Автор оригинала: Ху Тао, ChianCatcher

В то время как криптоиндустрия становится все более мейнстримовой, китайские предприниматели, кажется, все дальше отходят от центра сцены.

Было время, когда проекты, основанные китайцами, занимали половину отрасли, включая такие известные криптовалютные биржи, как Binance, OKX, Bybit, Bitget, Gate, HTX, Bitmart, которые были созданы китайцами. В майнинге это еще более заметно: проекты like Bitmain, Canaan, Spark Pool занимали важные позиции в отрасли. Их общая черта в том, что все они были основаны в 2017-2018 годах или даже раньше.

Хотя Чжао Чанпэн, Сюй Минсин, У Цзихань и Сунь Юйчэнь до сих пор активно работают на передовой, после бума DeFi Summer 2020 года постепенно сформировался общий консенсус: видимость и влияние нового поколения китайских предпринимателей в глобальной криптоиндустрии снизились, и до сих пор не появилось лидеров, способных сравниться с предыдущим поколением. На этом фоне возникает вопрос: что произошло с экосистемой китайских предпринимателей? И где будущие возможности?

Регулирование и изменение геополитической среды: первый удар по экосистеме

За последние пять лет самым значительным фактором стали резкие изменения в регулировании и геополитической среде.

Начиная с 2021 года, Китай значительно усилил регулирование деятельности, связанной с криптовалютой: торговля, майнинг и другие сценарии, которые ранее находились в серой зоне, были быстро прекращены. В последние годы почти каждая популярная концепция на рынке получала предупреждение от регуляторов — от ICO, NFT и цифровых коллекций до недавних платежей и активов реального мира. Это, несомненно, в определенной степени ограничивает приток качественных ресурсов и поддержку китайской криптоэкосистемы.

Эти меры не только ускорили перемещение майнинга и биржевого бизнеса за рубеж, но, что более важно, лишили китайских предпринимателей本地льного рынка, который естественным образом обладал сетевым эффектом, плотностью талантов и концентрацией капитала, вынудив их переехать в незнакомую зарубежную среду.

В ранней криптоэкосистеме многие быстрорастущие китайские проекты набирали пользователей благодаря механизмам мобилизации в китайском интернет-сообществе: вирусное распространение через WeChat, сеть KOL, медиа-матрицы, оффлайн-встречи... Эти каналы были одними из самых эффективных систем распространения крипто-нарративов. Однако изменения в регулировании сделали эту систему практически нерабочей.

В результате центр власти в отрасли быстро сместился в сторону США и Европы — доминирование compliance, приток институционального капитала, растущая зрелость регуляторных框架 начали формировать отраслевой порядок, кардинально отличающийся от 2017-2018 годов. Новые нарративы, новое регуляторное поле и новая структура капитала天然更偏向英语市场与合规导向强的创业团队. Например,预测市场这种具有一定博彩性质的加密项目,就很难诞生在对博彩严厉监管的华语市场环境中.

В такой отраслевой среде новому поколению китайских предпринимателей также сложнее получить «доверие по умолчанию» от глобальных СМИ, регуляторов, инвесторов и пользователей, и по сравнению с аналогичными欧美项目, им приходится вкладывать больше средств и усилий в маркетинг, compliance и другие аспекты методом проб и ошибок.

Изменение предпочтений капитала: второй удар по экосистеме

Если нормативные и геополитические барьеры являются первым ударом, то «структурный сдвиг предпочтений» со стороны资本市场进一步 усугубляет маргинализацию китайских предпринимателей в новом цикле.

В нынешней отраслевой среде проекты,缺乏强大 VC 的资金与资源支持, оказываются в невыгодном положении в привлечении пользователей, листинге, нарративах и других аспектах. Китайские предприниматели изначально находятся в невыгодном положении на этапе финансирования.

Из-за слабых показателей альткоинов и значительного снижения ROI, китайские VC в последние 2-3 года大幅降低了投资频次,甚至完全停止. У китайских предпринимателей очень ограниченный выбор как в плане привлечения финансирования, так и путей выхода. По сравнению с欧美主导 VC, китайские проекты难言优势 из-за языковых и культурных различий, поэтому объем и количество финансирования, полученного китайскими проектами в последние годы,持续呈下滑趋势.

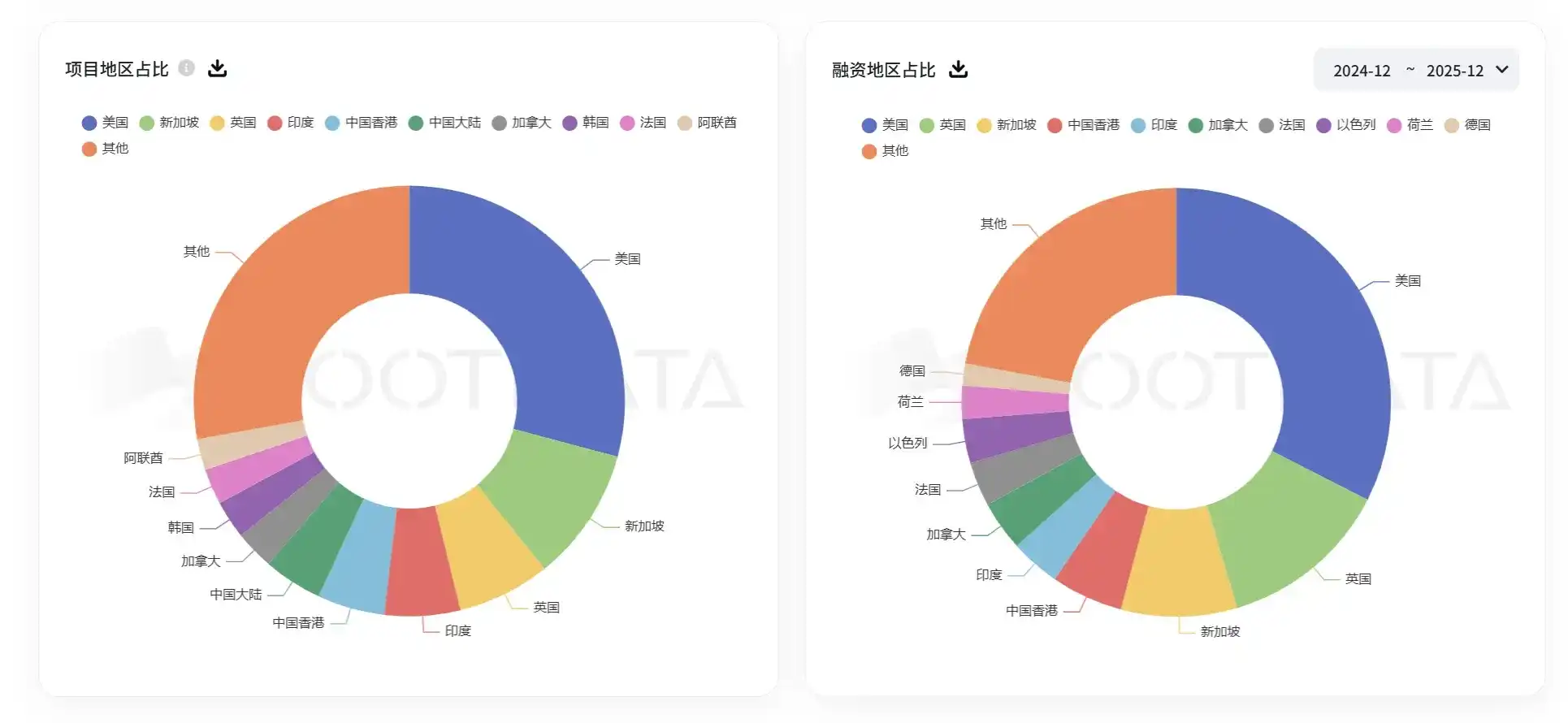

Доля проектов из материкового Китая по количеству и объему финансирования. Источник: RootData

В этом году в криптоиндустрии началась волна IPO и слияний/поглощений: Circle, Gemini успешно вышли на американский фондовый рынок, Coinbase, Ripple активно совершают поглощения — это значительно усиливает уверенность предпринимателей и даже VC, но все это基本都与华人项目无关. Можно сказать, что欧美项目正在享受加密行业主流化的制度性红利.

С точки зрения мейнстримного капитала,欧美项目具有天然优势 в compliance, культурной идентичности и путях выхода. Китайские проекты,除非 обладают исключительно сильной командой и технологическим бэкграундом,很难赢得欧美资本青睐.

Несоответствие структуры компетенций и зрелости отрасли: третий удар по экосистеме

За последнее десятилетие главным трендом криптоиндустрии一直 были инфраструктура и инструментальные направления. Хотя за это время появлялись новые концепции, такие как DeFi, NFT, игры,铭文, большинство из них не стали мейнстримными проектами.

В ранее данном ChainCatcher интервью основатель Folius Ventures Джейсон Кам (Jason Kam) отмечал, что развитие Web3 за последние 5-10 лет было закладкой фундамента, где более важными были категории и состояние продукта — это было десятилетие, смещенное в сторону экосистемы, инфраструктуры, инструментов и построения консенсуса. Другими словами, десятилетие B2B-продуктов.

В欧美 есть три поколения исключительно talented инженеров, очень擅长搭建这种 B2B 生态. В Азиатско-Тихоокеанском регионе в основном молодые инженеры 80-х и 90-х годов, чей профессиональный путь развития actually сопровождался большим подъемом китайской B2C-индустрии, начавшимся в 2005 году. Другими словами, их инженерный опыт лежит в области B2C и приложений, что格格不入 со всем процессом развития blockchain, поэтому они, возможно, плохо справляются с публичными блокчейнами и инфраструктурой.

«Если азиатско-тихоокеанские предприниматели будут соревноваться с欧美 предпринимателями на уровне To C, я считаю, что у азиатско-тихоокеанских предпринимателей нет никаких недостатков,甚至会有优势. Их преимущество заключается в极其丰富的产品经验 и в极具进攻性的抢占市场份额的落地打法.»

Хотя на более Web2-ориентированном方向 бирж китайские предприниматели уже доказали это, а в случае с C端 продуктами на链е кратковременный успех Stepn подтвердил天赋 китайских предпринимателей в C端 продуктах, общий взрыв рынка потребительских продуктов все не наступает, что тесно связано со зрелостью отраслевой инфраструктуры — рынок еще не достиг «зоны комфорта» китайских предпринимателей.

Предприниматели с мультикультурным бэкграундом становятся доминирующей силой в отрасли

Строго говоря, в последние几年 также не появилось новых репрезентативных кейсов китайских предпринимателей. Основатель Hyperliquid Джефф Ян (Jeff Yan) — этнический китаец, его родители иммигрировали из Китая, а он сам родился и вырос в Пало-Альто, Калифорния, затем поступил в Гарвардский университет, где изучал математику и computer science. После выпуска Джефф joined высокочастотный trading гигант Hudson River Trading в качестве quantitative trader. В 2022 году Джефф основал Hyperliquid и, благодаря философии «маленький, но精», без VC, рост driven пользователями, превратил его в одного из самых быстрорастущих гигантов криптоиндустрии за последние годы.

Однако, хотя Hyperliquid — один из самых успешных проектов этого цикла с «китайскими корнями», его很难将其视为延续 влияния китайских предпринимателей, поскольку он практически не активен в китайской экосистеме,在外界中塑造的几乎全是欧美价值观理念, и никогда не выражался на китайском. Восход Джеффа и Hyperliquid скорее подчеркивает факт, что в новом цикле китайское происхождение все еще может иметь глобальное влияние, но при условии интеграции в мейнстримную культурную систему, а не reliance на старые пути китайского предпринимательства. Если полагаться только на одну культурную систему, то можно стать лишь региональным лидером, но не достичь выдающихся результатов в процессе глобализации.

Фактически, основатели многих известных китайских проектов, ставших лидерами в своих направлениях в этом цикле, также имеют multicultural бэкграунд, по крайней мере, они учились в欧美 уже на университетском уровне, например, Шон Жэнь (Sean Ren), основатель Sahara, Ю Ху (Yu Hu), основатель Kaito, Эрик Чжан (Erick Zhang), основатель BuidlPad. Длительный опыт пребывания в欧美 играет важную роль в их development пути.

事实上, предприниматели с мультикультурным бэкграундом的确 более популярны в криптоиндустрии. Например, основатель Ethereum, основатель Solana и основатель Binance Чжао Чанпэн в детстве иммигрировали из Китая и России в北美 страны. Столкновение различных политических систем и культур позволило этим предпринимателям раньше осознать ценность blockchain в расширении прав и возможностей индивидуального суверенитета и быстро перейти к действиям. В формировании команды,对接 ресурсов, повседневной运营 они уделяют большое внимание культурной инклюзивности, что в конечном итоге также облегчает получение признания пользователей с разным культурным бэкграундом.

Сущностная характеристика крипто как безграничной отрасли и регулирование крипто, а также интересы разных стран —冲突与磨合 между этими двумя факторами будут в течение длительного времени определять trends развития криптоиндустрии. Китайские предприниматели на фоне множественных конфликтов между Китаем и США и мейнстримизации криптоиндустрии действительно сталкиваются со все большими вызовами. Но в近期, когда криптоиндустрия сталкивается с множеством质疑, связанных с склонностью к азартным играм, нигилизмом, и все больше проектных концепций оказываются опровергнуты, вопрос о том, как развивается ситуация с китайскими предпринимателями, возможно, уже не является важной отраслевой проблемой.真正值得关注的是: когда спекулятивный рост и叙事泡沫 постепенно спадают, кто还能持续投入 в долгосрочную ценность децентрализованных технологий и через реальные продукты и проверенные инновации重新定义方向 отрасли.

Ключевая конкурентоспособность будущей отраслевой格局 будет больше зависеть от того, обладает ли основательская команда способностью к межкультурному collaboration, долгосрочными технологическими инвестициями, а также пониманием регуляторной неопределенности и организационной resilience. Независимо от культурного или национального происхождения, те, кто способен persistently работать в этих измерениях,才有可能成为下一轮周期的真正受益者. Другими словами, путь к успеху в криптоиндустрии никогда не определялся тем, «откуда они», а тем, «что они могут сделать».