Автор: Тао Чжу, Jinse Finance

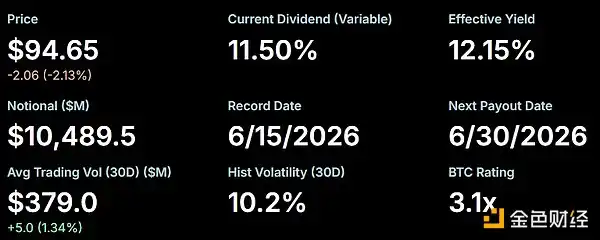

Краткое содержание: 29 мая STRC упал до 97,11 доллара, затем восстановился и закрылся на отметке 98,57 доллара. После этого STRC преимущественно снижался и на момент публикации торгуется на уровне 94,65 доллара. Для привилегированной акции, целью которой является долгосрочная торговля вокруг номинала в 100 долларов, такое падение действительно привлекает внимание рынка.

I. Что такое STRC?

Согласно описанию на официальном сайте Strategy, Stretch (STRC) — это бессрочные привилегированные акции компании Strategy, текущая годовая дивидендная доходность составляет 11,50%, выплаты производятся ежемесячно наличными. Дивидендная ставка STRC корректируется ежемесячно, что призвано стимулировать торговлю акциями вокруг их номинальной стоимости в 100 долларов и снизить ценовую волатильность. STRC торгуется на NASDAQ и доступна для торговли на большинстве крупных брокерских платформ.

«Привилегированность» означает более высокий приоритет по сравнению с обыкновенными акциями при распределении дивидендов и ликвидации. Как привилегированные акции, выпущенные Strategy, STRC занимают положение выше обыкновенных акций, но ниже облигаций. Конкретно, «привилегированность» акций может проявляться в двух аспектах. Во-первых, приоритетное получение дивидендов: акционеры привилегированных акций получают дивиденды раньше акционеров обыкновенных акций, и при недостатке прибыли акционеры привилегированных акций также получают доход в первую очередь. Во-вторых, приоритетное возмещение при банкротстве компании: по сравнению с полной потерей основной суммы у обыкновенных акций, привилегированные акции могут вернуть часть основной суммы.

По своей сути STRC больше похож на «продукт с высокодоходным денежным потоком», чем на акции роста, ориентированные на прирост капитала. Основная цель многих инвесторов, покупающих STRC, — получение доходности выше 11%, а не рост цены акций.

II. Почему STRC недавно отвязался от паритета?

1. Падение цены BTC

Самый крупный актив Strategy — это биткоин, он тесно связан с ценой BTC. В конце мая на криптовалютном рынке в целом произошла заметная коррекция: цена BTC упала с максимума в этом месяце около 82 000 долларов до текущих на момент публикации примерно 64 300 долларов, снижение составило 21,59%.

Быстрое падение BTC с высоких уровней привело к распродажам рисковых активов, продукты, связанные со Strategy, также оказались под давлением.

2. Давление со стороны конкурентов

Другая компания по управлению активами в биткоинах, Strive Asset Management (ASST), придерживается другой стратегии. Компания недавно объявила, что ее бессрочные привилегированные ценные бумаги SATA будут выплачивать дивиденды ежедневно. В течение последних двух недель цена SATA оставалась стабильной около номинальной стоимости в 100 долларов, а ее дивидендная доходность сохранялась на уровне около 13%, даже при падении цены биткоина.

За последние три месяца акции Strive выросли примерно на 110%, тогда как MSTR — только на 12%, а биткоин — всего на 8%. Такая дивергенция указывает на то, что инвесторы, возможно, предпочитают более устойчивый баланс Strive и структуру привилегированных акций с более высокой доходностью.

Примечание: Изначально Strive была компанией по управлению активами, основанной в 2022 году со штаб-квартирой в Далласе, штат Техас. Изначально она в основном выпускала ETF-фонды и была известна своей концепцией «максимизации акционерной стоимости (shareholder value maximization)». С 2025 года Strive претерпела серьезную трансформацию. Она начала копировать модель Strategy — стать компанией, накапливающей биткоин, и выпускать привилегированные акции.

Возможно, вдохновленная ежедневными выплатами дивидендов Strive, как показано в объявлении, Strategy предложила изменить частоту выплат дивидендов по STRC с ежемесячной на раз в две недели. Если предложение будет одобрено и принято, ожидается, что это сократит период задержки реинвестирования, повысит ликвидность и эффективность рынка, а также улучшит ценовую стабильность.

Это предложение требует совместного голосования акционеров двух классов — MSTR и STRC, и оно может быть принято только при одобрении обоими классами акционеров. Согласно графику предложения, голосование началось 28 апреля и завершится в день собрания 8 июня. В случае одобрения, первая дата регистрации прав по новому графику — 30 июня, а первая дата выплаты дивидендов — 15 июля. Акционеры, имеющие право голоса, должны были владеть акциями до 17 апреля.

3. Технические распродажи

Strategy хочет, чтобы STRC долгосрочно торговался около 100 долларов. Когда цена STRC падает ниже 100 долларов, многие количественные фонды могут посчитать, что рынок ставит под сомнение механизм ценообразования этого продукта. Тогда могут возникнуть такие проблемы, как пассивное сокращение позиций, технические стоп-лоссы, уход арбитражного капитала и т.д., что может привести к дальнейшему расширению падения.

III. Существует ли риск дефолта по STRC?

В настоящее время явного риска дефолта нет.

Во-первых, ранее инвесторы задавались вопросом, будет ли Strategy в конечном итоге продавать биткоины для погашения долгов или выплаты дивидендов, или продолжит использовать средства, привлеченные от выпуска ценных бумаг, для увеличения своих запасов биткоина. Сайлор в своем посте в X ответил: «Работа идет хорошо».

1 июня основатель Strategy Майкл Сайлор подтвердил, что дивидендная доходность бессрочных привилегированных акций STRC в июне 2026 года останется неизменной на уровне 11,50%. Дивиденды по STRC не сокращены, не приостановлены и нет дефолта, все идет нормально.

Во-вторых, Strategy по-прежнему обладает огромными запасами биткоина. Strategy прочно занимает первое место среди корпоративных казначейств по запасам BTC с 843 706 BTC, что составляет 4,01% от общего предложения в 21 миллион монет. При условии отсутствия долгосрочного обвала BTC и незакрытых каналов финансирования компании, давление на денежный поток STRC остается управляемым.

IV. Что думают представители отрасли?

-

Forbes отмечает: STRC вышел на биржу в июле 2025 года, это было крупнейшее IPO в США в том году, объем привлеченных средств составил 25,21 миллиарда долларов, ежемесячные выплаты дивидендов составляют около 80-90 миллионов долларов. Открыто и намеренно продавая небольшое количество биткоинов для выполнения этих обязательств, Strategy показывает рейтинговым агентствам, что компания рассматривает держателей привилегированных акций как приоритетных кредиторов. Эта репутация делает STRC более привлекательным. Рост спроса на STRC означает привлечение большего объема финансирования, что, в свою очередь, приводит к покупке большего количества биткоинов.

-

Аналитик Benchmark Марк Палмер указывает: «Теперь инвесторы должны рассматривать запасы биткоина Strategy как надежный резервный план для финансирования дивидендов по привилегированным акциям».

-

Известный сторонник золота и ненавистник криптовалют Питер Шифф написал в X: «Большинство инвесторов в STRC в конечном итоге могут потерять большую часть своих средств, потому что как только Майклу Сайлору придется отменить выплату дивидендов, цена STRC в конечном итоге рухнет. Тогда большое количество судебных исков, вероятно, еще больше усугубит проблемы, с которыми сталкивается Strategy (MSTR). Ожидается, что инвесторы, понесшие убытки из-за вводящей в заблуждение рекламы, будут искать компенсацию через судебные разбирательства, чтобы вернуть свои инвестиции».

-

The Motley Fool считает: Во-первых, следует обратить внимание на проблему инфляции в отношении STRC. Инфляция наносит двойной удар: она размывает реальную стоимость ваших акций в 100 долларов, а также снижает стоимость получаемых дивидендов. Таким образом, чем дольше вы держите эти акции, тем серьезнее становится проблема инфляции. Во-вторых, Strategy может легко сократить или отсрочить выплату дивидендов без традиционного долгового дефолта. Поэтому, если цена упадет ниже номинала, выпуск новых акций прекратится, и тогда вы будете держать актив с доходностью ниже первоначально заявленной, и основная сумма может не быть возвращена в краткосрочной перспективе или даже никогда.

Итог

Недавнее падение STRC с уровня около 100 долларов до 94,65 доллара в основном обусловлено такими факторами, как падение цены биткоина, влияние конкурентов, технические распродажи и т.д. На данный момент риск дефолта по STRC отсутствует, компания продолжает выплачивать дивиденды на уровне 11,5% и по-прежнему рассматривает STRC как основной инструмент финансирования.