Автор: Thejaswini M A

Перевод: Chopper, Foresight News

Я нахожусь в Бангалоре, в часовом поясе UTC+5:30. Открытие американского фондового рынка приходится здесь на 7 часов вечера по местному времени. Я уже пять лет работаю в сфере крипторепортажа, и все эти пять лет я наблюдаю за рынками, которые никогда не останавливаются. Здесь нет механизмов закрытия торгов, нет пред- и послеторговых сессий — независимо от времени суток, выходных или праздников, котировки непрерывно меняются.

Режим работы традиционных финансовых рынков кардинально отличается. Нью-Йоркская фондовая биржа торгует с понедельника по пятницу с 9:30 до 16:00 по восточному времени (ET). Лондонская фондовая биржа — с 8:00 до 16:30. Токийская фондовая биржа — с 9:00 до 15:30, с перерывом на обед.

Крупные биржи открываются по очереди. Теоретически, пока мир вращается, капитал должен двигаться непрерывно. Однако в реальности основные биржи устанавливают фиксированные торговые сессии, и регулируемые рынки подолгу простаивают.

Этот график унаследован от физических ограничений ранних площадок с голосовым аукционом. Компьютерные технологии должны были сломать временные рамки, но в итоге лишь ускорили процесс сопоставления заявок, сохранив при этом фиксированные правила открытия рынка.

Законы физики гласят, что объект остается в покое, если на него не действуют внешние силы. Торговые часы финансовых рынков оставались неизменными именно из-за отсутствия движущей силы перемен. Но в одно майское воскресное утро этого года рынок, опередив традиционные инвестиционные банки, сам определил оценку компании SpaceX, занимающейся космическими исследованиями, и нарушил установленный порядок.

Платформа Hyperliquid работает без остановок. Соответствующие производные контракты были запущены в 05:16 по всемирному координированному времени (UTC). Объем сделок за 24 часа достиг 33 миллионов долларов, в то время как такие учреждения, как Morgan Stanley, еще даже не открылись.

Индийский часовой пояс как раз стал свидетелем этой необычной ценовой игры. Американские финансовые СМИ начали сообщать об этом только в 9:30 утра по восточному времени (ET), а к тому моменту я уже наблюдал за рынком полдня.

CME Group — крупнейшая в мире платформа для торговли деривативами. Институциональные трейдеры торгуют здесь фьючерсами на нефть, золото, процентные ставки, фондовые индексы и биткоин, с ежедневным оборотом в триллионы долларов. История бренда восходит к 1898 году.

Межконтинентальная биржа (ICE), которой принадлежит Нью-Йоркская фондовая биржа и несколько других глобальных платформ для торговли деривативами, также является отраслевым гигантом.

Обе они контролируют ведущую мировую финансовую инфраструктуру, и их предупреждения о рисках легко привлекают внимание регулирующих органов. Сейчас эти две организации лоббируют Комиссию по торговле товарными фьючерсами США и Конгресс с требованием навести порядок на платформе Hyperliquid, обвиняя ее в отсутствии проверки личности пользователей, что, по их мнению, легко приводит к манипулированию рынком и может стать каналом для уклонения от санкций.

На платформе Hyperliquid нет механизма проверки личности пользователей. Веб-интерфейс блокирует адреса, находящиеся под санкциями, но базовый протокол полностью открыт и не имеет порога входа. Пользователи могут обойти веб-интерфейс и напрямую взаимодействовать со смарт-контрактом без какой-либо проверки личности.

На платформе не существует правил лимитов позиций, в то время как CME ограничивает максимальный размер позиции по одному контракту, чтобы предотвратить манипулирование рынком и избежать системных рисков. CME отслеживает модели торговли для предотвращения таких нарушений, как ложные заявки или сговор, в то время как у Hyperliquid нет соответствующей системы мониторинга рисков.

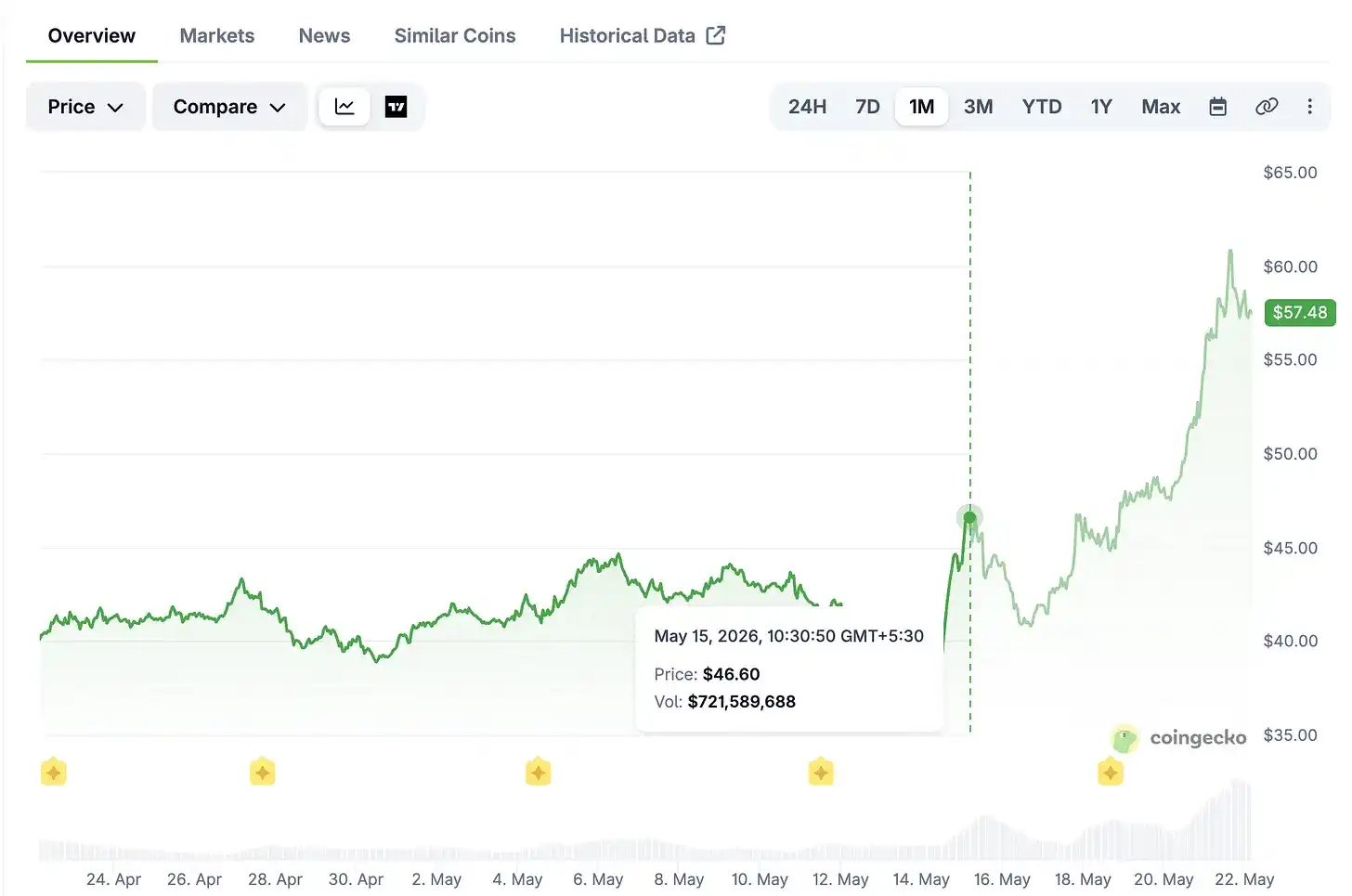

Эти критические замечания имеют под собой разумные основания. Под влиянием негативных новостей о регулировании цена токена HYPE упала на 9% 15 мая. 18 мая два маркет-мейкера вывели ликвидность на сумму 1 миллиард долларов.

Однако регулирующие органы нацелились не на криптовалютные бессрочные контракты, которые работали годами без вмешательства, а на контракты на производные нефти. Объем торгов по этим контрактам на выходных, когда CME была закрыта, достиг 720 миллионов долларов, что задело интересы традиционных институтов.

Опасения CME и ICE небезосновательны, но они также не являются нейтральными наблюдателями. Их бизнес-модель основана на монопольном барьере, установленном нормативными правилами, которые определяют время торговли. Конкуренция на технологическом уровне еще приемлема, но конкуренция во временном измерении, выходящая за установленные рамки, для традиционных гигантов невыносима.

Hyperliquid захватила окно простоя традиционного рынка для торговли нефтью, полностью разрушив временную систему функционирования традиционных финансов. Устоявшиеся институты пытаются оказать давление на регуляторов, чтобы унифицировать график торгов, в то время как новые платформы выступают за право легально работать в выходные дни.

В команде Hyperliquid всего 11 человек, офис находится в Сингапуре. За 30 дней до 21 мая 2026 года платформа заработала 51 миллион долларов. В марте этого года номинальный объем торгов деривативами достиг 2,6 триллиона долларов.

Платформа направляет 97% торговых комиссий в ончейн-пул ликвидности для выкупа токенов HYPE. Маленькая команда генерирует высокие доходы — доход на сотрудника является исключительно редким как в финансовом, так и в криптосекторе. К концу мая HYPE вырос на 101% с начала года.

Эта конкурентоспособность проистекает не только из технологического превосходства продуктов на основе деривативов. Ключевой ценностью является преимущество во времени — возможность круглосуточной торговли. Последующие новые типы контрактов еще больше усилили это дифференцирующее преимущество.

1 мая платформа Trade.xyz, построенная на Hyperliquid, запустила бессрочные контракты на компанию Cerebras, производителя ИИ-чипов, в преддверии ее IPO. Контракт охватывал период за две недели до официального IPO.

Изначально рынок предполагал премию в 50% к цене размещения в 185 долларов, прогнозируя цену открытия около 277 долларов. По мере поступления новой информации, за час до официального открытия на NASDAQ, цена контракта на платформе составила 340 долларов, что всего на 3% отличалось от окончательной цены открытия в 350 долларов. После размещения акции выросли на 89% от цены IPO.

Для сравнения, прогнозы на традиционных вторичных платформах, таких как Forge и EquityZen, отличались от фактической цены открытия на 35%, что демонстрирует высокую эффективность ценового обнаружения Hyperliquid. Рынок корректирует котировки по мере поступления информации — это и есть разумный механизм ценового обнаружения.

В воскресенье, 17 мая, Trade.xyz снова запустил бессрочные контракты на SpaceX в преддверии IPO. Начальная референтная цена контракта составляла 150 долларов, за несколько часов она поднялась до 216 долларов и в итоге стабилизировалась на уровне 203 долларов, что соответствует общей оценке компании в 2,4 триллиона долларов.

На тот момент SpaceX еще не публиковала проспект эмиссии, аналитики Уолл-стрит не выпускали отчетов об оценке, и компания не начинала роуд-шоу. Трейдеры не знали, что компания тайно подала документы в SEC еще в апреле, с предполагаемым диапазоном оценки от 1,75 до 2 триллионов долларов.

Рыночная оценка, рассчитанная самостоятельно, достигла верхней границы внутренней оценки компании, при этом вообще не ссылаясь на официально раскрытые данные. Лишь несколько дней спустя, 20 мая, SpaceX официально опубликовала публичный проспект эмиссии объемом в 277 страниц.

В настоящее время три продукта предлагают инвесторам доступ к SpaceX, используя различную логику соответствия нормативным требованиям, причем стратегия каждого продукта с юридической точки зрения отличается.

Платформа PreStocks использует структуру специального инвестиционного фонда, который приобретает реальные акции компании и разделяет их на ончейн-токены, позволяя обычным инвесторам косвенно владеть долями. Это было удобным каналом для инвестиций в непубличные технологические компании.

Однако незадолго до запуска контрактов на Hyperliquid, компании Anthropic и OpenAI публично отрицали продукты с токенизацией их акций, выпущенные третьими сторонами. Некоторые платформы в Гонконге и ОАЭ выпускали такие токенизированные активы без разрешения компаний, и обе компании заявили, что такая передача прав на акции не имеет юридической силы. После этого новости цена токена PreStocks упала вдвое. Если целевая компания возражает, производный продукт, основанный на лежащих в его основе акциях, теряет основу для существования.

Ondo Global Markets, опираясь на лицензированного американского брокера, выпускает токенизированные акции, каждый токен обеспечен соответствующими базовыми ценными бумагами. Ее система соответствия требованиям надежна, а Американская депозитарно-клиринговая корпорация (DTCC) также создает для этого клиринговую инфраструктуру.

Но главное преимущество Ondo также является ее главной слабостью — ее юридическое лицо четко идентифицируемо и подотчетно. Если регуляторы приостановят деятельность или компания подаст иск о нарушении прав, соответствующие учреждения и кастодианы напрямую столкнутся с риском преследования. Работа по правилам может сделать их легкой мишенью для регулирующих ударов.

Синтетические бессрочные контракты на SpaceX, запущенные Hyperliquid, полностью оторваны от какого-либо физического актива. Продукт не связан с акциями, лицензированными учреждениями или правами собственности на реальные активы. Это чисто синтетический дериватив, расчеты по которому производятся исключительно в USDC в децентрализованной сети, а торговля ведется исключительно на основе движения цены.

Даже если SpaceX захочет остановить торговлю оценкой, у нее не будет рычагов воздействия. У продукта нет соответствующего юридического лица, на которое можно было бы подать в суд, и нет централизованного эмитента, на которого можно было бы оказать давление.

Эта модель искусно обходит риск ответственности. Нет физической основы — не будет и прямого удара.

Однако плюсы и минусы этой модели также трудно однозначно определить. Торговые каналы без проверки личности позволяют огромным капиталам перемещаться вне глобальной банковской системы, что действительно создает угрозу для национальной безопасности. 17 мая соучредитель Hyperliquid Джефф Ян отправился в Вашингтон на встречу с законодателями, что косвенно подтверждает серьезное давление со стороны регуляторов, с которым сталкивается платформа.

У основателя есть публичная личность и история. Если SpaceX подаст иск о нарушении прав на товарный знак или интеллектуальную собственность, на него можно будет подать в суд в соответствии с законом.

Однако преследование отдельных лиц не может остановить работу смарт-контракта. Продукт PreStocks зависит от реальных акций — если акции становятся недействительными, продукт умирает. Если счета платформы Ondo будут заморожены, ей будет трудно нормально функционировать.

Контракты Hyperliquid, напротив, развернуты на основе автономно работающего кода. Даже если основатель столкнется с юридическими проблемами, смарт-контракт, будучи развернутым, неизменяем, и ончейн-торговля заявками будет продолжать работать самостоятельно.

Это идеализированная форма децентрализованной концепции, но в реальной работе все еще есть недостатки. В сети валидаторов платформы Ondo всего 20 узлов, это не крупномасштабная распределенная сеть, и личность поддается отслеживанию. Предыдущий инцидент с токенами также доказал, что команда проекта может вмешиваться в дела платформы по своему усмотрению — узлы не являются абсолютно невмешиваемыми.

В конечном счете, преимущество во времени — возможность круглосуточной торговли — это ключевой барьер, который традиционные финансы не могут воспроизвести.