Автор: Thejaswini M A

Компиляция: Luffy, Foresight News

У истории Optimism могла быть версия грандиозной победы.

В той версии OP Stack стал бы инфраструктурой по умолчанию для масштабирования Ethereum, десятки хорошо финансируемых блокчейнов присоединились бы к Superchain, доходы поступали бы в Collective, функции взаимодействия плавно запустились, и вся экосистема постоянно наращивала бы сложный процент, издалека напоминая совершенно новую форму интернета: он никому не принадлежит, всеми управляет и самоподдерживается.

Эта версия не была фантастикой. Был период, когда казалось, что это действительно произойдет. Проблема в том, что все, что Optimism сделал для реализации этого видения, также сделало защиту этого видения невозможной.

OP Stack был выпущен под лицензией MIT с открытым исходным кодом. Важность этого решения почти превосходит любой другой выбор, сделанный Optimism, поэтому важно прояснить его значение: MIT в настоящее время является самой разрешительной общей лицензией с открытым исходным кодом. Любой может взять код, доработать его, изменить, коммерциализировать или даже сделать полный форк. Никаких лицензионных отчислений, никакого разделения доходов, никаких обязательств — вам даже не нужно говорить спасибо.

Optimism сознательно сделал этот выбор. Логика проста: если вы хотите стать фреймворком по умолчанию, вы должны устранить все причины не использовать вас. Сведите затраты на вход к нулю, сделайте протокол бесспорным, чтобы любая команда, компания или биржа с бюджетом на разработку могла запустить цепочку OP Stack без разрешения, без подписания каких-либо документов, одним нажатием кнопки.

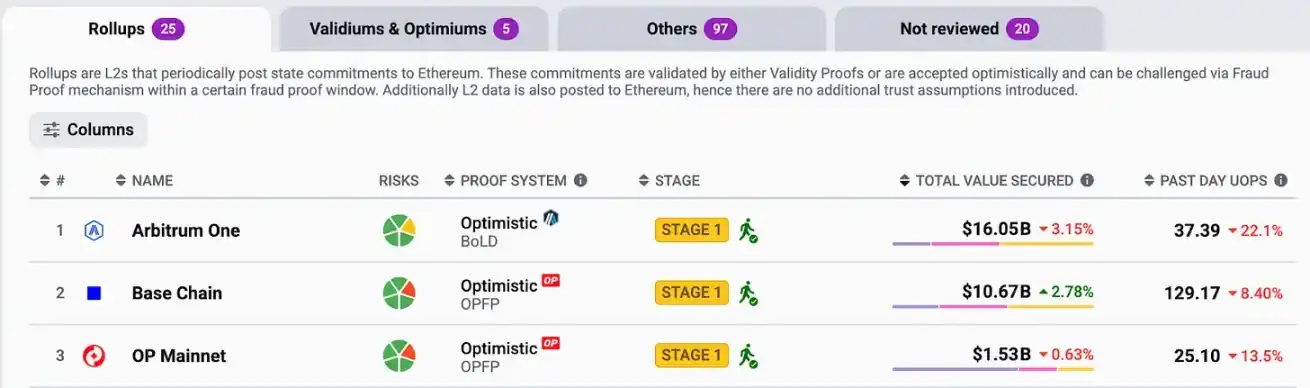

Это удалось. К середине 2025 года OP Stack обрабатывал 69,9% комиссий за транзакции L2, 34 цепочки были запущены в основной сети. Coinbase, Uniswap, Kraken, Sony, Worldcoin используют его. Когда люди говорят о масштабировании Ethereum, они обычно имеют в виду то, что построено на основе кода Optimism.

Optimism выиграл войну стандартов.

Затем самая большая цепочка, которую он помог построить, объявила, что больше не нуждается в этих отношениях.

18 февраля 2026 года Coinbase опубликовала в блоге запись с тщательно подобранным и дружелюбным заголовком — типичный стиль для компании, объявляющей о крупном событии, но не желающей казаться резкой. Блокчейн Base объединит кодобазу, ускорит циклы разработки и снизит затраты на координацию. В статье выражалась благодарность и восхвалялось сотрудничество.

После новости токен OP упал на 28% за 48 часов, объем продаж резко вырос на 157%. Всего за несколько дней токен упал на 89,8% по сравнению с прошлым годом и на момент написания статьи стоил всего 0,12 доллара, тогда как в марте 2024 года его максимум составлял 4,85 доллара. Генеральный директор OP Labs Цзин Ван написал в X: «Это удар по краткосрочным доходам в ончейне».

Чтобы понять причину, вы должны понять, что на самом деле продает Superchain.

OP Stack бесплатен. Протокол делает это постоянным и безотзывным. Так почему же какая-либо цепочка захочет делиться доходами с Optimism Collective? Ответ Optimism: взаимодействие. Присоединившись к Superchain, ваша цепочка становится не просто цепочкой, а частью единой сети — ликвидность и пользователи могут свободно перемещаться между всеми цепочками-участницами, разработка на одной цепочке эквивалентна разработке на всех, достигается эффект 1+1>2.

Таково его ценностное предложение: платите 2,5% от общего дохода или 15% от чистой прибыли, и в ответ вы получите то, что ни одна отдельная цепочка не может построить самостоятельно.

Но взаимодействие так и не было запущено.

Optimism изначально планировал запустить нативное взаимодействие в основной сети в начале 2025 года, но этого не произошло. Один давний представитель управления заявил: «Несмотря на годы технической разработки, к сожалению, этого достичь не удалось».

Участники платили «налог», а продукт, который должны были поддерживать эти деньги, оставался теоретическим. На практике Superchain предлагал только общий бренд, общие затраты на управление и обязательство по доходам. А то, ради чего стоило брать на себя это обязательство, всегда было «уже на подходе». Тем временем Base продолжал расти.

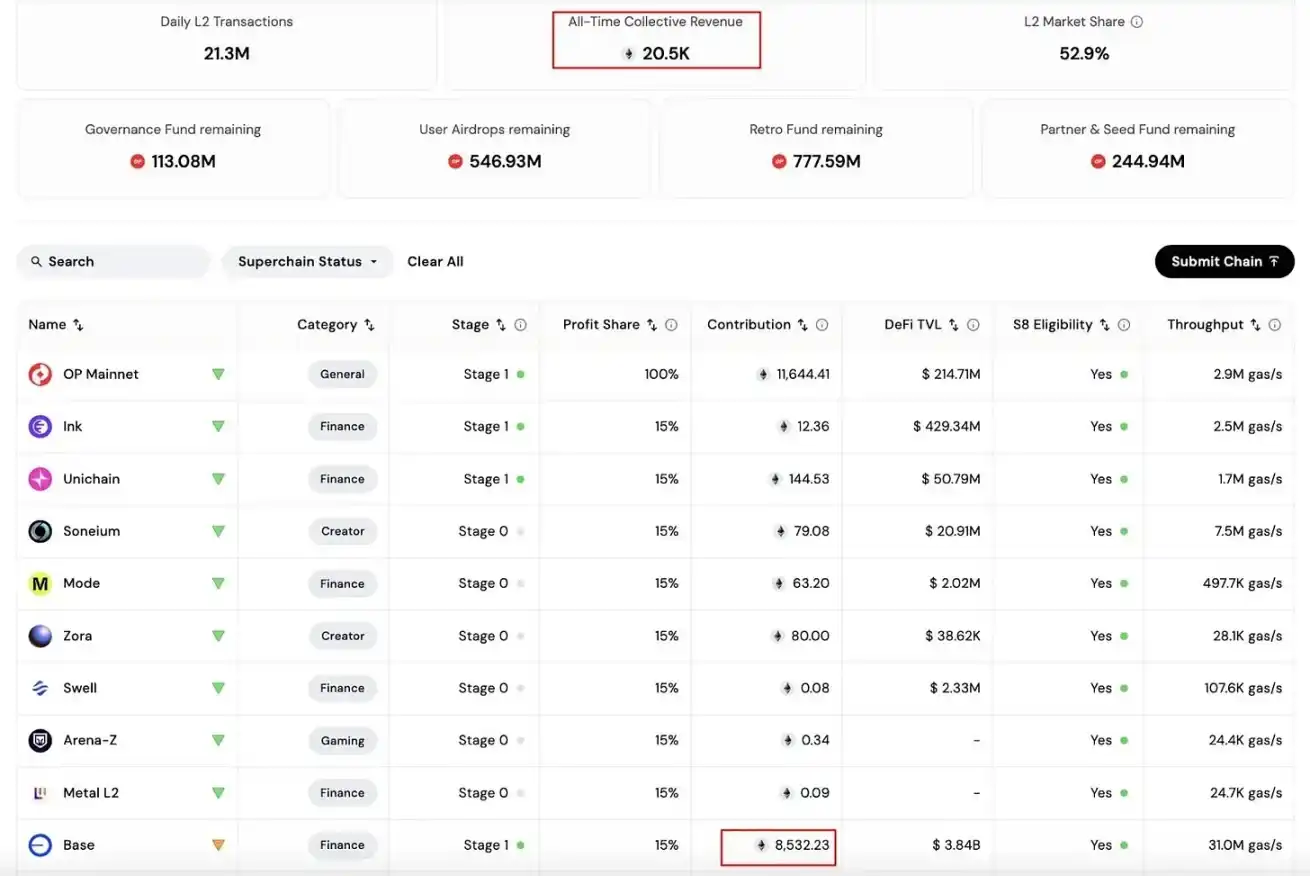

К январю 2026 года Base обеспечивала 96,5% всех комиссий за газ, поступающих в Optimism Collective, — почти все. Объем транзакций Base был примерно в 4 раза больше, чем у OP Mainnet, объем транзакций на DEX — примерно в 144 раза, а generation комиссий за газ — в 80 раз. За время сотрудничества Collective в общей сложности получил около 14 000 ETH, из которых Base внесла 8 387 ETH, причем доля ежемесячных доходов приближалась к 100%.

Остальные 33 участника Superchain, хотя и числились в списке, экономически не имели значения. В первой половине 2025 года второй по активности участник, World Chain, составлял лишь 11,5% от общего объема вычислений Superchain, сам OP Mainnet — 11,4%, а Ink, Soneium, Unichain вместе — менее 13%.

За исключением названия, Superchain de facto превратилась в экосистему одной цепочки. Альянс был реальным на бумаге, но экономически полностью состоял из Base.

В любом альянсе на определенном этапе самый сильный участник задает очевидный вопрос: что я вообще от этого имею?

Почти в каждой успешной истории с открытым исходным кодом разворачивается одна и та же логика. MongoDB создала широко используемую базу данных, выпустила ее с открытым исходным кодом, а затем смотрела, как AWS строит на ее основе прибыльный хостинговый сервис, не платя ни копейки. AWS контролировала распределение трафика, MongoDB установила стандарт, ценность流向 к实体, которая контролирует пользователей, а не к той, которая написала код. В итоге MongoDB изменила лицензию, а AWS форкнула ее в OpenSearch.

Elastic, Redis прошли через тот же цикл. Детали разные, но структура完全相同: создатель инфраструктуры устанавливает стандарт, гигант с возможностями дистрибуции принимает его, гигант пожинает ценность, в конечном итоге гигант интернализирует технологический стек и уходит.

Optimism — это криптовалютная версия этой истории.

Arbitrum понял эту логику и сделал другой выбор. Цепочки Orbit, аналог Superchain, используют лицензию Business Source, разделение доходов основано на договорных обязательствах, а не на добровольности. Когда ваш самый большой партнер может уйти без юридических последствий, выживание альянса полностью зависит от его желания остаться. Arbitrum не хотел строить экосистему, основанную на таком предположении.

Официальная причина ухода Base — техническая: унификация кодобазы означает более быструю разработку, цель увеличивается с 3 крупных обновлений в год до 6; независимый контроль над security committee означает, что никакие внешние органы не могут задерживать или блокировать сетевые решения; снижение зависимости означает, что Base может успевать за节奏ом обновлений самого Ethereum, не дожидаясь неподконтрольных ей процессов управления.

Координация между несколькими кодобазами действительно медленнее, чем управление собственным технологическим стеком.

Но есть и другая причина, которую не нужно подробно описывать. По расчетам Morgan Stanley, токен Base может принести Coinbase около 34 миллиардов долларов стоимости акционерного капитала и повысить целевую цену акций до 404 долларов. Пока Base платит 15% чистой прибыли внешнему протоколу Collective, структурно крайне сложно разработать токен Base с надежным механизмом захвата стоимости. Выход из Superchain является prerequisite, а не побочным эффектом. Оба мотива указывают в одном направлении, и Base так и поступила.

Optimism остался не с пустыми руками, но нужно честно признать произошедшие изменения.

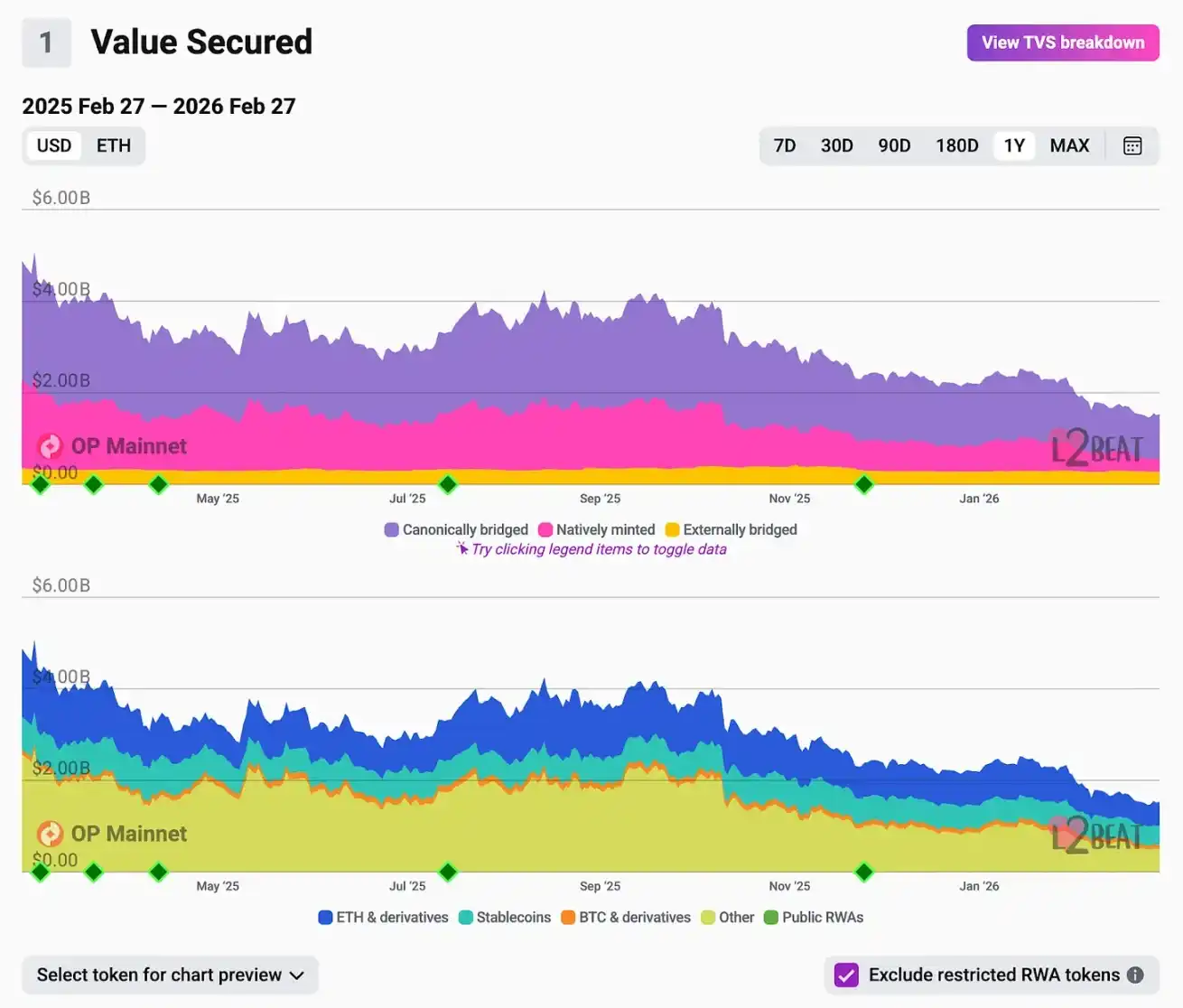

OP Mainnet по-прежнему имеет TVL в 1,5 миллиарда долларов. В тот же день, когда Base объявила об уходе, ether.fi заявил о переносе своего ончейн-продукта кредитных карт на OP Mainnet, что принесет 70 000 активных карт, 300 000 аккаунтов и более 160 миллионов долларов TVL. Несколькими неделями ранее Collective принял программу buyback, согласно которой 50% доходов секвенсора будет ежемесячно направляться на выкуп OP.

Партнерство с ether.fi предоставило OP Mainnet более четкий вариант использования в области потребительских платежей. Но годовой вклад ether.fi в комиссии составляет всего около 13 миллионов долларов, в то время как только за 2025 год прибыль Base составила 55 миллионов долларов. Доходная база, на которую опиралась программа buyback, исчезла. Разблокировка токенов инвесторов и контрибьюторов продолжается с объемом около 32 миллионов долларов в месяц.

Поворот в сторону корпоративных услуг, возможно, является правильным шагом. OP Labs привлекла более 175 миллионов долларов финансирования, обладает талантливыми инженерами высшего класса, и существует реальный спрос со стороны институтов на размещение развертываний OP Stack, эти институты хотят запустить цепочку, но не хотят создавать собственные возможности для обслуживания. Цзин Ван позиционирует это как «Databricks в области инфраструктуры блокчейна» — это разумная аналогия. Это сервисный бизнес, и он может сработать.

Но сервисный бизнес совершенно不同于 сеть, генерирующая сложный процентный доход протокола через альянс. Оценка токена OP изначально была предназначена для последнего. Рынок понял это менее чем за 12 часов после публикации блога.

Если взглянуть шире. То, что произошло 18 февраля, по сути, касается не только Optimism.

Большую часть 2024 года более 50 сетей L2 боролись за пользователей и ликвидность. К концу 2025 года Base, Arbitrum и Optimism обрабатывали почти 90% транзакций L2, причем только Base — более 60%. Активность небольших роллапов с июня снизилась на 61%. Обновление Dencun привело к снижению комиссий на 90%, что сжало рентабельность всей отрасли. Base был единственным L2, получившим прибыль в 2025 году.

Цепочки, которые выжили, и те, которые будут определять этот уровень в ближайшие годы, не обязательно являются технически самыми совершенными. Это цепочки, которые имеют структурные причины для удержания пользователей. Цепочки, связанные с биржами (Base, Ink, Mantle), опираются на существующую пользовательскую базу материнской компании, которая обладает встроенными возможностями дистрибуции — каждый пользователь Coinbase, желающий выйти в ончейн, находится на расстоянии одного клика от Base. Такие нативные DeFi-цепочки, как Arbitrum и Hyperliquid, удерживают свои позиции за счет глубины ликвидности, которую трудно восстановить в другом месте.

Технологию можно форкнуть. OP Stack доказал это как нельзя лучше. То, что нельзя форкнуть, — это отношения Coinbase с ее 100 миллионами пользователей или открытые позиции на сотни миллиардов долларов на Arbitrum. Постоянная ценность заключается именно здесь, и она почти не зависит от того, какой протокол вы выберете для своей кодобазы.

Решение Optimism выпустить OP Stack под разрешительной лицензией с открытым исходным кодом было правильным. Оно привело к самому широкому внедрению среди фреймворков L2, позволив Optimism стать инфраструктурным стандартом для целого поколения масштабирования Ethereum. Без этого решения Base, возможно, была бы построена на другой технологии или вообще не появилась бы.

Но решение, которое сделало все это возможным, также сделало выход бесплатным. Когда Base выросла достаточно, обзавелась своими пользователями, собственной дорожной картой токена и своими причинами для追求 полного суверенитета инфраструктуры, в протоколе не было никаких ограничений, а обещание взаимодействия оказалось недостаточной причиной, чтобы остаться.

Optimism выиграл войну стандартов. Просто этот стандарт не поставлялся с механизмом, способным захватить создаваемую им ценность. Цена токена в 0,12 доллара — это окончательная оценка рынком всей этой ценности.