Автор: Prathik Desai

Компиляция: Chopper, Foresight News

Оригинальное название: Кто контролирует жизненно важные источники дохода в криптоиндустрии?

Мне нравятся сезонные традиции криптоиндустрии, такие как «Октябрьский рост» (Uptober) и «Октябрьский хаос» (Recktober). Сообщество всегда выкладывает кучу данных вокруг этих событий, а люди ведь любят такие интересные факты, не так ли?

Тенденции и отчеты вокруг этих событий еще интереснее: «На этот раз потоки ETF отличаются», «Финансирование в криптоиндустрии наконец-то стало зрелым в этом году», «Биткоин готов к росту в этом году» и так далее. Недавно, просматривая «Отчет о состоянии индустрии DeFi за 2025 год», меня заинтересовали несколько графиков о том, как криптопротоколы создают «значительный доход».

Эти графики перечисляют ведущие криптопротоколы с самым высоким годовым доходом, подтверждая факт, который многие в индустрии обсуждали в прошлом году: криптоиндустрия наконец-то начинает делать доход привлекательным. Но что именно движет этот рост доходов?

За этими графиками скрывается еще один малоизвестный вопрос, который стоит изучить: куда в конечном итоге поступают эти комиссии?

На прошлой неделе я углубился в данные о комиссиях и доходах DefiLlama (прим.: доход относится к комиссиям, оставшимся после выплат поставщикам ликвидности и провайдерам), пытаясь найти ответ. В сегодняшнем анализе я добавлю больше деталей к этим данным, чтобы объяснить, как и куда движутся деньги в криптоиндустрии.

Криптопротоколы создали доход в размере более 16 миллиардов долларов в прошлом году, что более чем в два раза превышает примерно 8 миллиардов долларов в 2024 году.

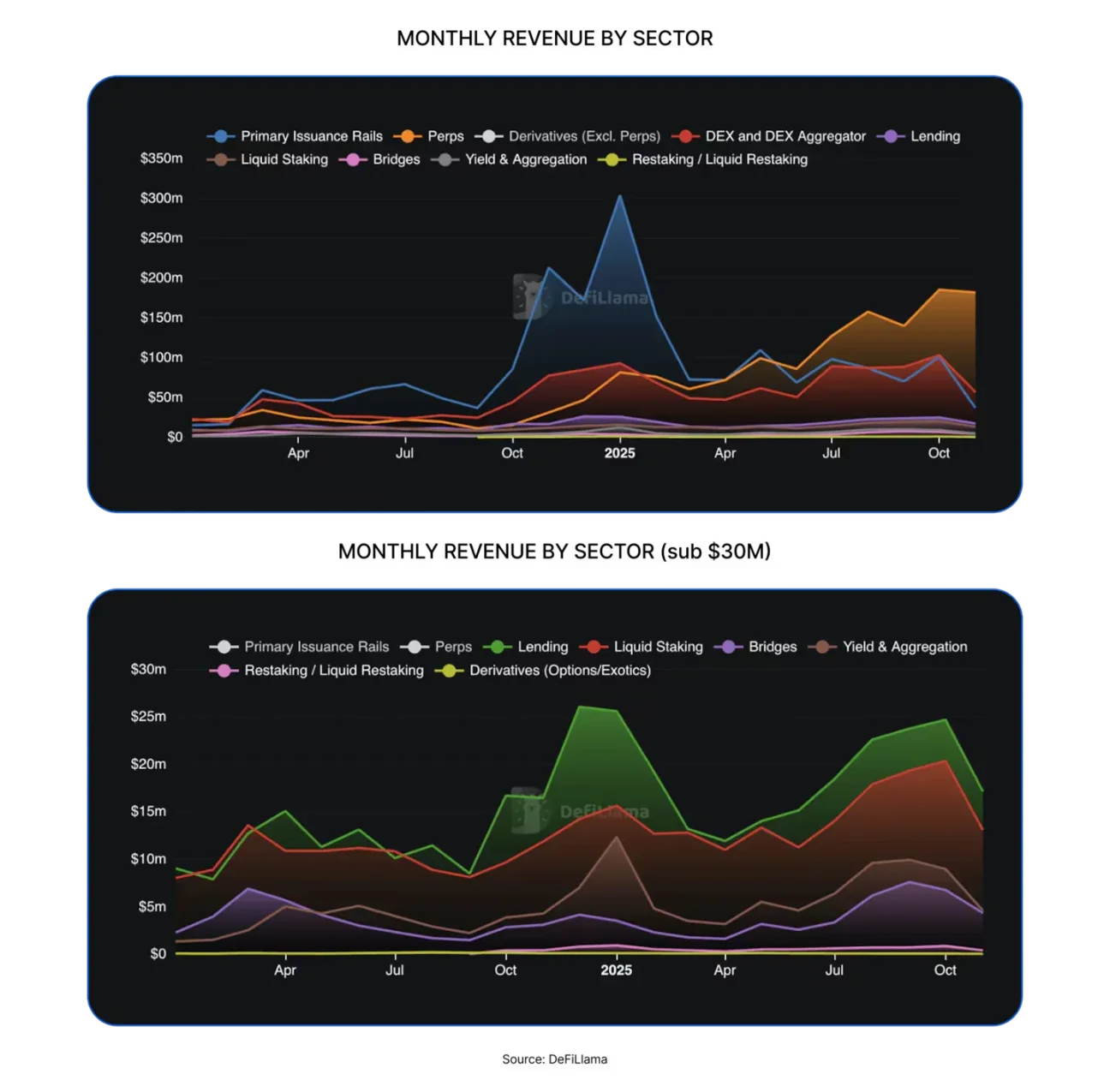

Способность криптоиндустрии捕获 стоимость全面提升, за последние 12 месяцев в области децентрализованных финансов (DeFi) появилось множество новых направлений, таких как децентрализованные биржи (DEX), платформы выпуска токенов и децентрализованные биржи перпетных контрактов (perp DEX).

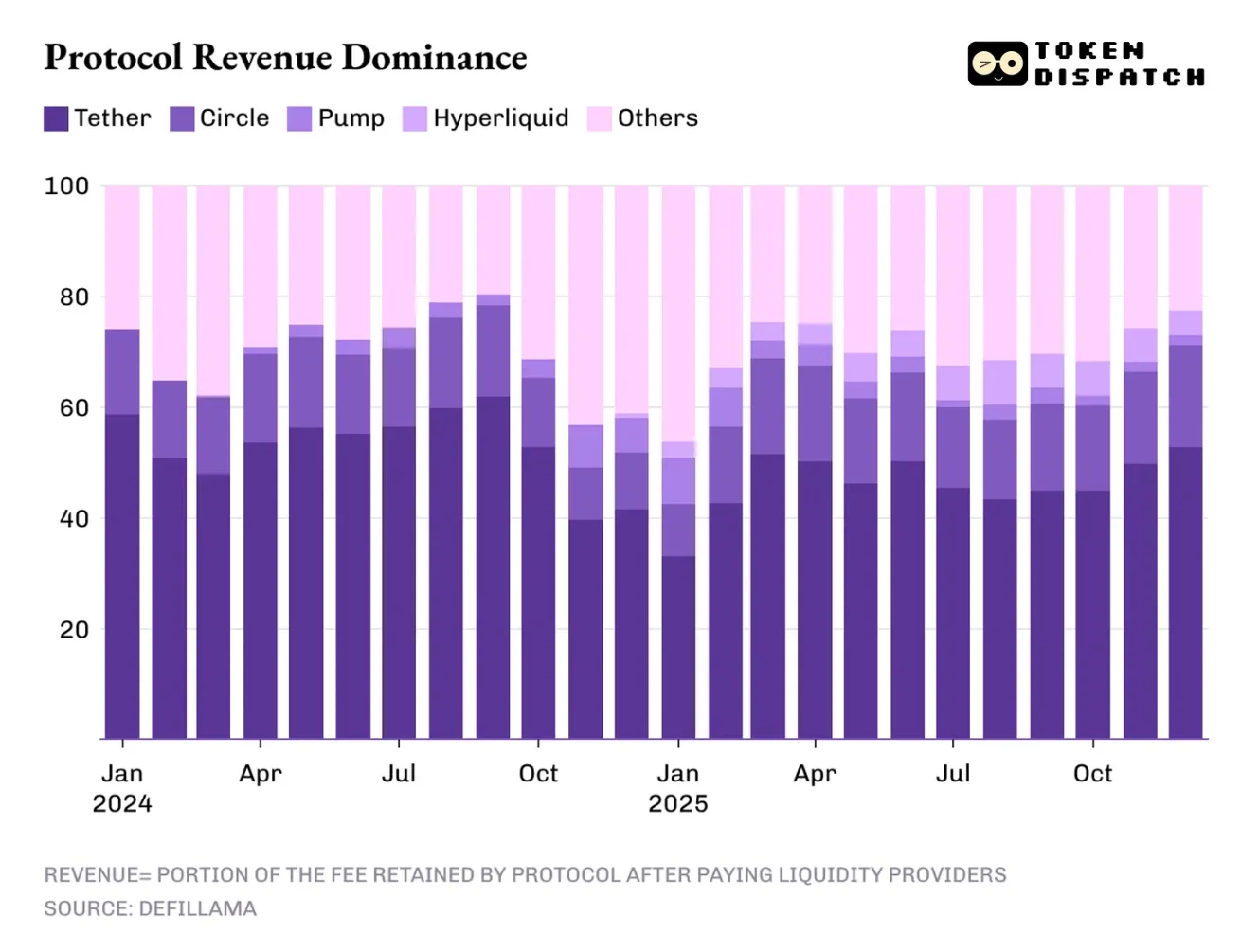

Однако центры прибыли, генерирующие наибольший доход, по-прежнему сосредоточены в традиционных секторах, и наиболее выделяются среди них эмитенты стейблкоинов.

Два ведущих эмитента стейблкоинов, Tether и Circle, обеспечили более 60% общего дохода криптоиндустрии. В 2025 году их доля рынка незначительно снизилась с примерно 65% в 2024 году до 60%.

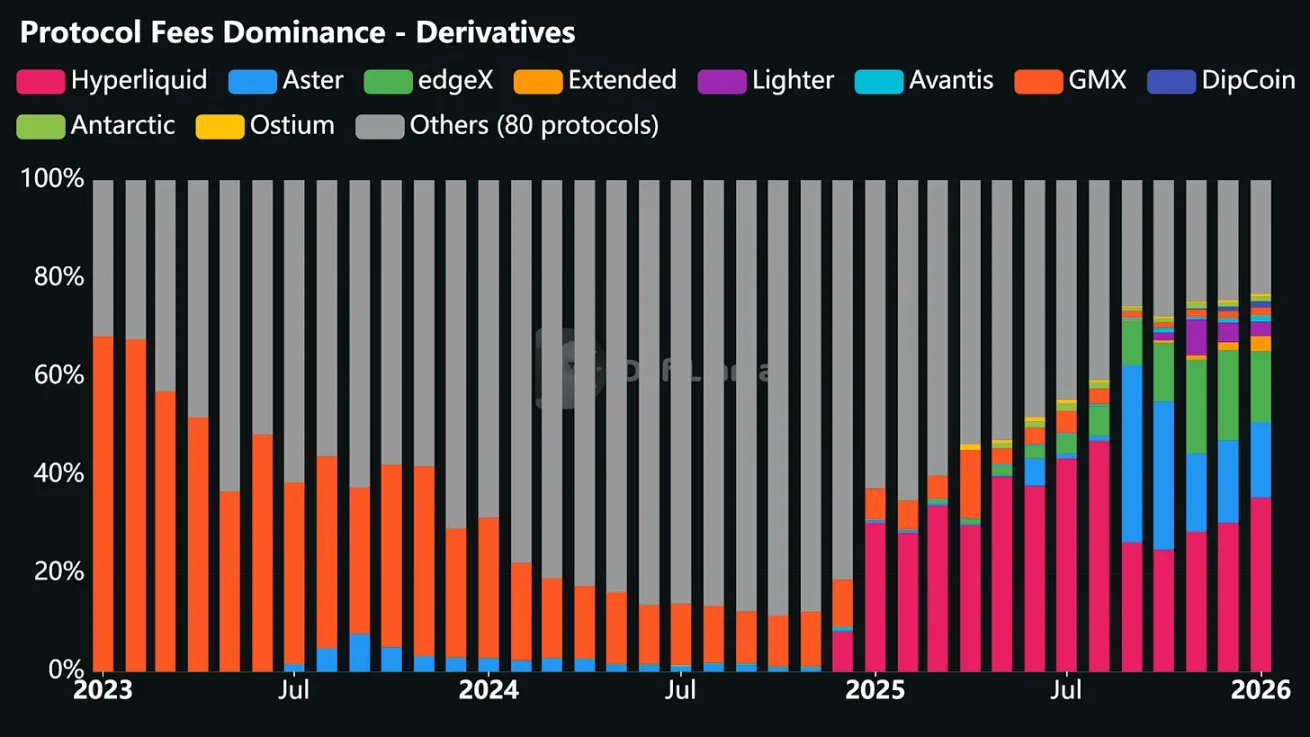

Но нельзя недооценивать表现 децентрализованных бирж перпетных контрактов в 2025 году, этот сектор в 2024 году был практически незаметен. Четыре платформы — Hyperliquid, EdgeX, Lighter и Axiom — вместе заняли от 7% до 8% общего дохода индустрии, что значительно превышает совокупный доход протоколов таких зрелых секторов DeFi, как кредитование, стейкинг, мосты и агрегаторы децентрализованных бирж.

Так что же будет движущей силой дохода в 2026 году? Я нашел ответ в трех основных факторах, повлиявших на ландшафт доходов криптоиндустрии в прошлом году: доход от спреда, исполнение сделок и дистрибуция каналов.

Торговля спредом означает, что тот, кто держит и перемещает деньги, получает прибыль от этого процесса.

Модель дохода эмитентов стейблкоинов является одновременно структурной и хрупкой. Ее структурность заключается в том, что масштабы дохода расширяются синхронно с объемом предложения и обращения стейблкоинов: каждый цифровой доллар, выпущенный эмитентом, обеспечен казначейскими облигациями США и приносит проценты. Хрупкость же заключается в том, что эта модель зависит от макроэкономических переменных, которые эмитент почти не контролирует: процентных ставок ФРС. Сейчас цикл монетарного смягчения только начинается, и по мере дальнейшего снижения ставок в этом году доминирующее положение эмитентов стейблкоинов в доходах также ослабнет.

Далее следует уровень исполнения сделок, место рождения самого успешного сектора DeFi в 2025 году — децентрализованных бирж перпетных контрактов.

Самый простой способ понять, почему децентрализованные биржи перпетных контрактов так быстро заняли значительную долю рынка, — это посмотреть, как они помогают пользователям выполнять торговые операции. Эти платформы создали торговые площадки с низким трением, позволяющие пользователям входить и выходить из рискованных позиций по мере необходимости. Даже если волатильность рынка низкая, пользователи все равно могут хеджировать, использовать leverage, арбитражировать, корректировать позиции или заранее открывать позиции для будущих развертываний.

В отличие от спотовых децентрализованных бирж, децентрализованные биржи перпетных контрактов позволяют пользователям совершать непрерывные, высокочастотные сделки без необходимости тратить усилия на перемещение базовых активов.

Хотя логика исполнения сделок звучит просто и выполняется очень быстро, техническая поддержка behind the scenes гораздо сложнее, чем кажется на поверхности. Эти платформы должны создавать стабильные торговые интерфейсы, обеспечивающие стабильность при высоких нагрузках; создавать надежные системы сопоставления ордеров и ликвидации, остающиеся стабильными в условиях рыночного хаоса; а также обеспечивать достаточную глубину ликвидности для удовлетворения потребностей трейдеров. На децентрализованных биржах перпетных контрактов ликвидность является ключом к победе: тот, кто может постоянно обеспечивать достаточную ликвидность, привлечет наибольший объем торговой активности.

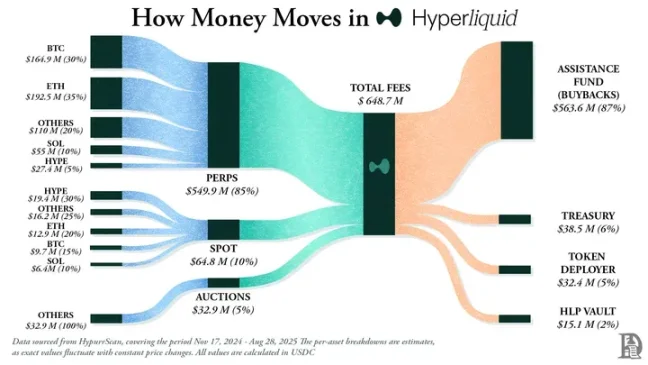

В 2025 году Hyperliquid доминировал в секторе децентрализованной торговли перпетными контрактами благодаря充足ной ликвидности, предоставляемой наибольшим количеством маркет-мейкеров на платформе. Это позволило платформе в течение 10 из 12 месяцев прошлого года быть децентрализованной биржей перпетных контрактов с самыми высокими доходами от комиссий.

Ирония заключается в том, что эти биржи перпетных контрактов в секторе DeFi смогли добиться успеха именно потому, что они не требовали от трейдеров понимания блокчейна и смарт-контрактов, а采用了人们熟悉的传统交易所运作模式.

Как только все вышеперечисленные проблемы решены, биржа может добиться автоматического роста доходов, взимая с трейдеров небольшие комиссии за их高频ные и крупные сделки. Даже если спотовые цены движутся в боковом тренде, доход может сохраняться, и причина в том, что платформа предоставляет трейдерам богатый выбор операций.

Именно поэтому я считаю, что, хотя доля доходов децентрализованных бирж перпетных контрактов в прошлом году составляла лишь однозначные цифры, это единственный сектор, который потенциально может бросить вызов доминированию эмитентов стейблкоинов.

Третий фактор — это дистрибуция каналов, которая приносит инкрементный доход таким криптопроектам, как инфраструктура выпуска токенов, например, платформы pump.fun и LetsBonk. Это не сильно отличается от模式, которые мы видим в Web2-компаниях: Airbnb и Amazon не владеют никакими inventory, но благодаря огромным каналам дистрибуции они давно вышли за рамки агрегаторов, а также снизили предельные затраты на новое предложение.

Инфраструктура выпуска криптотокенов также не владеет криптоактивами, такими как мемкоины, различные токены и микро-сообщества, созданные через ее платформу. Но, обеспечивая беспрепятственный пользовательский опыт, автоматизируя процесс листинга, предоставляя充足ную ликвидность и упрощая торговые операции, эти платформы стали предпочтительным местом для выпуска криптоактивов.

В 2026 году два вопроса могут определить траекторию развития этих драйверов дохода: упадет ли доля доходов эмитентов стейблкоинов в индустрии ниже 60% по мере снижения процентных ставок, ударяющих по торговле спредом? Сможет ли доля рынка платформ перпетных контрактов превысить 8% по мере консолидации ландшафта уровня исполнения сделок?

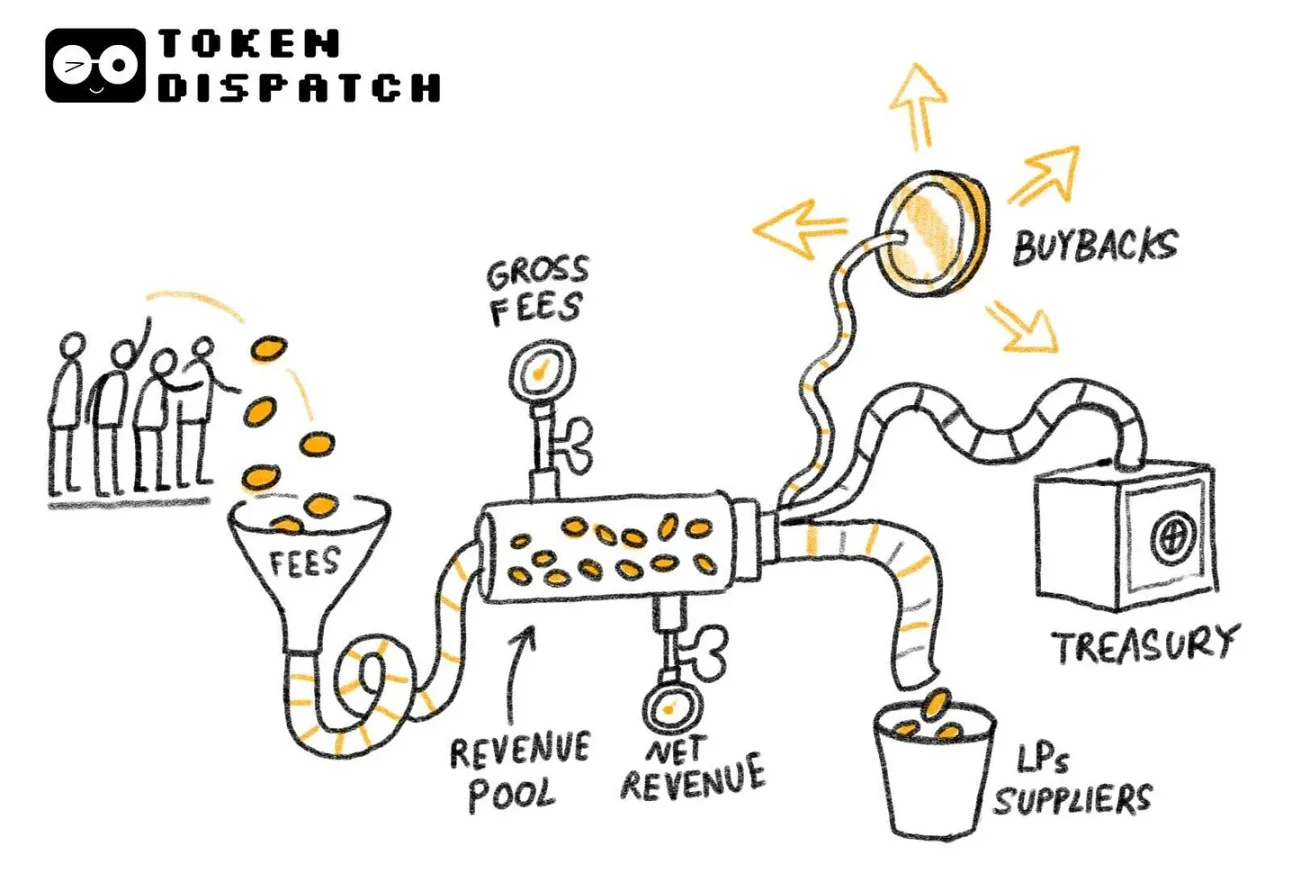

Доход от спреда, исполнение сделок и дистрибуция каналов — эти три фактора揭示, откуда берется доход в криптоиндустрии, но это только половина истории. Не менее важно понимать, какая доля общих комиссий分配ляется держателям токенов до того, как протокол сохранит чистый доход.

Передача стоимости через выкуп токенов, сжигание и распределение комиссий означает, что токены больше не являются просто инструментами управления, а представляют собой экономическое право собственности на протокол.

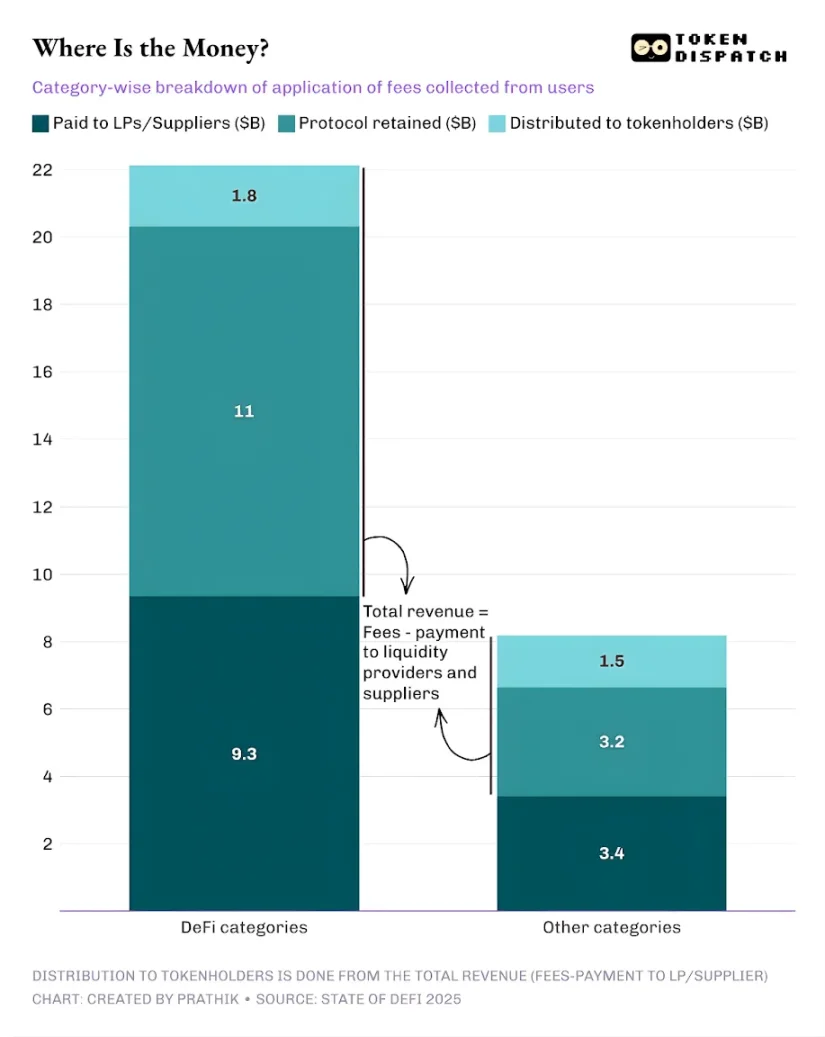

В 2025 году пользователи децентрализованных финансов и других протоколов заплатили общие комиссии на сумму около 30,3 миллиарда долларов. Из них протоколы сохранили доход в размере около 17,6 миллиарда долларов после выплат поставщикам ликвидности и провайдерам. Из общего дохода примерно 3,36 миллиарда долларов были возвращены держателям токенов в виде стейкинг-вознаграждений, распределения комиссий, выкупа и сжигания токенов. Это означает, что 58% комиссий были преобразованы в доход протокола.

По сравнению с предыдущим отраслевым циклом это уже значительное изменение. Все больше протоколов начинают экспериментировать с тем, чтобы сделать токены требованием права собственности на операционные результаты, что предоставляет инвесторам реальные стимулы продолжать держать и открывать длинные позиции по проектам, в которые они верят.

Криптоиндустрия далека от совершенства, большинство протоколов по-прежнему не распределяют任何 доход среди держателей токенов. Но с макроскопической точки зрения в индустрии произошли немалые изменения, и этот сигнал указывает на то, что все движется в хорошем направлении.

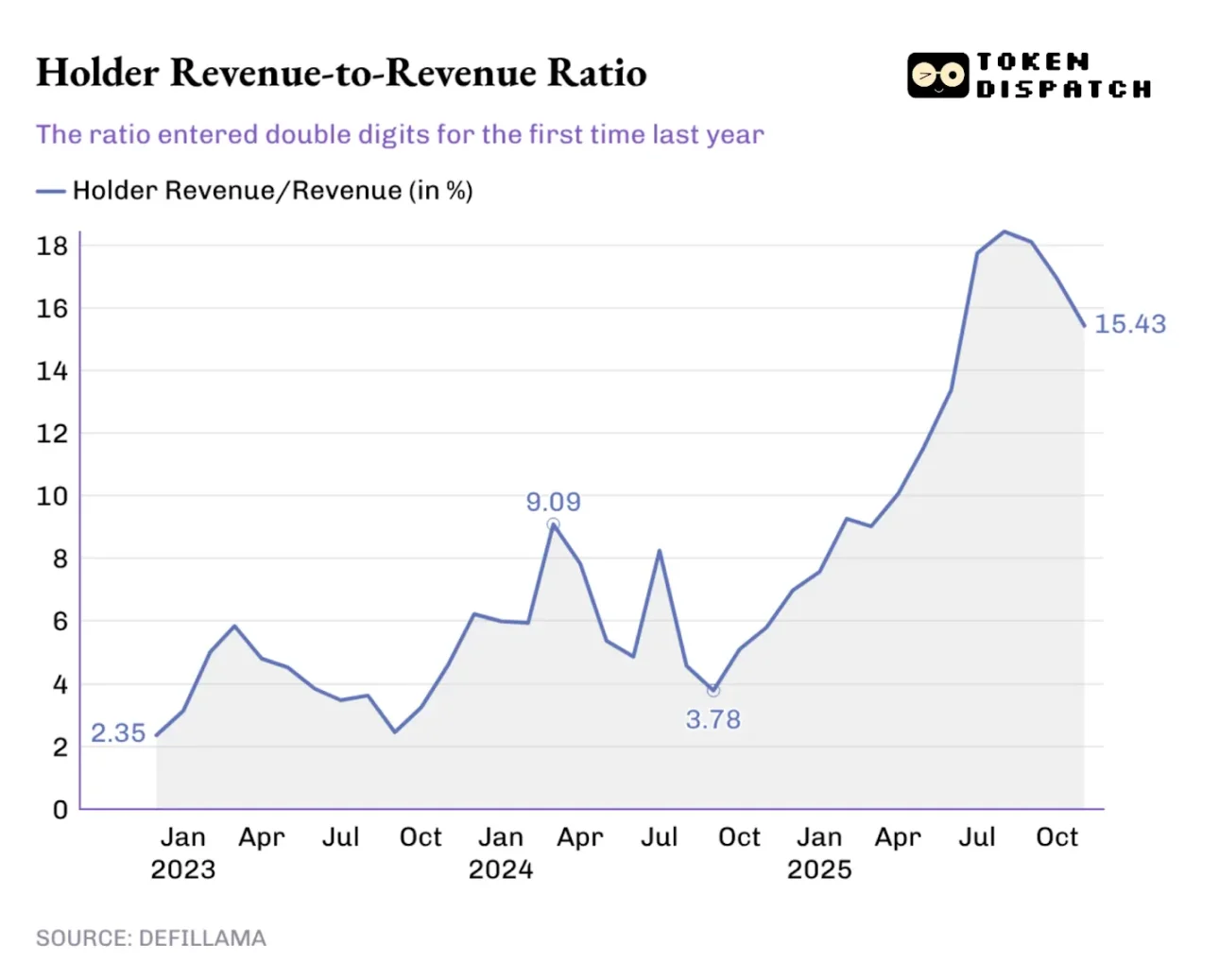

За последний год доля дохода держателей токенов в общем доходе протоколов持续增长, в начале прошлого года она превысила исторический максимум в 9,09%, а в пике в августе 2025 года даже превысила 18%.

Это изменение также отражается в торговле токенами: если токены, которые я держу, никогда не приносят никакой отдачи, мои торговые решения будут зависеть только от медийных нарративов; но если токены, которые я держу, могут приносить мне доход через выкуп или распределение комиссий, я буду рассматривать их как приносящие доход активы. Хотя они не обязательно безопасны и надежны, это转变 все равно повлияет на то, как рынок оценивает токены, приблизив их valuation к基本面, а не оставляя его на усмотрение медийных нарративов.

Когда инвесторы оглядываются на 2025 год, пытаясь предсказать, куда будут направляться доходы криптоиндустрии в 2026 году, стимулы станут важным фактором考虑. В прошлом году команды проектов, которые уделяли приоритетное внимание передаче стоимости, действительно выделялись.

Hyperliquid создал уникальную экосистему сообщества, возвращая около 90% дохода пользователям через Фонд помощи Hyperliquid.

Среди платформ выпуска токенов pump.fun укрепил концепцию «вознаграждения активных пользователей платформы», сжег 18,6% объема обращения原生ного токена PUMP за счет ежедневного выкупа.

В 2026 году ожидается, что «передача стоимости» перестанет быть нишевым выбором и станет обязательной стратегией для всех протоколов, которые希望, чтобы их токены торговались на основе基本面的. Изменения на рынке в прошлом году научили инвесторов различать доход протокола и стоимость для держателей токенов. Как только держатели токенов осознают, что токены на их руках могут представлять требование права собственности, возврат к предыдущей модели будет казаться нерациональным.

Я считаю, что «Отчет о состоянии индустрии DeFi за 2025 год» не揭示全新的 суть探索 криптоиндустрией моделей дохода, эта тенденция уже активно обсуждалась в течение последних нескольких месяцев. Ценность этого отчета заключается в использовании данных для揭示 истины, и, копнув глубже в эти данные, мы можем найти секрет того, где криптоиндустрия, скорее всего, добьется успеха в доходах.

Проанализировав доминирующие тенденции доходов различных протоколов, отчет четко указывает: тот, кто контролирует ключевые каналы, доход от спреда, исполнение сделок и дистрибуцию каналов, получает наибольшую прибыль.

В 2026 году я ожидаю, что больше проектов будут преобразовывать комиссии в долгосрочную отдачу для держателей токенов, особенно на фоне снижения привлекательности торговли спредом из-за цикла снижения процентных ставок.

Twitter:https://twitter.com/BitpushNewsCN

Группа общения比推 TG:https://t.me/BitPushCommunity

Подписка比推 TG: https://t.me/bitpush