Автор: Caitlin Ostroff, Katherine Long и Neil Mehta, WSJ

Перевод: AididiaoJP, Foresight News

33-летний Джон Педерсен в настоящее время не может работать. Этот бывший шеф ресторана Outback Steakhouse восстанавливается после автомобильной аварии, и его сбережения почти закончились. Платформа прогнозных рынков Kalshi, возможно, могла бы быстро решить проблему — он взял кредит с плавающей процентной ставкой и начал делать ставки.

Сначала всё шло хорошо. Педерсен превратил около 2000 долларов в почти 8000, делая ставки на суточное количество снегопадов в Детройте, городе, где он живёт. Затем он вложил средства в торговлю на спортивных событиях, используя стратегию, разработанную с помощью ИИ, и, согласно данным его счёта, изученным The Wall Street Journal, в итоге довёл сумму до 41 000 долларов.

Затем он сделал самую смелую ставку на сегодняшний день: поставил все 41 000 долларов на то, что определённая знаменитость произнесёт конкретное слово на телевидении, и проиграл всё.

Педерсен не единственный, кто ушёл с пустыми руками с рынков, где «можно ставить на что угодно», включая спорт, знаменитостей, новости и многое другое.

Kalshi и её конкурент Polymarket позиционируют себя как инструменты, способные изменить судьбу обычных людей, — намекая, что у каждого есть равные шансы сорвать большой куш. «Я чуть не осталась без арендной платы, но благодаря прогнозам на Kalshi я заработала деньги на два года вперёд», — восторженно говорит женщина в рекламе Kalshi на TikTok.

Но для большинства пользователей реальность совершенно иная.

Напротив, согласно анализу данных платформ и интервью с трейдерами, проведёнными The Wall Street Journal, обычные трейдеры постоянно теряют деньги, а небольшая группа опытных профессионалов — включая торговые компании с огромными ресурсами данных — съедает их средства.

The Wall Street Journal обнаружила, что на Polymarket 67% прибыли приходится на всего 0,1% счетов. Это означает, что менее 2000 счетов в общей сложности заработали чистую прибыль в размере почти 500 миллионов долларов. WSJ проанализировала 1,6 миллиона счетов, торговавших на Polymarket с ноября 2022 года. На платформе зарегистрировано как минимум 2,3 миллиона счетов.

То же самое происходит на Kalshi, где проигравших гораздо больше, чем победителей. Представительница Элизабет Диана заявила, что по данным за последний месяц на каждого прибыльного пользователя приходится 2,9 убыточных. Она отметила, что по мере роста платформы это соотношение может измениться. Компания не раскрывает полные данные о прибыли пользователей и общее количество пользователей.

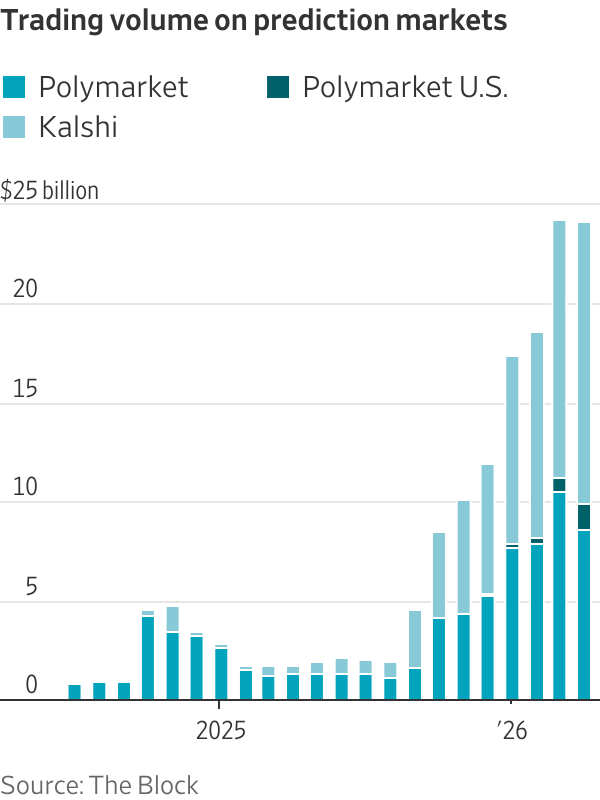

Согласно данным аналитической компании The Block, совокупный объём торгов на двух платформах в апреле взлетел до 242 миллиардов долларов, тогда как годом ранее он составлял всего 18 миллиардов долларов.

Сторонники утверждают, что эти рынки не являются азартными играми, а представляют собой использование коллективного разума для точного прогнозирования будущих событий. Исследования Федеральной резервной системы показали, что Kalshi является эффективным инструментом для прогнозирования экономических тенденций.

Трейдеры платят за потоки больших данных от третьих сторон, чтобы получить преимущество. Компьютеры используют данные и алгоритмы для прогнозирования движения цен и управления рисками гораздо быстрее, чем любой человек. Профессионалы также используют преимущества масштаба, совершая частые, стратегические сделки — иногда десятки тысяч в день — и получая прибыль от незначительных колебаний, что требует концентрации и дисциплины, редко встречающейся у обычных пользователей.

Бывший профессиональный игрок в покер, обученный статистике, Майкл Бос, говорит: «У розничных трейдеров нет никаких шансов». Он совершает 60 сделок в минуту на Kalshi, внося изменения в свои котировки на покупку и продажу 30 раз в секунду.

Диана заявила, что многие финансовые рынки демонстрируют аналогичную концентрацию богатства, и что на Kalshi больше пользователей, зарабатывающих деньги, чем при дневной торговле или традиционных спортивных ставках. Она сказала, что Kalshi больше не размещает рекламу «помогите мне заплатить за аренду».

Представитель Polymarket отказался комментировать анализ WSJ.

Polymarket имеет партнёрские отношения по обмену данными с издателем WSJ Dow Jones; этот анализ использует только общедоступные данные.

Возьмём пример полностью провалившейся ставки безработного шефа Педерсена: он попал в категорию, полную «простаков»: рынки упоминаний (ставки на то, скажет ли человек определённое слово).

Профессиональные трейдеры заявляют, что они не трогают такие ставки, потому что они непредсказуемы, и даже данные на миллионы долларов не дают надёжного преимущества.

Согласно анализу WSJ, ставки на рынках упоминаний фактически выплачиваются реже, чем ожидается. Розничные бетторы берут на себя больший риск, чем осознают, отчасти из-за явления «смещения на аутсайдеров» — бетторы из-за азарта переоценивают вероятность маловероятных событий.

Месячный объём торгов на рынках упоминаний Kalshi намного превышает объём Polymarket, с середины 2025 года наблюдается взрывной рост. Эти ставки очень популярны среди молодых пользователей, которых платформа стремится привлечь, — включая инфлюенсеров, которые продвигают их в прямых эфирах в социальных сетях и других видео, где они хвастаются победами.

Джон Педерсен стоит у приюта для бездомных в Детройте, где он живёт с тех пор, как потерял деньги на инвестициях в Kalshi. © Emily Rose Bennett для The Wall Street Journal

«Те, кто умнее тебя»

Реклама Polymarket и Kalshi для всех типов ставок проста: пользователи могут монетизировать свои знания и быстро заработать деньги — этот посыл покорил мир.

Однако анализ WSJ показывает, что более 70% пользователей Polymarket терпят убытки. Аналогичный вывод был сделан в рабочем документе французских и канадских исследователей в прошлом месяце. Они обнаружили, что почти вся прибыль от прогнозных рынков достаётся опытным трейдерам, в то время как отчаянные ставки и розничные трейдеры несут убытки.

Анализ данных о торгах на Polymarket, проведённый WSJ, показал, что средний пользователь теряет от 1 до 100 долларов, а 10% худших пользователей теряют в среднем по 4000 долларов каждый.

Некоторые принимают эмоциональные решения — следуют интуиции или делают ставки на основе информации, полученной из открытых источников.

Житель Коннектикута, который называет себя человеком с проблемой азартных игр, потерял 2000 долларов за один день, делая ставки на Супербоул на Kalshi — всё в напряжённом четвёртом квартале. 31-летний житель Индианы назвал такую торговлю «наркотиком» и в первые месяцы этого года почти ежедневно делал ставки на спортивные события на Kalshi, потеряв около 5000 долларов.

Для сравнения, прогнозные рынки всё чаще привлекают компании с десятками сотрудников, тратящие миллионы долларов на покупку профессиональных спортивных и финансовых данных и запускающие торговые алгоритмы. Их цель — обыграть студентов, любителей азартных игр и других трейдеров с низким объёмом торгов, которые составляют большинство пользователей платформ.

В традиционных азартных играх букмекер устанавливает коэффициенты, принимает ставки и выплачивает выигрыши. На прогнозных рынках нет «букмекера», пользователи торгуют между собой. Платформы только взимают комиссию за сделку, которая варьируется в зависимости от цены контракта, типа рынка и других факторов.

В офисе в Сохо студент-недоучка пристально смотрит на экран компьютера, наблюдая за потоком миллионов долларов от розничных трейдеров, делающих ставки на цену биткойна.

Сэмюэл Вуд-Сорлофф бросил Принстонский университет в этом году и получил чек на 500 000 долларов от крипто-стартап-акселератора Alliance Capital, поддерживаемого известными инвесторами Кремниевой долины, включая криптопредпринимателя Баладжи Шринивасана. В старшей школе он посещал математические курсы в Калифорнийском университете в Беркли, а перед поступлением в Принстон взял годичный перерыв для торговли криптовалютами. Теперь он и четверо друзей переехали в Нью-Йорк, чтобы торговать на прогнозных рынках на полную ставку, делая ставки на спорт, политику и будущие цены криптовалют.

В интервью он сказал: «Наши единственные конкуренты — маркет-мейкеры». Он имел в виду другие компании, которые, как и они, постоянно выставляют котировки на покупку и продажу. Он отказался раскрывать прибыли или убытки своей компании, но сказал, что развернул от 500 000 до 1 миллиона долларов на Polymarket, Kalshi и других небольших прогнозных рынках.

Бывший профессиональный игрок в покер Бос заработал на Kalshi более 668 000 долларов, в основном на спортивных ставках, с тех пор как начал серьёзно торговать около трёх месяцев назад. Помимо скорости торговли, он крайне тщательно подходит к ценообразованию своих котировок на покупку и продажу.

Он говорит: «Вы обнаружите, что легче всего зарабатывать на спорте». «Спорт привлекает всех „больных“ молодых парней, я думаю». Он уточнил, что «больные» означает людей с игровой зависимостью.

Он заметил на Kalshi, что множество розничных трейдеров просто делают ставки «Да» на то, что они хотят, чтобы произошло. «Это совершенно не похоже на криптобиржи или фондовые биржи, где люди торгуют ценными бумагами».

Студент Университета Вирджинии в Шарлоттсвилле Джонатан Столл-Райан управляет компанией, которая входит в пятёрку крупнейших трейдеров по объёмам торгов на ценах криптовалют на Kalshi. © Laura Thompson для WSJ

Компания Столла-Райана платит за получение данных в реальном времени от третьих сторон и использует алгоритмы для выполнения десятков тысяч сделок в день. © Laura Thompson для WSJ

Другой основатель компании, в которой работает около 12 сотрудников (все, как и он, студенты), Джонатан Столл-Райан, входит в пятёрку крупнейших трейдеров по объёму ставок на цены криптовалют на Kalshi. Компания ежегодно тратит более 200 000 долларов на источники данных в реальном времени, агентов ИИ-кодирования и серверы, используя алгоритмы для выполнения десятков тысяч сделок в реальном времени каждый день.

Столл-Райан, находясь в Университете Вирджинии с членом братства, увидел, как тот небрежно делает ставки на цену биткойна на Kalshi. Он говорит, что тогда подумал: «Этот парень потеряет деньги».

Большинство этих профессиональных трейдеров выступают в роли маркет-мейкеров. Kalshi и Polymarket заявляют, что возвращают часть комиссий маркет-мейкерам, а иногда даже платят им за обеспечение ликвидности.

Количественная торговая компания Susquehanna International Group стала первым крупным институциональным маркет-мейкером на Kalshi в 2024 году. По словам профессиональных трейдеров, отслеживающих стакан заявок Kalshi, компания торгует через Kalshi на миллиарды долларов в неделю. Её счёт является частным, и точная прибыль неизвестна. Susquehanna отказалась от комментариев.

Другая количественная торговая компания Jump Trading активна как на Polymarket, так и на Kalshi. В середине апреля президент Citadel Securities Джим Эспозито на мероприятии Semafor заявил, что компания «внимательно следит» за развитием прогнозных рынков. Некоторые трейдеры, покупающие высокорискованные опционные контракты, теперь стекаются на прогнозные рынки.

Соучредитель Susquehanna Джефф Ясс в подкасте о спортивных ставках 2020 года сказал: «Все спортивные ставки, весь покер, вся торговля опционами по своей сути — это игра против кого-то глупее тебя». В том же подкасте он описал свою роль в поддержке развития прогнозных рынков как «миссию от Бога».

С одной стороны, он считает, что американцы должны иметь возможность легально делать спортивные ставки, даже если в некоторых штатах это запрещено; с другой стороны: «Я ожидаю заработать много денег».

Столл-Райан в кампусе Университета Вирджинии. Его компания нанимает около дюжины студентов. © Laura Thompson для WSJ

В поисках лёгких денег

Платформы предлагают пользователям заключать контракты с ответом «да/нет» на будущие события. Контракты обычно устроены так, что выплачивают 1 доллар в случае правильного прогноза и обнуляются в случае ошибки. Цена контракта отражает оценку трейдерами вероятности наступления события. Например, если контракт на определённое событие торгуется по цене 41 цент, прогнозный рынок считает, что вероятность наступления этого события составляет 41%. Если вы выиграете, контракт, купленный за 41 цент, выплатит 1 доллар; если ошиблись, вы теряете свои деньги.

Цена контракта постоянно меняется до расчёта в зависимости от рыночных сил покупателей и продавцов. Трейдеры получают прибыль от незначительных колебаний цены, как и трейдеры с Уолл-стрит.

Многие наивные участники прогнозных рынков повторяют путь спекулянтов на финансовых рынках, ищущих лёгкие деньги. Десятилетия исследований показывают, что дневные трейдеры редко зарабатывают. В последние годы многие розничные трейдеры, подстёгиваемые социальными сетями, теряли свои сбережения на высоковолатильных «мемных» акциях.

Американские операции Kalshi и Polymarket (последняя недавно запустила свой сервис для небольшого количества ранних пользователей) регулируются Комиссией по торговле товарными фьючерсами (CFTC), и компании заявляют, что торговля на их платформах аналогична другим регулируемым финансовым рынкам. Большая часть активности Polymarket происходит на её офшорной платформе, которая технически запрещена для американцев, но её легко обойти с помощью VPN.

Критики утверждают, что эти рынки подвержены таким проблемам, как инсайдерская торговля. Недавние примеры включают предполагаемую инсайдерскую торговлю в связи с военными действиями США в Венесуэле, анонсами Google и выборами в Конгресс.

Председатель CFTC Майкл Селиг защищал прогнозные рынки и разъяснил юрисдикцию федерального агентства над этими платформами. Агентство уже пресекало предполагаемую инсайдерскую торговлю и намекало на усиление правоприменения со стороны правительства.

Polymarket заявила, что сотрудничает с Министерством юстиции по борьбе с инсайдерской торговлей. Kalshi запрещает инсайдерскую торговлю на своей платформе и в последние месяцы оштрафовала нескольких трейдеров за нарушения.

Бывший сотрудник Kalshi Ади Раджапрабакаран в прошлом году на Substack назвал розничных трейдеров «рыбой» (жаргон игроков, обозначающий новичков, которые легко теряют деньги). В интервью он сказал, что, хотя в целом по-прежнему считает это правдой, он также верит, что присутствие неосведомлённых трейдеров на прогнозных рынках является сильным стимулом для более опытных трейдеров выходить на них, что ведёт к более точным прогнозам.

«Когда каждый делает ставку, он думает, что обладает более полной информацией, чем другие», — сказал он. «В долгосрочной перспективе более правые зарабатывают больше денег. Никто не принуждается к этому».

Ставка в 41 000 долларов

До знакомства с рынками упоминаний дела Педерсена на Kalshi шли неплохо. «Я широко слежу за финансами, — говорит он. — Я всегда ищу способы отточить свою проницательность, если можно так выразиться».

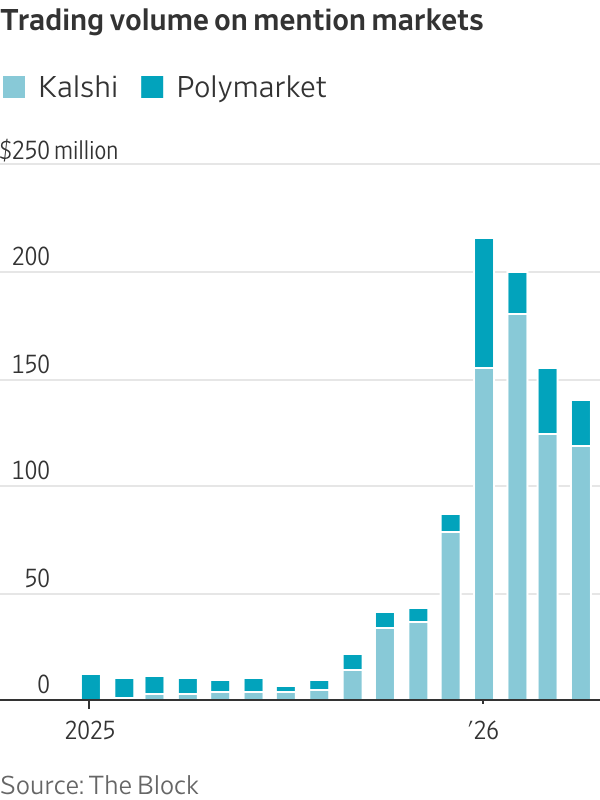

Объём торгов на рынках упоминаний

В основе ставок на рынках упоминаний лежит один простой вопрос: произнесёт ли публичное лицо определённое слово? В этом году пользователи Kalshi поставили более 28 миллионов долларов на то, произнесёт ли Трамп в послании о положении страны слова «картель», «сомалийский» или «хоккей». По данным The Block, в феврале пользователи Kalshi в общей сложности поставили на рынках упоминаний почти 181 миллион долларов.

Анализ данных Kalshi, проведённый WSJ, показывает, что фактический процент выплат на рынках упоминаний значительно ниже, чем ожидают бетторы, исходя из указанных коэффициентов.

WSJ проанализировала более 35 000 завершённых рынков упоминаний на Kalshi и обнаружила, что в среднем сделки «Да», оценённые с вероятностью выигрыша 50%, фактически выплачиваются примерно в 40% случаев. Поскольку цена контракта должна соответствовать вероятности, эти бетторы фактически переплачивают.

Анализ показал, что торговля на этих рынках часто демонстрирует смещение в сторону аутсайдеров с высокими коэффициентами, которые часто проигрывают. В среднем трейдеры, которые делают ставку «Да», увидев первую цену на рынке упоминаний (это обычная модель для розничных трейдеров), теряют 11% от поставленной суммы. Согласно исследованиям Университета Невады в Лас-Вегасе, эта отдача хуже, чем у большинства игровых автоматов в Лас-Вегасе.

Представитель Kalshi Диана признала наличие систематического отклонения на рынках упоминаний, но заявила, что эти рынки не репрезентативны для общего ценообразования на платформе и не являются подходящим объектом для такого анализа. Она добавила, что собственный анализ Kalshi показывает, что ценообразование на рынках упоминаний становится более точным в течение четырёх часов до события.

Kalshi поощряет трейдеров на рынках упоминаний транслировать в прямом эфире процесс своей торговли во время событий; два стримера заявили, что это делается для повышения вовлечённости на рынке. Аналитики Bank of America написали в апрельском отчёте о прогнозных рынках: «Прямые трансляции рынков упоминаний в социальных сетях часто становятся вирусными и повышают узнаваемость бренда Kalshi».

В январе этого года Педерсен поставил все свои заработанные 41 000 долларов на то, что рэпер A$AP Rocky произнесёт слово «рэпер» в «Вечернем шоу с Джимми Фэллоном» — недавно эта звезда сыграла рэпера в фильме. У него был шанс выиграть более 168 000 долларов.

Но в версии, показанной NBC, этот фрагмент был вырезан. Согласно правилам рынка Kalshi, учитывается только то, что было произнесено в телевизионной версии.

Педерсен в своём видео заявил, что эта часть правил не была очевидна на сайте платформы, и он её не видел. (Позже Kalshi обновила интерфейс, сделав правила рынка более заметными.)

Педерсен потерял всё, и у него почти не осталось других ресурсов. В настоящее время он живёт в приюте для бездомных в центре Детройта, хотя говорит, что недавно получил предложение о работе продавцом ипотечных кредитов.

Он говорит, что его цель, когда он снова встанет на ноги, — попасть в финансовую отрасль, чтобы поддержать свою музыкальную карьеру. Вернётся ли он к торговле на прогнозных рынках? «Возможно, — говорит он. — Я бы предпочёл проводить время на более регулируемых рынках».