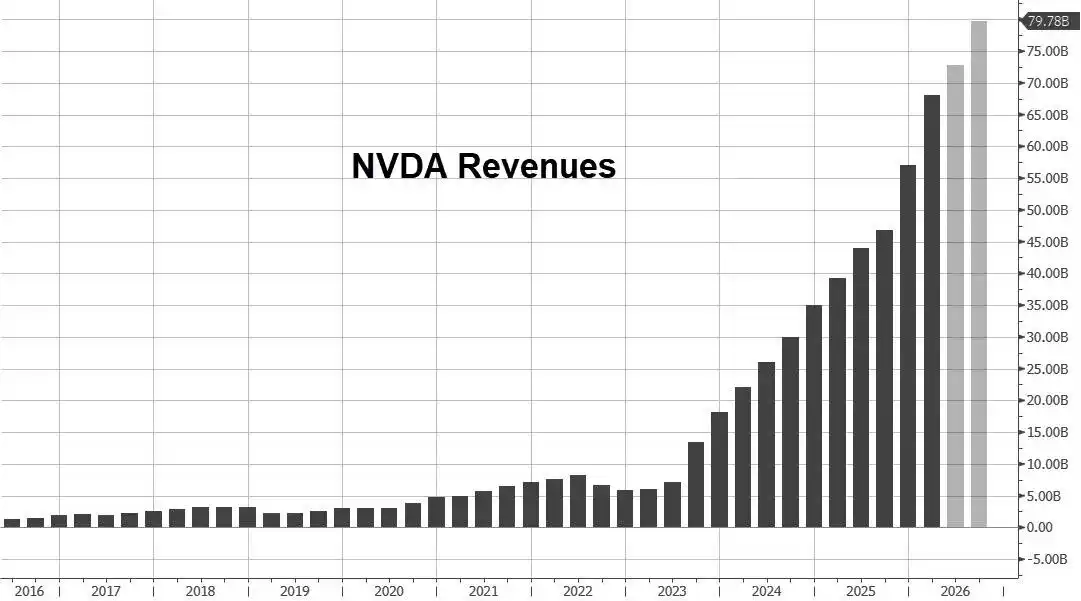

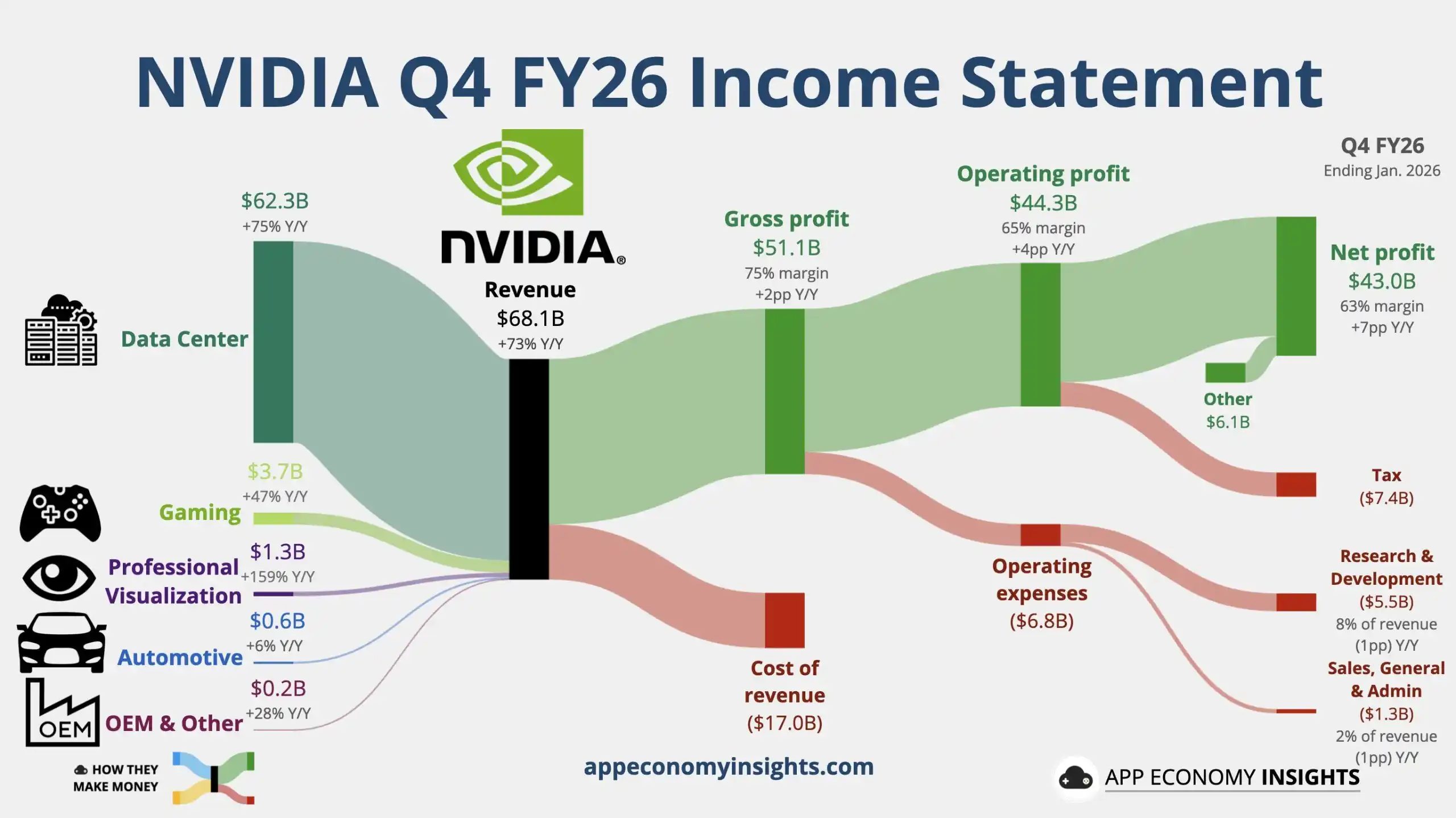

On Wednesday, February 25th, US Eastern Time, NVIDIA announced that for the company's fiscal fourth quarter ("Q4") ended January 31, 2026, revenue reached a record $681 billion, a surge of approximately seventy percent year-over-year. The core data center business, contributing over ninety percent of revenue, also set a new quarterly revenue record, both exceeding analyst expectations by over 3%.

NVIDIA's profitability in QQ4 was equally robust. On a non-GAAP basis, adjusted earnings per share (EPS) increased by over eighty percent year-over-year, approximately 5.9% higher than analyst expectations. The gross margin also climbed beyond expectations to 75.2%, reaching a new high in a year and a half.

Even more encouraging for investors was NVIDIA's guidance for the first quarter of fiscal year 2027 (Q1), which was stronger than expected. Revenue is expected to set another record high, with the midpoint of the guidance range being 7.1% higher than the analyst consensus midpoint and even 4% higher than the optimistic expectations of buy-side analysts. The year-over-year growth rate accelerated compared to QQ4 to nearly 77%. NVIDIA noted that this guidance excludes data center computing revenue from the China market.

During the earnings call this Wednesday, NVIDIA CEO Jensen Huang also raised the chip revenue forecast he had previously provided, stating, "We will exceed the $500 billion target. Supply will meet demand through next year and beyond." At the GTC conference last October, Huang revealed that NVIDIA had collectively received chip orders worth $500 billion for the calendar years 2025 and 2026, including the next-generation Rubin chip, which will begin mass production this year.

Huang stated that customers are racing to invest in AI computing. Computing demand is growing迅猛ly. The use of agents by enterprises is surging. He mentioned "space data centers," saying the current economics of space data centers are still "barren," but the situation will change over time.

After the earnings release, NVIDIA's stock price, which had already closed up over 1% on Wednesday, surged in after-hours trading, with gains rapidly widening to over 4%. Analysis suggests the key reasons the market bought into it were: Data center revenue and total revenue both exceeded expectations; the gross margin continues to improve as production of the new Blackwell architecture chips ramps up; and the guidance for the current fiscal quarter is even stronger despite excluding some China market revenue, reinforcing the narrative of resilient AI computing demand.

However, during the conference call, NVIDIA's stock price continued to give up its gains, turning negative in after-hours trading and falling over 1%. Some commentary noted that the stock's turn lower indicates investors were not impressed by the latest guidance, suggesting that market concerns about an overheated AI economy will continue to haunt NVIDIA. Other analysis pointed out that operating expenses continue to grow rapidly, and the inclusion of stock-based compensation (SBC) in non-GAAP metrics starting in Q1 may temporarily alter investors' perception of "profit growth."

Q4 Revenue Hits Quarterly Record, Gross Margin Reaches 1.5-Year High

NVIDIA's QQ4 revenue grew 73% year-over-year to $681.27 billion, a growth rate significantly higher than the previous quarter's 62% and exceeding NVIDIA's own guidance midpoint of $650 billion. Analysts had expected revenue of $659.1 billion, representing approximately 68% year-over-year growth. For the full fiscal year, NVIDIA's revenue also set an annual record, reaching $2,159.38 billion, a 65% increase compared to the previous year.

Gross margin was another highlight in QQ4: the non-GAAP gross margin was 75.2%, up 1.7 percentage points year-over-year and 1.6 percentage points sequentially, reaching the highest level since Q2 of fiscal year 2025. This exceeded the analyst consensus expectation of 74.7% and the optimistic expectation of 75.0%.

NVIDIA CFO Colette Kress interpreted this, stating that the year-over-year improvement in gross margin came from "reduced inventory charges," while the sequential improvement was related to the "improved product mix and cost structure" brought by the continued volume ramp of Blackwell chips.

However, for the entire 2026 fiscal year, the non-GAAP gross margin declined, falling from 75.5% in the previous fiscal year to 71.3%, a decrease of 4.2 percentage points year-over-year, indicating that full-year profit margins were still subject to structural disruptions during the platform transition and supply ramp phase.

Data Center: Compute Growth Stabilizes, Networking Accelerates

In QQ4, NVIDIA's Data Center business recorded revenue of $623.14 billion, a 75% increase year-over-year, with growth higher than the 66% in the previous quarter. Analysts had expected a near 70% year-over-year increase to $603.6 billion.

Within the Data Center segment, NVIDIA provided two sets of numbers that are even more noteworthy:

- Data Center Compute revenue was $513.34 billion, up 58% year-over-year, with growth slightly higher than the 56% in Q3.

- Data Center Networking revenue was $109.80 billion, up 263% year-over-year, far exceeding the 162% growth in Q3.

NVIDIA attributed the explosion in Networking revenue to: the launch and continued ramp of the NVLink compute fabric for GB200 and GB300 systems, coupled with continued growth in Ethernet and InfiniBand platforms.

In other words, the market should not only focus on the shipment pace of the GPUs themselves but also see that NVIDIA is packaging "computing power, interconnect, and systems" into an overall solution that is harder to replace. The high growth rate of Networking revenue is the financial reflection of this strategy.

Regarding customer structure, the company disclosed: In QQ4, revenue from hyperscale cloud providers accounted for slightly over 50% of the total Data Center business revenue, remaining the largest customer category. However, growth in the quarter came more from other data center customers, indicating a diffusion of revenue sources and a marginal mitigation of concentration risk.

Blackwell Drives Gaming Demand, Short-Term Disruptions from Supply and Channels

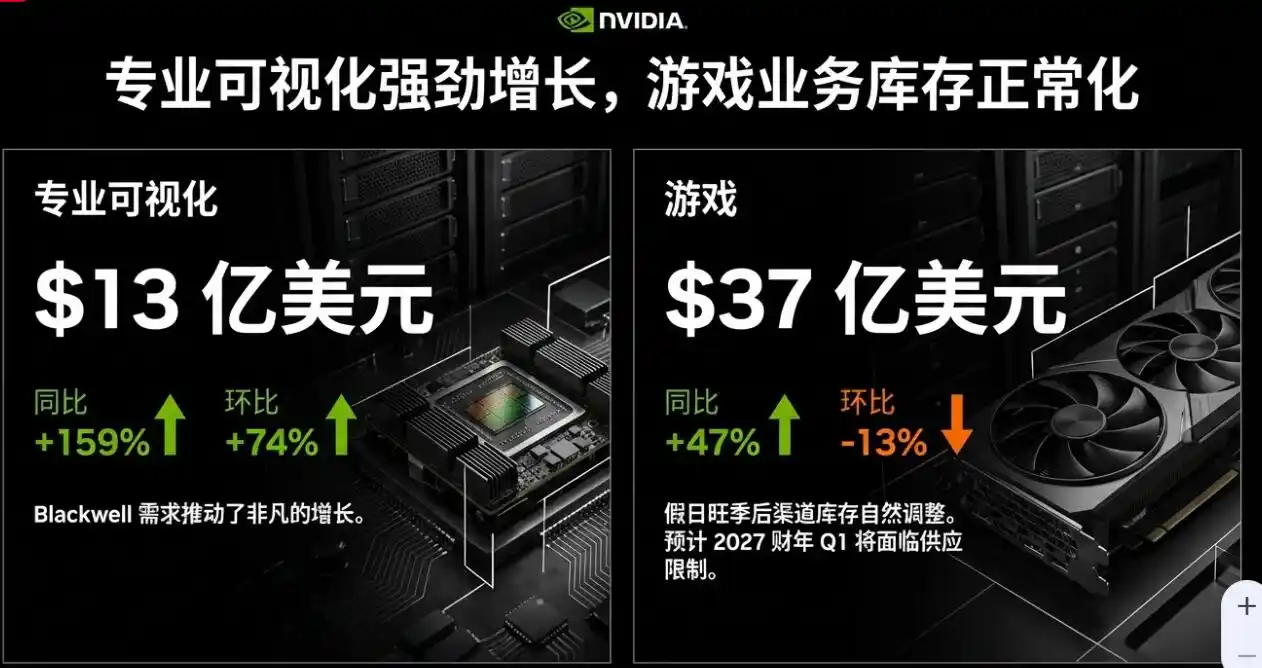

NVIDIA's Gaming business revenue in QQ4 was $37.27 billion, a 47% increase year-over-year. Analysts had expected $40.1 billion. The previous quarter saw 30% year-over-year growth.

The accelerated year-over-year growth in the Gaming business in QQ4 was explained by NVIDIA as primarily driven by strong demand for Blackwell chips. However, revenue for this segment decreased 13% sequentially due to a "natural post-holiday season channel inventory drawdown." Notably, NVIDIA explicitly warned: Supply constraints are expected to be a headwind for the Gaming business in Q1 and beyond.

Professional Visualization revenue in QQ4 was $13.21 billion, a 159% increase year-over-year. Analysts had expected $7.707 billion. The previous quarter saw 56% year-over-year growth.

Professional Visualization also saw revenue more than double year-over-year and grow 74% sequentially, driven by Blackwell, becoming one of the brightest incremental businesses besides Data Center. However, the scale of this business is far smaller than Data Center.

Q1 Revenue Guidance Midpoint Indicates ~77% YoY Growth, Excludes China Data Center Compute Revenue

Regarding performance guidance, NVIDIA announced that Q1 revenue is expected to be $780 billion, plus or minus 2%, i.e., $764.4 billion to $795.6 billion. This range implies that NVIDIA's revenue this fiscal quarter will refresh the record high set in QQ4.

Calculated using the revenue guidance midpoint, this means NVIDIA expects Q1 revenue to grow 76.9% year-over-year, further accelerating from the 73% growth rate in QQ4.

NVIDIA's revenue guidance midpoint is not only higher than the analyst consensus midpoint of $727.8 billion but also exceeds the buy-side's optimistic expectations of $740 to $750 billion.

NVIDIA's Q1 gross margin guidance is consistent with the optimistic expectations of Wall Street buy-side analysts, expected to reach a new high since Q2 of fiscal year 2025.

The Q1 non-GAAP adjusted gross margin is expected to be 75%, plus or minus 50 basis points, i.e., 74.5% to 75.5%. The buy-side optimistic expectation was 75%, and the sell-side consensus expectation was 74.7%.

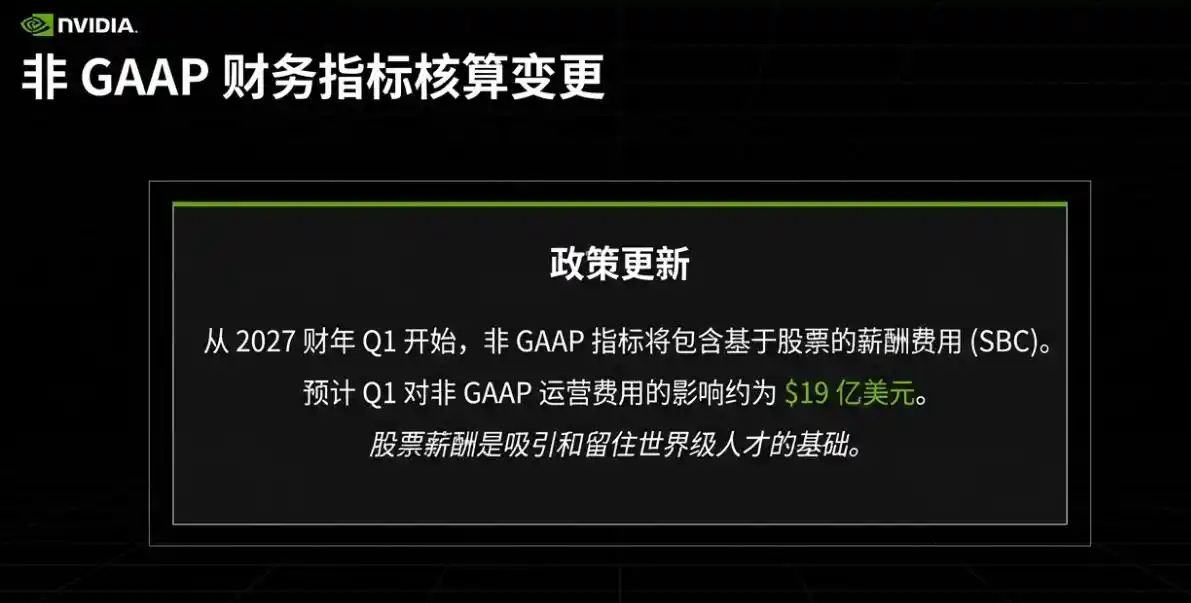

Stock-Based Compensation Included in Non-GAAP Starting Q1

Along with the earnings release, NVIDIA announced that starting in Q1, non-GAAP financial metrics will no longer exclude stock-based compensation (SBC). Due to this adjustment, NVIDIA estimates the impact on Q1 non-GAAP operating expenses will be approximately $19 billion.

This change will directly alter the "customary口径" that the market has long used for横向 comparing profit margins and expense ratios. In the short term, it may lead to a recalibration of consensus expectation models and will also allow investors to see more clearly the真实 cost NVIDIA incurs to maintain talent and R&D leadership.