Автор|Azuma(@azuma_eth)

22 декабря новость о ведущем рынке прогнозов Polymarket привлекла всеобщее внимание — член команды Polymarket Mustafa подтвердил в сообществе Discord, что Polymarket планирует мигрировать из Polygon и запустить собственную сеть Layer2 на Ethereum под названием POLY, и это является главной задачей проекта на данный момент.

Неожиданный, но закономерный «развод»

Решение Polymarket покинуть Polygon не стало неожиданностью. Один — восходящая звезда среди приложений, другой — постепенно теряющий влияние старый базовый слой, рыночный ажиотаж и ценностные ожидания между ними изначально были не совсем совместимы. По мере того как Polymarket постепенно превращался в нового гиганта, нестабильная работа сети Polygon (последний сбой произошел 18 декабря) и относительно слабая экосистема объективно стали ограничением для первого.

Для Polymarket создание собственной платформы означает двойной выигрыш как с продуктовой, так и с экономической точки зрения.

С продуктовой стороны, помимо поиска более стабильной среды для работы, создание собственной сети Layer2 позволяет Polymarket customizedровать базовые функции в соответствии с потребностями платформы, что обеспечивает большую гибкость для будущих обновлений и итераций.

Более важное значение имеет экономический аспект. Создание собственной сети означает, что Polymarket может собрать всю экономическую активность и сопутствующие услуги, связанные с его платформой, в собственную систему, предотвращая утечку связанной стоимости во внешние сети и постепенно накапливая ее в виде системных преимуществ.

Явный и скрытый экономический вклад

Как приложение, взрывной рост Polymarket принес Polygon ощутимый прямой экономический вклад. Данные, собранные аналитиком dash на Dune, показывают:

- Количество активных пользователей Polymarket в этом месяце составило 419 309 человек, общее историческое количество пользователей — 1 766 193 человека;

- Общее количество сделок в этом месяце — 19,63 млн, общее историческое количество сделок — 115 млн;

- Общий объем торгов в этом месяце — 1,538 млрд долларов США, общий исторический объем торгов — 14,3 млрд долларов США.

Что касается оценки доли вклада Polymarket в экономику экосистемы Polygon, Odaily Planet Daily при анализе данных обеих сторон обнаружил довольно coincidentalную пропорцию.

- Во-первых, по объему заблокированных средств: данные Defillama показывают, что текущая общая стоимость позиций на всей платформе Polymarket составляет около 326 млн долларов США, что составляет примерно четверть от общей стоимости блокировки в сети Polygon в 1,19 млрд долларов США;

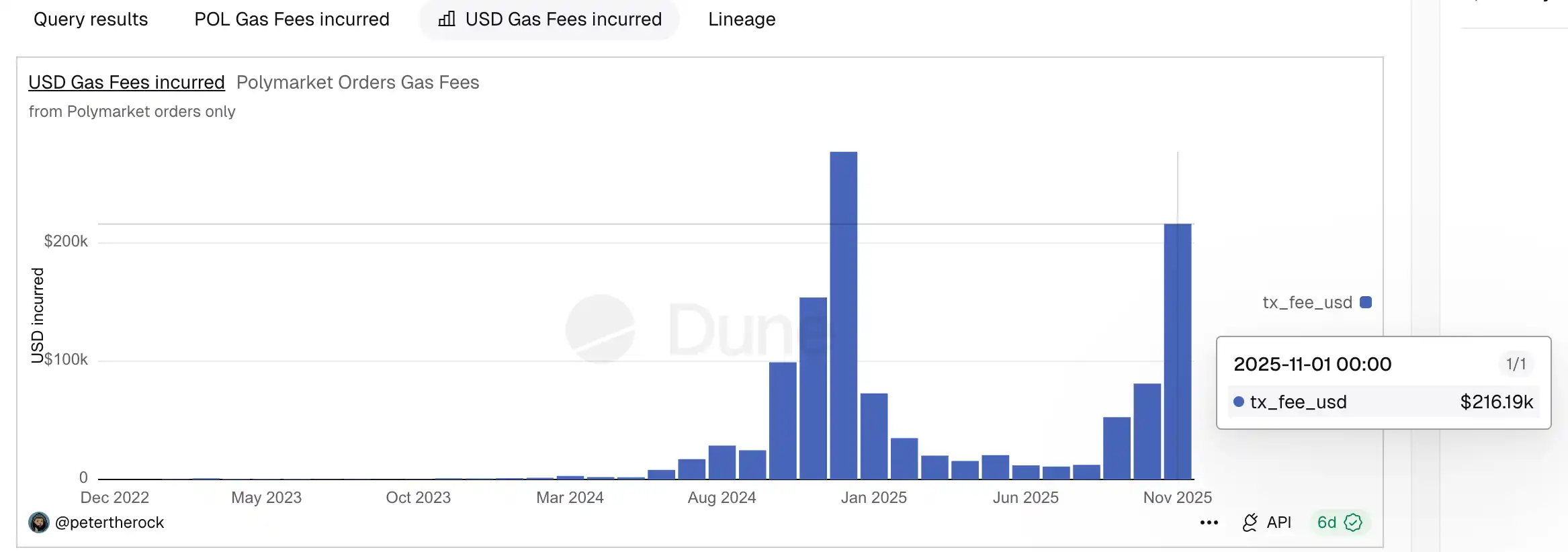

- Во-вторых, по потреблению газа: Coin Metrics в октябре прошлого года сообщали, что сделки, связанные с Polymarket, предположительно потребляли 25% всего газа в сети Polygon;

- Учитывая, что эти данные немного устарели, мы проверили recentние изменения: статистика, составленная аналитиком petertherock на Dune, показывает, что в ноябре сделки, связанные с Polymarket, в совокупности потребили около 216 тыс. долларов США на комиссиях gas, в то время как Token Terminal сообщает, что общее потребление газа в сети Polygon за тот же месяц составило около 939 тыс. долларов США, что также составляет почти четверть (около 23%).

Здесь, конечно, может быть совпадение из-за differentных методик и временных окон подсчета, но схожие результаты across differentных измерений в определенной степени могут служить оценочным referenceом для измерения экономической значимости Polymarket для Polygon.

Помимо quantifiableых показателей, таких как активные пользователи, заблокированные средства, объем торгов, вклад в комиссии газа, экономическое значение Polymarket для Polygon также заключается в ряде менее очевидных, но не менее реальных скрытых вкладов.

Во-первых, это оживление ликвидности стейблкоинов. Все сделки на Polymarket结算руются в USDC, их高频ная и постоянная торговая активность объективно значительно повышает спрос на оборот и сценарии использования USDC в сети Polygon; Во-вторых, это ценность сопутствующего поведения удержанных пользователей. Помимо самого рынка прогнозов, эти пользователи также могут перейти к использованию других продуктов экосистемы Polygon, таких как DeFi, для удобства, тем самым повышая общую ценность экосистемы сети Polygon. Эти вклады трудно измерить конкретными данными, но они constituteют самую важную и稀缺ную «реальную потребность» для базовой сети.

Почему именно сейчас? Ответ не сложно guessать

Фактически, судя только по масштабу пользовательской базы, данным и рыночной известности, Polymarket уже полностью обладает уверенностью для самостоятельной работы. Это давно уже не вопрос «стоит ли уходить», а вопрос «когда уходить».

Выбор именно этого момента для начала миграции, основная причина, вероятно, заключается в приближении TGE (Token Generation Event) Polymarket. С одной стороны, как только Polymarket завершит выпуск токена, его структура управления, система стимулирования и экономическая модель относительно закрепятся, и последующая миграция базового слоя станет значительно дороже и сложнее; с другой стороны, upgrade от «единичного приложения» до «полного стека приложение + базовый слой» сам по себе означает изменение логики оценки, создание собственного Layer2, несомненно, открывает для Polymarket более высокий потолок в нарративном и капитальном аспектах.

В конечном счете, уход Polymarket из Polygon по своей сути является не просто простой миграцией базового слоя, а отражением структурных изменений в криптоиндустрии. Когда топовые приложения начинают обладать способностью независимо нести пользователей, трафик и экономическую активность, базовые сети, если они не могут предоставить дополнительную ценность, неизбежно будут «преданы».

Ничего личного, просто бизнес.