Автор оригинала: Nishil Jain

Компиляция: Block unicorn

Предисловие

В 1960-х годах индустрия кредитных карт была в хаосе. Банки по всей Америке пытались создать собственные платежные сети, но каждая сеть существовала сама по себе. Если у вас была кредитная карта Bank of America, вы могли использовать ее только у продавцов, сотрудничающих с Bank of America. А когда банки пытались расширить свой бизнес на другие банки, все платежи по кредитным картам сталкивались с проблемами межбанковского расчета.

Если продавец принимал карту, выпущенную другим банком, транзакция должна была рассчитываться через его первоначальную чековую расчетную систему. Чем больше банков присоединялось, тем больше возникало проблем с расчетами.

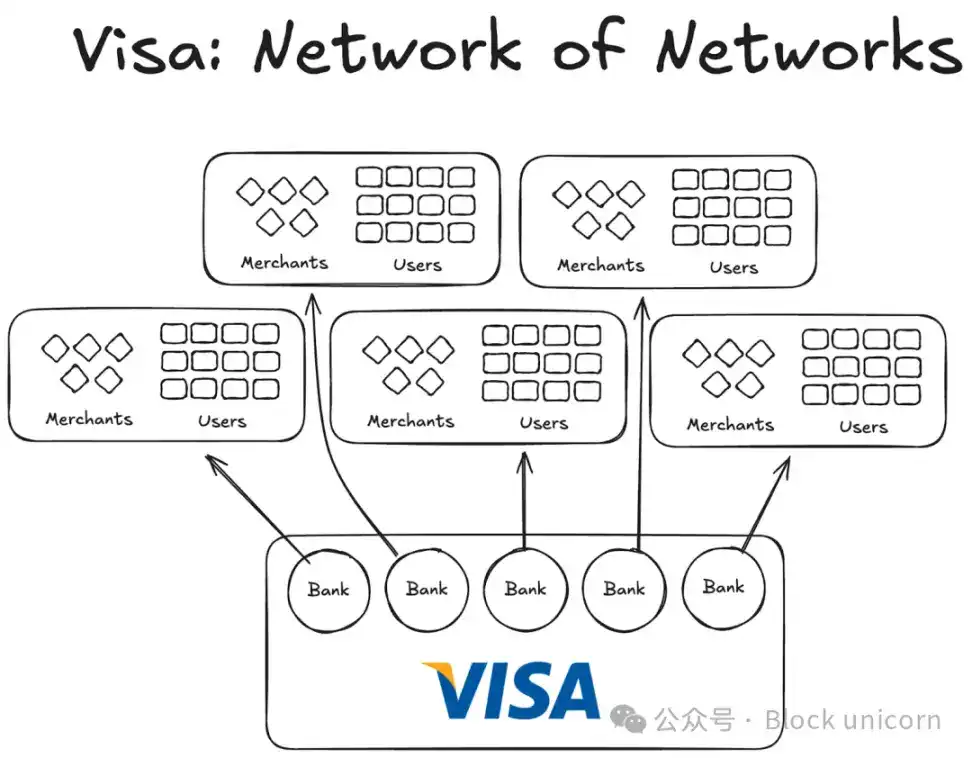

Затем появилась Visa. Хотя внедренные ею технологии, несомненно, сыграли огромную роль в революции платежей по банковским картам, более важным для успеха стала ее глобальная универсальность и то, с которым она смогла привлечь мировые банки в свою сеть. Сегодня почти все банки мира являются членами сети Visa.

Хотя сегодня это кажется совершенно нормальным, представьте, каково было убедить первую тысячу банков внутри и за пределами США, что присоединение к кооперативному соглашению, а не создание собственной сети, является разумным шагом, и вы начнете осознавать масштаб этого мероприятия.

К 1980 году Visa стала доминирующей платежной сетью, обрабатывая около 60% кредитных карточных транзакций в США. В настоящее время Visa работает более чем в 200 странах.

Ключом был не более передовая технология или больше денег, а структура: модель, которая могла согласовывать стимулы, распределять собственность и создавать сложные сетевые эффекты.

Сегодня стейблкоины сталкиваются с той же проблемой фрагментации. И решение, возможно, такое же, какое Visa применила пятьдесят лет назад.

Эксперименты до Visa

Другие компании, появившиеся до Visa, не смогли развиться.

American Express (AMEX) пыталась расширить свой бизнес кредитных карт как независимый банк, но ее масштабирование ограничивалось постоянным добавлением новых продавцов в свою банковскую сеть. С другой стороны, BankAmericard была другой: Bank of America владела своей сетью кредитных карт, а другие банки просто использовали ее сетевые эффекты и бренд.

American Express должна была обращаться к каждому продавцу и пользователю, чтобы они открыли банковский счет; в то время как Visa масштабировалась, принимая в себя банки: каждый банк, присоединившийся к кооперативной сети Visa, автоматически получал тысячи новых клиентов и сотни новых продавцов.

С другой стороны, у BankAmericard были проблемы с инфраструктурой. Они не знали, как эффективно рассчитывать транзакции по кредитным картам с одного потребительского банковского счета на другой торговый счет. У них не было эффективной расчетной системы между собой.

Чем больше банков присоединялось, тем хуже становилась эта проблема. Так появилась Visa.

Четыре столпа сетевого эффекта Visa

Из истории Visa мы узнаем о 2-3 важных факторах, которые привели к накоплению ее сетевого эффекта:

Visa выиграла от своего статуса независимой третьей стороны. Чтобы гарантировать, что ни один банк не почувствует угрозы конкуренции, Visa была разработана как кооперативная независимая организация. Visa не участвует в борьбе за долю распределения, за долю борются отдельные банки.

Это стимулировало участвующие банки бороться за большую долю прибыли. Каждый банк имел право на часть общей прибыли, пропорциональную общему объему обрабатываемых им транзакций.

Банки имели право голоса в функциях сети. Правила и изменения Visa должны были голосоваться всеми заинтересованными банками и требовали 80% голосов "за» для принятия.

Visa имела эксклюзивные条款 с каждым банком (по крайней мере, изначально); любой, кто присоединялся к кооперативу, мог использовать только карты и сеть Visa, а не присоединяться к другим сетям — поэтому для взаимодействия с банками Visa вам также нужно было быть частью их сети.

Он должен был объяснить, что присоединение к Visa означает, что больше пользователей и больше продавцов подключатся к одной сети, что будет способствовать увеличению количества цифровых транзакций по всему миру и принесет больше выгод всем участникам. Он также должен был объяснить, что если они создадут свою собственную сеть кредитных карт, их пользовательская база будет очень ограничена.

Откровение для стейблкоинов

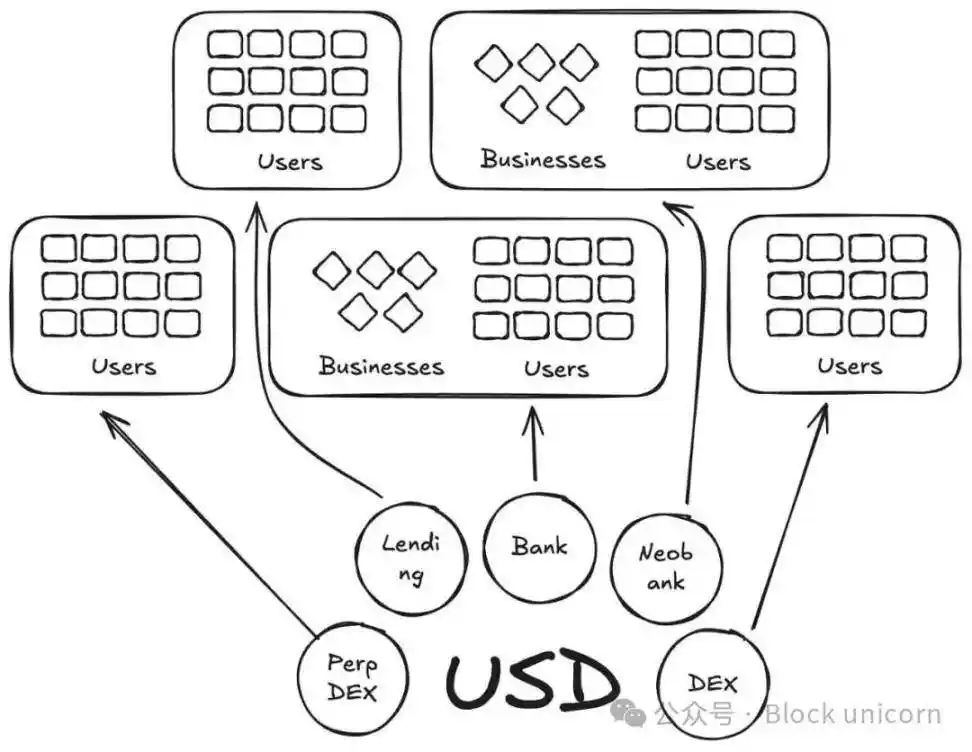

В некотором смысле, Anchorage Digital и другие компании, которые сегодня предлагают стейблкоин как услугу (stablecoin as a service), повторяют историю BankAmericard в сфере стейблкоинов. Они предоставляют новым эмитентам базовую инфраструктуру для создания стейблкоинов, в то время как ликвидность постоянно рассеивается по новым токенам.

В настоящее время на платформе Defillama уже запущено более 300 стейблкоинов. И каждый новый созданный стейблкоин ограничен своей собственной экосистемой. Следовательно, ни один стейблкоин не может генерировать сетевой эффект, необходимый для выхода в мейнстрим.

Если одни и те же базовые активы поддерживают эти новые монеты, зачем нам нужно больше монет с новым кодом?

В нашей истории с Visa они похожи на BankAmericards. Ethena, Anchorage Digital, M0 или Bridge — каждый из них позволяет протоколу выпускать свой собственный стейблкоин, но это только усугубляет фрагментацию отрасли.

Ethena — это еще один подобный протокол, который позволяет передавать доход и настраивать свои стейблкоины под белую маркировку. Как MegaETH выпустил USDm — они выпустили USDm с помощью инструментов, поддерживающих USDtb.

Однако эта модель провалилась. Она только фрагментирует экосистему.

В случае с кредитными картами брендовые различия между разными банками не имели значения, поскольку они не создавали трения в платежах от пользователя к продавцу. Базовый уровень выпуска и платежей всегда был Visa.

Однако для стейблкоинов это не так. Разные коды токенов означают бесконечное количество пулов ликвидности.

Продавцы (или, в данном случае, приложения или протоколы) не будут добавлять все стейблкоины, выпущенные M0 или Bridge, в свой список принимаемых стейблкоинов. Они будут решать, принимать их или нет, основываясь на ликвидности этих стейблкоинов на открытом рынке; монеты с наибольшим количеством держателей и наибольшей ликвидностью должны приниматься, остальные — нет.

Путь вперед: модель Visa для стейблкоинов

Нам нужны независимые第三方 организации для управления стейблкоинами различных классов активов. Эмитенты и приложения, поддерживающие эти активы, должны иметь возможность присоединиться к кооперативу и получать доход от резервов. В то же время они также должны иметь право управления, голосуя за направление развития выбранного ими стейблкоина.

С точки зрения сетевого эффекта, это была бы превосходная модель. По мере того, как все больше эмитентов и протоколов присоединяются к одной и той же монете, это будет способствовать широкому применению токена, который может сохранять доход внутри, а не отдавать его в карманы других.