Редакционное примечание: 5 февраля крипторынок снова пережил обвал: объем ликвидаций за 24 часа превысил 2,6 миллиарда долларов, а Биткоин в какой-то момент рухнул до 60 000 долларов. Однако у рынка, похоже, нет четкого консенсуса относительно причин этого падения. Джефф Парк, советник Bitwise, предлагает новый аналитический фреймворк с точки зрения опционов и механизмов хеджирования.

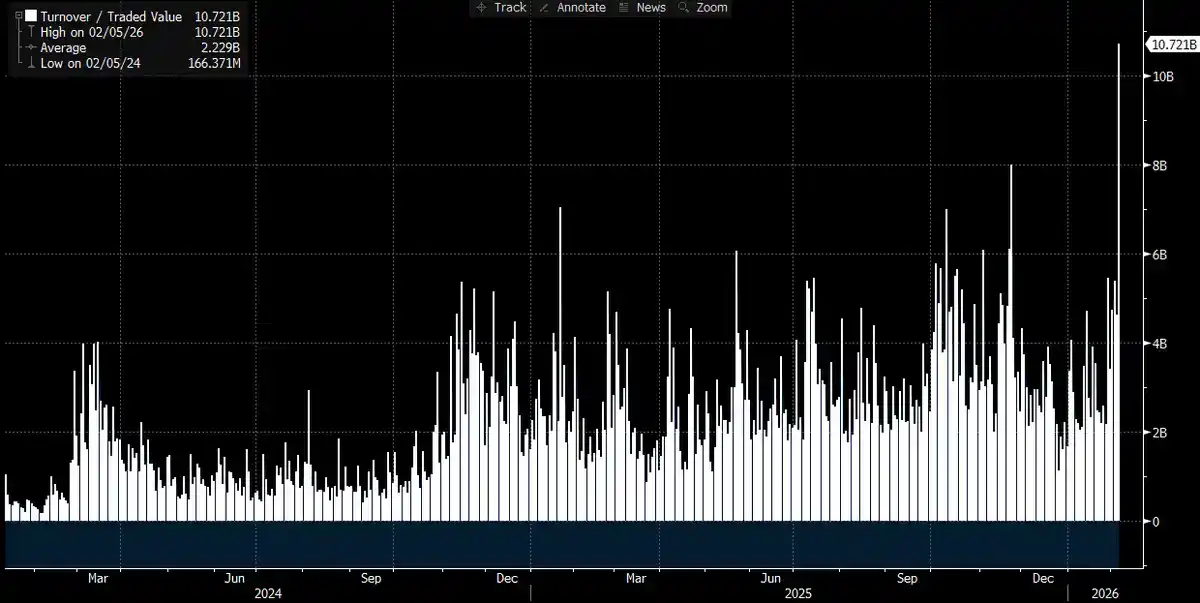

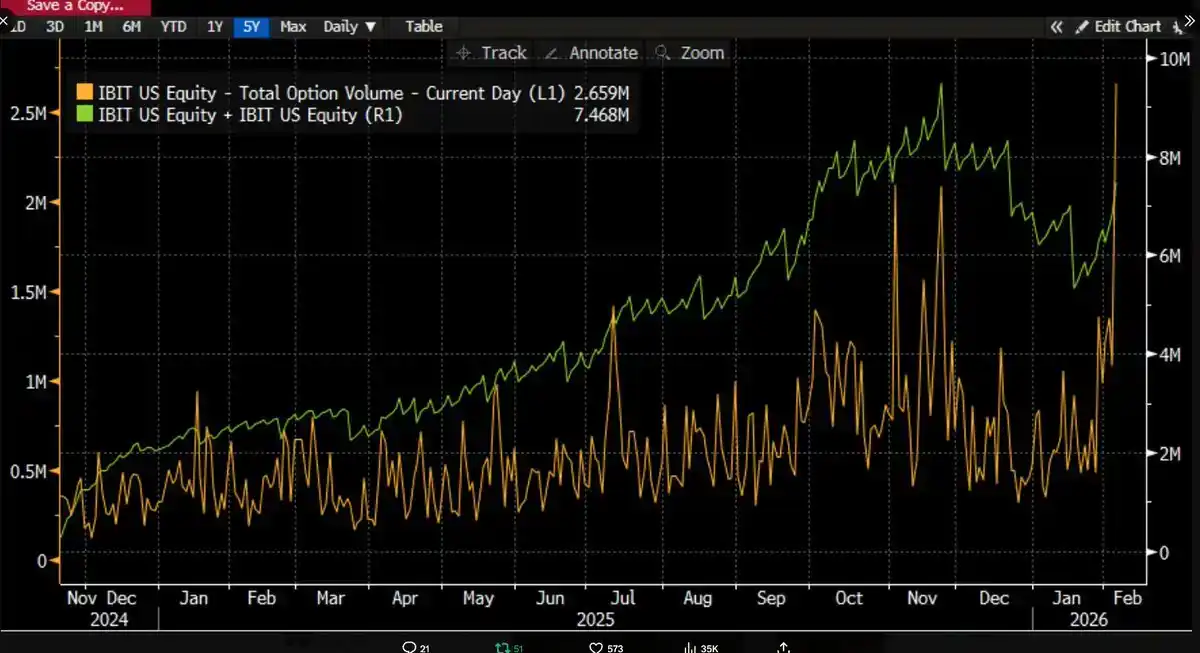

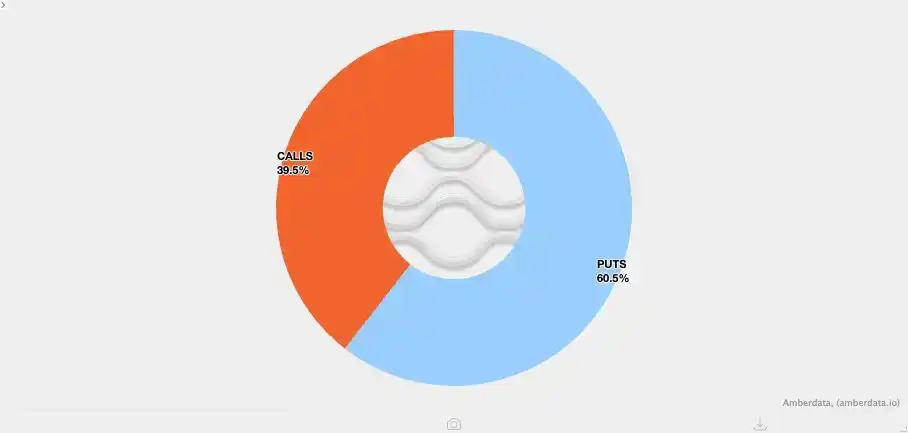

Со временем, по мере появления большего количества данных, ситуация проясняется: эта резкая распродажа, вероятно, связана с Биткоин-ETF, и сам этот день также стал одним из самых волатильных торговых дней на рынках капитала за последние годы. Мы можем прийти к такому выводу, потому что объем торгов IBIT в тот день достиг рекордно высокого уровня — оборот превысил 10 миллиардов долларов, что в два раза больше предыдущего рекорда (действительно впечатляющая цифра), в то время как объем торгов опционами также обновил рекорд (см. графики ниже, это самое большое количество контрактов с момента запуска этого ETF). Что несколько нетипично по сравнению с прошлым, так это то, что с точки зрения структуры объема на этот раз опционные сделки явно доминировали путами, а не коллами (об этом мы поговорим подробнее далее).

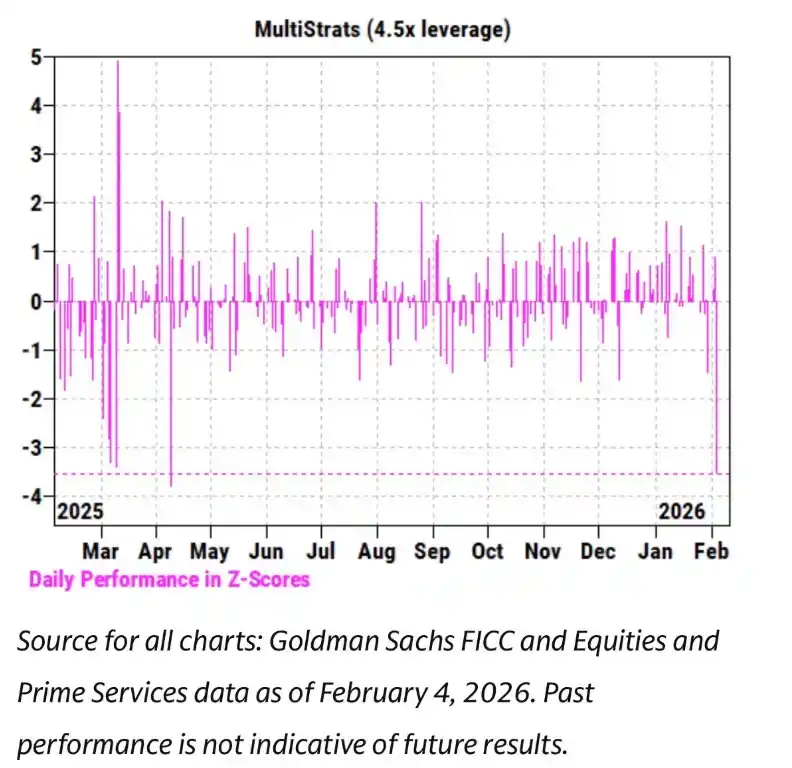

В то же время за последние несколько недель мы наблюдали чрезвычайно тесную корреляцию между динамикой IBIT и акциями софтверных компаний, а также другими рисковыми активами. Группа Prime Brokerage (PB) Goldman Sachs также сообщила, что 4 февраля стало одним из худших дней в истории для мультистратегических фондов с Z-score, достигшим 3,5. Это означает, что это экстремальное событие с вероятностью всего 0,05%, что в 10 раз реже, чем событие 3-sigma (классический порог «черного лебедя» с вероятностью около 0,27%). Можно сказать, что это был катастрофический шок. Именно после таких событий риск-менеджеры мультистратегических фондов (pod shop) быстро вмешиваются, требуя от всех торговых команд немедленного, безусловного и срочного делевериджа. Это объясняет, почему 5 февраля также превратилось в кровавую баню.

При таком количестве обновленных рекордов и четком нисходящем направлении цены (падение на 13,2% за день) мы изначально ожидали с очень высокой вероятностью увидеть чистый отток из ETF. Ссылаясь на исторические данные, такое предположение не было натянутым: например, 30 января IBIT, упав на 5,8% в предыдущий торговый день, показал рекордный отток в 530 миллионов долларов; или 4 февраля, на фоне непрерывного падения, IBIT показал отток около 370 миллионов долларов. Поэтому в рыночных условиях 5 февраля ожидать оттока средств как минимум на 5-10 миллиардов долларов было совершенно оправданно.

Но произошло обратное — мы увидели широкий чистый приток. В тот день IBIT добавил около 6 миллионов паев, что соответствует приросту активов под управлением более чем на 230 миллионов долларов. В то же время другие биткоин-ETF также зафиксировали приток средств, и вся система ETF в совокупности привлекла более 300 миллионов долларов чистого притока.

Этот результат несколько озадачивает. Теоретически можно с натяжкой предположить, что сильное ценовое ралли 6 февраля в некоторой степени снизило давление на вывод, но переход от «возможного сокращения оттока» к «чистому притоку» — это совсем другое дело. Это означает, что, скорее всего, одновременно сыграли роль несколько факторов, но эти факторы не складываются в единую, линейную нарративную структуру. Основываясь на информации, которой мы располагаем на данный момент, можно выдвинуть несколько разумных предпосылок, и на их основе я изложу свою общую версию.

Во-первых, эта распродажа биткоина, вероятно, затронула определенный тип мульти-ассетных портфелей или стратегий, не являющихся чисто криптовалютными. Это могли быть упомянутые выше мультистратегические хедж-фонды, а также такие структуры, как бизнес модельных портфелей BlackRock, которые распределяли средства между IBIT и IGV (софтверный ETF) и были вынуждены проводить автоматическую ребалансировку в условиях сильной волатильности.

Во-вторых, ускорение распродажи биткоина, вероятно, связано с опционным рынком, особенно со структурами, связанными с нисходящим направлением.

В-третьих, эта распродажа в конечном итоге не превратилась в отток средств на уровне активов биткоина, что означает, что основная движущая сила行情 исходила из «системы бумажных денег», то есть от корректировки позиций,主导 которой были дилеры и маркет-мейкеры, в целом находившиеся в хеджированном состоянии.

Основываясь на вышеизложенном, моя текущая ключевая гипотеза такова.

1. Непосредственным катализатором этой распродажи стал широкий делеверидж, triggered когда корреляция падения рисковых активов достигла статистически аномального уровня в мульти-ассетных фондах и портфелях.

2. Этот процесс, в свою очередь, спровоцировал чрезвычайно резкий делеверидж, который также включал в себя биткоин-экспозицию, но значительная часть этого риска фактически находилась в хеджированных «дельта-нейтральных» позициях, таких как базисные сделки, сделки относительной стоимости (например, биткоин против крипто-акций) и другие структуры, где остаточный дельта-риск обычно «упаковывается» дилерской системой.

3. Этот делеверидж затем вызвал эффект шорт гаммы, который дополнительно усилил нисходящее давление, вынудив дилеров продавать IBIT. Но поскольку распродажа была слишком стремительной, маркет-мейкеры были вынуждены чисто шортить биткоин, не считаясь с собственными инвентарями. Этот процесс, в свою очередь, создал новые инвентари ETF, тем самым снизив изначальные ожидания рынка относительно大规模 оттока средств.

Затем, 6 февраля, мы наблюдали положительный приток средств в IBIT, некоторые покупатели IBIT (вопрос в том, к какой категории они принадлежали) выбрали возможность配置 на падении, что further компенсировало возможный незначительный чистый отток.

Во-первых, я лично склоняюсь к тому, что первоначальным катализатором события стала распродажа софтверных акций, особенно учитывая высокую корреляцию, продемонстрированную между биткоином и софтверными акциями, которая даже выше, чем с золотом. Пожалуйста, обратитесь к двум приведенным ниже графикам.

Это логично, потому что золото обычно не является активом, которым в large объемах владеют мультистратегические фонды, участвующие в маржинальной торговле, хотя оно может присутствовать в модельных портфелях RIA (заранее разработанные схемы распределения активов). Поэтому, на мой взгляд, это further подтверждает вывод о том, что эпицентр этой нестабильности, скорее всего, находится within системы мультистратегических фондов.

И поэтому第二个 вывод кажется более reasonable: этот резкий процесс делевериджа действительно включал в себя биткоин-риск, находившийся в хеджированном состоянии. В качестве примера можно привести базисные сделки с биткоином на CME, которые долгое время были одной из самых предпочитаемых стратегий мультистратегических фондов.

Если посмотреть на полные данные с 26 января по вчерашний день, охватывающие базисы CME по биткоину на 30, 60, 90, 120 дней (благодарим ведущего отраслевого исследователя @dlawant за предоставленные данные), можно清楚地看到, что ближний базис 5 февраля подскочил с 3,3% до 9%. Это один из самых больших скачков, которые мы лично наблюдали на рынке с момента запуска ETF, что почти однозначно указывает на вывод: базисные сделки были принудительно закрыты по指令.

Just представьте себе такие institutions, как Millennium, Citadel, вынужденные强行平掉 базисные позиции (продавая спот, покупая фьючерсы). Учитывая их объем в системе биткоин-ETF,不难 понять, почему эта операция оказала такое резкое impact на общую рыночную структуру. Я и ранее писал о своих размышлениях на этот счет.

Редакционное дополнение: В настоящее время大量这种不加区分的抛售 в США, вероятно, исходит от мультистратегических хедж-фондов. Эти фонды часто используют стратегии дельта-хеджирования или запускают某种относительной стоимости (RV) или факторно-нейтральные сделки, которые в настоящее время расширяют спреды, возможно, accompanied перетеканием корреляции акций роста.

Грубая оценка: около 1/3 биткоин-ETF принадлежит институциональным типам, и about 50% (возможно, больше) из них считаются принадлежащими хедж-фондам. Это相当可观的流动快钱, которые很容易 капитулировать и закрываться, когда стоимость финансирования или требования к марже растут в условиях current высокой волатильности и вмешиваются риск-менеджеры, особенно когда базисный доход больше не стоит премии за риск. Стоит отметить, что сегодня объем торгов MSTR в долларах является одним из самых high в its истории.

Вот почему最大的因素最容易导致 хедж-фондов обанкротиться — это печально известный «риск совладельца»: несколько, казалось бы, независимых фондов hold高度相似的экспозиции, и когда рынок падает, все одновременно устремляются к одному узкому выходу, заставляя все нисходящие корреляции стремиться к 1. Продажа в таких условиях poor ликвидности — это классическое «закрытие риска», которое мы сегодня и наблюдаем. В конечном итоге это отразится в данных о потоках ETF. Если эта гипотеза верна, я подозреваю, что после всей этой清算ки цена быстро переоценится, однако восстановление доверия займет некоторое время.

Это подводит нас к第三条线索.既然 мы поняли, почему IBIT был распродан на фоне широкого делевериджа, то вопрос заключается в следующем: что именно ускорило падение? Возможным «катализатором» могли стать структурированные продукты. Хотя я не считаю, что市场规模结构турированных продуктов достаточно, чтобы单独 вызвать эту распродажу,但当所有因素以一种超出任何 VaR(风险价值)模型预期的方式异常且完美地同时对齐时, они完全有可能成为触发连锁清算行为的急性事件.

Это сразу же напомнило мне мой опыт работы в Morgan Stanley. Там структурированные продукты с knock-in put барьерами (опцион «активируется» и становится действующим пут-опционом только тогда, когда цена базового актива достигает/преодолевает определенный барьерный уровень) часто имели极具破坏性的 последствия. В некоторых случаях дельта опциона могла изменяться более чем на 1, что даже не учитывается в модели Black-Scholes — потому что в стандартной框架 Black-Scholes для обычных ванильных опционов (самые basic европейские кол/пут) дельта опциона никогда не может превышать 1.

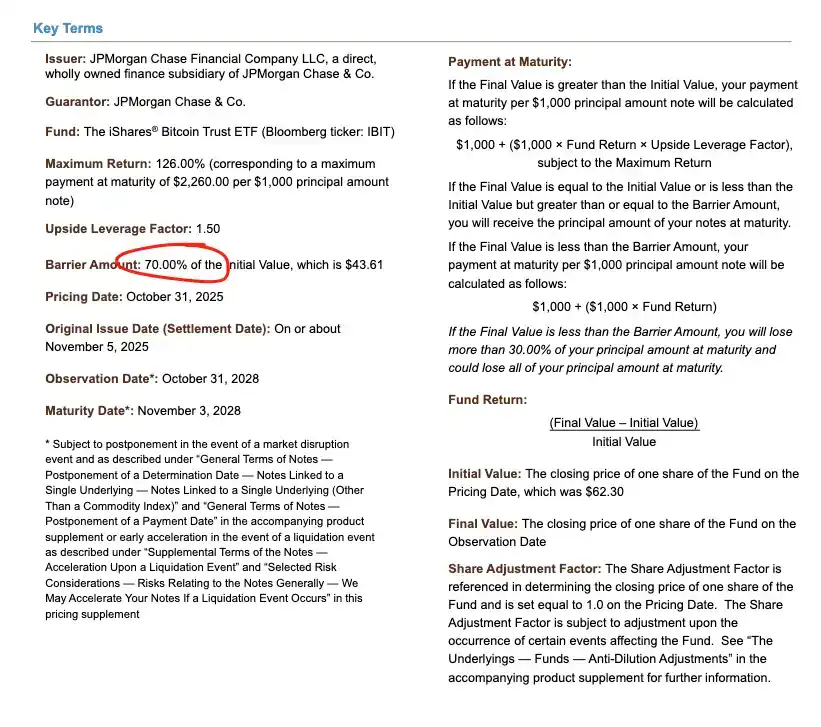

Возьмем, к примеру, note, выпущенный JP Morgan в ноябре прошлого года,可以看到其敲入障碍位正好设在 43.6. Если这些票据在 12 月继续发行,而比特币价格又下跌了 10%,那么可以想象,在 38–39 区间将堆积大量敲入障碍,这正是所谓的«风暴眼».

В случае пробития этих барьеров, если дилеры хеджировали риск knock-in, продавая, например, пут-опционы, то при negative ванна-динамике скорость изменения гаммы будет极其迅猛. В этот момент единственно可行ный способ действий для дилера — это агрессивно продавать базовый актив на ослаблении рынка. Именно это мы и наблюдали: подразумеваемая волатильность (IV) рухнула до исторических экстремумов,接近 90%, почти до состояния катастрофического сжатия, и в таких условиях дилеры были вынуждены увеличить объем шортов по IBIT до такой степени, что в конечном итоге создали чистые новые паи ETF. Эта часть действительно требует определенного пространства для размышлений, и без более detailed данных по спредам也难以 полностью подтвердить, но учитывая рекордный объем торгов в тот день и активное участие уполномоченных участников (AP), такая ситуация вполне могла произойти.

Если结合这个负 Vanna 动态与另一个事实, логика становится еще более清晰.由于此前一段时间整体波动率偏低,加密原生市场的客户在过去几周中普遍倾向于买入看跌期权.这意味着,加密交易商本身就处于天然的空 Gamma 状态,而且在定价上低估了未来可能出现的超幅波动.当真正的大幅行情出现时,这种结构性失衡进一步放大了下行压力.下方的仓位分布图也清楚地显示了这一点,在 6.4 万至 7.1 万美元区间,交易商主要集中在看跌期权的空 Gamma 头寸上.

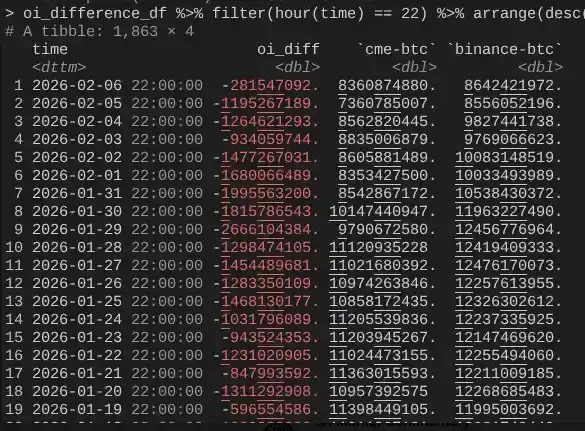

Это возвращает нас к 6 февраля, когда биткоин совершил мощное ралли более чем на 10%. В этот момент值得注意的现象是, что открытый интерес (OI) на CME расширялся明显 быстрее, чем на Binance (再次感谢 @dlawant за синхронизацию почасовых данных до 16:00 по восточному времени США). С 4 по 5 февраля可以清楚看到 CME OI 的明显坍塌,这再次印证了基差交易在 2 月 5 日被大规模平仓的判断;而在 2 月 6 日,这部分头寸可能重新建立,以利用更高的基差水平,从而抵消了资金流出的影响.

На этом整个逻辑链条重新闭合: IBIT в плане申购与赎回大致持平, потому что CME базисные сделки восстановились; но цена все еще偏低, потому что OI на Binance показал明显坍塌, что означает, что значительная часть давления делевериджа исходила от шорт гаммы позиций и форс-клосов в加密原生市场.

Вышеизложенное — мое лучшее объяснение поведения рынка 5 февраля и последующего 6 февраля. Это рассуждение основано на нескольких предположениях и не полностью удовлетворительно, потому что у него нет четкого «виновника», которого можно винить (как в случае с FTX). Но核心结论 таков: спусковым крючком этой распродажи послужили действия по снижению рисков в традиционных финансах, не связанных с криптовалютами, и этот процесс恰好 подтолкнул цену биткоина к интервалу, где хеджирование шорт гаммы ускоряет падение. Это падение было驱动не направленным медвежьим настроем, а triggered хеджевым спросом, и в конечном итоге быстро развернулось 6 февраля (к сожалению, это разворот в основном принес пользу рыночно-нейтральным капиталам в традиционных финансах, а не направленным стратегиям加密原生)). Хотя этот结论未必令人兴奋,但至少可以让人稍感安心的是:前一日的抛售,很可能与 10/10 事件并无关系.

Да, я не считаю, что произошедшее на прошлой неделе является продолжением процесса делевериджа 10/10. Я читал статью, в которой暗示лось, что эта нестабильность могла исходить от неамериканского фонда со штаб-квартирой в Гонконге, который участвовал в кэрри-трейде иен и в конечном итоге потерпел неудачу. Но у этой теории есть два очевидных изъяна. Во-первых, я не верю, что существует не-криптовалютный prime broker, который愿意 предоставлять услуги для如此复杂的 мульти-ассетных сделок,同时还提供长达 90 天的 маржинальный缓冲, и при ужесточении风险框架 еще не оказался бы в состоянии неплатежеспособности. Во-вторых, если кэрри-трейд资金是通过购买 IBIT 期权来 «脱困»,那么比特币价格下跌本身并不会加速风险释放——这些期权只会变成价外,其希腊值迅速归零.这意味着,这笔交易本身必须包含真实的下行风险.如果有人一边做多美元/日元套息,一边卖出 IBIT 看跌期权,那么这样的主经纪行,坦率说,根本不配继续存在.

Следующие несколько дней будут极其关键,因为我们将获得更多数据, чтобы判断, используют ли инвесторы это падение для формирования нового спроса, и если да, то это будет очень бычий сигнал. На данный момент я довольно воодушевлен потенциальным притоком средств в ETF. Я по-прежнему firmly верю, что настоящие покупатели ETF в стиле RIA (а не хедж-фонды относительной стоимости) — это проницательные инвесторы, и на институциональном уровне мы наблюдаем множество реальных и глубоких进展ов, что十分明显 в процессе продвижения всей отрасли и среди моих друзей в Bitwise. Поэтому я уделяю пристальное внимание чистому притоку средств, не accompanied扩张ом базисных сделок.

Наконец, все это также再次表明, что биткоин интегрировался в全球金融овые рынки капитала极其复杂ым и зрелым образом. Это также означает, что когда рынок в будущем окажется на стороне обратного сжатия, восходящий тренд будет более крутым, чем когда-либо прежде.

Хрупкость правил маржи в традиционных финансах — это антихрупкость биткоина. Как только начнется ценовое ралли — а я считаю это неизбежным, особенно после того, как Nasdaq повысил лимиты на открытый интерес по опционам — это будет极其壮观ное зрелище.