Автор: Клод, Deep Chao TechFlow

Резюме Deep Chao: ETF на полупроводники (SOXX) с начала года взлетел на 78.5%, в то время как ETF на программное обеспечение (IGV) за тот же период упал на 12.5%. Разрыв в доходности между ними превысил 90 процентных пунктов, достигнув исторического экстремума.

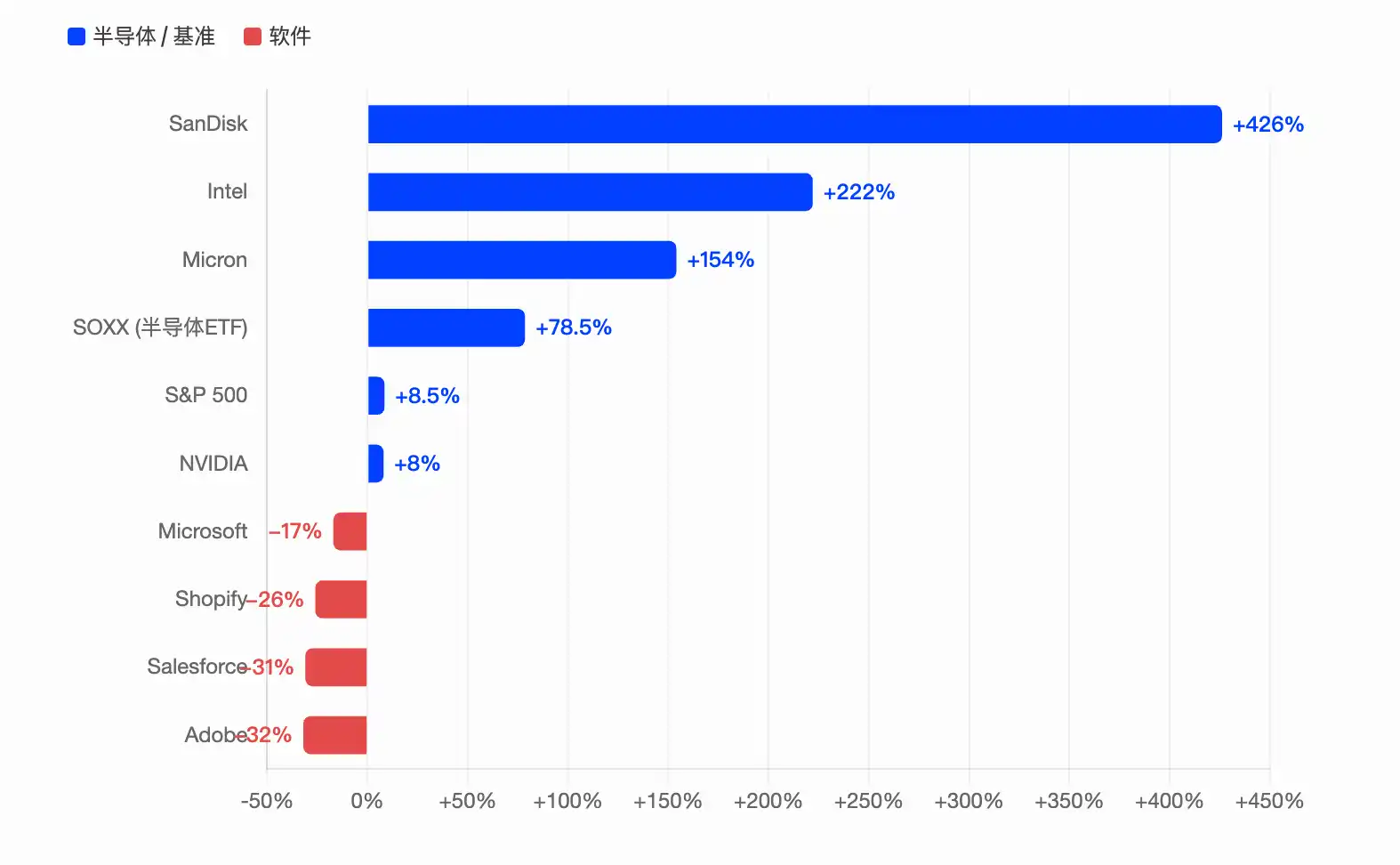

SanDisk с годовым ростом в 426% лидирует в индексе S&P 500, Intel утроился, Micron вырос на 154%. В то же время Microsoft, Adobe и Salesforce потеряли с начала года более 17%. Совокупные капитальные расходы четырех крупнейших инфраструктурных компаний в 2026 году приближаются к 7000 миллиардам долларов. Деньги, словно в черную дыру, вливаются в цепочку поставок чипов, в то время как сектор программного обеспечения сталкивается с двойным ударом от нарратива о замещении ИИ и оттока капитала.

Недавно на инвестиционном сабреддите Reddit набрал популярность пост о том, что акции полупроводниковых компаний — это «по сути черная дыра, которая засасывает всё остальное», что нашло широкий отклик.

Данные подтверждают это наблюдение. По состоянию на закрытие торгов 22 мая, доходность ETF iShares Semiconductor ETF (SOXX), отслеживающего сектор полупроводников, с начала года составила 78.5%, в то время как доходность ETF iShares Expanded Tech-Software ETF (IGV), отслеживающего сектор ПО, за тот же период составила -12.5%. Разрыв в доходности между двумя ETF, относящимися к широкому технологическому сектору, превысил 90 процентных пунктов.

По данным Tickeron, все акции программного обеспечения из индекса S&P 500 в настоящее время торгуются ниже 200-дневной скользящей средней, в то время как около 89% акций полупроводниковых компаний остаются выше этой отметки. Оба сектора синхронно падали до нулевой отметки во время медвежьего рынка 2022 года, после чего их траектории полностью разошлись. Это разделение не было постепенным, а носило взрывной характер.

SanDisk с ростом 426% лидирует в S&P 500, Intel с трехкратным ростом давит AMD

На уровне отдельных акций цифры еще более впечатляющие.

Согласно данным Benzinga Pro, SanDisk (SNDK) с начала года вырос примерно на 426%, став лучшей акцией S&P 500 в 2026 году, после уже ошеломляющего роста на 559% в 2025 году. У этой компании по производству чипов памяти, выделившейся из Western Digital, цена на флэш-память NAND под влиянием ИИ выросла более чем на 200% в годовом исчислении, выручка за квартал, завершившийся в марте, выросла на 250% до 5.95 миллиарда долларов, а маржинальность по не-GAAP составила 78.4%.

По сообщению 24/7 Wall Street, Intel (INTC) с начала года вырос примерно на 222% до 225 долларов, что в два раза превышает рост AMD. Отскок Intel произошел с очень низкой базы, усиленный прогрессом в техпроцессе 18A, слухами о заказах на производство для Apple и данными об улучшении выхода годных продуктов, озвученными CEO Патриком Гелсингером в интервью CNBC. Медведи были жестоко наказаны: по данным S3 Partners, с минимума 30 марта рыночная капитализация Intel выросла более чем на 440 миллиардов долларов, а убытки коротких продавцов превысили 12 миллиардов долларов.

Micron (MU) с начала года вырос примерно на 154%, а совокупный рост за последние 12 месяцев составил 661%. Финансовые результаты также подтверждают этот тренд: выручка за второй квартал 2026 финансового года составила 23.9 миллиарда долларов, что на 196% больше, чем годом ранее, скорректированная прибыль на акцию — 12.20 доллара, что значительно превышает рыночные ожидания в 9.21 доллара. DRAM составляет 79% от общего дохода, причем память с высокой пропускной способностью (HBM) является ключевым драйвером. Председатель SK Hynix Чхве Тхэ Вон даже прогнозирует, что дефицит чипов памяти может сохраниться до 2030 года.

Для сравнения, NVIDIA (NVDA), настоящая «денежная машина» ИИ-вычислений, с начала года выросла примерно на 8-15%, что значительно уступает динамике вышеупомянутых полупроводниковых компаний второго эшелона. По данным The Motley Fool, текущее форвардное P/E NVIDIA составляет около 21.5, что почти равно показателю S&P 500 (20.3). Это означает, что рынок больше не платит премию за рост NVIDIA, а средства перетекают в чипмейкеров с более низкой оценкой и большим потенциалом роста.

Капекс в 7000 миллиардов долларов: «гонка вооружений» гипермасштабных инфраструктурных компаний

За резким ростом полупроводников стоят реальные деньги.

Согласно данным Financial Times и сводкам ряда аналитических агентств, совокупные капитальные расходы четырех крупнейших инфраструктурных компаний — Microsoft, Alphabet (материнская компания Google), Amazon и Meta — в 2026 году, по прогнозам, составят от 6500 до 7250 миллиардов долларов, что почти вдвое больше, чем примерно 4100 миллиардов долларов в 2025 году. Это крупнейший в истории технологий цикл концентрированных инвестиций в инфраструктуру.

По сообщению Tom's Hardware, аналитик Jefferies Брент Тилл заявил прямо: «Экономика ИИ здорова. Медвежьи нарративы — это мусор».

Конкретно по компаниям: Amazon лидирует с квартальными капитальными расходами в 44.2 миллиарда долларов, рост AWS составил 28%; капитальные расходы Alphabet в первом квартале составили 35.67 миллиарда долларов, что вдвое больше, чем год назад, а объем неисполненных заказов Google Cloud вырос до более чем 460 миллиардов долларов; капитальные расходы Microsoft в 2026 календарном году достигнут 190 миллиардов долларов, из которых около 25 миллиардов долларов связаны с ростом цен на чипы памяти и компоненты; Meta повысила прогноз по годовым капитальным расходам до 125–145 миллиардов долларов.

Согласно статистике в блоге Ома Малика, три гипермасштабные компании отразили в отчетности за первый квартал крупные неденежные доходы от инвестиций: Alphabet — 36.8 миллиарда долларов (в основном от переоценки доли в Anthropic), Amazon — 16.8 миллиарда долларов, Microsoft — 5.9 миллиарда долларов (от OpenAI). Хотя капитальные расходы и требуют огромных средств, сами объекты инвестиций в ИИ также постоянно растут в цене.

Акции софта под двойным ударом нарратива о замещении ИИ, IGV показывает худшее падение с 2008 года

Обратная сторона медали — жестокий обвал акций софтверных компаний.

По данным The Motley Fool, после выпуска Anthropic в начале 2026 года инструмента Claude Code, сектор программного обеспечения пережил резкое падение — логика рынка заключалась не в поощрении инноваций в ИИ, а в наказании тех SaaS-компаний, которые могут быть замещены ИИ. IGV зафиксировал самое сильное падение с 2008 года.

По состоянию на конец мая, Microsoft с начала года упала примерно на 17%, Adobe — на 32%, Salesforce — на 31%, Shopify — на 26%. Индекс программного обеспечения и услуг S&P 500 торгуется примерно на 21% ниже своей 200-дневной скользящей средней — это самое большое отклонение с июня 2022 года. По данным Goldman Sachs и других институтов, короткие позиции по средним и крупным софтверным компаниям резко выросли за последние три месяца, причем компании в сфере кибербезопасности и SaaS подверглись наиболее агрессивному наращиванию коротких позиций.

За этим разделением стоят две логики. Первая — прямой переток ликвидности: ликвидность рынка ограничена, и когда капитальные расходы в 7000 миллиардов долларов толкают акции чипмейкеров по параболической траектории, средства должны откуда-то изыматься. Именно об этом говорил автор того поста в Reddit: «Акции софтверных компаний с хорошими фундаментальными показателями просто лежат на месте или тихо падают, в то время как индекс полупроводников растет практически вертикально».

Вторая — пересмотр нарратива оценки. Быстрая эволюция ИИ-агентов заставляет рынок переосмыслить рентабельность бизнес-модели SaaS: сколько продержится модель подписки с оплатой за место, когда ИИ сможет автоматически выполнять программирование, заполнение форм и обслуживание клиентов? The Motley Fool отмечает, что выживут те софтверные компании, которые обладают реальными данными, проприетарными рабочими процессами и глубокой интеграцией с клиентами — теми характеристиками, которые сложно заменить ИИ.

Вершина цикла или структурные изменения? Два ключевых вопроса остаются без ответа

В конце своего поста тот пользователь Reddit задал два вопроса, которые можно считать главными сомнениями инвесторов относительно того, сможет ли полупроводниковый сектор сохранить свой горячий тренд.

Однако на эти вопросы до сих пор нет ответа.

Первый: Как долго гипермасштабные инфраструктурные компании смогут поддерживать такой уровень капитальных расходов?

Согласно сообщению CNBC, Pivotal Research прогнозирует, что свободный денежный поток Alphabet в 2026 году упадет почти на 90% — с 73.3 миллиарда долларов в 2025 году до 8.2 миллиарда долларов. Из 190 миллиардов долларов годовых капитальных расходов Microsoft около 25 миллиардов съедает рост цен на чипы памяти и компоненты. Эти компании ставят будущую прибыль на ставку в AI-доходах, которые еще не полностью материализовались.

Второй: Не станет ли софт следующим объектом ротации капитала?

Согласно ранее озвученному суждению главного инвестиционного стратега Bank of America Майкла Хартнетта в отчете Flow Show, программное обеспечение является одним из лучших направлений для контрарианской покупки во втором квартале 2026 года, поскольку относительное отклонение сектора от 50- и 200-дневных скользящих средних стало экстремальным.

Однако это не означает, что ралли полупроводников закончилось. Индекс PHLX Semiconductor Sector (SOX) 25 апреля установил исторический рекорд, продемонстрировав рост в течение 18 торговых сессий подряд с приростом около 45% за этот период. По данным Intellectia, некоторые опытные аналитики начали сравнивать текущую динамику с пузырем доткомов 1999-2000 годов, предупреждая о возможной коррекции на 25-30%. Но SOX вырос в 22 из последних 23 торговых сессий, установив 15 внутридневных исторических максимумов, и этот собственный импульс сам по себе является сигналом.

Как сказал тот пользователь Reddit: «Я не хочу кричать о вершине, потому что слишком много раз уже получал по лицу, делая это раньше. Но высокая концентрация доходности в одном секторе начинает отдавать запахом поздней стадии цикла».