Вчера Financial Times сообщила, что правительство лейбористов Великобритании вскоре объявит новое правило: компании, жертвующие средства британским политическим партиям, должны будут раскрывать реальные личности тех, кто стоит за этими пожертвованиями.

Причиной этого нововведения стала серия скандалов, связанных с проникновением иностранных средств в британскую политику. Однако, говоря об иностранных средствах, нельзя не обратить внимание на «невидимого» криптомиллиардера с двойным гражданством, финансирует «британского Трампа».

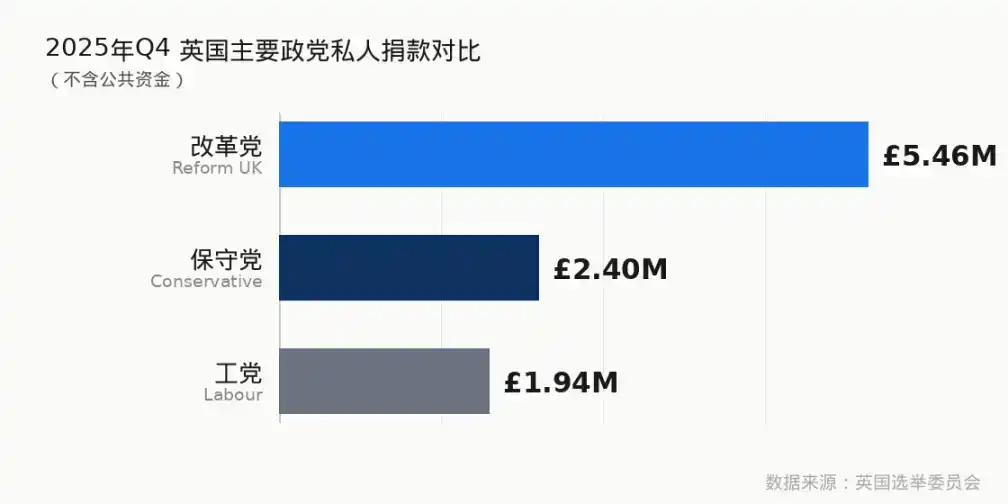

Согласно данным о политических пожертвованиях за последний квартал, опубликованным 5 марта 2026 года Избирательной комиссией Великобритании, Партия реформ (Reform UK) снова возглавила список британских партий по сбору средств, собрав 5,5 миллионов фунтов стерлингов. Однако 3 миллиона фунтов из этой суммы поступили от одного человека, источник указан как Таиланд.

Жертвователя зовут Кристофер Харборн. Иногда его зовут Чакрит Сакункрит.

Он проживает в Таиланде, имеет таиландское гражданство, под своим тайским именем владеет около 12% акций материнской компании крупнейшего стейблкоина Tether, управляет одной из крупнейших в мире частных сетей авиационного топлива и одновременно переправляет политические средства правой партии в Великобритании, находящейся за тысячи миль. За последние два года он использовал это состояние, чтобы сделать ставку на одно: привести Фараджа и Партию реформ к власти в британской политике.

Кембриджский инженер & Бангкокский затворник

В декабре 1962 года Кристофер Чарльз Шерифф Харборн родился в Англии. Он получил среднее образование в Вестминстерской школе, в списке выпускников которой значатся имена премьер-министров, судей и банкиров Великобритании — это верхнее звено конвейера элит Империи.

Затем — Колледж Даунинг в Кембридже, двойная степень по инженерии и менеджменту. Затем — Европейский институт делового администрирования (INSEAD) в Фонтенбло, Франция, где он получил MBA, окончив в 1988 году.

Его первая работа — консультант по управлению в McKinsey, где он проработал пять лет. В те времена карьерная траектория консультантов McKinsey обычно заканчивалась на руководящих должностях в инвестиционных банках или транснациональных корпорациях. Но Харборн поступил иначе. Он уехал в Азию, основал исследовательскую компанию, а в 2000 году создал Sherriff Global Group — компанию товарных торгов, изначально специализировавшуюся на рискованных офшорных услугах, названную в честь фамилии его отца.

Примерно в 2005 году он переехал в Таиланд. В том же году он зарегистрировал здесь AML Global Ltd., брокерскую компанию по авиационному топливу. Сегодня AML Global имеет более 1200 точек снабжения по всему миру и является одним из крупнейших в мире брокеров авиационного топлива для частных самолетов.

В 2011 году он официально получил таиландское гражданство, взяв имя Чакрит Сакункрит. Свидетельство о британском гражданстве и свидетельство о гражданстве Королевства Таиланд с тех пор сосуществуют в кармане одного человека.

Никто не знает о его семейном положении. Нет супруга, нет детей, нет никаких поддающихся проверке записей о личной жизни. Он никогда не дает интервью СМИ, почти не появляется на публике и не имеет аккаунтов в социальных сетях. В эпоху экономики внимания, работающей на曝光率, он использует полную невидимость в качестве талисмана.

Позиции в криптосфере

В 2011 году, когда биткоин был еще тайным словом в кругах гиков, Харборн купил его. В 2014 году он купил Ethereum, раньше绝大多数 институциональных инвесторов.

Но真正改变他在加密世界地位的,是 2016 年 8 月的一场黑客攻击。

Летом того года биржа Bitfinex подверглась хакерской атаке, в результате которой было потеряно биткоинов на сумму около 72 миллионов долларов — по сегодняшним ценам это接近 7 миллиардов долларов. Bitfinex не могла немедленно fully возместить убытки пользователям, поэтому采用了在当时颇具争议的方案:向所有受损用户发放一种名为 BFX 的代币,代表对交易平台的债权,承诺日后兑换。

大多数用户选择了抛售,恐慌折价,急于离场。

Харборн选择了买入,并持续买入,最终以 именем Чакрит Сакункрит накопил около 12% акций материнской компании Bitfinex и Tether — DigFinex.

Это была не маленькая ставка. Tether, дочерняя компания DigFinex, сегодня является эмитентом крупнейшего в мире стейблкоина USDT,每日交易量长期位居全球加密资产前列, рыночная капитализация превышает 1400 миллиардов долларов. Владение 12% акций DigFinex означает, что Харборн находится в核心圈层全球加密одолларовой системы.

Но эти акции также принесли ему неприятности. В марте 2023 года The Wall Street Journal опубликовала расследование о банковских счетах Tether и Bitfinex, в котором связывала Харборна и его компанию по авиационному топливу AML Global с путем доступа Tether/Bitfinex к американской банковской системе, намекая, что при открытии счета в Signature Bank под тайским именем Чакрит Сакункрит он умышленно скрыл свою личность.

Харборн немедленно подал в суд, обвинив The Wall Street Journal в публикации ложных утверждений о «мошенничестве, отмывании денег и финансировании терроризма», и в феврале 2024 года дело было официально возбуждено в Высшем суде штата Делавэр.

The Wall Street Journal随后删除了报道中涉及 Харборна и AML Global的段落,并在编者按中声明:「删除此段落是为了避免任何可能的暗示......Harborne 或 AML 在申请开户过程中有任何隐瞒或伪造信息的行为。」

Иск был разрешен к дальнейшему рассмотрению.

Крупнейшая переменная в британской политике

Помимо авиационного топлива и криптоакций, у Харборна есть третья ипостась: один из самых крупных индивидуальных жертвователей в истории британской политики.

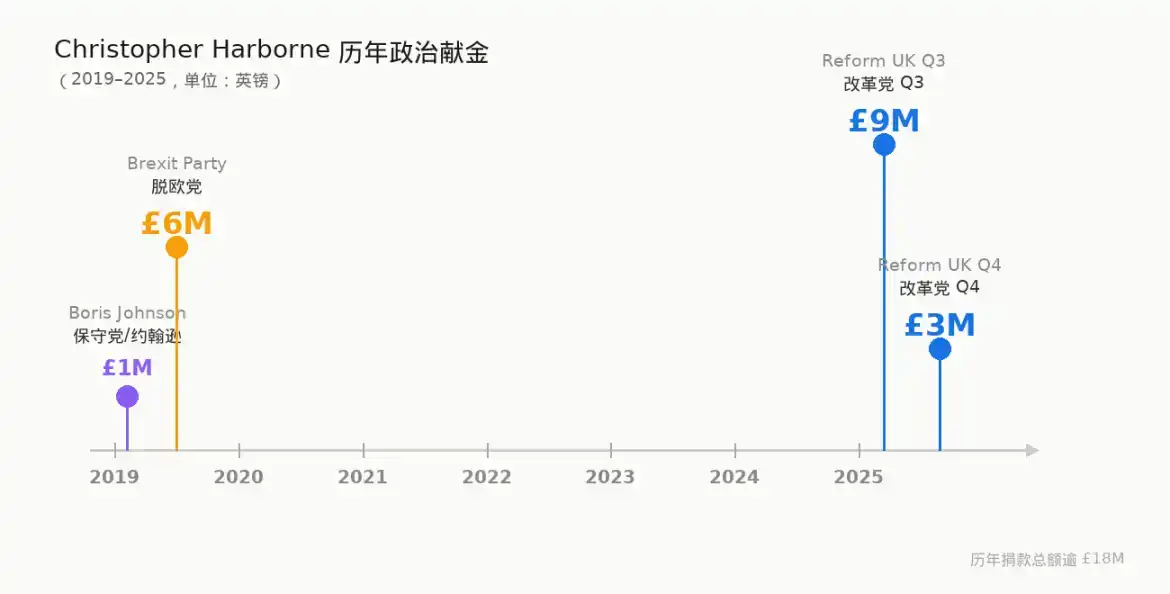

Его политический путь — это прослеживаемая траектория правых ставок. Ранее он жертвовал Консервативной партии, также捐出 1 миллион фунтов стерлингов на поддержку竞选 Бориса Джонсона. Но в 2019 году, когда переговоры по Brexit в консервативном парламенте一再 заходили в тупик, он счел, что решимость консерваторов продвигать Brexit недостаточна, и转而 вложил 6 миллионов фунтов в Партию Brexit Фараджа, став крупнейшим спонсором партии в том году. Партия Brexit затем одержала крупную победу на выборах в Европейский парламент.

В сентябре 2023 года он в качестве «советника офиса Бориса Джонсона» accompanied Джонсона в Украину для участия в Ялтинской European Strategy Forum, где, по сообщениям, встречался с высокопоставленными украинскими чиновниками и президентом Зеленским. Эта роль никогда публично не объяснялась.

В 2024 году Консервативная партия потерпела сокрушительное поражение на выборах, к власти пришли лейбористы. Две традиционные крупные партии потеряли свою полезность: лейбористы занимают четкую скептическую позицию в отношении криптовалют, депутат от лейбористов Рушанара Али (Rushanara Ali) публично призвала запретить партиям принимать пожертвования в криптовалюте, назвав их «потенциальным каналом вмешательства иностранных сил в демократию»; консерваторы же长期在加密监管议题上动作迟缓,始终停留在表态层面.

Партия реформ Фараджа — единственный вариант. Фараджа также часто называют британским Трампом.

Третий квартал 2025 года, 9 миллионов фунтов. Крупнейшее единовременное пожертвование living донора单一政党 в истории британской политики,一次性缔造纪录. Четвертый квартал, еще 3 миллиона фунтов. За 2025 год他的捐款总额 превысила 12 миллионов фунтов стерлингов.

Инвестиция с ожиданием отдачи

Харборн крайне редко публично говорит о мотивах своих пожертвований, за редким исключением, когда он кратко заявил: «Великобритания не использовала Brexit в полной мере, мы не поспеваем за технологиями в XXI веке».

Но外界很难忽视另一条更清晰的逻辑线:他持有全球最大稳定币 Tether 母公司约 12% 的股权. Если Великобритания станет дружественной к криптовалютам регуляторной средой, это имеет прямую коммерческую ценность для его核心资产. Политические пожертвования, в некотором смысле, также являются инвестицией — только объектом является политика, а не токен.

Временная шкала делает это суждение еще более трудным для игнорирования. Партия реформ公开拥抱加密货币是在收到 Харборна крупных пожертвований之后才发生的. Фарадж объявил, что в случае прихода к власти Партия реформ推出《Закон о криптоактивах и цифровых финансах》, пообещав сократить налог на прирост капитала от криптовалют, разрешить уплату налогов криптовалютой, создать национальный резерв биткоинов.

В июне 2025 года Партия реформ стала первой крупной британской партией, официально принимающей политические пожертвования в криптовалюте. Сам Фарадж затем лично вложил 215 тысяч фунтов стерлингов, приобретя около 6,3% акций британской компании Bitcoin Treasury Stack BTC.

В Партии реформ отрицают прямую связь между этими событиями. Либеральные демократы и лейбористы требуют провести расследование.

Скрытая логика

В США история о том, как криптоиндустрия вкладывает деньги в поддержку Трампа и возвращает себе主导权 в регулировании, уже рассказана. В Великобритании тот же сценарий разыгрывается вновь — только главные герои поменялись, а деньги все еще текут.

Влияние этой ставки уже частично видно. Партия реформ за 2025 год собрала 18,6 миллионов фунтов стерлингов, превысив показатели Консервативной партии (13,4 миллиона) и Лейбористской партии (8,2 миллиона), и стала партией, собравшей больше всех средств в Великобритании. Рейтинги поддержки Фараджа продолжают расти, Партия реформ в多项民调中跻身第一.

Если эта траектория сохранится, партия, явно дружественная к криптовалютам, получит возможность возглавить правительство Великобритании, и наибольшую выгоду от этого получат те, кто сделал ставку заранее.

Американская история уже提供了参照: В 2024 году криптоиндустрия влила более 200 миллионов долларов в кандидатов в Конгресс, после победы Трампа SEC сменил руководство, направление регулирования криптовалют резко изменилось, и отрасль получила долгожданные政策红利.

Британская история еще не дописана.