Editor's Note: Against the backdrop of accelerating AI, geopolitical conflicts, and a high-interest-rate cycle, the market discussion is shifting from 'How long can growth last?' to a more fundamental question: What happens when a debt-based system encounters a deflationary technological shock?

This article, starting from a series of current macroeconomic signals—such as rising sovereign debt pressure, energy price fluctuations, declining consumer confidence, and changes in employment structure—outlines a more tense picture: on one hand, AI brings unprecedented productivity gains; on the other, this 'efficiency dividend' may translate into demand contraction and default risks within a highly leveraged system, even amplifying systemic fragility. Meanwhile, the evolutionary paths of numerous historical asset bubbles also provide a reference point for the current狂热 in AI valuations.

Within this framework, the article brings the perspective back to the individual: when structural uncertainty becomes the norm, how should individuals build 'anti-cyclical capabilities' in terms of finance, career, and cognition. From cash flow defense and skill stacking to long-term asset allocation, the core is not about predicting inflection points, but about enhancing survival and choice-making abilities in an uncertain environment.

The following is the original text:

We are step by step moving towards a full-blown financial crisis. It will either make you or break you.

And this depends on two things: Do you choose to ignore it, or prepare in advance?

First, I must clarify a few points:

1. I am not a pessimist. But some of the content I will mention next might make it seem like I'm bearish. However, that's just reality itself; I am actually looking at all this with a relatively optimistic attitude.

2. Am I an expert? Of course not. But I will put my own money where my mouth is—both in market decisions and life choices.

I am also aware that, in the short term, the market might see a relief rally, or even rise (someone might quote this to mock me). But what I'm talking about is not this week's market movement, but a longer-term trend. Because I do spend time doing in-depth research, trying to understand what is happening. And right now, a lot is happening, and it's not just the war in Iran.

But we can start with this:

Oil, Energy, and That 'Invisible Tax'

War in the Middle East, destruction of critical infrastructure, threats of further destruction, escalation while pretending to 'de-escalate', plus the Strait issue—these factors will obviously push oil prices higher. And higher energy costs are essentially an 'invisible tax' that ultimately transmits through the entire supply chain, causing a comprehensive rise in the cost of living for ordinary people.

What happens next? Interest rates rise, people's financial pressure keeps getting squeezed, more and more people can't afford their mortgages, fail affordability assessments for refinancing, and are forced onto variable rates. And this rate could be double what they were paying during the low-rate era (e.g., a 1% fixed rate locked in last December).

Yes, the situation is not optimistic at all. In such an environment, consumer spending will be significantly compressed, even gradually 'suffocated'.

Oh, and right now, the US is trying its best to suppress this matter......

Sovereign Debt Death Spiral

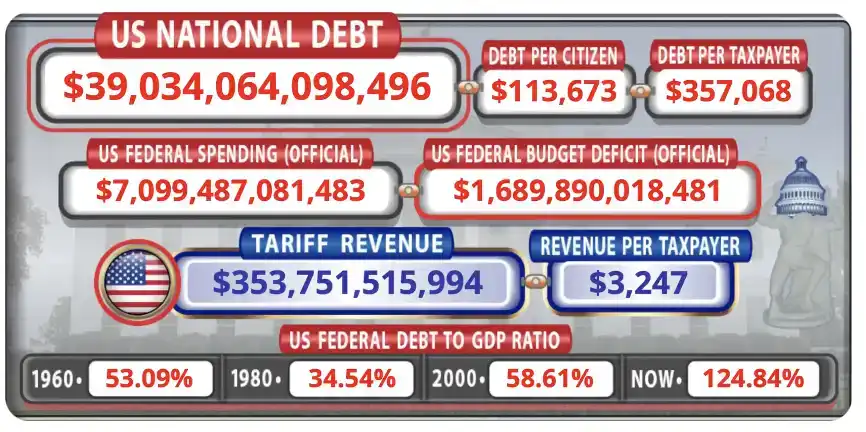

US national debt has just surpassed $39 trillion. That number alone is alarming enough.

At the same time, the government's annual revenue is only about $5.4 trillion, but spending is close to $7 trillion. About 120% of fiscal revenue is consumed by benefits for the baby boomer generation, interest on historical debt, and defense spending.

You can see these data in real-time on @USDebtClock_org.

It will only get worse from here. If the government cuts spending, GDP contracts, which ironically makes the 'deficit as a percentage of GDP' worse—a trap with no clean way out.

So, what have governments historically done when debt becomes mathematically impossible to repay? Either 'print money' (create currency out of thin air) or distract with war, sometimes both simultaneously.

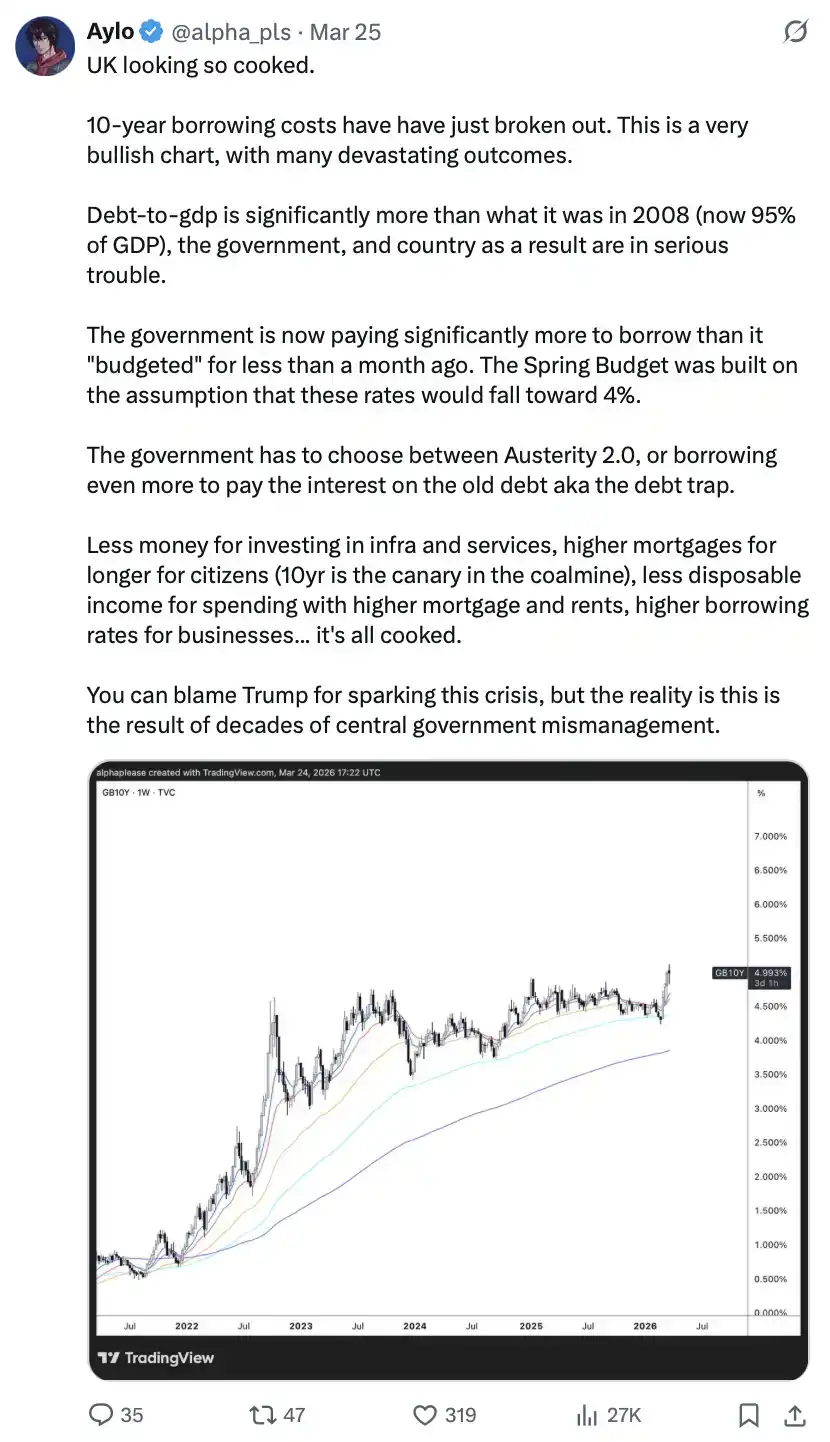

Across the Atlantic, your old friend the UK has already begun to fall into a 'vicious cycle': public sector wage increases exceeding inflation, forcing the government to raise taxes; higher taxes suppress economic growth; a weak economy then requires more 'money printing'. Rinse and repeat. Meanwhile, UK 30-year government bond yields have risen to their highest level since 2008, with the bond market effectively questioning the UK government's creditworthiness.

Looking globally, the narrowing yield spread between US 10-year Treasuries and Japanese Government Bonds (JGBs), coupled with a weakening Yen, is a textbook early warning signal of a 'sovereign debt death spiral'.

AI Deflation / Bubble Threat

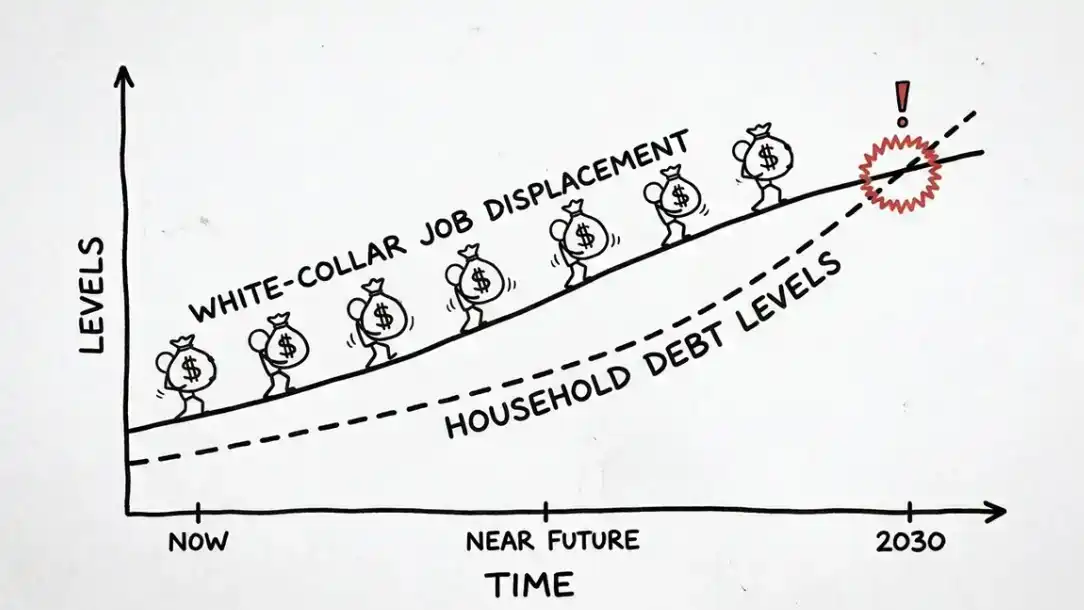

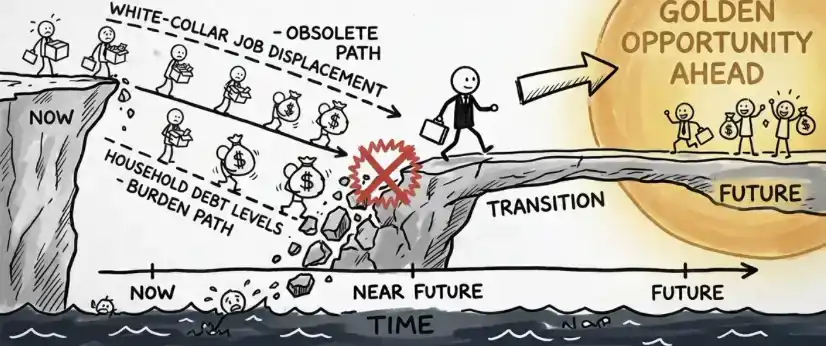

AI represents the fastest technological leap in human history, with massive productivity gains on the horizon. That sounds great until you realize the problem.

We are in a debt-based economic system. In a highly leveraged economy, large-scale 'deflationary productivity gains' don't bring prosperity; they can blow up the entire system. The white-collar crowd is普遍 burdened with mortgages, car loans, and non-dischargeable student debt. AI doesn't need to replace all jobs to trigger a crisis; even a small percentage of job losses can set off a chain reaction, eventually evolving into systemic defaults at the banking level.

Read that sentence once more. 'What if AI itself is a bubble?' The other side of the problem is: AI could also be a bubble, and bubbles never pop gently.

History has shown similar paths:

1929: People borrowed to the limit to buy stocks and durable goods, banks lent out almost every penny; when the music stopped, there was no buffer.

2000: If a company's name had '.com', investors threw billions at it—no revenue, no plan, no problem, until the funding dried up.

2008: Banks gave mortgages to the unemployed, rating agencies slapped 'AAA' on these toxic assets like handing out gold stars in elementary school, ultimately wiping out 20 million jobs globally.

And today? Some analysts look at the valuations of AI companies and are starting to feel the same unease. The entire system essentially runs on a credit bubble.

Austrian school economists have warned about this for decades: either proactively pop the bubble (at the cost of a severe recession) or see the currency itself destroyed (leading to hyperinflation).

You only get to choose between the two.

Early Warning Signals

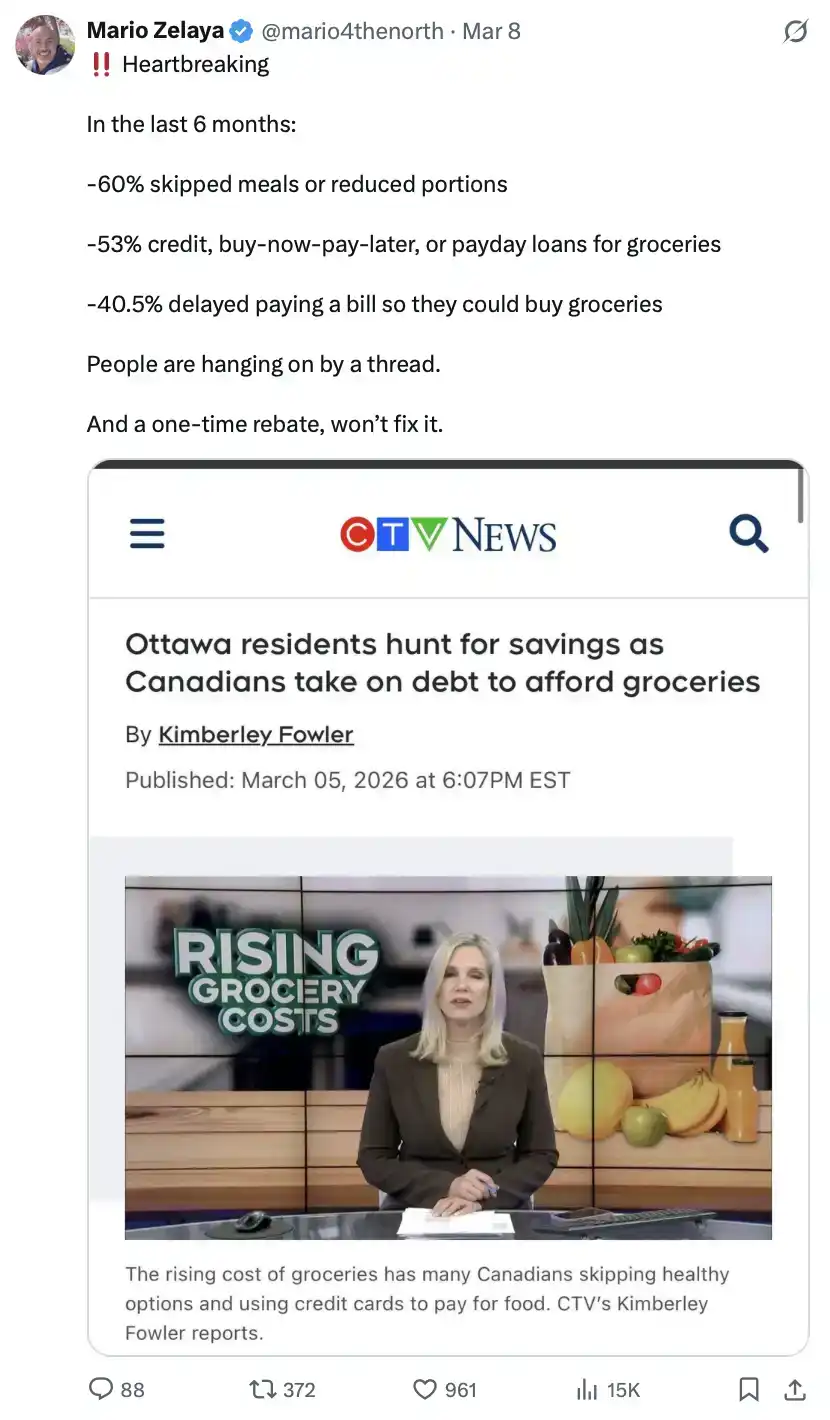

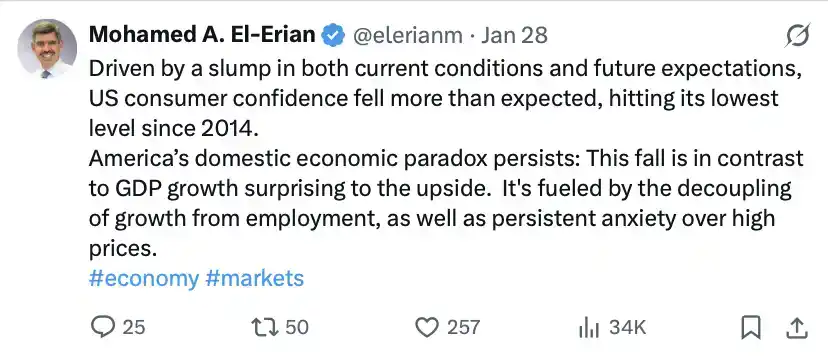

These are not predictions, but signals happening right now: Consumer confidence has plummeted to historical lows; the engine of consumption is stalling.

Anomalies in the government bond market, which look more like signs of 'capital flight' seen in emerging markets.

'Survival signals' in daily life are also becoming more obvious: People are using Klarna to buy fast food and daily necessities in installments; military recruitment is surging; graduate school enrollment is大幅上升 (translation: can't find a job).

Pressure is also showing at the corporate level: Tech companies are using overseas labor, or directly using AI, to replace domestic employees.

Don't believe it?

Alright, enough evidence. So what should we do? Sit there and complain about fate, sighing? Of course not.

What we need to do is first recognize its existence, then prepare for it, and thus survive.

How to Respond (Action Guide)

The following can be treated as an actionable checklist.

We must face it with a 'glass half full' mentality. Act with a pragmatic, can-do attitude, while also believing things will eventually get better. This is not the end of the world. Precisely because we know this, we can dare to take risks when it's time.

Immediate Financial Defense

Build an emergency fund that can cover 3 to 6 months of 'minimum living expenses'. Apart from minimum debt repayments, this takes priority over everything else. If you have no savings now, immediately save your first $1000.

This is not optional. Do not borrow money for consumption. If a large necessary expense is unavoidable, try to lock in a fixed rate now. In a downturn, variable rates will drag you down.

Pay off credit card debt as soon as possible. During an economic downturn, variable rates usually rise. Repay aggressively; if necessary, call the bank to negotiate a lower rate—asking costs nothing, and data shows about 70% of people succeed. Or, consider transferring to a 0% APR balance transfer card, but be sure to calculate if you can pay it off before the rate resets.

Do not co-sign for anyone. Nearly 40% of co-signers end up paying the borrower's debt. If you want to help someone, give them money directly or provide a private loan. In any case, protect your own credit score. These sound basic, but are crucial.

Career & Income Protection

Hate your boss? Understandable. But without a backup plan, in an environment where hiring opportunities are at a low and jobs are being replaced, quitting impulsively just because you're 'annoyed with the boss'—good luck.

Continuously upskill, especially learning to leverage AI. Of course, other directions work too. YouTube, Udemy, Khan Academy, coding bootcamps—mostly free or very low cost. Learn to code, learn SEO, stack skills that make you harder to replace, or enable you to start a side hustle.

Start a side hustle. Freelancing, online services, handmade products—all work. On average, a side hustle can bring in about $500 per month, and this money builds a safety net for you while you sleep.

Investment & Wealth Strategy

Ignore media-induced panic. Economists predict a recession almost every year, and 'doomscrolling' will only make you make emotional decisions that destroy your portfolio.

In the long run, the S&P 500 index goes up—after all, it represents the top 500 companies in the US. If you are prepared, this stage can be a good time to add risk assets. I will do this, while also allocating to Bitcoin as much as possible at the right time, and DCAing (Dollar-Cost Averaging) and building a position in batches before that.

The market always recovers eventually. If you miss the best 10 days of market performance, you miss most of the gains. So, when the market is already down 25%–35% (taking the S&P as an example), and people are telling you it will get worse, that might反而 be the time you should take risks.

Trust the power of time. A Schroders study covering 148 years of data shows: Investing for 1 month, the probability of loss is about 40%; for 1 year, it drops to 30%; for 20 years, it's almost zero.

Think in the long term. Maybe you don't have to wait 20 years, but at least think in terms of one cycle. Or, you can be a 'cockroach'.

Do you know who this is?

Today, 'being a cockroach' probably means: Cash + Commodities + Stocks, balanced allocation.

Such a portfolio can allow your assets to compound steadily through different cycles. However, this is more suitable for people with larger capital; it may not make you rich quickly, but it can keep you stable.

If you have cash on hand, I would personally still consider making some allocations further out on the risk curve, like adding to Bitcoin when it's down around 70%. Of course, this is just my view, not advice.

Remember: When everyone is panic selling, those willing to take on risk have the opportunity to gain huge wealth returns.

Next is an often overlooked but very important investment direction—

Personal Preparation

1) Invest in Your Health

Make yourself 'harder to knock down'. Start investing time and effort now to improve your physical condition, striving to reach the best fitness level of your life.

An illness, a surgery, or being unable to work for a short time can directly destroy your finances. Therefore, this is the investment with the highest return' you can make.

2) Asset & Tax Planning

Do tax planning, maximize the use of tax-free accounts and pension allowances. Complete estate and inheritance arrangements before the tax year ends, especially if policies might change (e.g., abolishing the 7-year rule or introducing capital gains tax on inheritance). Seek professional help if necessary.

3) Invest in Your Cognition & Knowledge

Don't be ridiculed for paying attention to things 'outside your field'. Maybe the algorithm won't reward you immediately, but those who remain genuinely curious and keep learning will eventually benefit. Keep outputting, keep learning; your abilities and influence will accumulate slowly, and the algorithm will 'see you' sooner or later.

The 2008 financial crisis destroyed millions of jobs, but it also gave rise to a whole generation of developers, digital marketers, and internet entrepreneurs. They learned skills at low cost during the trough and achieved wealth leaps in the subsequent bull market.

So, where should you invest your time?

First Layer: Skills that Directly Generate Income

Copywriting, sales, programming, SEO. These skills can be monetized immediately, whether through freelancing or creating value within a company. A copywriter who understands conversion can make money in any environment; a developer who can deliver products is someone a company dares not lose.

Second Layer: Skills that Protect and Amplify Income

Financial literacy, tax planning, negotiation skills, basic legal knowledge. Many people hand over money to advisors for things they could learn themselves in a weekend, and this 'cost of ignorance' compounds over time.

Third Layer: Abilities to Build Long-Term Advantage

Macro analysis, understanding technological cycles, identifying capital flows early. These abilities allow you to see trends before the masses react.

But in the end, the most important thing is to invest time in things you are truly interested in and willing to深耕 long-term. Everything you do is not just for yourself, but for your family—to give them less uncertainty and more peace of mind in the future.

It is precisely for this reason that we choose to prepare in advance. We are not children, nor are we blindly optimistic. We are清醒, rational, and still believe things will get better.

This article was written with great gusto. Whatever happens next in the world, we are prepared to face it.

P.S. This information is not scarce; it's just selectively ignored by most people. What truly creates the gap is never 'whether you know', but 'whether you act'.