Author: Thejaswini M A

Compiled by: Saoirse, Foresight News

The most expensive thing placed before a person is the need to make autonomous decisions. In comparison, the cost of fees is insignificant. People are willing to pay for peace of mind and convenience, nothing more.

The platform's extraction logic stems from this: removing the burden of decision-making from users. There is a term I like in Tim Wu's book 'The Age of Extraction' — 'passive restraint'. Platforms complete their extraction by depriving users of their autonomy in choice.

Don't know where to start with picking stocks? No problem, index funds, the S&P 500 will handle it for you. Don't understand lending products? Then change the name, package them directly as savings accounts, and promote them heavily. Their essence is charging a 'convenience service fee': saving users from decision-making, sometimes also taking away the excess returns that should belong to the users, and the public doesn't mind.

Traditional DeFi does the exact opposite, piling a massive amount of complex choices onto users: which public chain to choose, which liquidity pool, what are the real-time interest rates, when to move funds, whether cross-chain bridges have security risks, and also discerning if a page is the official platform or a phishing imitation site generated with the help of Claude before July 12th. Aave has only accumulated 2.5 million users after six years of deep cultivation, while Revolut, which focuses on minimalist operation, has 65 million users. Therefore, saying Aave needs to adapt to ordinary user demands and optimize the user experience is not an overstatement.

From January to July this year, the annualized interest rate for Aave's USDC pool fluctuated wildly between 2% and 9%. Interest rate volatility is the norm in DeFi: users watch rates rise and fall, moving funds wherever yields are higher. But this model simply cannot be marketed to the general public. Emerging digital banks cannot explain to users: deposit returns are determined by market borrowing demand and could drop to 2% one day. Users won't entrust their funds to such uncertain products, which is also the core reason why the vast majority never touch crypto wealth management applications.

On July 9th, Aave Labs launched a solution — Stable Vaults. This article will break down its operating logic, who benefits from it, and why ordinary users will still use this product even if they know the cost.

Stable Vaults Operating Mechanism

Any enterprise only needs to complete one integration to launch a savings deposit service, applicable entities include digital banks, crypto wallets, and payroll service providers. Funds deposited by users ultimately flow into the Aave lending market. Users only need to view returns within their daily-used App and can directly participate if they find it worthwhile.

The core feature of the vault: fixed returns, which is quite rare in the crypto industry. The returns of the underlying Aave lending pool fluctuate in real-time with market borrower demand. Stable Vaults essentially add a buffer layer on top, giving operators the authority to adjust interest rates: operators customize the externally displayed rate, for example, setting it at 4%. Thereafter, regardless of how the underlying Aave market rate fluctuates, the vault will consistently pay users a 4% annualized yield. The profit and loss risk from interest rate fluctuations is entirely borne by the operator. The portion of the underlying return exceeding 4% belongs entirely to the operator.

Depositor Perspective

Users essentially obtain a 'return guarantee'. When the Aave USDC pool rate dropped to 2% this spring, vaults promising a 4% annualized yield still paid in full, with the operator making up the rate shortfall.

In financial markets, transferring risk always requires a price, and it's no different here. It can be likened to a fixed-rate mortgage: compared to floating rates, fixed rates are usually 50 to 100 basis points higher. This premium is the cost the borrower pays for yield certainty.

Using the vault, users don't need to create their own crypto wallets, store seed phrases, operate cross-chain transfers, or select public chains; the platform will provide customer service, account recovery, and face ID login services. If assets have issues, there is a real entity company responsible for handling it. The official Aave app has SOC 2 security certification, supports two-factor authentication — these are services ordinary users are truly willing to pay for.

But users also pay a corresponding price: there is a ceiling on returns. When the underlying pool yield rises to 9% or 6%, users still only receive the operator-set 4%. Operators will set differentiated fixed rates based on user membership tiers. Floating rates allow users to directly see the market's real returns, while fixed rates completely obscure the spreads earned by intermediaries.

Simultaneously, users add a layer of counterparty risk: this model overlays two new types of risks to fund safety. One is the operational condition of the financial enterprise itself, and the other is vulnerabilities in the private script code that manages fund allocation. Natively depositing directly into Aave, users only bear the underlying protocol code risk; but using the vault, even if the Aave protocol itself has no vulnerabilities, if the operating enterprise goes bankrupt or the backend script fails causing fund transfer loss, user assets can still suffer.

In the traditional interest rate swap market, sufficient price comparison between supply and demand sides pushes fixed rates back to reasonable ranges. But under the Stable Vaults model, the rate is entirely set unilaterally by the operator, and users lack channels for horizontal comparison. Users won't compare the 4% with the Aave underlying 6% real return; they will only benchmark against traditional bank deposits: the Aave official page will display its rate alongside the FDIC-reported national average savings rate of 0.4%. In that juxtaposition, the vault yield looks very attractive.

Source: aave.com

Operator Perspective

For example: a digital bank holds $200 million in user idle stablecoins, with user acquisition costs already sunk. It only needs to complete one technical integration to launch Stable Vaults, advertising a 4% fixed annualized yield. If the underlying Aave pool yield is 6%, just by earning the 2% spread, it can generate an additional $4 million in annual profit. This previously idle capital that only incurred holding costs now becomes a low-input, stable revenue source.

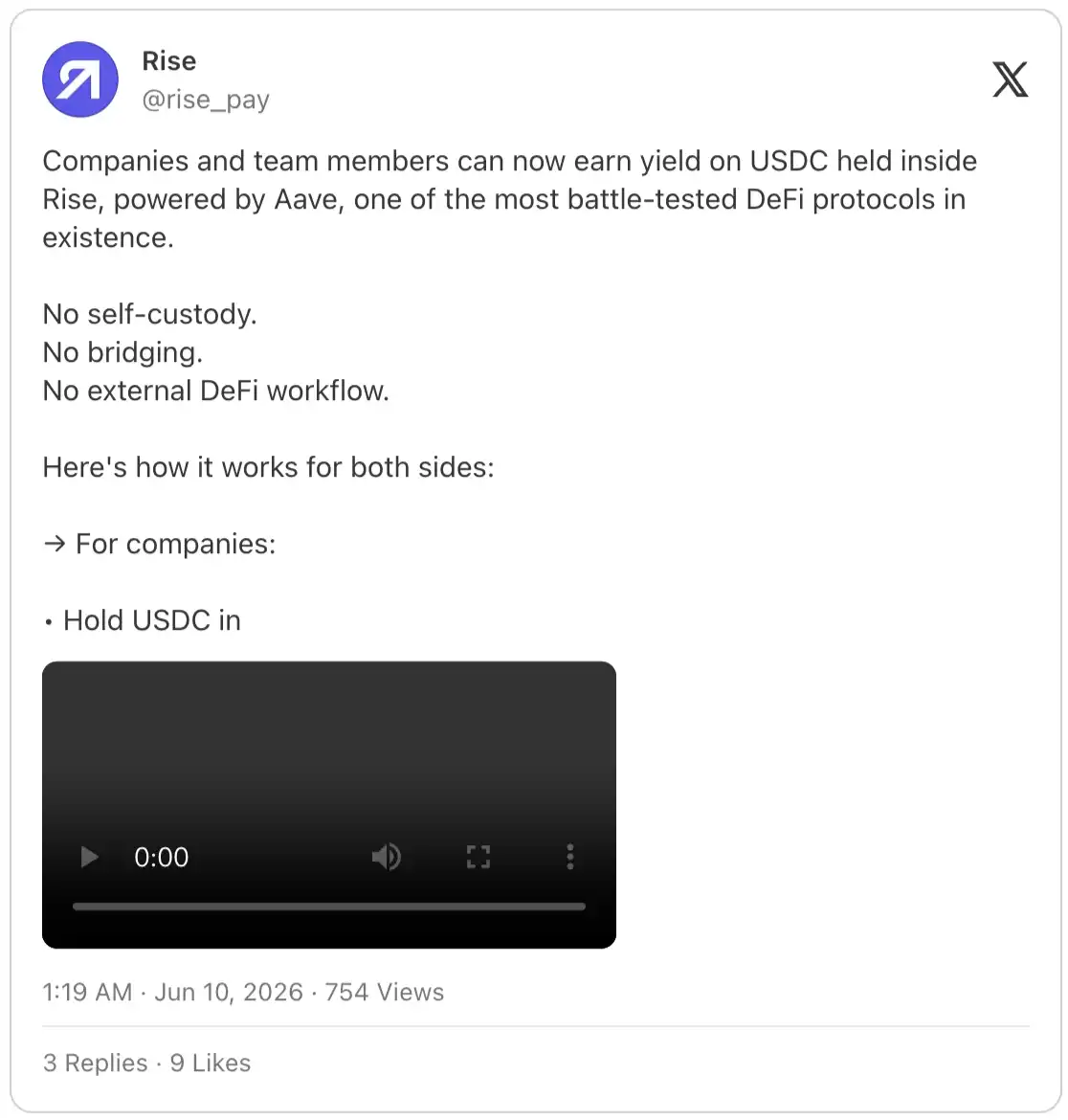

The payroll settlement service provider Rise is a typical case: the platform pays salaries for contractors in 190 countries, having processed over $1.5 billion in total funds. Companies typically pre-fund salaries in USDC a week in advance. These funds were previously idle throughout, so Rise launched its own wealth management feature, Rise Earn, temporarily depositing pre-funded salaries into the USDC pool on Arbitrum chain Aave until payday.

Rise only charges 1% of the total yield as a service fee, with no other deductions. From the underlying 6% annualized yield, the service provider only takes 6 basis points, leaving contractors with 5.94%, and the underlying real-time floating rate from Aave is displayed throughout.

Operating the same scale of funds through Stable Vaults, the operator could earn a 200 basis point spread, a 33-fold difference in revenue share.

Aave and Stable Vaults Perspective

Aave profits by selling the vault's layered interest rate functionality: operators can set differentiated returns for membership tiers and marketing campaigns — premium members 5% APY, regular users 3.5% — all sourced from the same underlying lending pool yield. Fintech companies issuing their own stablecoins can also register them as vault deposit assets, building a closed-loop capital flow system. Stable returns improve user capital retention rates, and continuously deposited assets themselves are a core tool for platform user retention.

Operators do not earn the spread out of thin air; they bear the profit and loss from interest rate fluctuations in both directions. When the underlying pool yield dropped to 2% this spring, all vault operators promising fixed rates above 2% had to dig into their own pockets to make up the difference.

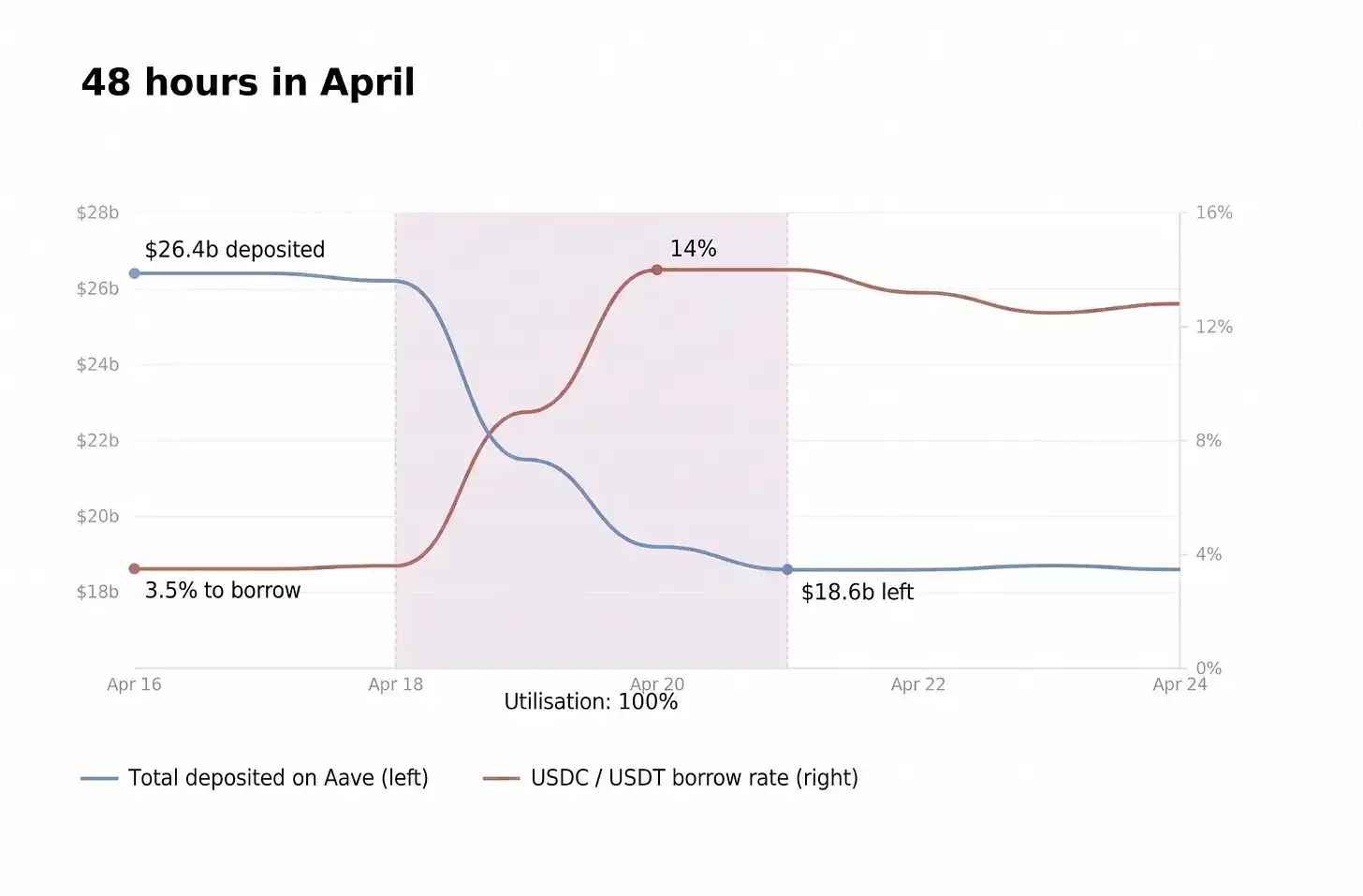

An event on April 18th this year fully exposed the potential risks of this model: the Kelp DAO cross-chain bridge was hacked, triggering a massive market run on the Aave pool. The pool's utilization rate instantly hit 100%, freezing all withdrawal operations. Operator paper profits and user principal were both stuck in the withdrawal queue.

When capital utilization hits the ceiling, vaults, like ordinary users, cannot withdraw any funds. Underlying yield surpluses can only remain on paper, tied up with user principal.

If market liquidity later recovers, operators can settle the paper surpluses accumulated during the freeze from the run. This surplus is essentially the premium the market pays for liquidity scarcity, and the ones bearing the cost of the liquidity freeze are always the depositors. If liquidity does not recover long-term and the pool develops bad debt, vaults will face yield shortfalls; Aave documentation only states authorized entities can cover system shortfalls but does not establish a corresponding reserve fund safety net mechanism.

Aave would argue externally that the protocol contracts have never been hacked, the vulnerability was in the Kelp bridge not its own code, and it froze the risky collateral asset rsETH within hours — these statements are true. But before that, the community voted to accept this high-risk collateral asset with a dangerously high loan-to-value ratio of 93%, then the risk lead resigned directly, ultimately leaving ordinary users to bear the full loss from the system failure.

Stable Vaults seem to complete the final piece in Aave's mass commercialization puzzle.

Payroll service provider Rise connects idle salary funds to Aave; crypto exchange Kraken, based on Aave V3, launched a customized protocol Tydro on its own Layer 2 network, with all its retail wealth management features connected to this protocol — Kraken's wealth management users are essentially indirect Aave users; Cap Finance also deposits stablecoin reserves into Aave pools.

The Horizon platform collaborates with Circle and Franklin Templeton, supporting tokenized treasury bond collateralized lending; the official Aave app directly targets C-end retail users; Stable Vaults opens integration channels to the entire industry, packaged externally as an asset diversification solution.

Aave actually doesn't lack deposits. Kulechov (Stani Kulechov, Aave founder and CEO) said in a March interview with The Block that the current DeFi market suffers from overall excess liquidity, and the industry focus must shift to the borrowing demand side. This is also the core reason why the underlying USDC yield has long remained at 2%-3%, never returning to the previous 8% highs. For a long time, DeFi capital has been extremely yield-chasing; a mere 50 basis point yield difference triggers large-scale capital outflows. By funneling through relationship-holding applications like payroll platforms and wallets, originally highly unstable crypto liquidity can transform into stable, deposit-like funds akin to traditional bank deposits.

The Aave Economic Model 3.0 mechanism, officially launched on June 27th, will use protocol revenue to automatically buy back and burn AAVE tokens. Regardless of market bull or bear, the platform needs stable revenue to sustain buybacks; in a bear market, sticky deposit funds with high retention attributes are key to ensuring continuous buyback fund flow, and Stable Vaults are precisely the tool to acquire such sticky capital.

Coinbase platform USDC wealth management yields around 4% APY; Robinhood launched its wealth management feature on July 1st, with yields close to 7% APY, with the platform having 2.8 million funded accounts. Both platforms call their wealth management products savings accounts.

Coinbase's backend connects to Morpho and Ethena protocols; Robinhood relies on Morpho and Maple to build its wealth management system, with risk parameters set by third-party firm Steakhouse.

Both platforms invested heavily in building the entire wealth management system, including custody partnerships, asset selection, risk management teams, and months of legal processes. The core value of Aave Stable Vaults is removing all this self-build cost: any application only needs one integration to display a fixed yield number to users. The profit and loss from the spread between the underlying Aave pool yield and the front-end displayed fixed rate is entirely handled by the integrating party.

Traditional banks can legally operate savings and lending businesses, backed by a century of perfected legal systems: reserve requirements, regular on-site inspections, deposit insurance, regulators can make unannounced visits. This regulatory system was born from a societal consensus: banks lend depositor funds, so there must be robust mechanisms to handle loan default risks.

All wealth management functions Stable Vaults can provide can be achieved by ordinary users themselves in just 20-30 minutes: create a crypto wallet, transfer in USDC stablecoins, then deposit into the native Aave pool. Self-operation requires no KYC verification, intermediary operator, or backend rebalancing scripts, nor does it incur yield spread extraction. The full underlying 6% yield is received, and all pool data can be viewed in real-time.

I understand the platform's considerations are far more long-term than ordinary users' short-term gains and losses, and I also never think people choosing vault products lack judgment.

Research by Iyengar and Huberman on retirement planning shows that the more fund options available, the lower the proportion of users actively participating in wealth management; faced with a sea of choices, most people simply give up on planning. Since then, all consumer finance products targeting the masses have followed this research conclusion in their design logic.

Over the past fifteen years, the industry has repeatedly preached the security of self-custody crypto wallets, but the market's real choice is截然相反: the vast majority of on-chain card spending funds still go through custodial platform channels. This is the real preference validated over time by massive user bases. The security logic of custodial platforms fits ordinary people better. For novices with only $2,000 in assets and no crypto knowledge, the two highest-incidence scenarios for asset loss are losing seed phrases and entering wrong transfer addresses; custodial Apps with Face ID and account recovery features directly eliminate such human operational risks. Users paying a 200 basis point spread are essentially buying insurance against their own operational errors — a completely rational consumption decision.

Therefore, Aave launching Stable Vaults is a commercially logical and correct strategic move. For DeFi protocols sitting on massive liquidity but lacking user loyalty, it's an inevitable choice; all crypto applications targeting ordinary consumers are iterating in the same direction, because the underlying human logic is omnipresent.

Ultimately, this product is an acceptance of human nature: ordinary people seek asset safety, predictable returns, and most importantly, simple, hassle-free operation. Managing personal assets already consumes significant energy; no one wants to personally operate a private central bank-like wealth management system. Users just want to close the App and see their account yield number remain stable and unchanged.