Автор: Yuanchuan Investment Review

Когда общение в инвестиционной группе становится всё реже, достаточно бросить график кривой чистой стоимости У Юэфэна, и атмосфера мгновенно оживляется.

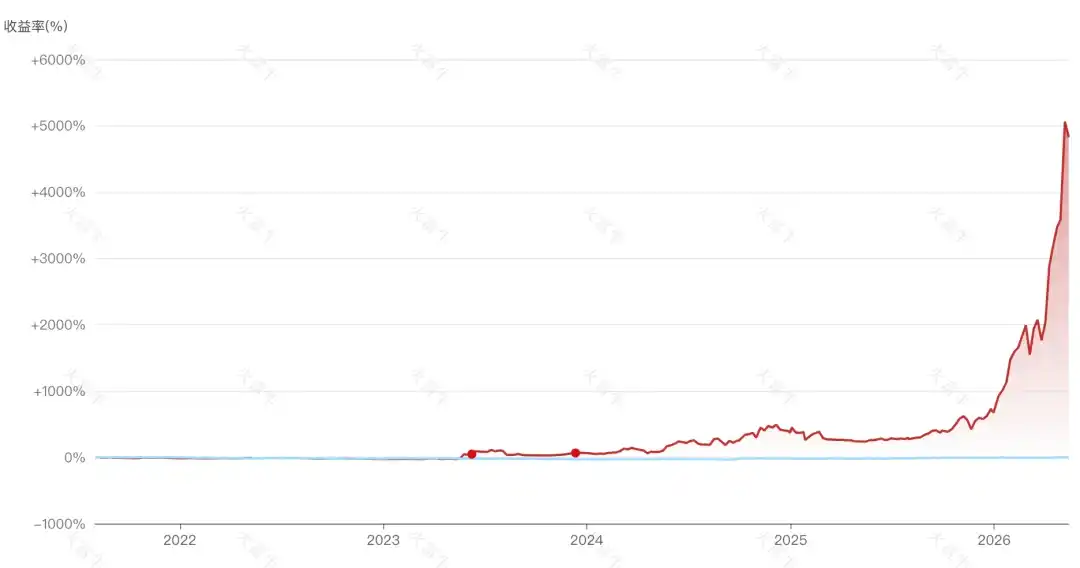

На этот раз чистая стоимость инвестиционного фонда Jia Yue Yuefeng Chuangshi не только вернулась к уровню воды, но и достигла нового исторического максимума. В прошлом году У Юэфэн поднял чистую стоимость с 30 с лишним центов обратно выше уровня воды, думая, что выбрался из бездны, однако вскоре она снова упала до 50 с лишним центов. И только к 8 мая этого года, чистая стоимость выросла почти на 167,54% за месяц, У Юэфэн снова в деле.

Судя по отчету о составе портфеля, общая доля акций доведена до 100%, 35% инфраструктуры AI-вычислений + 20% чипов памяти стали основной движущей силой резкого роста чистой стоимости. Модули A/H-акций оптических модулей и печатных плат составляют 5%, У Юэфэн почти полностью сделал ставку на цепочку поставок AI-вычислений[1].

За последний год достаточно было лишь немного изменить мышление и переключиться на рост оптической связи и памяти, вместо того чтобы обороняться с помощью спиртных напитков, и независимо от того, насколько плохо шли дела раньше, какой бы большой ни была яма, одним махом можно было всё вернуть. Стоять в свете, быть близко к сердцевине («синь») — вот был главный код доступа к богатству в этом году.

Юаньлэшэн, Сива, Цюши — эти субъективные фонды с капиталом в десятки миллиардов юаней, бесконечно блиставшие в 2020-2021 годах, показали резкий рост чистой стоимости своих флагманских продуктов за последний год, превысив исторические максимумы. Фу Лаоши из Ruiyuan за последний год тихонько удвоил стоимость, установив новый исторический максимум. А частный инвестиционный фонд под названием Zhunjin Zhizhan No.1 был ещё более невероятным: с начала этого года его стоимость выросла в 5 раз, а за менее чем 5 лет существования — в 50 раз.

Что такое «громовая» чистая стоимость

Ещё ходят слухи о частном фонде Яо Цзинхэ, который заработал астрономические суммы на памяти и CPO, о бывшем сотруднике OpenAI Леопольде, который за год увеличил размер хедж-фонда с 225 миллионов долларов до 5,5 миллиардов, а также о государственных активах Хэфэя, которые вновь получат титул «лучшего венчурного инвестора» в связи с предстоящим листингом Changxin. Кажется, повсюду есть люди, считающие деньги, стоя на «синь», «гуан» (свет/оптика) и «ли» (литий), а у тех, у кого их нет, остаётся только смотреть на непрерывный рост, наблюдать за различными «громовыми» показателями чистой стоимости и беспокоиться до повреждения префронтальной коры.

Людям, находящимся сейчас в акциях технологического сектора Хэншэна (Hang Seng Tech) и стоимостных акциях, в душе невольно возникает вопрос: даже шанхайские KTV-хостесс заработали 18 миллионов юаней, почему рынок ещё не переключился с высокого на низкое?

Кремниевый бык, углеродный медведь

В нынешнем рыночном цикле есть парадоксальный момент: даже при самой высокой переполненности AI-цепочка поставок не падает.

В первом квартале этого года доля AI-аппаратного обеспечения в портфелях активно управляемых фондов, ориентированных на акции, составила 31,5%, с избыточной долей в 17,7%. По сравнению с историческими основными секторами, хотя она и не превысила пик индекса «Маотай» (Mao Index) того времени, но уже превысила пик индекса «Нин» (Ning Index)[2].

Лю Чэньмин из GF также отметил, что в прошлом году доля TMT в портфелях фондов уже превысила 40%, доля электроники непрерывно превышала 20% более года. С точки зрения торговой переполненности, доля торгового оборота TMT в A-акциях уже давно пробила порог в 40% предыдущего отраслевого цикла.

Несмотря на такую переполненность, с апреля индекс Philadelphia Semiconductor вырос на 54%, индекс чипов STAR вырос на 60%. Не говоря уже о Фу Лаоши, который в первом квартале крупно вошёл в Zhongji Innolight, даже 18 фондов смешанных инвестиций с долей полупроводников более 10% выдали серию «громовых» показателей чистой стоимости.

Другой парадоксальный момент нынешнего рыночного цикла заключается в том, что даже при сильном падении Hengke его невозможно поднять.

Прошло два месяца с тех пор, как Ся Цзюньцзе сказал, что «Hengke, возможно, перепродан», но он по-прежнему не подаёт признаков жизни, словно мёртвая рыба, неподвижно лежащая на льду в морепродуктовой закусочной с широко открытыми глазами.

У слабости Hengke есть свои неизбежные причины, как объяснил Лю Сяолун из Juming в ответ на вопрос, почему он очистил портфель от акций технологического сектора Гонконга: 1) Потенциальное влияние AI на бизнес-модели интернет-компаний; 2) Гонконгский рынок в большей степени подвержен влиянию ужесточения зарубежной ликвидности; 3) Большой объём IPO в 25 году, поглощающий капитал.

В конечном счёте, текущая структура больших моделей всё ещё представляет собой ситуацию «победитель получает всё» и конкуренции с длинным хвостом однородных игроков. Hongshang Asset считает, что стратегия «бесплатно» и «дёшево» в потребительском сегменте (C-end) приводит к дилемме оценки китайских AI-компаний:

Когда способность к монетизации подвергается сомнению, даже AI-направления Tencent и Alibaba с трудом получают признание на рынке капитала. Хотя такие модели, как Alibaba's Qianwen, начинают пробовать модели с закрытым исходным кодом и платным доступом, результаты не очень хорошие. Это также является основной причиной того, почему рынок в последнее время постепенно теряет терпение к AI-историям Tencent и Alibaba, и их потенциал для расширения мультипликаторов оценки недостаточен.

Самым парадоксальным в нынешнем рыночном цикле является то, что менеджеры фондов потребительского сектора начали переквалифицироваться и преследовать «свет» (оптику).

Недавно, желая инвестировать в фонд потребительского сектора, я подумал, что название «Bosera Female Consumption Theme» очень подходит по вкусу. Открыв список десяти крупнейших холдингов, я увидел Crystal-Optech и Zhongji Innolight, которые буквально бросились в глаза.

Известные «старые мастера» потребительского сектора Тун Сюнь и Сяо Нань также постепенно растворяются в «свете» (следуют тренду). После изменения мышления кривая чистой стоимости Тун Сюнь Лаоши с апреля пошла по V-образной траектории; после третьего квартала прошлого года «содержание света» в управляемом Сяо Нанем фонде Yifangda Ruiheng постепенно увеличивалось, и по мере этого разрыв в результатах с его коллегой Чжан Кунем, погрязшим в проблемах со спиртными напитками, становился всё больше.

Эти странные явления напоминают пик предыдущего цикла субъективных лонгов в 2020-2021 годах.

Только тогда главными героями были менеджеры фондов поколения 60-х, обладавшие мышечной памятью о «монопольных барьерах + вечном бизнесе», которые по сравнению с рынком имели избыточный вес в акциях Kweichow Moutai и Alibaba; а в этом цикле главные роли перешли к поколению 85-х, обладающим предельной верой в жёсткие технологии, которые по сравнению с рынком имеют избыточный вес в акциях Zhongji Innolight и Cambricon, большинство из которых впервые в своей карьере управляющих столкнулись с уровнем в 4200 пунктов.

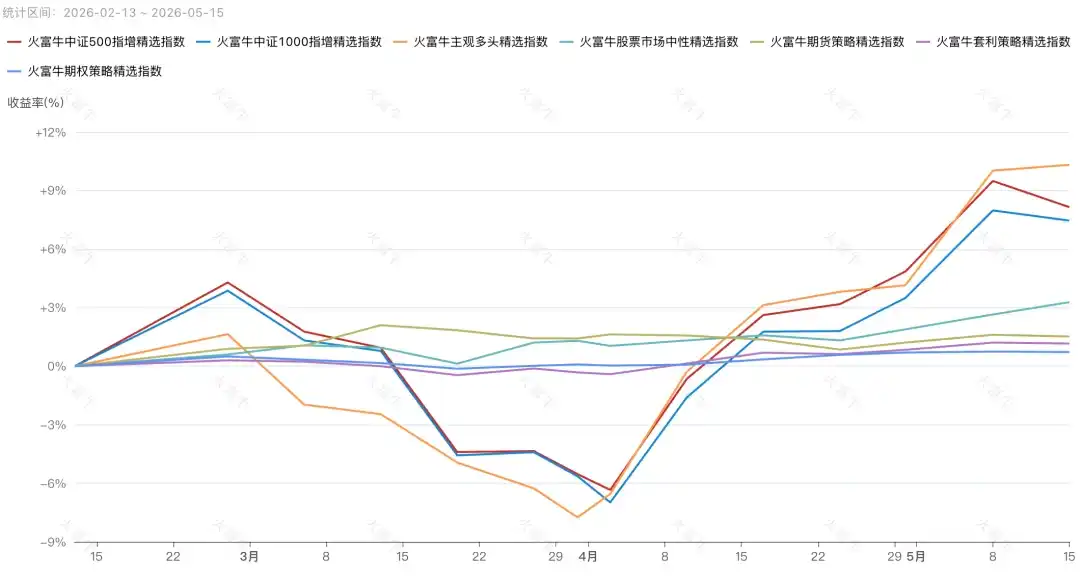

Если бы не AI, субъективные лонги, годами подавляемые количественными стратегиями, уже давно бы не почувствовали такого удовлетворения. За последний год у публичных фондов было 12 субъективных лонг-продуктов с доходностью более 300%; за последние 3 месяца индекс отобранных субъективных лонг-фондов Huofuniu обогнал индекс отобранных стратегий усиления CSI 500, став самым сильным индексом стратегий.

Жэнь Цзэпин говорит, что это бычий рынок, случающийся раз в десять лет, бык уверенности, наложенный на политического быка + технологического быка + денежного быка. Я считаю, что более точное выражение: для тех, кто верит в кремний, это бычий рынок; для тех, кто идёт покупать углерод на дне, это медвежий рынок.

Атаковать или защищаться

Для многих менеджеров фондов нынешняя ситуация похожа на положение Флика с этой бедной «Барселоной» — кажется, другого выбора нет.

Тактика Флика — атаковать вместо защиты, высокий прессинг, удерживание мяча на половине противника, чтобы снизить вероятность прямого выхода противника на свои ворота. Если отступить и засесть в обороне, полагаясь на эту слабую защитную линию «Барсы», можно только проиграть ещё хуже. По той же логике, даже защищаясь в Hengke и потребительском секторе, когда бычий рынок закончится, они всё равно упадут, но по крайней мере, покупая AI в атаке, можно накопить прибыльную подушку.

Тем более, что в условиях экстремальных эмоций FOMO (страх упустить выгоду) управлять настроениями на стороне обязательств становится всё труднее. В конце концов, клиенты сами могут зарабатывать, просто покупая акции и следуя за «светом», и, видя, как друзья покупают субъективные фонды с «громовой» чистой стоимостью, зачем тратить время и платить комиссию за управление, слушая твои разговоры о стоимостном инвестировании, и при этом упускать несколько поездов эпохи, которые выпадают в жизни?

Раз это быстрый поезд эпохи, несущийся вперёд, стоит ли тем, кто не успел на него, догонять? Стоит ли тем, кто уже в поезде, выходить? Это вопрос, с которым должны прямо столкнуться все управляющие. Как и то, что капитальные расходы пяти технологических гигантов США постоянно корректируются в сторону повышения до 720 миллиардов долларов, никто не хочет остаться позади времени.

Ван Чжунъюань, основатель инвестиционной компании Ziruixing, вошедший в отрасль в 1993 году, пережил событие с казначейскими облигациями "327" в 1995 году и был свидетелем пузыря доткомов в 1999 году. Он рассказал Yuanchuan реальную историю:

Стэнли Дракенмиллер в первой половине 1999 года играл на понижение технологических акций, к концу года вернулся в них с большой долей, а в январе 2000 года закрыл позиции, уйдя с вершины. Но к марту 2000 года технологии снова рванули вверх, он не выдержал и бросился в них со всем капиталом, в результате за полтора месяца потерял 18%.

«Что показывает эта история? Даже признанный во всём мире лучший трейдер, столкнувшись с эмоциями FOMO, может принять нерациональное решение. Как вы думаете, сколько из сегодняшних менеджеров фондов, преследующих „свет“, сильнее Дракенмиллера?»

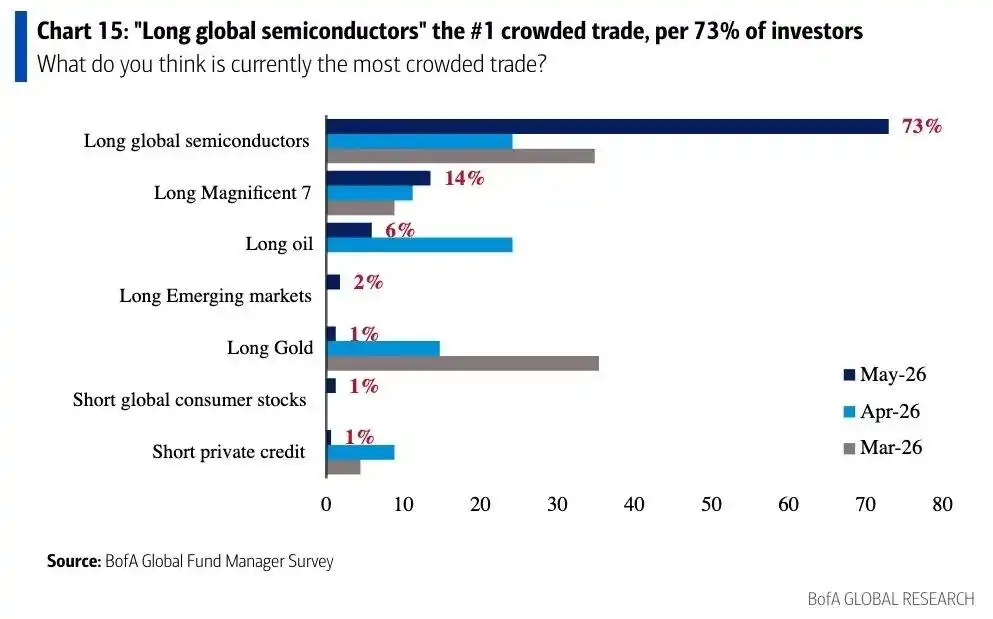

Интересно, что Zeyuan Investment опубликовали в WeChat статью с графиком — «Полупроводники заняли первое место в мировом рейтинге торговли за май».

Они рекомендуют инвесторам снизить ожидания от Zeyuan. Текущая ситуация аналогична пику пузыря доткомов, они ни за что не станут менять свои взгляды, отказываясь от традиционного стоимостного инвестирования, чтобы гнаться за пузырём доткомов, и даже если пузырь доткомов закипит ещё сильнее, они «ни за что не сдадутся». Они процитировали фразу: «Фондовый рынок — это место обмена мечтами и денег, те, кто продаёт мечты, получают деньги, а те, кто платит деньги, чаще всего оказываются в ловушке на рынке, охраняя мечты».

По сравнению с Ziruixing и Zeyuan, Jingyi Investment выразилась более прямо — базовые большие модели этой AI-революции, а также самая ключевая инфраструктура и аппаратное обеспечение, в подавляющем большинстве находятся в руках тех американских технологических гигантов, что за большим океаном. Нынешние спекуляции на AI на рынке A-акций имеют гораздо менее прочную фундаментальную поддержку, чем новая энергетика в своё время.

«В 2021 году большинство компаний в солнечной энергетике и литиевых батареях сопровождались реальным взрывным ростом прибыли и быстрым повышением уровня проникновения, а многие так называемые „AI-компании“ на рынке A-акций, сегодня раздутые до рыночной капитализации в сотни миллиардов, даже не имеют того мимолётного всплеска прибыли, что был у новой энергетики».

Нельзя отрицать, что некоторые субъективные частные фонды не играют в азартные игры. Они выдержали удар по коротким позициям от платной статьи Майкла Бёрри в 379 долларов в прошлом году и уловили, что главной линией инвестиций в AI является AI-аппаратное обеспечение. Но по мере того, как спекуляции распространяются с оптических модулей на память, CPU, электронные ткани, оптическое волокно и другие узкие сегменты, пространство для внутреннего переключения с высокого на низкое внутри сектора постоянно сужается, а потенциальная цена ошибки возрастает.

Плюс к этому, 30-летние казначейские облигации США пробили уровень 5%, и покупка AI на росте сейчас происходит в иной макроэкономической ситуации, чем в прошлом году, когда Майкл Бёрри кричал о пузыре.

Это похоже на «Барселону» Флика, которая в этом сезоне шла гладко, время от времени выдавая «громовые» результаты. Но пока в четвертьфинале Лиги чемпионов они не встретили «Атлетико», сильного в контратаках. По-прежнему упорствуя в высокой атаке, они заставили защитников часто отбегать назад и получить две красные карточки, что полностью похоронило матч.

Заключение

Когда люди ещё верили в углерод, «громовая» чистая стоимость тоже появлялась.

В предыдущем бычьем рынке спиртных напитков с 2020 года по июнь 2021 года результаты Линь Юаня выросли на 150%, после чего в течение пяти лет они колебались и падали, и сейчас осталась лишь доходность чуть более 20%. А Zheng Yuan и Chongji, которые в своё время концентрированно делали ставку на солнечную энергетику и новую энергетику, и вовсе стали воспоминаниями, о которых финансовые консультанты не любят вспоминать.

Также, например, Shifeng Asset, которая ранее показывала «громовую» чистую стоимость и на пике имела активы под управлением в 30 миллиардов юаней, пыталась трансформироваться в количественные стратегии, но так и не смогла переломить тенденцию к снижению. Сейчас активы под управлением сократились до 2-5 миллиардов юаней, и недавно стало известно, что они переехали из офиса в Shanghai Lujiazui Century Financial Plaza в более дешёвое по аренде здание Yuanshen Finance Tower.

Всё это, возможно, кажется несколько отдалённым, но в начале года, когда цена золота достигла максимума, тот частный фонд золота, который трижды выкрикивал «сядьте поудобнее и держитесь», вряд ли так легко забудется.

Иногда я спрашиваю у сотрудников каналов сбыта, почему они рекомендуют тот или иной частный фонд, и получаю ответ, не выходящий за рамки трёх пунктов: уволился из крупной компании, чтобы основать свой бизнес; активы под управлением ещё небольшие, стратегия всё ещё работает; и самое главное — кривая чистой стоимости выглядит красиво.

За «громовой» чистой стоимостью часто стоит увеличенная доходность, вызванная концентрированными позициями и даже использованием кредитного плеча. Покупка, основанная исключительно на остроте исторических результатов, с большой вероятностью приведёт к приобретению посредственного продукта, к покупке не более чем сильного рыночного тренда прошлого. Урок покупки на падении по графику история повторяла раз за разом.

У Динвэнь из Qinyuan как-то поделился: «При распределении активов нужно признавать базовую логику, то есть признавать торговлю, признавать стоимость, признавать команду, а не признавать зарабатывание денег». Признавая только зарабатывание денег, вы, скорее всего, не сможете вырваться из цикла: покупать то, что сейчас в моде, покупать — и оно падает, умирать там, где оно падает.