"Explosive! Telecom and Mobile have launched token packages." "9.9 yuan for only 10 million tokens? I used to have 1 yuan for 1M of mobile data, so this is the cycle." "The new era of SMS bundles is here."...

On May 15th, Shanghai Telecom took the lead in launching a token (token) computing power service for users, with 1 yuan corresponding to 250,000 quota points. The internet exploded, with some complaining about the high cost and model shelling; others mocked themselves, "I feel like I've been left behind by the times, I don't even know what a token is."

Following closely, China Telecom launched a national-level token package, with China Mobile and China Unicom following suit. Upon the news, the stock prices of the three major operators collectively rose.

Information from the National Data Bureau shows that as of March, China's daily token call volume has exceeded 140 trillion, a more than 1000-fold increase compared to the 100 billion at the beginning of 2024. Meanwhile, "accelerating the construction of a national integrated computing power network" has been frequently mentioned recently. From enterprise-level decentralized construction to national-level unified scheduling, the infrastructure for the computing power "highway" is ready to be launched.

However, telecom operators' model capabilities and AI products have weak user perception in the C-end. Ordinary users chatting with large models and writing copy can be satisfied with free large models. Do they really need to spend a lot of money to buy tokens? What exactly is the telecom operators' strategy with this move?

Operators Rush to Sell Tokens

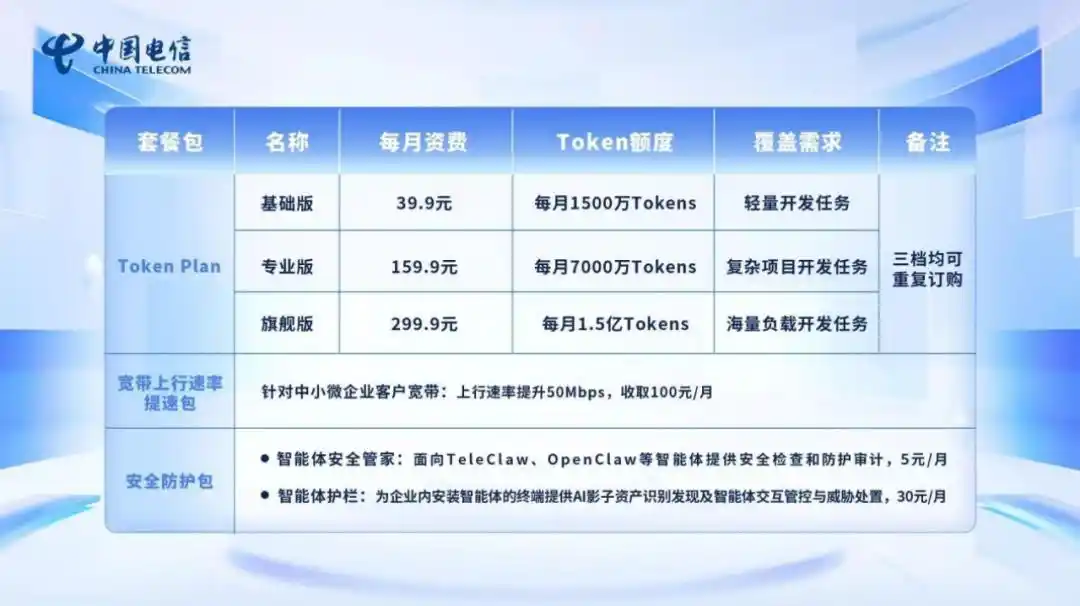

On May 15th, Shanghai Telecom took the lead in launching a token computing power package at the 2026 China Telecom Technology Festival. The packages are divided into two tiers: one is pay-as-you-go, with 1 yuan for 250,000 tokens; the other is a monthly subscription, with 9.9 yuan for 10 million tokens. To stimulate demand, Shanghai Telecom users can also receive a free 25 million token trial monthly package.

Two days later, China Telecom launched a series of trial commercial token packages nationwide, targeting developers and small and medium-sized enterprise customers, providing integrated services of "token + connection + security." At the same time, China Mobile and China Unicom successively launched token products for C-end users.

On social media, some netizens said: "Free trial first, then raise prices when you're hooked, I'm familiar with this routine." More people complained about the high cost. As a comparison, on April 26th, DeepSeek officially released an API price adjustment announcement, lowering the input cache hit price for its full suite of APIs. The V4Pro model's million token input cache hit price is as low as 0.025 yuan, about 1/40th of Telecom's price.

Although the top-level design is in place, in specific business promotion, the three major operators are not in sync. On May 20th, "Bao Bian" called Shanghai Telecom's customer service. From the call, the customer service seemed somewhat unfamiliar with the token package, needing to search for "token" in the backend to introduce the package price based on materials, but was not familiar with how to use tokens. During this process, English spelling mistakes even occurred multiple times.

Zhejiang Mobile's customer service, after searching for "token," began to introduce the "Cloud Computer" business: targeting B-end enterprises, employees can access the company's intranet and operate professional software through a virtual desktop in the cloud. However, the customer service was not familiar with the token package for C-end users. At a Wenzhou Unicom offline business hall, staff were also unaware of the token package, and there were no related materials displayed in the store.

Despite the market not yet being opened, compared to mainstream large models on the market, telecom token packages can be purchased directly with mobile phone credit and support cross-model use. After purchasing token credits, users can call over 30 mainstream large models on-demand through API interfaces, integrating AI capabilities into their own software or automated workflows. If directly recharging on a large model company's platform, the balance can only be used on that specific model. Different models have their own strengths. If a user needs to use another model, they have to recharge again, which may cause waste.

This is similar to users buying a general mobile data package from an operator, which can be used for apps like WeChat, Douyin, and Taobao; whereas if they buy Tencent's directed traffic package, they cannot open Taobao or Douyin.

For ordinary users, if they only engage in daily conversations with large models, write basic copy, etc., current mainstream large models can basically handle it. Token packages are more suitable for developers or heavy AI users who love to tinker, have programming basics, and know how to call APIs.

The Anxiety of Operators

From selling call and SMS packages, to internet data, and now to selling token packages, telecom operators' businesses are continuously evolving.

In recent years, as the growth of traditional mobile and broadband businesses has slowed, operators have fallen into growth anxiety. Looking at the 2025 financial reports released by Unicom, Telecom, and Mobile, their revenues increased by only 0.7%, 0.1%, and 0.9% respectively, hitting a six-year low. Mobile phone and broadband business growth has significantly slowed, with some core revenue indicators declining year-on-year. Among them, China Mobile's net profit attributable to the parent company even fell by 0.9% year-on-year.

On one hand, the traditional personal communication business market has reached its ceiling. Taking China Mobile as an example, the total number of users in 2025 was 1.005 billion, with only a net increase of 1 million for the whole year, indicating almost stagnant growth. On the other hand, under stock competition, operators are caught in homogeneous internal competition, competing on low prices, further depressing the tariff standards. In 2025, mobile ARPU (Average Revenue Per User) was 46.8 yuan, a year-on-year decrease of 3.5%.

When traditional telecom businesses fall into growth stagnation, emerging businesses become a breakthrough for new growth curves.

At the 2026 China Telecom Sixth Technology Festival, Shanghai Telecom General Manager Gong Bo stated in his speech that the "15th Five-Year Plan" period begins with fully embracing artificial intelligence, responding to the group's "Cloud Reform, Digital Transformation, Intelligence Benefits" strategy, and promoting the deep integration of AI with the economy, society, and people's livelihood.

Selling tokens to the C-end is essentially providing AI services to users. When the unfamiliar token is packaged into perceivable AI services, demand might be stimulated.

"Bao Bian" saw on the mobile APP that entering the AI trial zone on the homepage allows users to experience functions like smart cutout and smart removal. Cutting out a person from a photo consumes 31,000 tokens, while the token balance gifted in the backend is 500,000. This means that after users edit about a dozen photos, if they want to continue, they have to "pay more."

Token purchase page on China Mobile APP

During the cutout process, the system prompts that the specific service is provided by Meitu, with Mobile playing the role of a "channel." In the Meitu app, users can enjoy basic cutout services for free. If they want to experience advanced features, the continuous monthly subscription fee is 30 yuan/month. Therefore, if users have a large number of photo editing needs, buying a Meitu membership directly is clearly more cost-effective.

On the Unicom app, there is only a "Pet Ai" zone where users can use AI to generate images of pet cats and dogs, customizing exclusive electronic pets.

"Bao Bian" randomly surveyed several C-end users, all of whom gave feedback that these functions are not essential needs and they wouldn't specifically buy tokens from operators for this: "I already have a Meitu membership, bought cheaply on Xianyu," "Who keeps electronic pets nowadays?"...

Thus, even though operators are trying to transform into AI, their "pipeline" nature remains serious. They haven't been able to create sufficiently hardcore C-end products. Whether they can use AI to activate user consumption and reverse the decline still awaits market testing.

New Computing Power Infrastructure

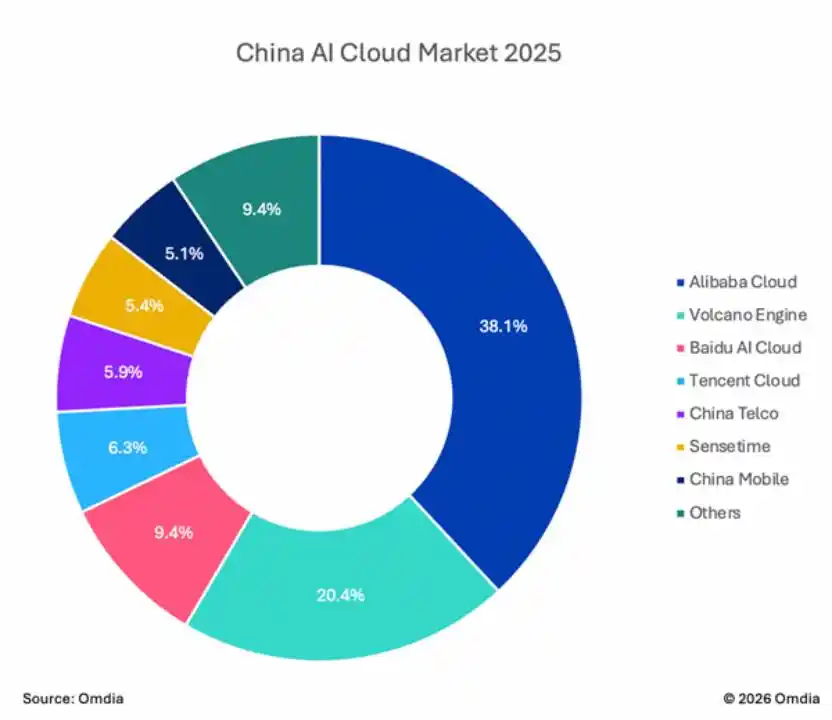

When operators squeeze into the AI track, they no longer face only competition among themselves but have to "grab the rice bowl" from numerous cloud vendors.

On this track, mainstream players like Alibaba Cloud, Volcano Engine, Huawei Cloud, Tencent Cloud, and Baidu AI Cloud have already captured the most lucrative markets with their first-mover advantages.

2025 China AI Cloud Market Share

At the same time, these cloud vendors' price echelons have matured. Facing a supply-demand imbalance market situation, they have recently intensively raised computing power prices, showing strong market performance.

Besides computing power advantages, Alibaba, ByteDance, and Tencent's Qwen, Doubao, Yuanbao large models have obvious advantages in C-end users. In contrast, operators' large models do not have advantages in product performance and developer ecosystems. Although China Telecom has its self-developed "Xingchen" large model, customer service, when introducing the token package, also highlighted support for models like DeepSeek and Zhipu GLM.

Essentially, telecom operators are doing the business of a "model supermarket," playing the roles of "pipeline" and "integrator." However, their advantages in offline base stations, networks, etc., are important cornerstones of the national unified computing power network.

Relevant policies indicate that AI must deeply integrate with advanced manufacturing, shifting focus from technological breakthroughs to large-scale, replicable, monetizable scenario penetration. Although cloud vendors' large models perform strongly, AI is far more than a cloud matter. The unique advantage of operators lies precisely in those ground-level capabilities that internet companies find difficult to replicate.

For example, autonomous driving is considered an important application scenario for AI + physical. High-speed movement of vehicles requires low-latency, high-reliability computing power. Operators' base stations spread across the country can become the frontier touchpoints for physical AI. Currently, China Telecom is focusing on building a "4+4+31+X" computing power network, creating a four-level computing power system of "center-province-edge-end." Whether for large models or physical AI, telecom operators participating in the unified scheduling of computing power resources can extend computing power coverage to the township level.

Especially when AI inference requires cross-regional scheduling of computing power, the stability, low latency, and high bandwidth of the network become particularly crucial. If cloud vendors' large models are imagined as "power plants," then operators are equivalent to the "power grid" covering the whole country. Power plants can be very strong in generating electricity, but delivering electricity to every household relies on the power grid.

A Vice President of Vipshop told "Bao Bian" that the computing power network is like the power grid over 100 years ago. In his view, when electricity was first born, many people didn't know how to use it. It wasn't until the power grid delivered electricity to every household that various electrical appliances emerged, creating new markets and application scenarios. Similarly, although most people are not familiar with tokens now, with the completion of the unified computing power network and the decline in computing power costs, entirely new computing power consumption scenarios will emerge.

From this perspective, operators entering the market to sell computing power is not just a showdown between large models but a reconstruction of computing power infrastructure. The competition for operators in the AI era is not to prove they can train models stronger than Alibaba or ByteDance. It is to prove that when AI computing power becomes infrastructure like water and electricity, operators with the "power grid" are the ones closest to delivering it to users.

This article is from the WeChat public account "Bao Bian" (ID: baobiannews), author: Chen Fashan