Author | Golem (@web 3_golem)

In the A-share market, the "White-Haired Stock God" Serenity has completely gone viral.

From June 5th to June 9th, Serenity successively "shilled" three A-shares on platform X. They were the embodiment intelligence robotics concept stock LeaderDrive, the digital intelligence new energy concept stock Yashi, and the leading optical module stock Innolight. The stock prices of the first two were vertically pulled to a 20cm limit-up on the same day, and LeaderDrive has already risen over 30% in June.

The reason Serenity possesses such strong "pumping power" is because before entering the view of domestic A-share investors, he had already gained extremely high popularity in international retail investor communities.

Serenity's investment characteristic is using the "Chokepoint Investment Method" to screen out small monopolistic companies in the AI industry chain that are not fully priced in. Because the over 16 stocks he has shilled this year have all achieved investment returns exceeding 100%, and his personal year-to-date investment return exceeds 3612%, coupled with his professional background as a former AI research scientist and his rigorous analysis of the AI industry and favored companies each time, Serenity has accumulated a large number of loyal retail followers in Europe, America, Japan, and South Korea. His X account subscribers exceed those of Musk, ranking first on the platform. Therefore, his influence on a single stock's price fluctuation surpasses that of ordinary stock analysts.

For example, on May 27th, Serenity posted on platform X announcing he had completed building a position in the European stock XFAB at a market cap of $1.28 billion. XFAB's stock price was subsequently pushed up continuously, with a single-day intraday maximum increase of 77%, and the stock price rose to a high of 13.13 euros. Since then, XFAB's stock price began a continuous decline and is currently trading around 8.8 euros, having returned to pre-shill levels.

Just the day after causing significant volatility in XFAB's stock price, Serenity posted in Chinese on platform X, saying, "Because I see so much support from the Chinese community... I might, just for fun, start writing about my views on a couple of Chinese stocks."

A storm of blood and rain sweeping the A-share market thus began.

Disrupting the A-Share Market Without Holding Positions, Just for Fun?

In hindsight, these two stocks Serenity mentioned were LeaderDrive and Yashi.

On June 5th, Serenity posted in Chinese, specifically emphasizing "written specifically for my Chinese readers," stating that LeaderDrive (688017, 57.73 billion RMB) was his most favored Chinese listed target when positioning in the humanoid robotics sector. The main reason is its absolute dominance in certain robot component supply chains, with over 60% domestic market share and more than 1,800 global customers.

As of now, this post has been viewed over 4 million times and has been disseminated to multiple domestic social media platforms. LeaderDrive's stock price triggered a 20% limit-up on June 5th. By June 10th, in just 4 trading days, the stock price had risen over 30%.

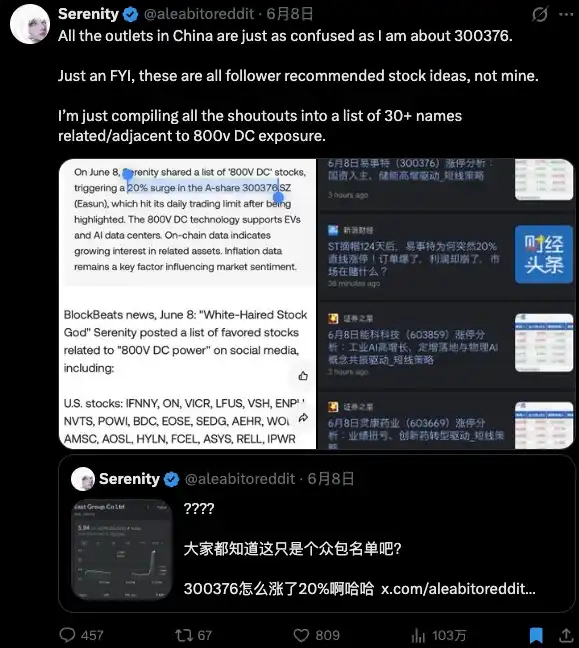

On June 8th, the same market script played out again. Serenity posted a crowdsourced list of over 30 companies in the "800V DC" concept on platform X, which included the A-share company Yashi. The news quickly fermented domestically, with Yashi's stock price happily receiving a 20CM limit-up within an hour, and by June 10th, its increase also exceeded 30%.

Serenity himself even seemed surprised, posting, 'Does everyone know this is just a crowdsourced list? How did 300376 (Yashi) go up 20%?'

Immediately after, he posted again saying, 'These are stocks recommended by fans, not my personal recommendations,' attempting to distance himself from it.

Besides these two stocks, Serenity also mentioned a third A-share, Innolight, on June 9th, stating it was the only Chinese listed company he invested in last year. However, because some AI mistranslated "Innolight" as another A-share listed company, Inno Laser, this caused Inno Laser to be violently pumped nearly 10% within 10 minutes. This "misunderstanding incident" also reveals the retail investors' FOMO towards Serenity himself—"blindly, just asking what to buy, afraid of missing out on the hot stuff."

Serenity's actions quickly drew the attention of domestic financial media and securities analysts, who began speculating about his purpose for "cross-border stock promotion." On June 9th, Cailian Press published a lengthy article warning domestic investors to be wary of overseas information flowing back in. If Serenity's sharing involved profit-sharing, the behavior would be classic "export-for-domestic-sale style cross-border pumping," requiring legal accountability. Some domestic securities analysts even openly vented on social media, "These clowns will be finished sooner or later, thinking they can act lawlessly just because they ran abroad."

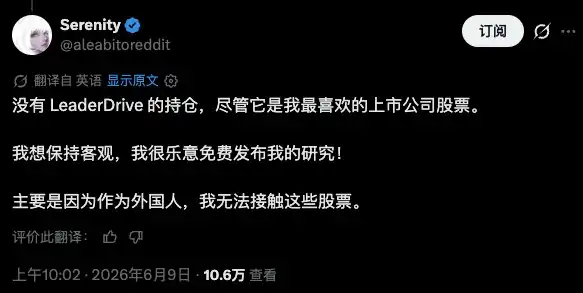

Facing domestic media's questioning about him "harvesting retail investors," Serenity responded that shilling A-shares was just because he thought "foreigners could bring a different perspective to A-shares." He also stated, "Although I really like LeaderDrive, I do not hold its stock." Perhaps, as he initially said, the original intention behind all this was just for fun.

Serenity appears almost like a "philanthropist." He emphasizes he does not do any paid promotions or marketing. The only paid thing is a $1 monthly subscription service. He is not a member of any institution or the Illuminati. The reason for his continuous free sharing is his belief that the stock market is a positive-sum game. He hopes retail investors can buy quality stocks without joining any expensive paid communities, even before institutions enter. He claims he is promoting information democratization.

In the investment field, don't overly deify anyone. Serenity may not seek profit, but he certainly seeks fame. Since starting to shill A-shares on June 5th, Serenity's follower count has surged again by over 200,000. As of June 11th, his X platform followers exceed 8.1 million, and account subscribers have grown to 54,000, surpassing Musk (46,000). With such a massive number of subscribers, even at $1, Serenity's fixed monthly income reaches $54,000, easily earning over a million RMB annually.

Serenity's pinned posts celebrate his account subscriber count surpassing Musk, calling it his goal. The fact that an anonymous account can have such high influence and attention makes investors even more curious about his real identity. Behind this account, is it a person, a team, or even just an AI?

Most Likely a Chinese National Living in Japan?

Serenity explains that his reason for remaining anonymous is to be able to freely express ideas online. He stated that when he first published negative views about IREN (a Nasdaq-listed stock), he received threats and harassment from dozens of accounts in real life, which is why he continues to remain anonymous.

Nevertheless, the community has gradually pieced together an image of Serenity from various collected fragments of information. It is highly likely he is a Chinese national living in Japan.

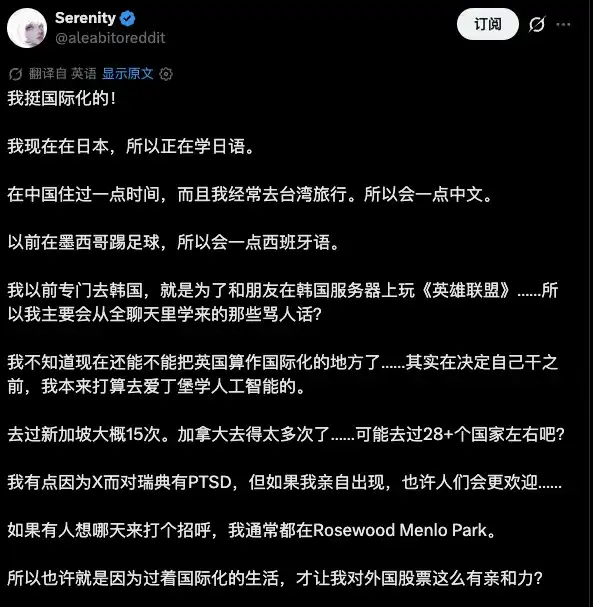

At the end of May, Serenity revealed some personal information. He said he is quite international, currently studying Japanese in Japan. Because he once lived in mainland China for a period and often traveled to Taiwan, he knows a bit of Chinese. Additionally, he played football in Mexico for two or three years, went to South Korea specifically to play League of Legends... his life seems quite comfortable.

Serenity has lived in Japan for at least half a year. At the end of 2025, he often posted photos of his life in Japan on platform X, but since becoming popular, he rarely mentions personal life.

Serenity in Japan

Serenity is a high-frequency poster, averaging 9~10 posts per day, peaking at over 20. Looking at his daily posting frequency using AI statistics, he has about 5 hours of absolute account silence each day. This silence period is likely when Serenity is resting or sleeping. This timeframe corresponds roughly to the early morning hours (3:00 to 8:00) in some Asian time zones (UTC+8, UTC+9). Combined with the previous information, this basically locks Serenity's location to Japan.

The community leans towards thinking Serenity is a Chinese national, but Serenity emphasizes English is his native language. Most of his posts are still in English. Occasional posts in Chinese seem only to cater to Chinese fans. Moreover, if you count posts in different languages, his Japanese post count is higher than his Chinese.

Combining this with Serenity's early experiences—active on Reddit WSB (Odaily Note: Wall Street Bets is the largest US retail trading community) before moving to X, rejected an offer from Nvidia's AI team in 2018, and was reported by overseas renowned media like Bloomberg and Reuters—it is therefore possible to basically rule out Serenity being a Chinese citizen.

Serenity's anonymous identity, non-transparent investment returns, and excessive craving for influence are all increasing market controversy around him. But interestingly, everyone who questions him is also constantly refreshing his homepage.

Stock investment has always seen different idols in different eras: Warren Buffett, Cathie Wood, Roaring Kitty. Each era has its own spiritual totem. Bull markets magnify returns and also magnify faith. When more and more people start making money, we always want to find someone who can "scientifically explain the bubble." Serenity might just be the outward projection of this round of AI bull market sentiment—mysterious, professional, successful, fitting all the public imagination of a "stock god."

But next to the altar is the guillotine, because when the market turns, it will want to find someone to blame for the losses, and Serenity might then be the most suitable candidate. History repeats, the market moves forever forward, people enjoy creating idols and are also adept at "destroying idols." As for who Serenity really is, it probably isn't that important anymore.