Автор: Prathik Desai

Перевод: Block unicorn

Предисловие

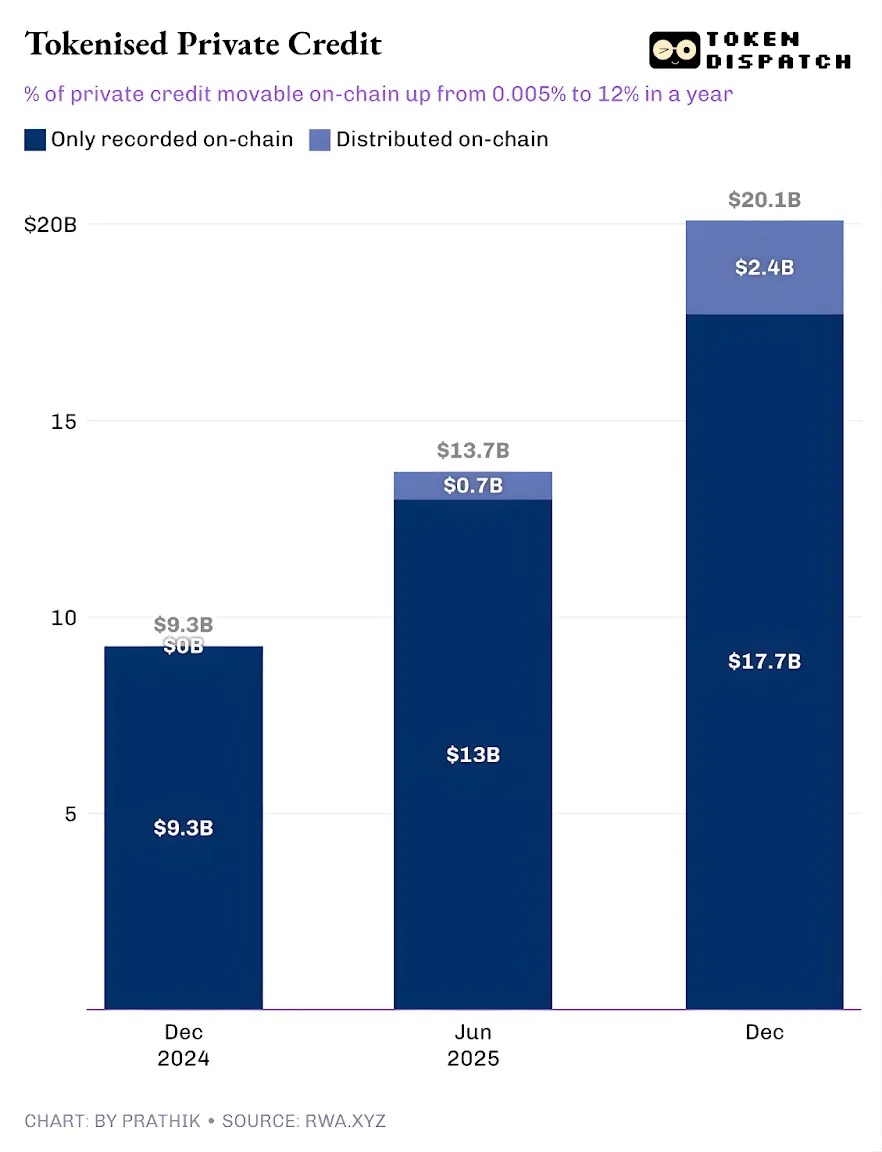

На платформах токенизации реальных активов (RWA) частное кредитование находится на переднем крае развития. За последний год токенизированное частное кредитование стало самой быстрорастущей категорией, увеличившись с менее чем 50 000 долларов до примерно 2,4 миллиарда долларов.

Если исключить стейблкоины (чьи платежные каналы охватывают всю ончейн-активность), токенизированное частное кредитование уступает только ончейн-товарам. К ведущим токенизированным товарам относятся золотые ноты Tether и Paxos, а также токены Justoken, обеспеченные хлопком, соевым маслом и кукурузой. Это кажется серьезной категорией с реальными заемщиками, денежными потоками, механизмами андеррайтинга и доходностью, которая, в отличие от товаров, менее зависима от рыночных циклов.

Но история усложняется, если копнуть глубже.

Эти 2,4 миллиарда долларов непогашенного токенизированного частного кредита составляют лишь небольшую часть от общего объема непогашенных кредитов. Это говорит о том, что лишь часть активов действительно может храниться и передаваться в виде токенов в блокчейне.

В сегодняшней статье я рассмотрю реальность, стоящую за цифрами токенизированного частного кредитования, и то, что эти цифры означают для будущего этой категории.

Давайте перейдем к делу.

Двойной лик токенизированного частного кредита

Общий объем активных кредитов на платформе RWA.xyz составляет чуть более 19,3 миллиарда долларов. Однако только около 12% этих активов могут храниться и передаваться в токенизированной форме. Это иллюстрирует двойственность токенизированного частного кредитования.

Одна сторона — это «репрезентативный» токенизированный частный кредит, где блокчейн предоставляет лишь операционные улучшения, создавая в цепи реестр непогашенных кредитов для записи займов, происходящих с традиционного рынка частного кредитования. Другая сторона — это дистрибутивное улучшение, где рынки, работающие на блокчейне, сосуществуют с традиционными (офчейн) рынками частного кредитования.

Первое используется только для учета, сверки и записи в публичном реестре. А распределенные активы можно переводить в кошельки для передачи.

Как только мы поймем эту систему классификации, вы перестанете спрашивать, находится ли частный кредит в блокчейне. Вместо этого вы зададите более острый вопрос: сколько активов частного кредитования originates from the blockchain? Ответ на этот вопрос может быть более показательным.

Траектория развития токенизированного частного кредитования обнадеживает.

До прошлого года почти весь токенизированный частный кредит был лишь операционным улучшением. Кредиты уже существовали, заемщики исправно платили, платформы работали, а блокчейн лишь фиксировал эту активность. Весь токенизированный частный кредит лишь записывался в блокчейне, но не мог передаваться как токен. За год эта доля передаваемых ончейн-активов выросла до 12% от отслеживаемого общего объема частного кредитования.

Это демонстрирует рост токенизированного частного кредитования как распространяемого ончейн-продукта. Это позволяет инвесторам владеть долями в фондах, пуловыми токенами, нотами или структурированными инвестиционными продуктами в форме токенов.

Если эта модель распределения продолжит расширяться, частный кредит будет меньше походить на кредитную книгу, а больше на инвестируемый класс ончейн-активов. Этот сдвиг изменит выгоду, которую кредиторы получают от сделки. Помимо дохода, кредиторы получат инструмент с более высокой операционной прозрачностью, более быстрым расчетом и более гибким кастодиальным решением. Заемщики получат доступ к финансированию, не зависящему от единственного канала распределения, что может быть большим преимуществом в условиях избегания риска.

Но кто будет двигать рост рынка распределяемого частного кредита?

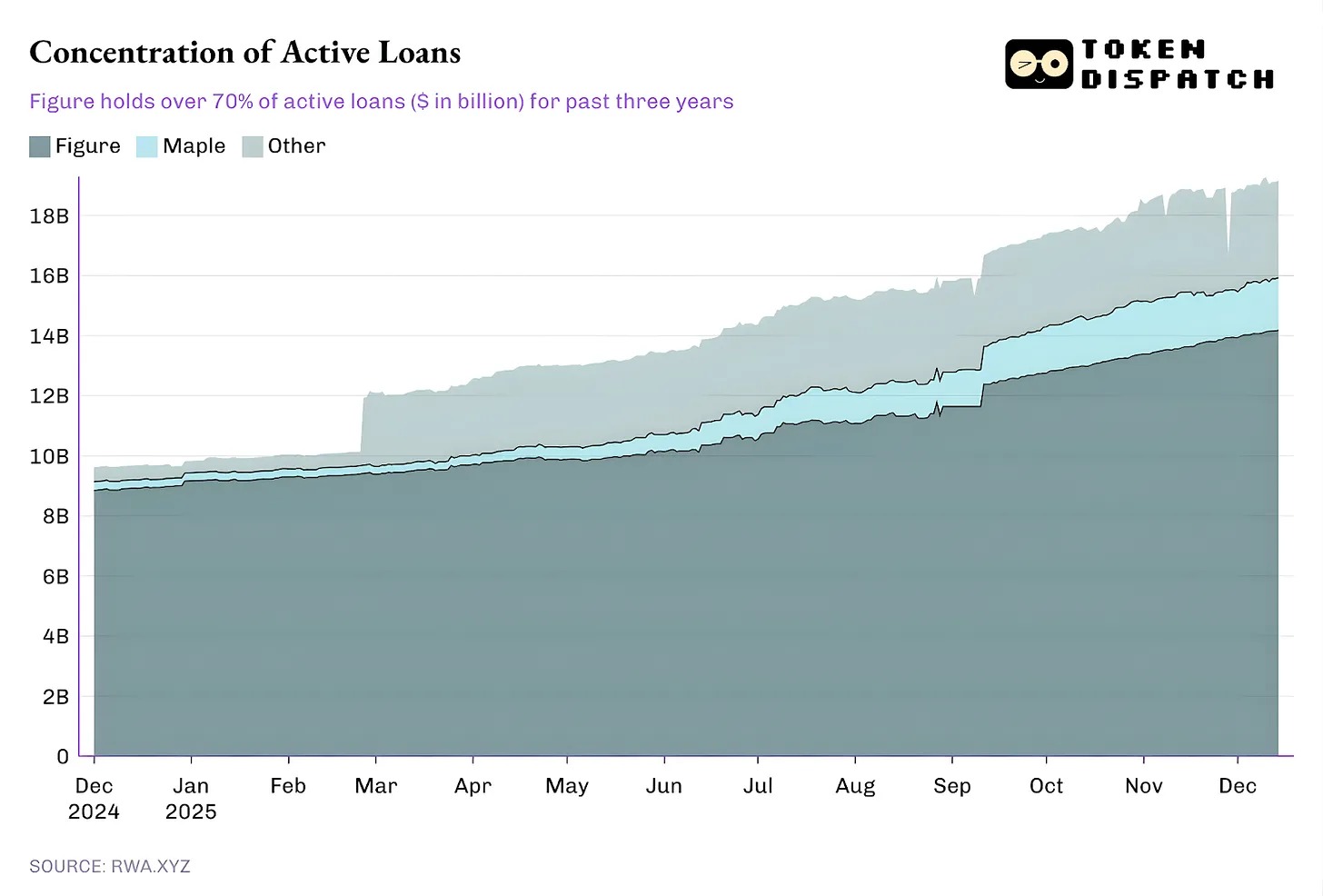

Эффект Figure

В настоящее время большая часть непогашенных кредитов поступает с одной платформы, а остальная часть экосистемы образует длинный хвост.

С октября 2022 года Figure монополизировала рынок токенизированного частного кредитования, но ее доля рынка снизилась с более чем 90% в феврале до нынешних 73%.

Но более интересна модель частного кредитования Figure.

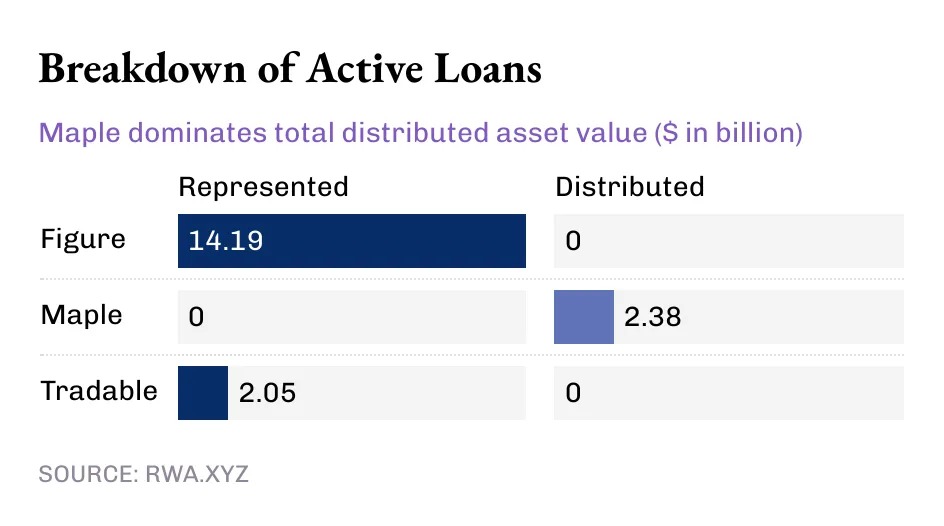

Хотя сегодня объем токенизированного частного кредитования превышает 14 миллиардов долларов, вся стоимость этого отраслевого лидера выражена в «репрезентативной» стоимости активов, в то время как распределенная стоимость равна нулю. Это указывает на то, что модель Figure — это операционный конвейер, который записывает выдачу кредитов и право собственности в блокчейне Provenance.

Между тем, некоторые более мелкие игроки продвигают дистрибуцию токенизированного частного кредита.

Figure и Tradable хранят весь свой токенизированный частный кредит как репрезентативную стоимость, в то время как стоимость Maple полностью распределяется через блокчейн.

С макроскопической точки зрения, подавляющая часть текущих 19 миллиардов долларов ончейн-кредитов записана в блокчейне. Но тенденция последних месяцев неоспорима: все больше частного кредита распределяется через блокчейн. Учитывая огромный потенциал роста токенизированного частного кредитования, эта тенденция будет только усиливаться.

Даже при объеме в 19 миллиардов долларов, RWA в настоящее время составляют менее 2% от общего объема рынка частного кредитования в 1,6 триллиона долларов.

Но почему важно, чтобы частный кредит был «перемещаемым, а не просто записанным»?

Перемещаемый частный кредит предлагает не только ликвидность. Получение экспозиции к частному кредиту вне платформы через токены обеспечивает портативность, стандартизацию и более высокую скорость распределения.

Активы, полученные через традиционные каналы частного кредитования, заставляют держателя оставаться в рамках экосистемы конкретной платформы. В таких экосистемах ограничены окна передачи, а процессы вторичных торгов громоздки. Кроме того, переговоры на вторичном рынке продвигаются медленно и в основном ведутся профессионалами. Это дает существующей рыночной инфраструктуре гораздо больше власти, чем держателям активов.

Распределяемые токены могут уменьшить это трение за счет более быстрого расчета, более четкого изменения права собственности и более простого кастодиального решения.

Что еще более важно, «перемещаемость» является предпосылкой для массовой стандартизированной дистрибуции частного кредита, чего исторически не хватало в этом секторе. В традиционной модели частный кредит представлен в виде фондов, бизнес-компаний развития (BDC) и обеспеченных кредитных обязательств (CLO), каждый из которых добавляет множество посредников и непрозрачных комиссий.

Ончейн-дистрибуция предлагает другой путь: программируемые обертки на уровне инструмента обеспечивают соблюдение нормативных требований (белые списки), правила движения денежных средств и раскрытие информации, а не ручные процессы.