Author: Seven Research

An elder colleague once recommended that I read Huang Zheng's "Turning Capitalism on Its Head." After the recommendation, I sought it out and read it, and jotted down some thoughts afterward.

Why bring it up now? Because many might find it hard to imagine that Huang Zheng—someone in e-commerce, famous for "low prices" and "help me cut the price"—could have anything to do with blockchain. Yet, after reading that article, I discovered there indeed is a connection, and it was pointed out by Huang Zheng himself.

I. The Underlying Logic of Pinduoduo: A Business About "Uncertainty"

First, let's talk about what this article is about.

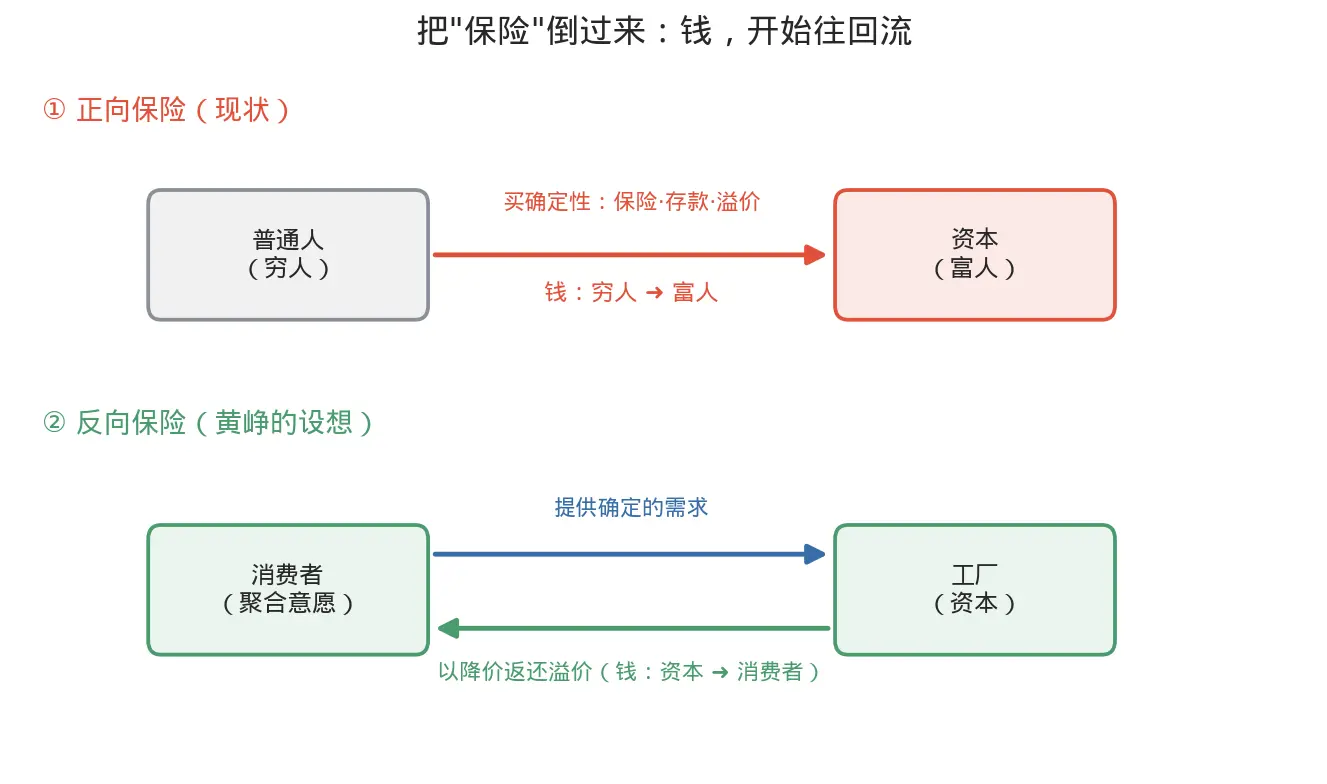

Most people see Pinduoduo and see cheapness, see targeting lower-tier markets. But Huang Zheng himself said that what he's actually doing is an "insurance" business—a business about "uncertainty."

He first poses a poignant question: Why does money always flow toward the wealthy?

His answer: Because the wealthy bear "uncertainty" for others. The probabilities of life's misfortunes—sickness, unemployment, major illness—striking anyone are roughly the same. But the same blow that might cripple a poor person is just a small, calculable fluctuation on a rich person's ledger. Thus, the poor are willing to spend money for "peace of mind"—buying insurance, depositing money in banks for meager interest, preferring to pay more for goods to get certainty. Money, bit by bit, flows from the bottom to the top. This is the "upright" way.

II. "Reverse Insurance": Turning Capitalism on Its Head

So, can it be turned upside down? Can ordinary people, in turn, sell "certainty" to capital?

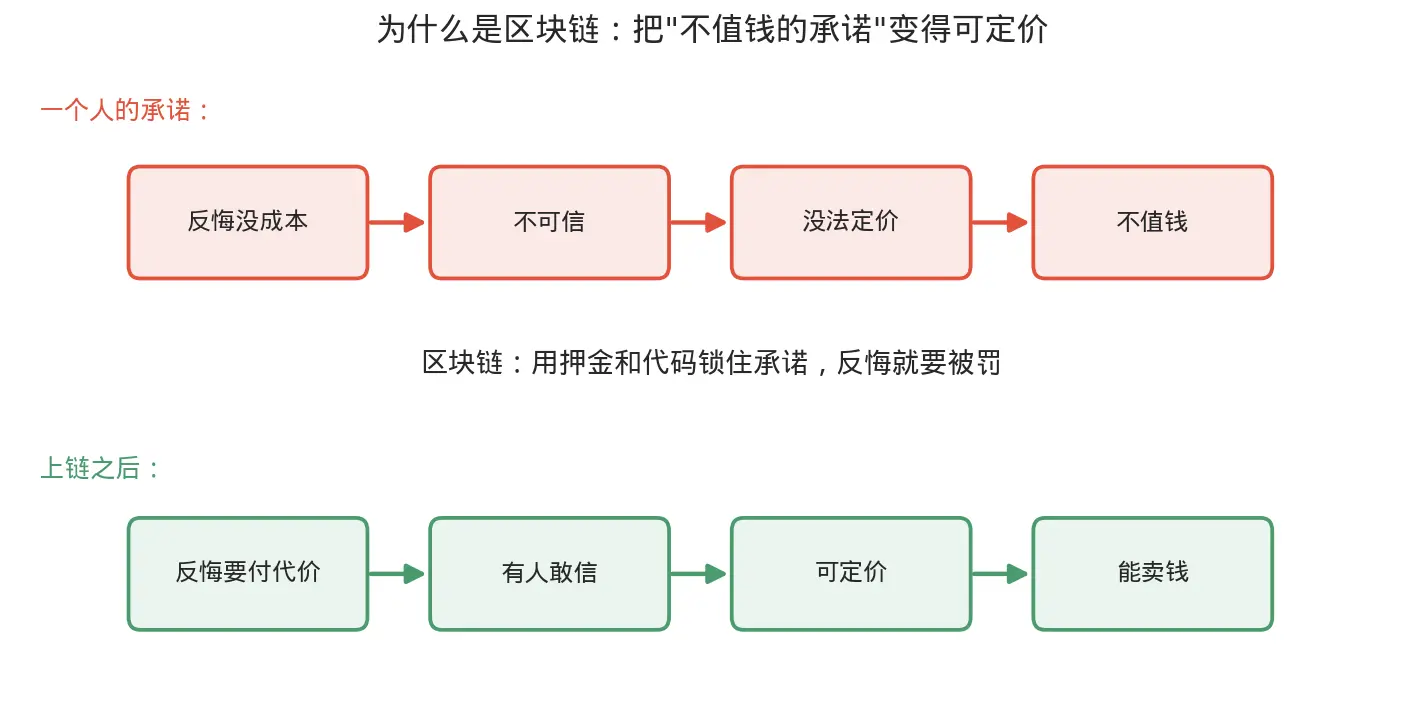

The difficulty lies in this: an individual's promise is worthless. You can cancel an online order anytime with zero cost to yourself; merchants have no recourse. They can only overstock, passing the cost back into the price. Huang Zheng puts it bluntly:

"Your action is treated as a statistical fluctuation, not as a promise that must be fulfilled."

But what if it's not one person, but ten thousand? Pinduoduo's group buying, flash sales—essentially, they catch you before you can hesitate, locking ten thousand people's "intention to buy" at the same moment, forcefully assembling a guaranteed order, eliminating the factory's risk of "producing and not selling." Grateful for this certainty, the factory converts the premium it would have set aside for risk into a "price reduction" returned to consumers. Money flows backward a notch. This is what he calls "reverse insurance."

III. The Final Puzzle Piece: Blockchain

By now, you might still not see the connection to blockchain. Honestly, I didn't either at first.

It's near the end of the article that Huang Zheng himself poses a question. He says that to productize, standardize, and monetize this kind of "certainty," a decentralized approach is needed to prevent fraud and create a virtuous cycle of good money driving out bad; then he asks: Isn't blockchain inherently designed for this kind of "reverse insurance"?

Just this one sentence made me pause. An e-commerce entrepreneur, after a long detour, lands the point squarely on blockchain. He doesn't elaborate further, but upon reflection, it makes perfect sense.

The biggest deadlock for reverse insurance, as mentioned, is that "an ordinary person's promise is worthless"—costless, untrustworthy, unpriced. And blockchain precisely cures this disease:

-

Use smart contracts to irrevocably bind your promise to a deposit. If you renege, the deposit is forfeited, and you face penalties.

-

This way, your "intention to buy" becomes, for the first time, a real promise with a cost to breaking it, a promise that can be enforced. Only then would the factory dare to believe it and arrange production accordingly.

Ultimately, it shifts the basis of "trust" from people to rules. You see, the missing puzzle piece he needed—making promises trustworthy, priceable, and immune to middleman fees—is exactly the inherent capability of blockchain.

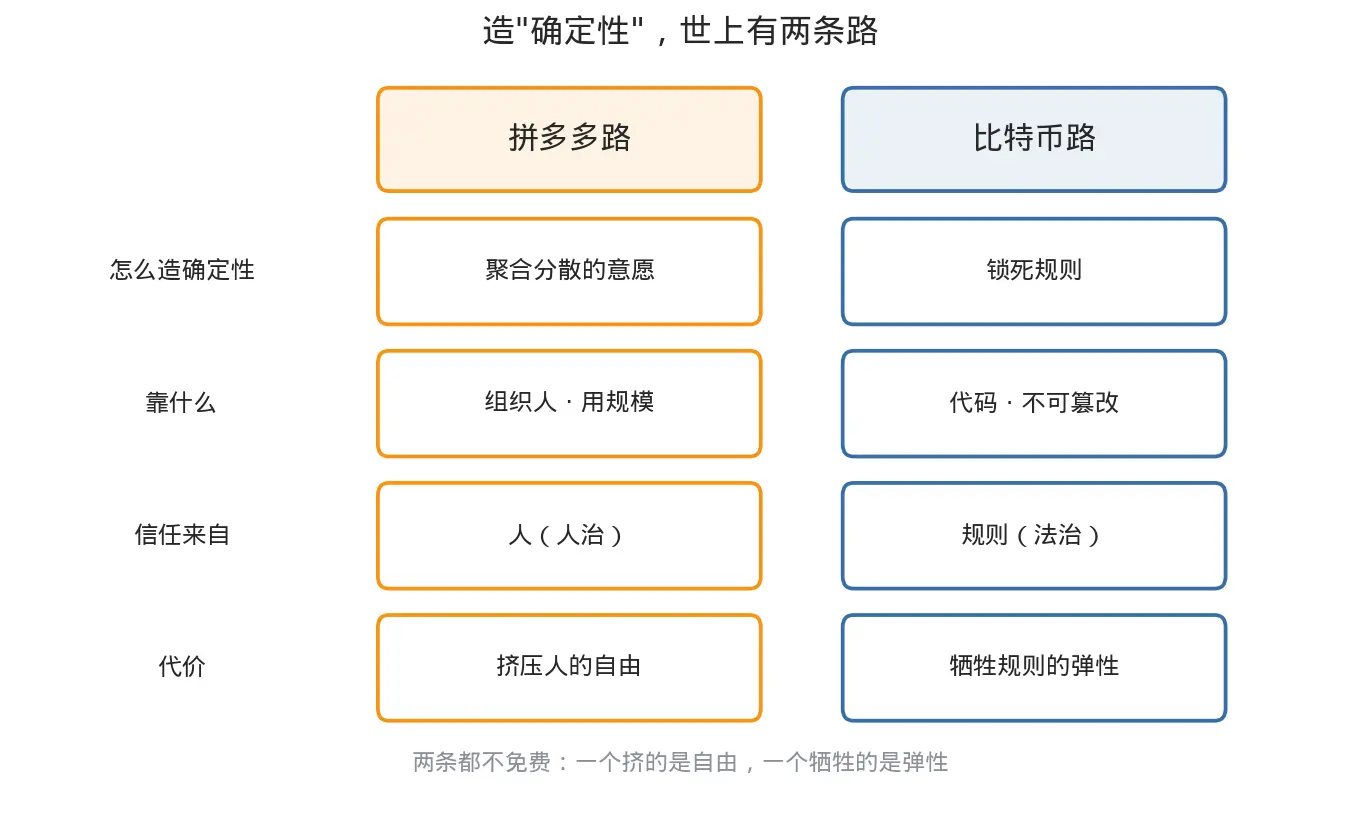

IV. Extended Thought: Two Paths to Creating Certainty

Following his question, I couldn't help but think one layer deeper about Bitcoin (an occupational hazard, forgive me for bringing crypto into this).

Bitcoin is essentially the purest example of "trusting rules": fixed supply, open-source algorithm, immutable rules.

-

The certainty of fiat currency relies on the restraint of the issuer; it's rule by man.

-

The certainty of Bitcoin relies on cold, impersonal, unfeeling code; it's rule by law.

One relies on people, the other on rules. So, there are actually two paths in the world to creating certainty:

-

The Pinduoduo path: Aggregate scattered intentions into momentum, using scale to forcibly flatten uncertainty.

-

The Bitcoin path: Lock the rules completely from the start, leaving no room for human discretion or intervention.

Neither path is free. The former squeezes human freedom; the latter sacrifices rule flexibility.

If you're interested, you can also re-read the article "Turning Capitalism on Its Head."