Автор: Simon Taylor

Перевод: Block unicorn

Банки создают деньги, стейблкоины обеспечивают их движение. Нам нужно и то, и другое.

Сторонники токенизированных депозитов заявляют: «Стейблкоины — это нерегулируемый теневой банкинг. Как только банки запустят токенизированные депозиты, все предпочтут именно их».

Некоторым банкам и центральным банкам нравится эта идея.

Сторонники стейблкоинов утверждают: «Банки — это динозавры. Они нам не нужны в ончейн-пространстве. Стейблкоины — это будущее денег».

Крипто-энтузиасты особенно любят этот нарратив.

Обе стороны упускают суть.

Банки предоставляют крупнейшим клиентам более дешёвый кредит

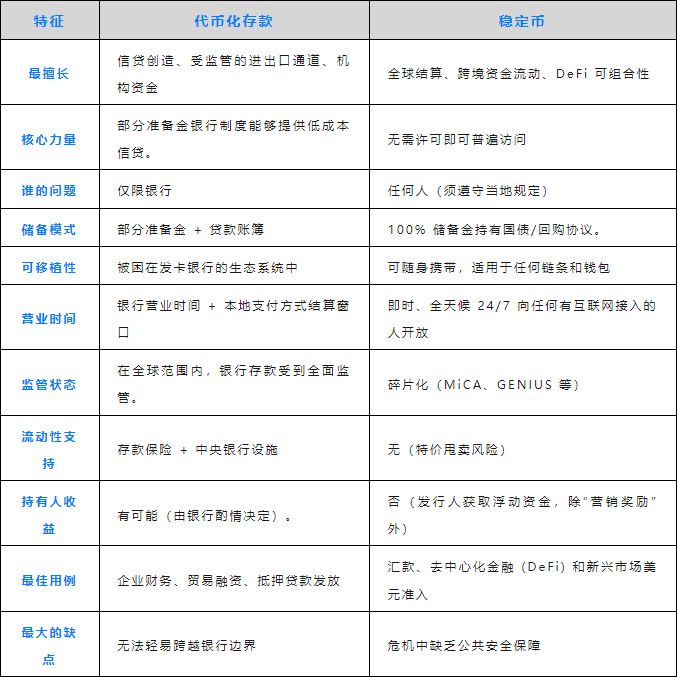

Вы вносите 100 долларов, они превращаются в 90 долларов кредита (или даже больше). Так работает банкинг с частичным резервированием. Веками он был двигателем экономического роста.

-

Компания из списка Fortune 500 размещает 500 миллионов долларов в JPMorgan.

-

Взамен она получает огромные кредитные линии по ставкам ниже рыночных.

-

Депозиты — это бизнес-модель банка, и крупные компании это прекрасно понимают.

Токенизированные депозиты переносят этот механизм в блокчейн, но они обслуживают только собственных клиентов банка. Вы по-прежнему находитесь в регулируемом пространстве банка, подчиняетесь его часам работы, процессам и compliance-требованиям.

Для тех, кому нужны дешёвые кредитные линии, токенизированные депозиты — хороший выбор.

Стейблкоины — как наличные

Circle и Tether держат 100% резервов, что эквивалентно 2000 миллиардам долларов в облигациях. Они получают 4-5% доходности, но не платят вам ничего.

Взамен вы получаете средства, свободные от банковского регулирования. Ожидается, что к 2025 году через стейблкоины будет осуществляться 9 триллионов долларов трансграничных переводов. Доступно в любое время, в любом месте, где есть интернет, без разрешения, 24/7.

Никаких запросов от банков-корреспондентов, никакого ожидания клиринга SWIFT, никаких «мы ответим вам в течение 3-5 рабочих дней».

Для компании, которой нужно заплатить аргентинскому поставщику в субботу в 11 вечера, стейблкоин — отличный выбор.

Будущее — за обоими

Компания, которая хочет получить хорошую кредитную линию от банка, также может захотеть использовать стейблкоины как канал выхода на нишевые рынки.

Представьте себе сценарий:

-

Компания из Fortune 500 держит токенизированные депозиты в JPMorgan

-

Взамен она получает льготные кредитные линии для американского бизнеса

-

Ей нужно заплатить аргентинскому поставщику, который предпочитает стейблкоины.

-

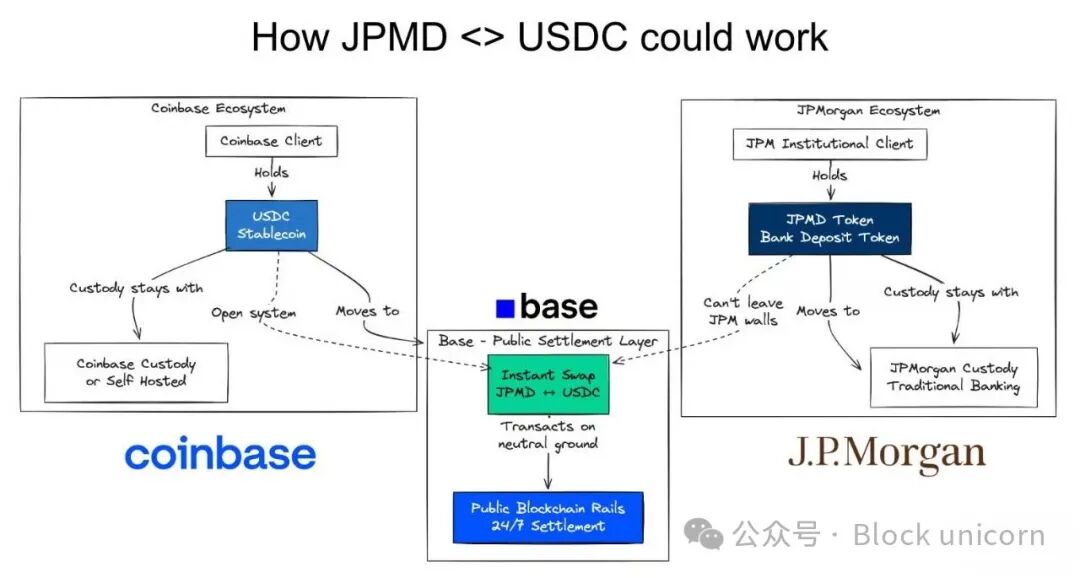

Она конвертирует JPMD в USDC.

Это пример того, куда мы движемся.

В ончейн. Атомарно.

И то, и другое.

Использовать традиционные каналы там, где это уместно.

Использовать стейблкоины там, где это не работает.

Это не вопрос выбора, а вопрос совмещения.

-

Токенизированные депозиты → дешёвый кредит внутри банковской системы

-

Стейблкоины → кеш-подобный расчёт вне банковской системы

-

Ончейн-конвертация → мгновенное преобразование, нулевой риск расчётов

У обоих есть свои плюсы и минусы.

Они будут сосуществовать.

Ончейн-платежи > API для оркестрации платежей

Некоторые крупные банки могут сказать: «Нам не нужны токенизированные депозиты, у нас есть API», и в некоторых случаях они правы.

Именно в этом и заключается преимущество ончейн-финансов.

Смарт-контракты могут создавать логику между множеством компаний и частных лиц. Когда депозит поставщика зачисляется, смарт-контракт может автоматически запустить финансирование запасов, оборотного капитала, хеджирование валютных рисков. Будь то банк или небанковская организация, всё делается автоматически и мгновенно.

Депозит → стейблкоин → оплата счёта → завершение последующих платежей.

API — это точка-точка, а смарт-контракты — много-ко-многим. Это делает их идеальными для рабочих процессов, пересекающих организационные границы. В этом сила ончейн-финансов.

Это совершенно другая архитектура финансовых услуг.

Будущее — за ончейн

Токенизированные депозиты решают проблему дешёвого кредита. Депозиты заблокированы. Банки выдают кредиты под залог депозитов. Их бизнес-модель остаётся неизменной.

Стейблкоины решают проблему портативности денег. Средства могут перемещаться куда угодно без разрешения. Развивающиеся страны получают доступ к доллару. Компании получают быстрые расчёты.

Сторонники токенизированных депозитов хотят только регулируемые платёжные каналы.

Сторонники стейблкоинов хотят заменить банки.

Будущее требует и того, и другого.

Компании из Fortune 500 хотят получать огромные кредитные линии от банков и мгновенные глобальные расчёты. Развивающиеся рынки хотят локального создания кредита и доступа к доллару. DeFi хочет композабельность и обеспечение реальными активами.

Споры о том, кто победит, упускают суть происходящего. Будущее финансов — в ончейн. И токенизированные депозиты, и стейблкоины являются необходимой для этого инфраструктурой.

Хватит спорить, кто победит. Пора начать строить интероперабельность.

Композабельные деньги.