Биткоин сильно пострадал 5 февраля (падение на 13,2%), и мнение Джеффа Парка довольно прямое: это не было похоже на криптозаголовок. Это было больше похоже на традиционные финансовые механизмы: маржа, деривативы и механика ETF, проходящие через спотовые биткоин-ETF, с BlackRock's IBIT прямо в центре. Вот странная часть: потоки не показали крупных выкупов, которые вы обычно ожидали бы в такой день.

Почему биткоин рухнул 5 февраля?

Парк начинает с ленты ETF в своем посте в X от 7 февраля. IBIT, сказал он, показал рекордный объем — «в 2 раза выше предыдущего пика, 10 млрд+» — и опционы тоже сошли с ума, с количеством контрактов на максимумах с момента запуска. И в отличие от предыдущих всплесков интереса к опционам, он говорит, что на этот раз преобладали путы, основываясь на четком дисбалансе объемов.

Это время имеет значение. Это произошло как раз тогда, когда рынки повсеместно уходили от риска. Парк ссылался на prime brokerage desk Goldman Sachs, которая назвала 4 февраля одним из худших дней по производительности для мультистратегических фондов, около 3,5 z-score — basically a «0.05% event» в его формулировке. Когда это происходит, риск-менеджеры pod-шопов вмешиваются и говорят всем одно и то же: быстро сокращайте гросс. Парк описывает 5 февраля как вторую фазу этого вынужденного делевериджа.

Но данные о потоках не соответствовали очевидной истории. Он указывает на предыдущие просадки IBIT, когда действительно наблюдались реальные выкупы: примерно 530 миллионов долларов чистого оттока 30 января после падения на 5,8% и примерно 370 миллионов долларов 4 февраля во время серии проигрышей. В день с падением на -13% можно было бы ожидать оттока в размере 500 млн – 1 млрд долларов. Он этого не увидел.

Вместо этого Парк указывает на чистые создания: создано около 6 миллионов новых акций IBIT, что добавило примерно 230 миллионов долларов в AUM. И остальной комплекс спотовых биткоин-ETF также был чистым положительным — более 300 млн долларов. «Это немного озадачивает», — написал он. Его точка: вероятно, дело было не в одной вещи.

Сначала делеверидж, затем механика короткого гамма

Его главное утверждение: триггер не был крипто-нативным. «Катализатором распродажи стало то, что произшел широкомасштабный делеверидж по мульти-активным фондам/портфелям из-за того, что высокая отрицательная корреляция рисковых активов достигла статистически аномальных уровней», — написал он. По его мнению, это спровоцировало агрессивное снижение рисков, которое включало биткоин, даже если большая часть экспозура была предположительно «дельта-нейтральной»: базисные сделки, RV против крипто-акций и другие setup'ы, которые хеджируют дельту через дилеров.

После этого вступила в действие хеджирующая механика. «Этот делеверидж затем вызвал эффект короткого гамма, который усугубил движение вниз», — написал он, basically говоря, что дилерам пришлось продавать IBIT по мере обновления их хеджей. И поскольку это произошло так быстро, он считает, что маркет-мейкеры в итоге оказались в чистой короткой позиции по биткоину без реального управления инвентарем «обычным» способом. Это может приглушить то, что вы в противном случае увидели бы как большой отток из ETF на ленте.

Он также отмечает, насколько близко IBIT отслеживал софтверные акции и другие рисковые активы в недели, предшествовавшие падению. В его формулировке, распродажа, инициированная софтверным сектором, является более чистым спусковым крючком здесь: золото важно, конечно, но оно менее центрально для финансируемых мультистратегических сделок, о которых он говорит.

Один из твердых данных, на которые он опирается, — это базис CME. Используя набор данных, который он приписал главе исследований Anchorage Digital Дэвиду Лоуманту, Парк сказал, что ближний базис CME BTC подскочил с 3,3% 5 февраля до 9% 6 февраля — необычно большое движение с момента запуска ETF. Он интерпретирует это как вынужденный unwind базисной сделки крупными мультистратегическими шопами (продажа спота, покупка фьючерсов).

В качестве дополнительного топлива он упоминает структурированные продукты: нокауты и барьерные уровни. Не обязательно драйвер, но нечто, что может сделать быстрое движение более неприятным. Он ссылался на ноту JPM, оцененную в ноябре с барьером «прямо на 43,6», и утверждал, что если похожие ноты были выпущены позже, по мере снижения BTC, барьеры могли сгруппироваться вокруг «38–39».

Это та зона, где быстрая распродажа может превратить хеджирование в каскад. Если барьеры пробиваются, негативная ванна и быстро меняющаяся гамма могут заставить дилеров агрессивно продавать на слабости. Он также отмечает, что подразумеваемая волатильность почти достигла 90% в его описании.

Почему биткоин отскочил 6 февраля

Парк описывает «героическое восстановление более чем на 10%» 6 февраля как сброс позиционирования. Открытый интерес на CME расширялся быстрее, чем на Binance. Он говорит, что OI на CME рухнул с 4 по 5 февраля (поддерживая идею unwind базиса), затем восстановился, поскольку игроки снова leaned into относительно-стоимостные setup'ы.

По его словам, создания/выкупы ETF могут выглядеть довольно плоскими, если базисная сделка восстанавливается, даже если цена остается под давлением, потому что крипто-нативное кредитное плечо и экспозуры короткого гамма — часто на офшорных площадках — все еще очищаются.

В итоге, по его мнению: это, возможно, не было «фундаментальным» вообще. Это была техническая механика: снижение рисков по мульти-активам, затем петли обратной связи деривативов, усугубляющие ситуацию. Если приток в ETF продолжается без соответствующего расширения базисной сделки, он подразумевает, что это более чистый сигнал реального спроса, меньше ресайклинга дилерами, больше стабильных покупателей.

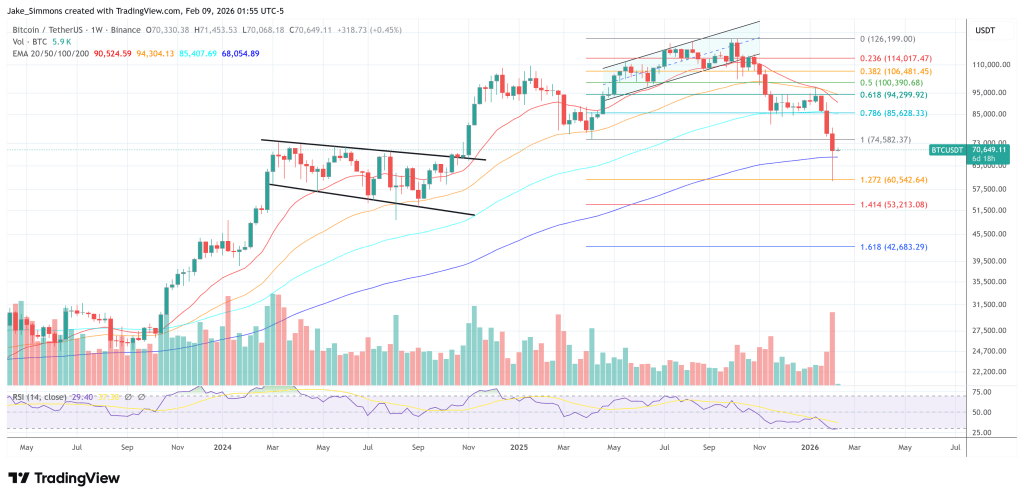

На момент публикации BTC торговался на уровне 70 649 долларов.