Автор: Ба Сяолин, Канал У Сяобо

«Самолет с 'Иерусалимом фондового рынка' летит к нам».

Вечером 13 мая официальная делегация президента США прибыла в столичный международный аэропорт Пекина.

В глазах инвесторов приземлился самый горячий бычий рынок ИИ.

Вместе с Трампом прибыли главы 17 американских компаний. Совокупная рыночная стоимость их компаний превышает 10 триллионов долларов, что составляет более одной пятой фондового рынка США, эквивалентно перевозке половины американской экономики.

Такие знакомые лица, как Дженсен Хуанг и Илон Маск, само собой разумеются. В этой поездке также присутствуют представители самых горячих на Уолл-стрит компаний по производству аппаратного обеспечения для ИИ.

Например, генеральный директор Micron Technology Санджай Мехротра. На фоне спроса на память для ИИ акции Micron выросли более чем на 320% за последний год. Еще один пример — Джим Андерсон, чья компания Coherent Corp. является представителем «концепции оптической связи» на американском фондовом рынке, и ее акции также удвоились в цене за этот год.

Дженсен Хуанг и Илон Маск прибыли в Пекин с Трампом

Другими словами, в этой команде стоят не только Трамп — «король свечей», но и все «твердые быки» американской индустрии ИИ.

Фондовый рынок США также способствовал этому событию. В ту ночь индексы NASDAQ и S&P 500 достигли исторических максимумов, при этом акции Tesla выросли более чем на 2%, а Nvidia и Apple — более чем на 1%, две последние крупные компании также достигли своих предыдущих пиковых значений рыночной капитализации.

Менее чем за день появилась еще одна хорошая новость. После закрытия акций в Китае в тот же день Reuters сообщило о важной позитивной новости: США разрешили 10 китайским компаниям, включая Alibaba, ByteDance, Tencent и JD.com, закупать чипы Nvidia H200. Вечером, после открытия торгов, акции Nvidia сразу же достигли исторического максимума.

Такая динамика, похоже, еще больше укрепила увлеченность инвесторов текущей рыночной логикой: «Переключение с высокого на высокое — счет постоянно растет, переключение с высокого на низкое — уровень все ниже».

Переключение с высокого на высокое — счет постоянно растет

Как правило, при относительно стабильной ситуации на рынке происходит серия ротаций секторов: капитал перетекает из переоцененных акций, которые сильно выросли, в недооцененные акции, которые не росли, что называется «переключением с высокого на низкое».

По опыту инвесторов, после роста технологических акций прибыльный капитал переключается на циклические акции, после усталости цикличности подключаются акции с высокими дивидендами, и все заканчивается фармацевтикой и потребительским сектором.

Однако за последний месяц на глобальных фондовых рынках капитал не перетекал из секторов с высокими ценами в низкооцененные активы, а продолжал преследовать более сильное, горячее и переполненное направление ИИ, что и является «переключением с высокого на высокое».

Рынок похож на змею, кусающую себя за хвост, просто перекатываясь от связанного с ИИ к связанному с ИИ, в итоге порождая одну акцию за другой, удваивающую свою стоимость.

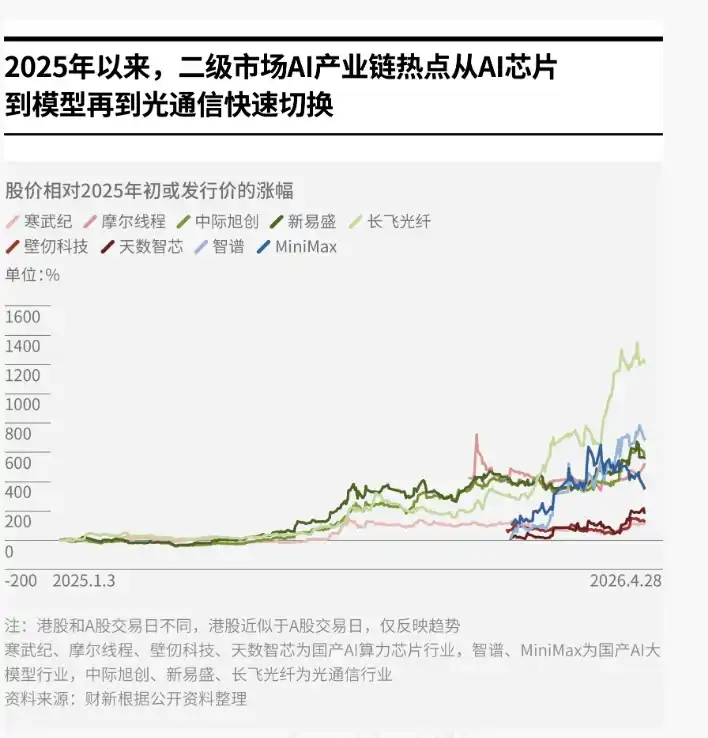

С начала апреля до 11 мая в акциях Китая капитал перетекал от оптических чипов на начальном этапе (представитель — YOJIA Technology, рост более 60%) к трем «мечам» оптических модулей на среднем этапе «И Чжунтянь» — New Easun (рост более 70%), Zhongji Innolight (рост более 55%), Tianfu Communications (рост более 45%).

Затем он перетекал на печатные платы (представитель —沪电股份, рост более 70%), и наконец, на мощности вычислений для ИИ на конечном этапе (представитель —寒武纪, рост более 90%). Почти вся цепочка инфраструктуры ИИ росла.

Фондовый рынок США также двигался в этом странном круге: после роста Nvidia (30%) наступала очередь памяти, представленной Micron (181%) и SanDisk (100%).

По данным Dongwu Securities, по состоянию на 24 апреля доля торгового оборота акций, составляющих 5% от общего оборота, достигла 43,7% от оборота всех акций, приближаясь к критическому значению переполненности в 45%.

В условиях стремительного роста «переключения с высокого на высокое» на рынке даже возникла крайняя эмоция: «Кроме ИИ, ничего не хочется покупать».

И это именно тот выбор, который сделали основные инвесторы.

Среди 50 крупнейших акций в портфелях фондов за первый квартал этого года в Китае 18 принадлежат к информационно-технологическому сектору. Например, акциями Zhongji Innolight владеют 1163 фонда, количество фондов, владеющих акциями New Easun, также достигает тысяч. В то же время чистая доля полупроводниковой отрасли в глобальных хедж-фондах выросла с 5,5% в прошлом году до нынешних 20%.

Главными жертвами «переключения с высокого на высокое», естественно, стали те, кто держит другие «не-ИИ акции».

Новый мир ускоряет свое приближение, но не все могут сидеть на этой ракете.

По данным CITIC Securities, среди индексов, выросших более чем на 10% в апреле, секторы «Информационные технологии + Коммуникационные услуги» в среднем составляли 68,9% от роста индекса. Даже для слабо растущих индексов доля технологического сектора в росте индекса достигала 54%.

Для сравнения, в условиях, когда в апреле индекс Шанхайской фондовой биржи стабилизировался на уровне 4100 пунктов, общий рост составил 5,66%, секторы продуктов питания и напитков (-1,1%), транспорта (-0,7%) и банковского сектора (-0,6%) в Китае оказались в числе отстающих, уступив общему рынку.

ИИ пользуется исключительным процветанием

Однако, когда многие индикаторы предупреждают о рисках единого «стадного» поведения, никто не решается легко выйти из игры.

Причина в том, что люди предпочитают «переключаться с высокого на высокое» не только из-за страха упустить возможности, но и из-за реальных соображений.

В настоящее время ИИ реально поднимает экономику и корпоративные прибыли, преувеличивая, можно сказать, стал «надеждой всей деревни».

Возьмем США в качестве примера. В первом квартале этого года ВВП США вырос на 2% (исключая инфляцию). По оценкам Wall Street Journal, экономика ИИ выросла на 31%, в то время как не-ИИ экономика выросла лишь на 0,1%.

Из них личное потребление, крупнейший компонент ВВП США, выросло лишь умеренно на 1,6%. Инвестиции в коммерческое строительство, такое как жилье, офисные здания и заводы, а также в транспортное оборудование, такое как грузовики и самолеты, снизились. В то же время инвестиции в технологическое оборудование взлетели на 43%, инвестиции в программное обеспечение выросли на 23%, а инвестиции в строительство центров обработки данных выросли на 22%.

Центр обработки данных, разработанный Oracle и OpenAI

Подобная ситуация также просматривается в структуре китайской экономики.

В первом квартале 2026 года прибыль высокотехнологичной обрабатывающей промышленности, представленной компьютерными коммуникациями, производством оборудования и т.д., выросла на 47,4% по сравнению с предыдущим годом, что способствовало росту прибыли всех промышленных предприятий выше установленного размера на 7,9 процентных пункта.

Что касается инвестиций, разница между темпами роста инвестиций в высокотехнологичные отрасли и темпами роста общих инвестиций в основные фонды увеличилась с 4,8 процентных пункта в 2024 году до 5,7.

На уровне экспорта стимулирующее влияние цепочки поставок, связанной с ИИ, еще более очевидно.

В первом квартале этого года экспорт интегральных схем вырос на 77,5% по сравнению с предыдущим годом, экспорт промышленных роботов с возможностью визуального распознавания ИИ и автономной навигации вырос на 42%, что значительно превышает общий рост экспорта.

К апрелю темпы роста экспорта Китая в годовом исчислении далее восстановились до 14,1%. Из них экспорт интегральных схем вырос на 99,6%, экспорт автоматического оборудования обработки данных вырос на 47,3%, став основной движущей силой роста экспорта.

То же самое относится и к импорту.

Под влиянием спроса на вычислительные мощности для ИИ объем импорта интегральных схем в Китай в первом квартале вырос на 45% по сравнению с предыдущим годом, а в апреле далее увеличился до 54,7%.

На рынке капитала те, кто получает прибыль, также сосредоточены в «ИИ».

По оценкам, в первом квартале этого года сектор информационных технологий обеспечил 80% прироста прибыли на фондовом рынке США. Например, общая прибыль S&P 500 выросла на 15,1% по сравнению с предыдущим годом, но прибыль «Семи сестер» США выросла на 61%, в то время как прибыль остальных 493 компаний выросла лишь на 16%.

Фондовый рынок Китая также демонстрирует схожие характеристики.

В первом квартале этого года чистая прибыль TTM отраслей, тесно связанных с ИИ, таких как коммуникации, электроника и цветные металлы, выросла на 60,9% по сравнению с концом 2023 года. Без учета этих 3 отраслей чистая прибыль TTM остальных нефинансовых секторов акций Китая снизилась на 23,5% за тот же период.

То, что ИИ пользуется исключительным процветанием, также дает инвесторам смелость для «стадного» поведения.

Новая история против старого нарратива

Однако, несмотря на такую сильную нарративную линию ИИ, трехдневный визит Трампа в Китай все же принес новые переменные на рынок.

14 мая индекс Шанхайской фондовой биржи после достижения этапного максимума в 4258 пунктов в тот день развернулся вниз, закрывшись ниже 4200 пунктов, на фоне красных свечей на графике закрылся большой красной свечой с падением на 1,52%; гонконгский индекс Hang Seng также открылся ростом, но закрылся снижением.

Это признак появления разногласий.

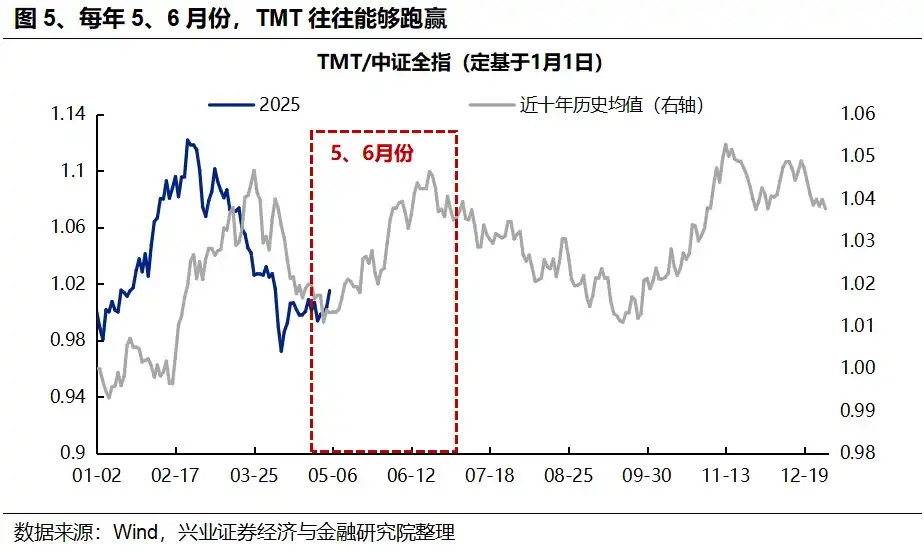

Исторически, ежегодно с мая по июнь обычно происходит сближение скорости ротации отраслей, что означает, что рынок может породить новую структурную основную линию.

Уолл-стрит также подготовилась к этому, заявив, что не ожидает суперпримирения, но с большими ожиданиями относится к «разрядке отношений».

В конце концов, помимо ИИ, в реальном мире есть так много нерешенных проблем, а ключ к их решению находится в руках этих двух сверхдержав.

По обобщению СМИ, в этом американо-китайском диалоге могут быть затронуты такие вопросы, как американо-иранская война, тарифы, критически важные минералы, инвестиции в США, импорт сельскохозяйственной продукции и т.д., каждый из которых может стать новым ориентиром для рыночных тенденций.

Но это также не означает, что странный круг «переключения с высокого на высокое» в ИИ на этом остановится.

С одной стороны, согласно календарному эффекту, технологические отрасли часто превосходят рынок в мае-июне, потому что этот период также является временем, когда проводятся более важные отраслевые конференции.

С другой стороны, учитывая присутствие стольких «быков ИИ», будущие новости будут естественным образом благоприятствовать сторонникам «переключения с высокого на высокое», и сообщение Reuters является большим подтверждением этому.

Судя по их ответам, будущая эволюция рыночной ситуации по-прежнему зависит от степени связи соответствующих активов с ИИ и степени влияния геополитики.

Иронично, что некоторые мнения уже начали рассматривать новую логику: когда ИИ становится единственным источником процветания, все больше и больше отраслей, изначально не связанных с ИИ, также начинают, в свою очередь, зависеть от эффекта богатства, созданного бычьим рынком ИИ.

Другими словами, потребление, рынок недвижимости, рисковые активы и даже восстановление внутреннего спроса нуждаются в том, чтобы эта ракета продолжала лететь вверх.

Возможно, все так же, как сказал бывший генеральный директор Citigroup Чак Принс:

Пока играет музыка, ты должен встать и танцевать.

Тонкость в том, что это было сказано накануне финансового кризиса.

Опубликованы результаты опроса о богатстве в мае

В конце статьи мы пригласили 9 инвесторов и экспертов по финансам дать прогнозы и оценки рынку на ближайший месяц.

Ежемесячный отчет о росте богатства выходит уже в 3-й раз с марта. Каждый месяц проводится проверка на основе рыночной ситуации за прошедший месяц, и приглашаются эксперты для прогнозирования.

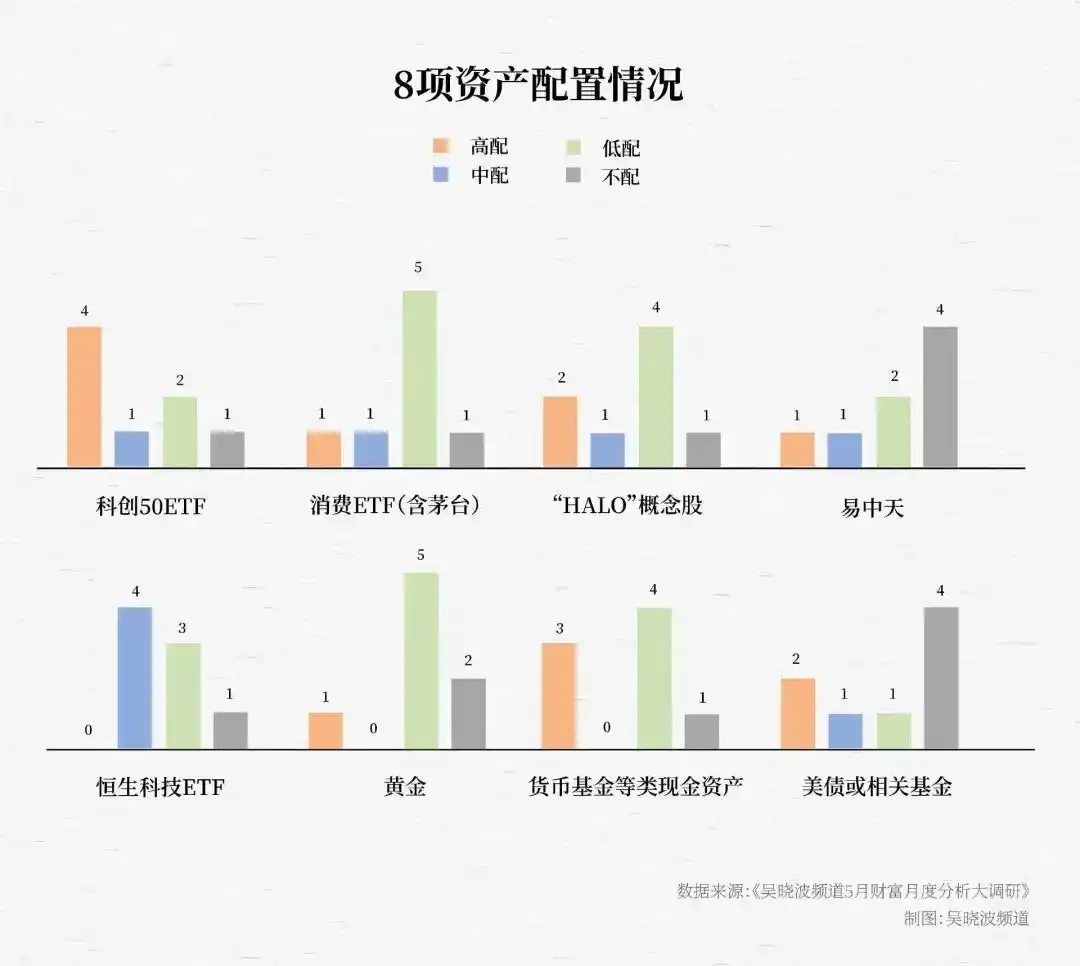

Классы активов, участвующие в голосовании в этом месяце: индекс CSI 300 (акции крупных компаний Китая), индекс Hang Seng (представляет Гонконг), фондовый рынок США (индикатор пузыря ИИ), индекс доллара США (ожидания инфляции), цена золота (убежище), цены на жилье в городах первого уровня (доверие), цена на нефть (геополитика), индекс основных потребительских товаров CSI (ожидания внутреннего спроса).

Результаты опроса показаны на рисунке:

Кроме того, после того как эксперты завершили оценку роста или падения активов, следующим шагом является распределение активов, связанное с реальными деньгами. На основе вышеупомянутых восьми классов активов мы далее выбрали 8 соответствующих инвестиционных инструментов и пригласили их сделать выбор по распределению.

Результаты показали, что среди активов, выбранных наиболее часто в порядке приоритета, прорисовались две четкие основные линии: технологический рост и активы «HALO».

В частности, проявляются следующие пять явных характеристик:

▶▷ Во-первых, ETF на индекс STAR 50 третий месяц подряд становится самым предпочтительным активом.

Эксперты, явно оптимистичные и выбравшие высокое распределение, приводят три причины:

◎ Первая: ChiNext/STAR Market уже демонстрируют сильный эффект заработка.

◎ Вторая: Сущность этого бычьего рынка — «технологический бык», STAR Market является главной ареной новой качественной производительности, и поддерживается ключевыми направлениями «Пятнадцатой пятилетки».

◎ Третья: Индекс STAR 50 обладает высокой определенностью, лучше, чем конкретные акции или сектора.

▶▷ Во-вторых, предпочтения в распределении активов «HALO» снова повысились.

За последние 3 месяца степень оптимизма экспертов в отношении акций концепции «HALO» претерпела явные изменения:

В марте акции концепции HALO были выбраны 6 раз, к апрелю количество выборов снизилось до 3, в основном из-за того, что рынок начал беспокоиться о перегреве эмоций. Ситуация изменилась в мае: огромные энергетические потребности инфраструктуры ИИ дали активы HALO, представленные цветными металлами, электроэнергией и энергетикой, новую историю в эпоху ИИ, количество выборов акций концепции HALO увеличилось до 5, снова заняв второе место.

▶▷ В-третьих, большинство экспертов предпочли избегать популярных активов «И Чжунтянь».

Основная причина — снижение вероятности успеха. За последний год «И Чжунтянь» выросли в 7–10 раз каждая, переполненность сектора оптических модулей, который они представляют, достигла самого высокого уровня за последние 10 лет.

▶▷ В-четвертых, хотя эксперты сохраняют осторожность в отношении тенденции восстановления потребления, они в целом признают ценность распределения потребительских ETF.

С точки зрения доли распределения, количество экспертов, выбравших среднее или высокое распределение потребительских ETF, невелико, более половины экспертов выбрали низкое распределение, но только 2 человека выбрали нераспределение.

Эксперты в целом считают, что потребительский сектор почти не воспользовался ростом бычьего рынка и все еще имеет пространство для восстановления; в условиях, когда популярные сектора уже переполнены, соотношение цена/качество становится очевидным. Поэтому распределение на данном этапе — это вариант «проигрыша времени, но не денег».

▶▷ В-пятых, предпочтения в распределении защитных активов продолжают снижаться.

За три месяца степень оптимизма в отношении золота и общая доля его распределения продолжали снижаться. Большинство экспертов в краткосрочной перспективе пессимистично настроены в отношении динамики золота, рассматривая его лишь как актив для распределения.

Что касается денежных фондов и казначейских облигаций США, то оптимизм и распределение разделились на два лагеря: одна группа в целом имеет высокое распределение технологических активов роста, низкое или отсутствующее распределение в продукты, подобные денежным средствам. Причина в том, что медленный и длинный бычий рынок по-прежнему устойчив, рынок продолжит идти вверх, поэтому они склонны переводить средства в высокоэластичные инструменты.

Другая группа имеет высокое распределение в продукты денежного рынка, низкое или отсутствующее распределение в технологические продукты. Причина — управление рисками, «При распределении на относительно высоких уровнях процветающих активов трудно найти рентабельное направление, в настоящее время не подходящее время для увеличения позиций».