Ripple и Stellar оказались в центре новой волны спекуляций в социальных сетях на выходных, после того как в опубликованных письмах из документов Эпштейна, появившихся в открытом доступе, упоминались эти два проекта в контексте инвестиционного спора 2014 года. Бывший технический директор Ripple Дэвид Шварц публично опроверг эту информацию, заявив, что ему неизвестны какие-либо прямые связи между Эпштейном и любой из сетей, и охарактеризовал этот эпизод как еще один пример того, как племенная политика проникает в криптосферу.

Реакция Шварца после упоминания Ripple и Stellar в документах Эпштейна

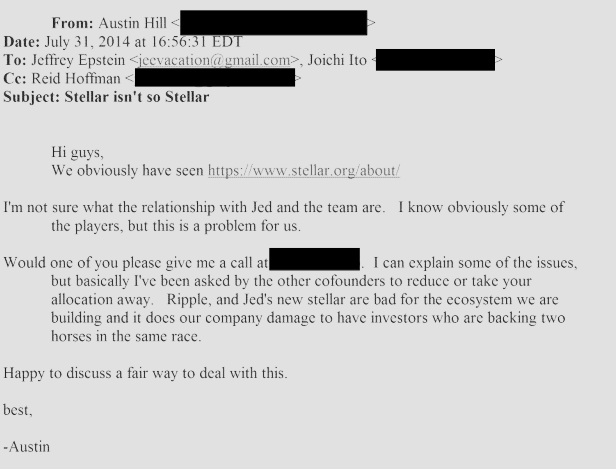

Искрой послужил скриншот, распространявшийся в X, на котором видна цепочка писем, где Остин Хилл (соучредитель Blockstream) жаловался группе влиятельных получателей, включая Эпштейна, на инвесторов, распределяющих капитал между конкурирующими проектами. По словам Шварца, документ «является письмом от Остина Хилла Джеффри Эпштейну, в котором Хилл объясняет, что считал поддержку Ripple или Stellar признаком врага/оппонента», добавив, что Хилл, вероятно, делился подобными взглядами «со многими другими людьми».

По мере распространения изображения некоторые публикации представили mere упоминание Ripple и Stellar в письме как свидетельство более глубокой вовлеченности. Шварц ответил сообщением, в котором попытался отделить провокационные формулировки от того, что документ показывает на самом деле.

«Мне неизвестны какие-либо связи между Джеффри Эпштейном и Ripple, XRP или Stellar. [Мне неизвестны] какие-либо доказательства того, что кто-либо из Ripple или Stellar когда-либо встречался с Эпштейном или кем-то из его ближайшего окружения», — написал он. — «Существуют некоторые косвенные связи между Эпштейном и людьми, так или иначе связанными с Bitcoin, но это, вероятно, верно для большинства очень богатых людей».

Первое сообщение Шварца в ветке отразило настроение дня — и подозрительность, и нежелание подпитывать ее. «Ненавижу быть теоретиком заговора, но я ни капли не удивлюсь, если это лишь верхушка гигантского айсберга», — написал он, разместив ссылку на файл, размещенный на сайте Министерства юстиции США. Позже он заявил, что более разрушительной проблемой является мышление в категориях «враг/оппонент», написав, что «мы действительно все вместе в этом деле, и подобное отношение вредит всем в нашем пространстве».

В исходном письме 2014 года, описанном в материале, Хилл, как portrayed, выступает против того, чтобы бэкеры финансировали несколько «лошадей» одновременно, рассматривая поддержку Ripple или Stellar как враждебную по отношению к ориентированной на биткоин «экосистеме», которую он строил в Blockstream. В отчетах, summarizing цепочку, говорится, что оно было отправлено Джоити Ито, Эпштейну и Рейду Хоффману и содержало формулировки о том, что инвесторы в обоих лагерях «ставят на двух лошадей в одной гонке».

Всплывшее письмо также revived старый разлом в том, как ранние проекты структурировали себя. В ответ на вопрос пользователя о некоммерческом статусе Ripple versus Stellar, Шварц сказал, что эта идея обсуждалась в начале пути и что он был против нее.

«Мы обсуждали это на ранних этапах. Я был категорически против, потому что это казалось нечестным и borderline незаконным — иметь некоммерческую организацию, успех которой так тесно связан с выгодой частных лиц», — написал он. — «Это ощущалось, по крайней мере для меня, как если бы Walmart создал некоммерческую организацию, чтобы обучать людей тому, сколько денег они могут сэкономить, покупая в Walmart».

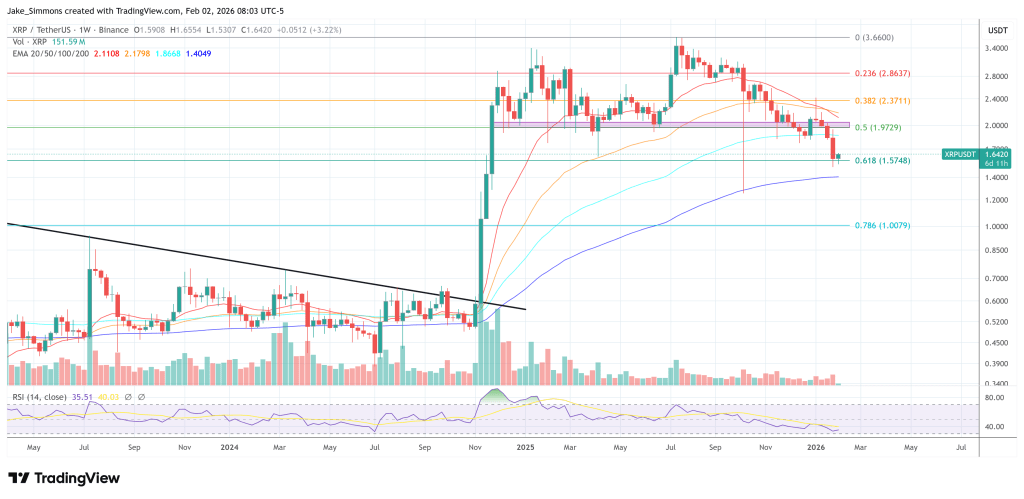

На момент подготовки материала XRP торговался на уровне $1,64.