Автор: Ли Цзя

Источник: Wall Street News

Война и доходы идут рука об руку. В то время как рынок горячо обсуждает, затормозит ли конфликт на Ближнем Востоке мировую экономику, индексы S&P 500 и Nasdaq снова обновили исторические максимумы. Что же война означает для американского фондового рынка?

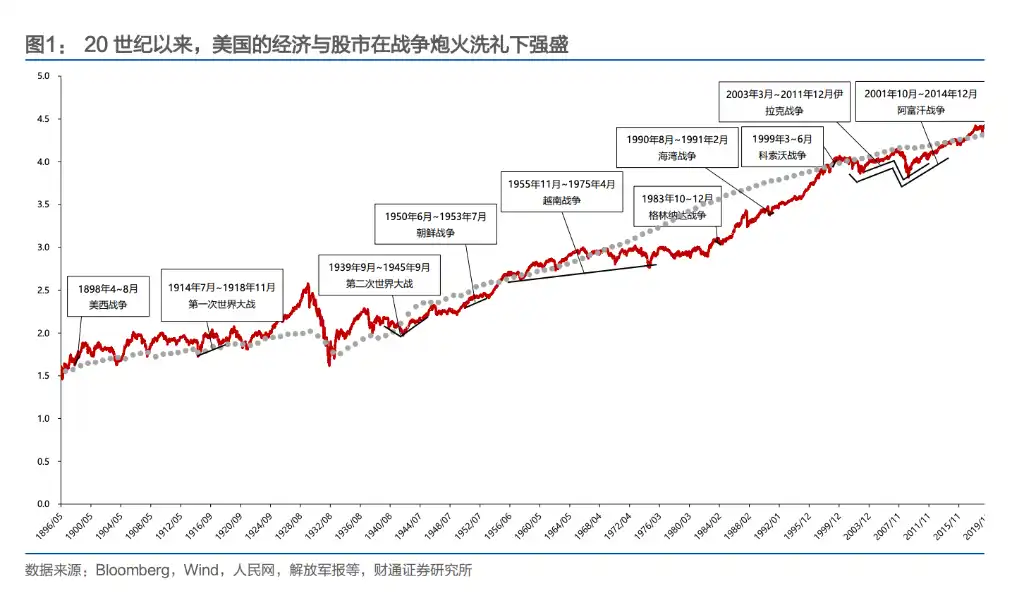

Отчет компании Caitong Securities дает прямой ответ: между войной и долгосрочным бычьим трендом на американском рынке нет противостояния, скорее, они почти сосуществуют в симбиозе. Исторические показатели индекса Доу-Джонса подтверждают это: во время испано-американской войны рост составил 28%, во время Корейской войны — 26%, 19-летняя война во Вьетнаме все же принесла рост индекса более чем на 80%, а война в Афганистане, захватившая период до и после финансового кризиса 2008 года, привела к почти удвоению индекса.

С конца XIX века, когда США стали крупнейшей экономикой мира, они в большинстве войн (кроме Вьетнамской) получали реальные выгоды. От захвата испанских колоний в испано-американской войне до наживы на двух мировых войнах, и далее до войны в Персидском заливе и последующих мелких конфликтов вокруг нефтяных ресурсов, США совершили переход от «участника войны» к «инициатору войны».

Реакция американского фондового рынка на войну также следует четкой траектории: во время Второй мировой войны и ранее войны в основном влияли на рынок через эмоциональный шок; начиная с Корейской войны, этот прямой эффект постепенно ослабевал, и война все больше стала воздействовать на фондовый рынок через экономические каналы, такие как инфляция, цены на нефть и бюджетный дефицит.

Война во Вьетнаме стала для США единственной «убыточной» войной, которая глубоко изменила их военную логику. Практически все конфликты, инициированные США с тех пор, обладают тремя характеристиками: короткая продолжительность, ограниченное пространство и разворачиваются вокруг нефти — и в конечном итоге все они достигают поставленных целей.

От «грабежа во время пожара» до активного провоцирования: три поворотных момента в стратегии ведения войны США

Испано-американская война 1898 года стала первой важной войной, которую США начали по собственной инициативе. В то время внутренние монополистические концерны остро нуждались в новых рынках, местах для инвестиций и источниках сырья, а дряхлеющая испанская колониальная империя стала идеальной целью. После войны США получили контроль над Кубой, а также Филиппинские острова, Гуам и Пуэрто-Рико. Промышленный индекс Доу-Джонса за три месяца войны вырос на 28%, причем синхронно с победами на фронте.

Когда разразилась Первая мировая война, США первоначально сохраняли нейтралитет. В период закрытия рынков в июле 1914 года инвесторы осознали, что США станут крупнейшим бенефициаром европейского конфликта — удаленная от поля боя страна сможет продолжать производство и экспортировать оружие в Европу. К 1917 году американские банки, включая Morgan, уже предоставили правительствам Великобритании и Франции кредиты на сумму 10 миллиардов долларов для покупки оружия. Хотя после официального вступления в войну в апреле 1917 года индекс упал почти на 10%, промышленный индекс с минимальной точки в 1914 году по март 1917 года уже вырос примерно на 107%.

Вторая мировая война стала ключевым сражением, заложившим основы глобального лидерства США. В начале войны в сентябре 1939 года американские акции упали из-за подавления ожиданий корпоративной прибыли «налогом на сверхприбыль» — Конгресс ввел многоуровневую налоговую ставку до 95% на прибыль предприятий сверх 5000 долларов, что серьезно ударило по «числителю» в модели DDM. Только после битв в Коралловом море и у атолла Мидуэй в мае 1942 года, переломивших ход войны, инвесторы остро почувствовали изменение ситуации, и американский рынок заранее развернулся от дна. Промышленный индекс вырос на 82% во второй половине войны, транспортный — на 127%, а коммунальный — на 203%.

Корейская война стала первой войной, которую США «не выиграли». Хотя спрос на оружие стимулировал ослабевшую после войны экономику, американские войска не достигли поставленных целей. Тем не менее, промышленный индекс Доу-Джонса за весь период все равно вырос на 26%, а транспортный индекс взлетел на 86%.

Война во Вьетнаме стала водоразделом. Это единственная война, которую США проиграли и не получили от нее выгоды.

Оборонный бюджет США вырос с 49,6 млрд долларов в 1961 году до 81,9 млрд долларов в 1968 году (43,3% федерального бюджета), бюджетный дефицит увеличился с 3,7 млрд до 25 млрд долларов, инфляция выросла с 1,5% до 4,7%. Доля ВВП США в мировом объеме производства снизилась с 34% до менее 30%. После войны военная стратегия США радикально изменилась: они отказались от масштабных наземных войн в пользу коротких, с малыми потерями конфликтов с упором на авиаудары и «войны по доверенности».

Последующие войны в Персидском заливе, Косово, Афганистане и Ираке без исключения были инициированы США под предлогом локальных конфликтов или «черных лебедей», места боевых действий в основном сосредоточены на Ближнем Востоке и Балканах, а ключевой целью был контроль над нефтяными ресурсами и спрос на оружие.

Изменение способа воздействия войны на фондовый рынок: от эмоций к экономике

Во время Второй мировой войны и ранее военные события часто напрямую влияли на настроения инвесторов. Победы в битвах в Манильском заливе и заливе Сантьяго во время испано-американской войны приводили к росту индекса примерно на 10% в течение десяти дней; в то время как новости о вступлении США в две мировые войны часто вызывали панические распродажи.

Но начиная с Корейской войны, это прямое влияние постепенно ослабевало. С ноября 1950 по февраль 1951 года, когда корейско-американские войска терпели одно поражение за другим, американский фондовый рынок продолжал расти. Причина заключалась в том, что экономика, застопорившаяся после Второй мировой, вновь заработала во время Корейской войны: в 1950 году реальный ВВП США вырос примерно на 8,7%, а в 1951 году продолжал держаться выше 8%. Фискальная экспансия, вызванная войной, стала катализатором экономического восстановления.

Во время войны во Вьетнаме этот переход стал еще более очевидным. Битва в долине Йа-Дранг в ноябре 1965 года (первое крупное сражение для США во Вьетнаме) не оказала заметного влияния на рынок; «Тетское наступление», начатое Северным Вьетнамом в начале 1968 года, также не смогло остановить американский рынок от обновления максимумов. Настоящими драйверами рынка были ужесточение кредитных условий ФРС в 1966 году в ответ на расходы на войну во Вьетнаме, а также два экономических спада в 1969-1970 и 1973-1975 годах. Эмоции от войны уступили место макроэкономической политике и корпоративным прибылям.

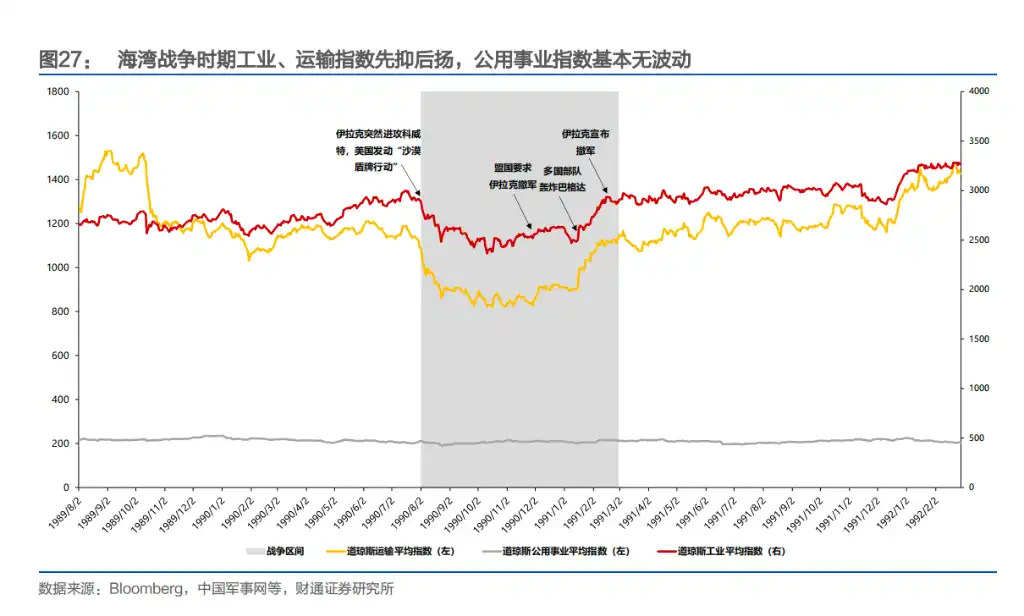

Война в Персидском заливе предоставила самый наглядный пример «экономической трансмиссии». После нападения Ирака на Кувейт в августе 1990 года цены на нефть взлетели, рынок ожидал рецессии в американской экономике, и оценка S&P 500 достигла дна. В январе 1991 года, после бомбардировок Багдада коалиционными силами, цены на нефть упали до довоенного уровня, а рынок синхронно отскочил вверх. Во время войны индекс Доу-Джонса и цены на нефть двигались почти идеально в противоположных направлениях — рынок торговал компромисс между инфляцией и ростом.

Война в Афганистане 2001 года и война в Ираке 2003 года еще больше подтвердили эту закономерность. Наиболее символичным, пожалуй, стало убийство Усамы бен Ладена в мае 2011 года — событие, которое должно было стать прорывным моментом в афганской войне, на следующий день индекс Доу упал лишь на 0,02%, а S&P 500 — на 0,18%. Рынок практически полностью проигнорировал эту новость.

Подводя итог, реакция американского фондового рынка на войну прошла четкий путь эволюции: от «доминирования эмоций» к «экономической трансмиссии». Ранние войны напрямую сотрясали рынок новостями о победах и поражениях, а начиная с Корейской войны рынок все больше стал фокусироваться на реальных экономических переменных: фискальной экспансии, инфляционных ожиданиях, волатильности цен на нефть и денежно-кредитной политике.

Сама по себе война перестала быть причиной роста или падения. То, как война влияет на рост и издержки, стало настоящим объектом оценки для рынка.

Какая отрасль зарабатывает на войне? Ответ меняется

Во время Второй мировой войны уголь был кровью войны, его доля выросла с 43,8% до войны до 48,9%, отрасль в целом выросла на 415%.

В Корейской войне нефть сменила его в качестве нового главного героя, добыча и переработка нефти заняли первые два места по росту, доходность росла с середины 1950 года до первой половины 1952 года. Во время войны во Вьетнаме распад Бреттон-Вудской системы вынудил обесценить доллар, ОПЕК получила право повышать цены для компенсации потерь, отрасль добычи нефти взорвалась во время долларового кризиса с конца 1970 до начала 1973 года, за всю войну рост составил 1378%.

Косовская война продолжила эту модель, сырьевые и энергетические отрасли показали наилучшие результаты.

Война в Персидском заливе стала единственным исключением — путь трансмиссии сместился в сторону косвенной модели «цена на нефть → экономические ожидания», краткосрочно преобладали потребительские товары первой необходимости и здравоохранение, в то время как энергетика, сырье, промышленность и другие капиталоемкие отрасли оказались в аутсайдерах.

Стоит отметить тенденцию: по мере роста экономики США военно-промышленный комплекс превратился из двигателя роста в фундамент экономики. Маржинальный вклад отдельной войны в общий объем продолжает снижаться, драйверы фондового рынка все чаще уступают место макроэкономическим переменным, таким как инфляция, процентные ставки и бюджетный дефицит.