Автор |Odaily Planet Daily(@OdailyChina)

Автор|Golem(@web3_golem)

6 апреля Polymarket объявил о крупном обновлении платформы в ближайших 2-3 неделях, включающем переход CTF и CLOB к версии V2, а также замену залогового обеспечения платформы с USDC.e на нативный стейблкоин Polymarket USD.

Согласно официальной информации, Polymarket USD обеспечен USDC в соотношении 1:1. Для большинства пользователей переход с USDC.e на Polymarket USD будет незаметным: интерфейс автоматически обработает всё, пользователю нужно лишь один раз подтвердить действие. Для продвинутых и API-трейдеров процесс может быть сложнее, но также не вызовет трудностей: им потребуется использовать функцию wrap() контракта доступа к залогу для обертывания своих USDC или USDC.e в Polymarket USD.

На поверхности кажется, что Polymarket просто меняет залоговый актив для торговли. По мере роста платформы продолжение использования USDC.e действительно стало риском. Еще в феврале Circle и Polymarket объявили о миграции с бриджированного USDC.e на нативный USDC, и сейчас это просто плановое продолжение сотрудничества.

Но Polymarket выбрал не прямое внедрение нативного USDC для замены USDC.e, а добавил оболочку, чтобы аккумулировать USDC в своем собственном пуле ликвидности. Имя этой оболочки — Polymarket USD. Таким образом, появление Polymarket USD определенно является «Еще кое-чем»(Прим. Odaily: One more thing — классическая традиция презентаций Apple,如今寓意企业压轴大戏、颠覆行业等动作).

Polymarket получает право эмиссии

Первый смысл этого события — Polymarket может аккумулировать пользовательские средства.

Раньше деньги, внесенные пользователями на Polymarket, превращались в USDC.e. Можно провести аналогию: Polymarket — это огромная торговая площадка, которая только отвечает за matching, ценообразование,清算, деньги проходят через нее, но сами деньги не принадлежат ее системе, Polymarket — не казначейство.

Но скоро всё изменится. После замены USDC.e на Polymarket USD Polymarket сможет протянуть руку к тем деньгам, которые изначально были лишь «транзитными». Как заявил официально Polymarket, пользовательский опыт не изменится, но фактически путь ончейн-расчетов behind the scenes был изменен. Это преобразование не уступает переходу биржи от зависимости от сторонних расчетных палат к созданию собственного расчетного центра.

Polymarket USD обеспечен USDC 1:1, то есть, сколько будет Polymarket USD на рынке, столько же USDC будет в пуле ликвидности Polymarket. В настоящее время каждая пара Yes/No долей на Polymarket обеспечена USDC.e. Когда игроки делают ставки или проводят расчеты, USDC.e также перемещается в блокчейне. Но после перехода на Polymarket USD, хотя он также будет перемещаться в блокчейне при пользовательских операциях, USDC в пуле ликвидности Polymarket не будет двигаться. Поэтому, пока пользователи не приходят для выкупа, эти деньги, по сути, принадлежат Polymarket.

Polymarket из сценария использования стейблкоина, наоборот, получает право ончейн-эмиссии. Polymarket USD перенаправляет пользовательские активы из «открытого моря» во «внутреннее озеро» Polymarket. Как только средства начинают аккумулироваться, Polymarket перестает быть просто платформой для прогнозных рынков, и его бизнес-модель перестает ограничиваться только комиссиями за сделки, потому что он может начать играть в самую древнюю игру финансовых рынков — «деньги делают деньги».

Расширение каналов дохода Polymarket

Второй смысл этого события — расширение бизнеса Polymarket.

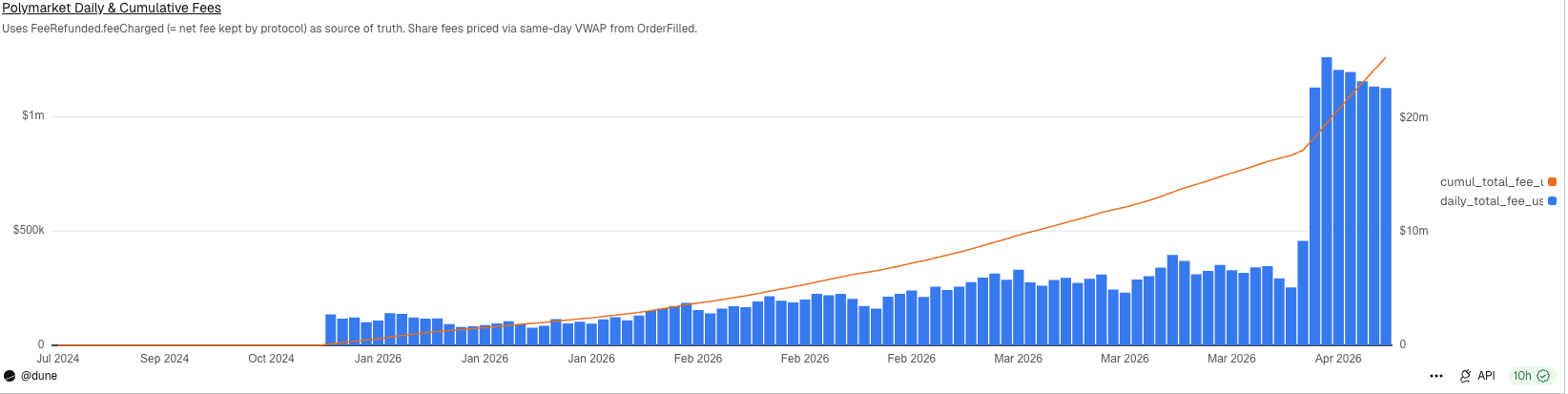

В настоящее время бизнес-модель прогнозных рынков проста — это сбор комиссий за транзакции. После корректировки механизма комиссий Polymarket 30 марта (Прим. Odaily: добавление категорий Finance, Politics, Economics, Culture, Weather в сферу взимания taker fee помимо原有 Crypto、Sports), ежедневный доход Polymarket от комиссий превысил 1 миллион долларов.

Ежедневный доход Polymarket от комиссий

Хотя это впечатляет, этого недостаточно для амбиций Polymarket. Прогнозные рынки, безусловно, являются самым популярным направлением на рынке, но потолок бизнес-модели не очень высок, защитный ров проекта также неглубок (регуляторные разрешения), а пользовательская лояльность невысока. В ситуации, когда все делают прогнозные рынки, как Polymarket может гарантировать, что в будущем его не обойдут конкуренты?

Сейчас его ответ таков: я не только организую сделки, но и могу оживить деньги игроков.

По своей бизнес-сути, самое соблазнительное в стейблкоинах за эти годы — это никогда не быстрые платежи и переводы, а скромный, но чрезвычайно прибыльный печатный станок behind the scenes — доход от резервных активов. В 2025 году подавляющая часть дохода Circle по-прежнему поступала от резервного дохода. Polymarket понял эту модель, поэтому запустил Polymarket USD.

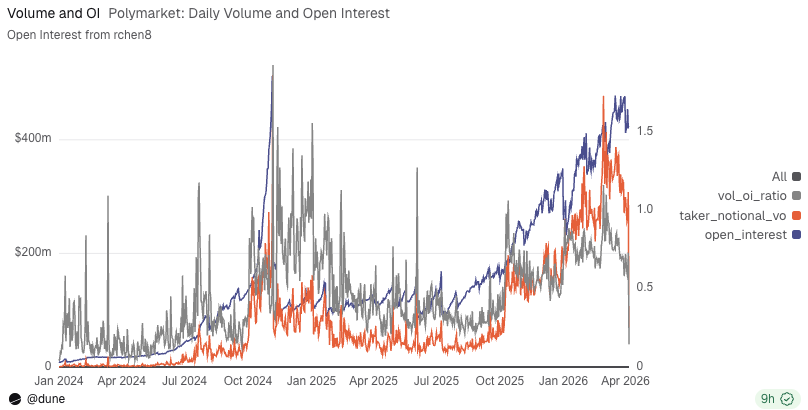

Согласно данным Dune, стоимость открытых позиций на платформе Polymarket превышает 400 миллионов долларов. Если все эти деньги будут конвертированы в Polymarket USD, Polymarket сможет просто разместить базовый обеспеченный USDC на институциональном счете Circle или в протоколе казначейских облигаций и, при безрисковой ставке 4-5%, ежегодно получать десятки миллионов долларов «процентного налога», ничего не делая.

Основатель Defillama 0xngmi напрямую написал, что в кошельках пользователей Polymarket находится около 1.25 миллиарда долларов. Если они сохранят этот процентный доход, то при текущих ставках будут получать дополнительно 54 миллиона долларов дохода в год. Более того, Polymarket может участвовать в DeFi-продуктах с более высокой APY, превращая замороженные средства пользователей на платформе прогнозов в живое плечо, а затем возвращая полученный доход пользователям, косвенно хеджируя их риски.

Кривая ежедневного OI и объема торгов Polymarket

Прогнозные рынки天然有两个特征,一是资金滞留,二是事件驱动下的高频再配置。用户的钱不会真像赌场那样秒进秒出,它要么已经在持仓,要么趴在账户里等下一场事件、下一轮赔率变化。这类钱,最适合被拿去金融再加工,而且对用户而言也有个美丽的借口:提高资金效率。

Конечно, Polymarket еще публично не объявил, что после выпуска стейблкоина обязательно будет заниматься извлечением дохода или ончейн-управлением активами. Но этот путь практически лежит на поверхности: как только масштаб Polymarket USD будет расти, у него естественным образом появится пространство для управления доходами, расширения залога и создания финансовых комбинаций внутри платформы.

Недавно Закон CLARITY столкнулся с сопротивлением из-за возможного запрета криптокомпаниям предоставлять пользователям проценты по стейблкоинам. Если итог споров все же останется запретом, все вышеописанные рассуждения о потенциале Polymarket USD превратятся в прах. Но 6 апреля, согласно сообщениям американских СМИ, ключевые разногласия между американским криптосообществом и банковским сектором относительно механизма доходности стейблкоинов, возможно, близки к разрешению. Хотя детали еще не раскрыты, общие ожидания оптимистичны, и Закон CLARITY может进入委员会审议阶段 в конце апреля.

Так что не думайте, что Polymarket еще далек от этого.

Polymarket получает право дистрибуции USDC

Запуск стейблкоина Polymarket имеет и третий смысл — получение права дистрибуции USDC.

Сегодня Polymarket仍然是USDC体系的一个大分发场景,Circle提供原生USDC,Polymarket分发USDC,双方其乐融融。Polymarket正值发展势头正猛的时候,毫无疑问未来其平台内沉淀的USDC储备会越来越大,甚至可能成为与Coinbase一样重要的分发渠道。真到那时,Polymarket和Circle的关系,可能也会变味。

Реальность мира стейблкоинов такова, что право эмиссии и право дистрибуции одинаково важны, поэтому Coinbase может уводить более половины резервного дохода Circle. Поэтому в будущем, когда Polymarket станет важным каналом дистрибуции USDC, у него неизбежно появится право торга, и он также получит право уводить большую долю резервного дохода. Более того, когда Polymarket USD достаточно созреет, можно будет исследовать стейблкоины с мульти-резервным обеспечением, а не висеть только на USDC.

Вот почему я считаю, что Polymarket USD — это не обычное обновление Polymarket, а смена идентичности. Polymarket превратится из «платформы, взимающей комиссии за волатильность событий», в платформу, которая также является «платформой для организации и расчетов вокруг доллара».

Первое — это логика казино, а второе — логика банка.

Защитный ров Polymarket因此又多了一道。它依旧维持着信息即市场、提前定价事实这套漂亮的叙事。但在商业模式上,它正在悄悄把自己往更重要的地方挪,不再满足于做市场的表层流量,不再满足于仅靠赔率吸引用户,也不再满足于把产业链中最肥的一块(资产储备收益)继续让给别人。