Рынок стейблкоинов столкнулся с критическим испытанием. Не рыночным циклом. Не ликвидным кризисом. А законодательным – и ущерб уже виден.

Отчет XWIN Research Japan документирует произошедшее за одну торговую сессию: Circle, эмитент USDC, потерял 18% своей рыночной стоимости вчера, потеряв примерно 4,6 миллиарда долларов за несколько часов. Триггером стал не провал по прибыли или крах биржи. Им стал проект поправки – предложенное обновление к закону CLARITY, которое полностью запретит доходность по стейблкоинам.

Одна эта законодательная оговорка, еще не закон, еще не окончательная, была достаточна для переоценки всей концепции того, чего стоит Circle. Рынок понял последствия раньше, чем появились заголовки новостей.

Отчет помещает ценовую реакцию в proper context: это не волатильность. Это структурный сигнал. Годами стейблкоины функционировали как инструменты двойного назначения – цифровые доллары для платежей и расчетов, а также активы, генерирующие доход для кошельков, которые их хранили. Это сочетание и было продуктом. Фреймворк CLARITY, в его текущей редакции, нацелен на то, чтобы разделить эти функции навсегда, ограничив пассивный доход и разрешив только вознаграждения, основанные на активности.

Один законопроект. Две функции разделены. Модель, которая построила USDC в краеугольный камень рынка, теперь является моделью, находящейся на рассмотрении.

Капитал стейблкоинов не исчезает. Он перемещается.

Отчет точно определяет, что на самом деле поставлено на карту beneath the regulatory language: это конкуренция за капитал, и каждый участник финансовой системы это знает. Банки лоббируют против доходности стейблкоинов не из принципа. Они лоббируют, потому что отток депозитов – это вопрос платежеспособности. Криптоплатформы защищают доходность не из идеологии. Они защищают структуру стимулов, которая удерживает ликвидность на их платформах. Регулирование – это арена. Капитал – это приз.

Что нам говорит история – и отчет прямо на это ссылается – так это то, что ограничение доходности не уничтожает спрос на доходность. Он перенаправляет его. Когда в прошлую эпоху ограничивали ставки по депозитам, деньги текли в фонды денежного рынка. Та же логика применима и здесь. Спрос на доходность мигрирует в сторону DeFi-протоколов, токенизированных казначейских обязательств или офшорных рынков, которые работают вне зоны досягаемости фреймворка CLARITY. Капитал переместится. Он всегда так делает.

То остается – и это самое важное наблюдение отчета – может оказаться более устойчивым, чем то, что потеряно. Уберите доходность из стейблкоинов, и то, что выживет, – это utility: платежи, расчеты, залог, ликвидность. Они перестают быть финансовыми продуктами, конкурирующими со сберегательными счетами, и начинают быть инфраструктурой, конкурирующей с корреспондентским банкингом.

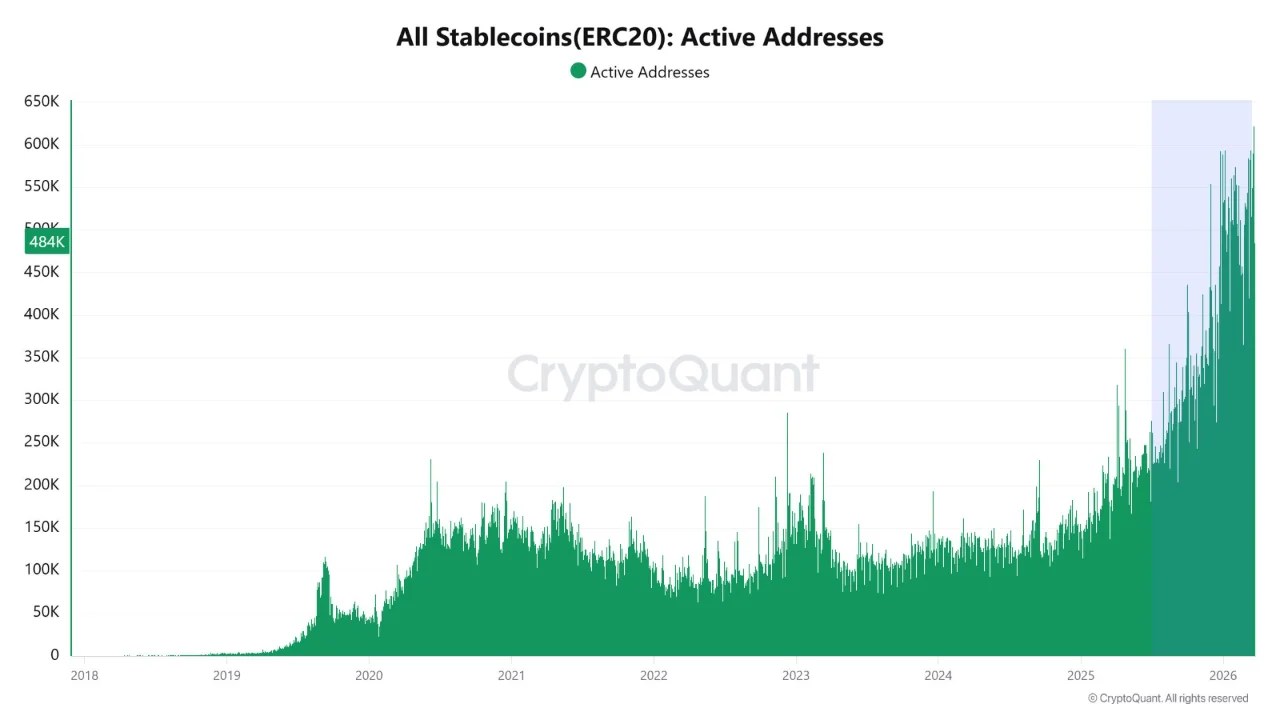

Данные в блокчейне уже отражают этот переход. Количество активных адресов стейблкоинов находится на историческом максимуме. Капитал не простаивает. Он используется – и если регулирование обеспечит заявленную ясность, этой кривой использования есть куда расти.