Author: Insightful Commentary

Some time ago, I was strongly recommended a few stocks related to minor metals. Looking back, I can only say it was a great tip. We shouldn't start researching only after getting stuck in a position; we should do our research *before* getting stuck. Hence, I recently started a new series: metal and mineral research, to examine the landscape of various minor metals.

Sometimes, market rumors are quite interesting. For instance, a few days ago, there was talk about increased explosives imports in Myanmar's Wa State, and immediately the price of tin dropped a bit. This hints at a potential supply-side story.

[Reminder: Fundamentals are just fundamentals; they are not meant to guide trading decisions.]

So-called minor metals aren't necessarily small, especially as a foundation for industrial transformation. Once a technological breakthrough occurs, a minor metal can very likely become a strategic metal.

For example, before becoming an "energy metal," the lithium market was not large, primarily used in glass, ceramics, lubricating greases, and other fields. But with the explosive growth of the new energy vehicle and energy storage industries, lithium, as a core raw material for power batteries, saw its demand and market size expand dramatically, fundamentally changing its status.

Magnesium is currently a relatively clear candidate to be the next minor metal listed on futures exchanges. The current global magnesium market is roughly at the million-ton level, mainly used as an aluminum alloy additive, for die-cast parts, etc. In the future, if magnesium sees major breakthroughs in lightweight materials (like automobiles, aerospace) or batteries, leading to orders-of-magnitude increases in production and consumption, it could very well be upgraded to a base metal or an independent category.

I remember vividly a segment from a previous Huaxia dialogue with Everbright's Qiu Suo on the non-ferrous market:

"Strategic minor metals, such as rare earths, tungsten-molybdenum, cobalt, nickel, tin—the value of these varieties will continue to be revalued. The core logic is the backdrop of global competition. Even if China-US competition eases temporarily, in the long run, the competitive nature of strategic metals will only intensify. These metals must meet two conditions: either strong scarcity or concentrated supply chains.

For example, cobalt: the Democratic Republic of Congo is the main supplier, and it uses cobalt supply as an important bargaining chip; pricing involves strong political factors. Another example is Indonesia's nickel and tin; global reliance on Indonesia is very high, and their inherent scarcity is prominent. They are very likely to become core varieties in the next round of competition. These varieties are either at a bottom, or their value hasn't been fully realized yet; there's significant room for revaluation in the future."

This year's strong performance in non-ferrous metals, aside from macro monetary reasons, is importantly due to the huge challenges faced by global supply chain security (especially for resources, mineral resource security).

China, as early as 2016, clarified its strategic mineral layout through top-level design: The State Council issued the "National Mineral Resources Plan (2016-2020)", using "ensuring national economic security, defense security, and the development needs of strategic emerging industries" as the core criteria, formally listing 24 minerals including chromium, aluminum, nickel, tungsten, tin, antimony, cobalt, lithium, rare earths, zirconium, crystalline graphite, petroleum, natural gas, shale gas, coal, coalbed methane, uranium, gold, iron, molybdenum, copper, phosphorus, potash, and fluorite into the strategic mineral catalog. This includes multiple core strategic metals, laying a solid resource foundation for the high-quality development of related industries.

China possesses "resource endowment + production advantage" in the four mineral areas of tungsten, antimony, tin, and molybdenum. Tungsten, antimony, tin, and molybdenum are China's four major strategic advantage minerals. Let's look at the supply of these four types of minerals.

I. Tin Supply Side Ore Types

The primary source of tin supply is cassiterite (SnO2, tin oxide), the main natural form of tin, accounting for over 95% of global tin ore resources. There are also smaller amounts of sulfide ores like stannite (Cu2FeSnS4), but their economic value is relatively low. Cassiterite is processed through beneficiation to produce tin concentrate, which is then smelted via pyrometallurgical or hydrometallurgical methods to produce refined tin.

2025 data is not fully released yet, but due to continued production halts in Myanmar's Wa State, production is expected to further drop below 20,000 tons, its share falling to around 7%. The top five producing countries account for 69% combined, the top eight account for 85% combined, indicating highly concentrated supply.

Myanmar's Wa State has a huge impact on the tin industry chain, primarily because:

1) Historical Supply Volume: Before the August 2023 production halt, Myanmar's normal annual production was about 50,000-60,000 tons (15-20% of global supply), with the Wa State region accounting for over 90% of Myanmar's total production, i.e., an annual supply of about 45,000-54,000 tons. This volume equates to one-sixth of global supply; a sudden halt created a huge gap.

2) Crucial for Chinese Tin Exports: China is the world's largest refined tin producer (45% of global production), but domestic mine resources are depleted, making it heavily reliant on imports. Myanmar was once China's largest source of tin concentrate imports; in 2022, about 36,000 metric tons of tin-in-concentrate were imported from Myanmar, accounting for 60-70% of China's total imports. The Wa State halt directly caused shortages for Chinese smelters.

3) High Uncertainty in Resuming Production: Although Wa State began the resumption process in 2025, affected by policy, equipment, rainy season, and other factors, the actual resumption progress is far below expectations. As of the end of 2025, monthly exports averaged only 2,000-3,000 physical tons (approx. 1,000-1,500 metal tons), far below the pre-halt monthly average of 3,000 metal tons.

4) Amplifies Global Supply-Demand Tight Balance: The global tin market has long been in a tight supply-demand balance (reserve-to-production ratio only 15 years); any minor fluctuation in a major supplier is amplified by the market. Wa State's "halt-slow resumption" process became the core driver for the sustained high tin prices in 2024-2025.

Tin ore is rarely found alone; it is often associated with various metal and non-metal minerals.

Deposits related to intermediate-acidic granites: This is the most important tin deposit type. In skarn-type (e.g., Hunan's Shizhuyuan deposit) and cassiterite-sulfide-type deposits (e.g., Yunnan's Gejiu, Guangxi's Dachang deposits), tin is often closely associated with tungsten, molybdenum, bismuth, copper, lead, zinc, silver, etc., forming large-scale polymetallic ore fields. In pegmatite-type deposits, tin tends to be associated with rare elements like niobium, tantalum, lithium, beryllium, rubidium, cesium.

Placer tin deposits: Formed by the weathering, transport, and enrichment of primary tin deposits. Besides cassiterite, placer deposits often also enrich heavy minerals like native gold, wolframite, monazite, rutile, fergusonite, making comprehensive utilization of placer tin deposits highly valuable.

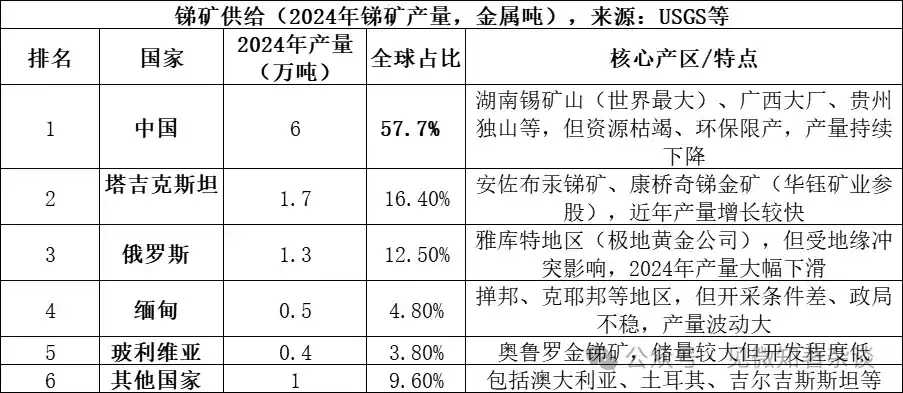

II. Antimony Supply Side Ore Types

The primary source of antimony supply is stibnite (Sb2S3, antimony sulfide), the main antimony ore in nature, accounting for over 80% of global antimony ore resources. There are also smaller amounts of secondary minerals like valentinite (Sb2O3, antimony trioxide). Stibnite is processed through beneficiation to produce antimony concentrate, which is then smelted via pyrometallurgical or hydrometallurgical methods to produce metallic antimony or antimony compounds.

The top three producing countries (China, Tajikistan, Russia) account for 86.6% combined, indicating highly concentrated supply. Although China's production share is over half, it has significantly decreased from the 90% share in 2010, mainly due to tightened environmental policies and resource depletion.

Antimony ore associations:

Mainly found in medium-low temperature hydrothermal environments: The vast majority of economically valuable antimony deposits form under medium-low temperature hydrothermal conditions. In this environment, stibnite often precipitates along with cinnabar (mercury), pyrite, quartz, and other minerals, forming typical low-temperature hydrothermal deposits.

Characteristic associations by type: 1) In the famous Xikuangshan Antimony Mine in Hunan, stibnite is associated with pyrite, orpiment, realgar, cinnabar, calcite, quartz, etc.; 2) When antimony mineralization overlaps with gold or tungsten mineralization, higher-value complex deposits like antimony-gold-tungsten are formed.

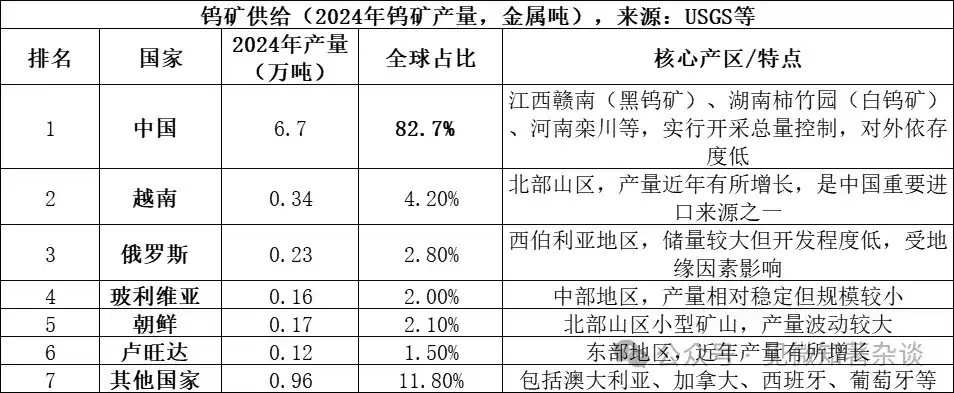

III. Tungsten Supply Side Ore Types

The primary sources of tungsten supply are scheelite (CaWO4, calcium tungstate) and wolframite ((Fe,Mn)WO4, iron-manganese tungstate), the two main ore forms of tungsten in nature. Among them, scheelite accounts for over 70% of global tungsten resources, wolframite accounts for 25-30%. Scheelite is mostly found in skarn-type deposits, wolframite mostly in high-temperature hydrothermal quartz vein-type deposits. Both are processed through beneficiation to produce tungsten concentrate (≥65% WO3 content), which is then smelted via pyrometallurgical or hydrometallurgical methods to produce ammonium paratungstate (APT), tungsten oxide, or metallic tungsten.

Tungsten market supply structure:

1) China dominates supply, but growth is weak: China is not only the largest tungsten producer (83% of global production) but also holds about 52% of global tungsten ore reserves. However, domestic tungsten mining is strictly managed by total control quotas. Although the 2024 mining quota was set at 114,000 tons, actual production was 127,000 tons, indicating that over-mining has been effectively controlled. Simultaneously, long-term mining has depleted high-grade ores, and the original ore grade continues to decline, constraining supply growth from the source.

2) Limited new supply overseas: In 2024, global tungsten mine production outside China was about 14,000 metal tons, from scattered sources. Important new supply mainly comes from projects like the Bakuta Tungsten Mine in Kazakhstan, but these represent a small share of global supply and are unlikely to change the China-dominated supply structure in the short term.

3) Recycled tungsten is an important supplement: Besides primary ore, recycled tungsten scrap (e.g., used hard metals) is also an important supply source. Currently, about 35% of global tungsten supply comes from recycled materials, although China's recycling rate and product quality still lag behind international advanced levels.

Tungsten ore associations:

Quartz vein-type and greisen-type deposits: These deposits are typically associated with granite intrusions. Associated minerals are very rich; besides wolframite, cassiterite, molybdenite, bismuthinite, beryl, topaz, tourmaline, etc., are common. They often occur in quartz veins at the top of granite bodies or in nearby country rock.

Skarn-type deposits: These deposits form at the contact zone between intermediate-acidic intrusive rocks and carbonate rocks (like limestone), primarily containing scheelite. Their associated mineral assemblage differs from quartz vein types, often closely associated with sulfides like chalcopyrite, galena, sphalerite, as well as molybdenite. The Shizhuyuan deposit in Chenzhou, Hunan, is a world-class example, enriching tungsten, tin, molybdenum, bismuth, beryllium, fluorite, and other resources simultaneously.

IV. Molybdenum Supply Side Ore Types

The primary source of molybdenum supply is molybdenite (MoS2, molybdenum disulfide), the main and most economically valuable molybdenum ore in nature. Molybdenite is often associated with copper, tungsten, and other metals in porphyry-type deposits. The ore is processed through beneficiation to produce molybdenum concentrate (typically requiring ≥85% MoS2 content), which is then processed through roasting or hydrometallurgical methods to produce molybdenum oxide (technical molybdenum oxide), ferromolybdenum, ammonium molybdate, and other products, used subsequently in steel alloys, chemicals, and other fields.

The top five producing countries (China, Peru, Chile, USA, Mexico) account for 91.9% combined, indicating highly concentrated supply; global molybdenum reserves in 2024 were about 15 million tons, with Chinese reserves at 5.9 million tons (39.3% share), and a reserve-to-production ratio of about 57 years.

China holds a triple position in the molybdenum market: "resources + production + consumption":

1) Resource Endowment Advantage: China holds nearly 40% of global molybdenum reserves (5.9 million tons in 2024), primarily primary molybdenum deposits, with large deposit scales and relatively high grades (e.g., Luanchuan molybdenum mine average grade around 0.1%), giving it a resource endowment superior to most countries.

2) Absolute Production Dominance: China's molybdenum production accounts for over 42% of the global total and has ranked first globally for many consecutive years. Unlike metals like tin or antimony, China's molybdenum industry does not rely on imports; raw material self-sufficiency exceeds 90%, differing from the tin market where China depends on imports from Myanmar.

3) Complete Industrial Chain: China possesses a complete industrial chain from mining, beneficiation, to smelting and deep processing (ferromolybdenum, molybdenum powder, molybdenum chemicals). Leading companies like China Molybdenum Co., Ltd. (CMOC) and Jinduicheng Molybdenum Co., Ltd. possess global competitiveness.

4) Consumption Market: China is also the world's largest molybdenum consumer (2024 consumption about 130,000 tons, over 45% of global total),主要用于钢铁合金 (over 70% of consumption), forming a closed-loop system of self-production and self-consumption.

5) A large portion of global molybdenum is a by-product of copper mining: The ore grades of many large porphyry copper mines are declining. Several major copper mines may reach end-of-life by the mid-2030s, which will constrain future molybdenum supply growth.

Molybdenum ore associations:

Porphyry Molybdenum / Porphyry Copper Deposits: This is the world's most important molybdenum deposit type. In porphyry copper deposits (e.g., Dexing Copper Mine), molybdenum (molybdenite) is closely associated with copper sulfides as a by-product. In porphyry molybdenum deposits (e.g., Henan's Luanchuan, Shaanxi's Jinduicheng), molybdenum is the primary product but is often associated with elements like tungsten and rhenium.

Skarn-type deposits: These deposits form at the contact zone between intermediate-acidic intrusive rocks and carbonate rocks. Here, molybdenite is often closely associated with scheelite, forming a molybdenum-tungsten combination (e.g., Hunan's Shizhuyuan deposit), and can also be associated with various metal sulfides.

Quartz vein-type and greisen-type deposits: These deposits are typically associated with granite. In wolframite-quartz veins, molybdenite is often present as an associate, along with possible bismuthinite, arsenopyrite, and other minerals.