Автор: Бао Илун

Источник: Wall Street News

Рациональность корпоративных расходов на ИИ подвергается серьёзной проверке: потребление токенов продолжает расти, в то время как измеримая бизнес-ценность остаётся неуловимой.

22 мая операционный директор Uber с рыночной капитализацией более 200 миллиардов долларов Эндрю Макдональд в подкасте публично заявил, что между ростом потребления токенов и реальным улучшением продукта «эта связь ещё не установлена».

Макдональд отметил, что компаниям становится всё труднее оправдывать постоянно растущие расходы на ИИ. Он даже придумал специальный термин для явления расточительства внутри инженерных команд: «токенмаксинг» (максимизация токенов).

Ранее, в середине мая, Microsoft под предлогом того, что счёта за токены «стали неприемлемыми», начала сокращать внутренние лицензии на Claude Code.

Совокупность этих двух событий заставила рынок серьёзно взглянуть на ранее игнорируемую переменную. Токеномика, то есть экономика потребления токенов в корпоративных масштабах, превратилась из маргинальной темы в ключевую опорную колонну всей дискуссии об инвестициях в ИИ.

Пять наборов данных, складывающихся в новую картину

С апреля было опубликовано несколько наборов данных, вместе рисующих тревожную картину.

В апреле этого года технический директор Uber публично заявил, что компания израсходовала годовой бюджет на Claude Code за четыре месяца.

Среди 5000 инженеров месячный уровень использования составил от 84% до 95%, а средний месячный счёт на человека варьировался от 150 до 2000 долларов. По сообщениям, сам технический директор в ходе двухчасовой внутренней презентации израсходовал токены на сумму 1200 долларов.

Макдональд заявил, что, услышав эту цифру, «был буквально ошеломлён».

Что касается Microsoft, то, согласно отчёту информационного бюллетеня Notepad Tома Уоррена из The Verge, Claude Code быстро завоевал популярность среди внутренних инженеров Microsoft, однако модель оплаты по потреблению токенов сделала крупномасштабные расходы неприемлемыми, и Microsoft немедленно приступила к сокращению соответствующих лицензий.

GitHub объявил, что с 1 июня все тарифные планы Copilot переходят с фиксированной подписки на оплату по потреблению.

Официальное обсуждение собрало почти 900 голосов против, поскольку, по расчётам пользователей, один сеанс программирования с ассистентом обычно потребляет токены на 30–40 долларов, что означает, что месячный пакет за 10 долларов можно исчерпать за один раз.

Платформа повышения продуктивности разработчиков Entelligence.AI, проанализировав данные 2444 компаний, обнаружила следующее:

- На каждый 1 доллар, потраченный на токены ИИ, только 18 центов создали реальную ценность, достигшую пользователей.

- 44 цента были потрачены на исправление ошибок, внесённых самим ИИ; 27 центов ушли на переделку работы; 11 центов были израсходованы на трение при проверке.

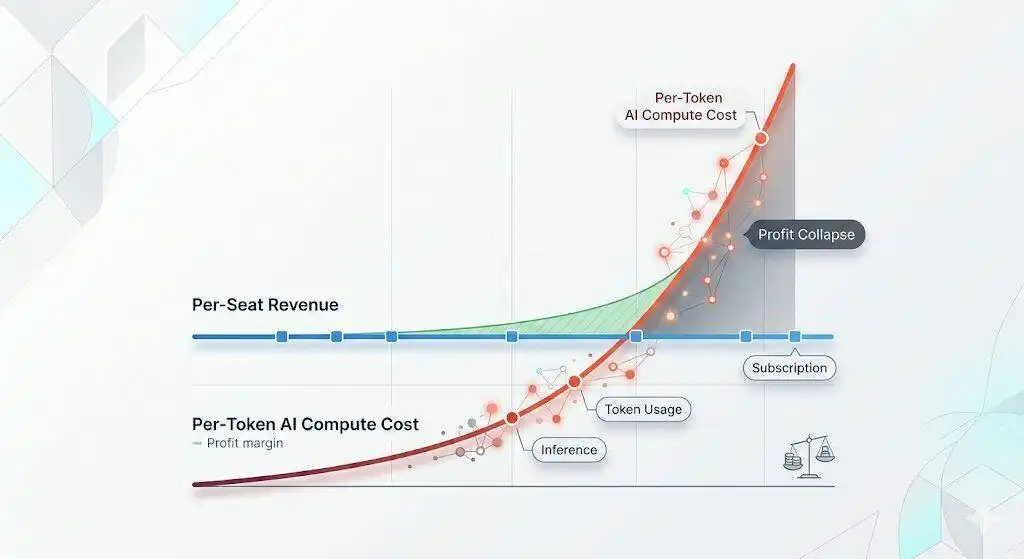

Согласно индексу расходов на токены LLM Silicon Data от Bloomberg, цена токена с конца февраля этого года выросла примерно на 65%, а цены на программное обеспечение ИИ в США за последний год выросли в общей сложности на 20–37%.

Битва быков и медведей: один факт, две интерпретации

Одни и те же данные в разных аналитических рамках указывают на совершенно разные выводы.

Быки считают, что нынешний хаос — это всего лишь болезненный переходный период успешной трансформации.

По оценкам Джима Шнайдера из Goldman Sachs, сделанным в начале мая, к 2030 году ИИ-агенты увеличат потребление токенов в 24 раза, примерно до 120 триллионов токенов в месяц, а валовая прибыль гипермасштабных облачных провайдеров и поставщиков моделей станет положительной в ближайшие 3–12 месяцев.

Рич Приворотски из Goldman Sachs считает, что первый квартал 2026 года, возможно, стал пиком использования «токенмаксинга» в качестве KPI, и отрасль переходит от стремления к объёму потребления к более здоровому измеримому параметру — «стоимости за единицу эффективного действия».

Экономические исследования JPMorgan также показали, что в начале 2026 года на PyPI наблюдался скачкообразный рост количества новых и обновлённых пакетов Python, тогда как эта тенденция не проявилась при запуске ChatGPT в 2022 году, что указывает на реальный рост производительности.

Кроме того, текущее отношение P/E Magnificent 7 составляет около 20 к будущей прибыли, что значительно ниже пика 52 во время пузыря доткомов в 2000 году, 67 в Японии в 1989 году и 34 в эпоху «Nifty Fifty». По стандартам измерения исторических пузырей текущая ситуация не является пузырём.

Медвежья точка зрения была наиболее систематически изложена в отчёте аналитика по полупроводникам Goldman Sachs Джима Ковелло в апреле.

Он отметил, что почти вся ценность в цепочке поставок ИИ перетекает к полупроводниковым компаниям, что беспрецедентно и неустойчиво в истории. Компании-производители чипов должны были бы получать выгоду, когда выигрывают их клиенты, однако в этом цикле их процветание достигается за счёт потребления ресурсов всеми звеньями верхнего потока цепочки.

Чистая прибыль NVIDIA с момента запуска ChatGPT выросла примерно в 20 раз; крупнейшие гипермасштабные облачные провайдеры уже израсходовали операционный денежный поток и прибегают к заимствованиям — объём выпуска долговых обязательств, связанных с центрами обработки данных, в 2025 году составил около 182 миллиардов долларов, что вдвое больше, чем в 2024 году.

Исследование MIT Nanda показывает, что 95% предприятий, инвестировавших в генеративный ИИ, получили нулевую отдачу. Такой разрыв может сохраняться какое-то время, но не может длиться вечно.

Проблемы циклической финансовой структуры

Эта дискуссия затрагивает и более сложный аспект: финансовый цикл между гипермасштабными облачными провайдерами и лабораториями ИИ.

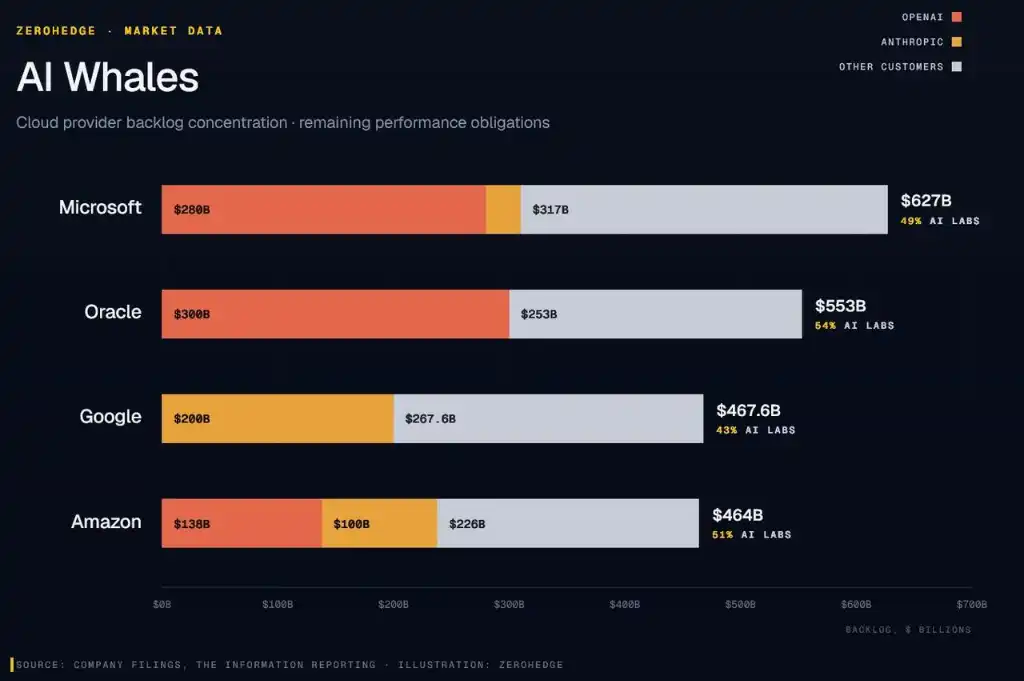

Согласно корпоративным документам, собранным The Information, на OpenAI и Anthropic вместе приходится более половины будущих облачных обязательств Microsoft, Oracle, Google и Amazon на сумму около 2 триллионов долларов. В частности:

- Из невыполненных заказов на облачные услуги Microsoft на 627 миллиардов долларов 280 миллиардов связаны с OpenAI;

- Из 553 миллиардов долларов потенциального бизнеса Oracle 54% (около 300 миллиардов долларов) обещаны OpenAI;

- Из 467,6 миллиарда долларов Google на Anthropic приходится 43% (около 200 миллиардов долларов);

- Соответствующая доля Amazon также достигает 51% от её невыполненных заказов на 464 миллиарда долларов.

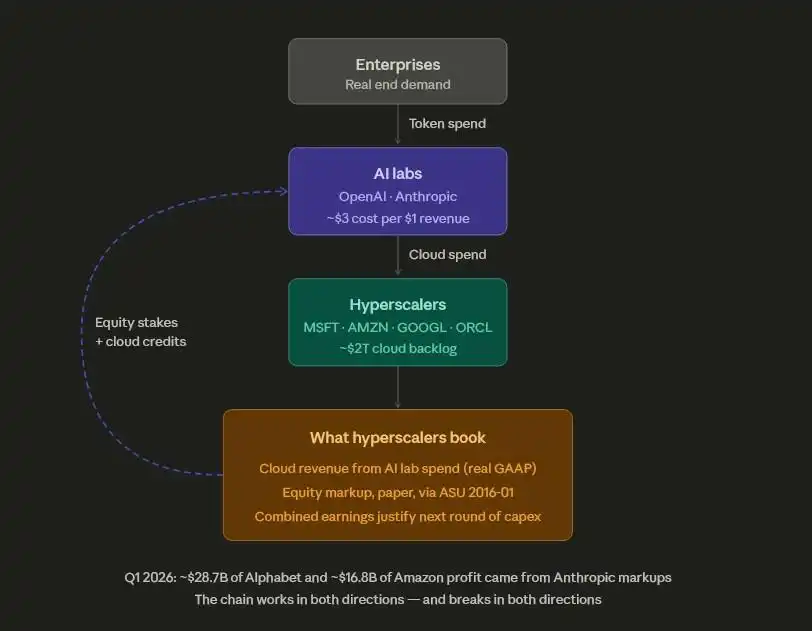

Эта финансовая структура имеет эндогенный циклический характер. Инвестиции Microsoft в OpenAI в размере 13 миллиардов долларов были осуществлены в основном в форме кредитов Azure, которые OpenAI использует для покупки вычислительных мощностей Azure, а Microsoft затем учитывает это как облачный доход.

Одни и те же гипермасштабные облачные провайдеры являются как акционерами-инвесторами лабораторий ИИ, так и поставщиками услуг, выставляющими счета за вычислительные мощности.

Эта структура также отражается в данных о прибыли. Alphabet объявила о рекордной прибыли за первый квартал в размере 62,6 миллиарда долларов, из которых около 28,7 миллиарда долларов, почти половина, пришлась на бумажное увеличение стоимости доли в Anthropic.

Из прибыли Amazon за первый квартал в размере 30,3 миллиарда долларов 16,8 миллиарда составили нереализованная прибыль до налогообложения от Anthropic, в то время как её свободный денежный поток, поскольку капитальные расходы на центры обработки данных в тот же период достигли 44,2 миллиарда долларов, рухнул на 95% до 1,2 миллиарда долларов.

Устойчивость этой системы зависит от способности лабораторий ИИ продолжать привлекать внешнее финансирование для выполнения облачных обязательств, что, в свою очередь, зависит от готовности корпоративных клиентов продолжать оплачивать растущие счета за токены.

По сообщениям, в настоящее время Anthropic тратит 3 доллара на каждый заработанный 1 доллар. Как только темпы финансирования замедлятся, надёжность прогнозов облачных доходов снизится, а мультипликаторы оценки гипермасштабных облачных провайдеров также окажутся под давлением переоценки.

Эта цепочка передаёт напряжение в обе стороны и также может разорваться в обе стороны.

Это не 1999 год, но проблема реальна

Текущая ситуация не является типичным пузырём.

С точки зрения мультипликаторов оценки, «Великолепная семёрка» в настоящее время торгуется с коэффициентом P/E примерно в 20 к будущей прибыли, что значительно ниже уровня 52 на пике пузыря доткомов в 2000 году, 67 на японском рынке в 1989 году или 34 в эпоху «Nifty Fifty».

Технология ИИ реальна. Для активных пользователей данные о росте производительности также поддаются проверке. Годовой доход OpenAI составляет около 20 миллиардов долларов, Anthropic — около 4,3 миллиарда долларов, и эти две лаборатории никуда не денутся.

Сегодня стоимость токенов (расходы на вычисления) стала ключевым фактором, определяющим успех ИИ, тогда как полгода назад об этой теме даже не говорили.

Тогда всех волновал только вопрос «работает ли технология». Теперь ответ ясен: для определённых задач и определённых людей технология действительно работает.

Но возникает новый вопрос: смогут ли сэкономленные предприятиями благодаря ИИ деньги достаточно быстро передаваться наверх, чтобы опередить окно оценки, оставленное рынком капитала для лабораторий ИИ и облачных гигантов?

Оптимисты в отношении ИИ считают, что по мере созревания технологий ROI (окупаемость инвестиций) предприятий может стать положительным в течение 1–1,5 лет.

Пессимисты же полагают, что всё больше руководителей, подобно Макдональду, будут публично жаловаться на низкую отдачу от инвестиций в ИИ и начнут сокращать бюджеты.

Оба сценария возможны, и исход ещё не определён. Единственное, что можно сказать наверняка, — это то, что ложь о том, что «если потребление токенов растёт, значит, трансформация ИИ проходит успешно», развеяна.

Большой объём потребления токенов не равен коммерческой ценности, и этот пузырь в конечном итоге придётся сдуть. Счёт за ИИ уже выставлен, но кто в итоге его оплатит? Пока это неизвестно.