Оригинал | Odaily Planet Daily (@OdailyChina)

Автор | Azuma (@azuma_eth)

27 января по местному времени США коммерческое подразделение MLS (Высшей футбольной лиги США) Soccer United Marketing (SUM) объявило о заключении многолетнего соглашения о сотрудничестве с платформой прогнозных рынков Polymarket. Согласно соглашению, Polymarket станет официальным и эксклюзивным партнером MLS, Матча всех звезд MLS, финала MLS и Кубка лиг Северной Америки на рынке прогнозов. Со своей стороны, MLS потребует от Polymarket использования официальных данных лиги и систем мониторинга добросовестности третьих сторон, при этом запрещается открывать проекты для ставок, которые, по мнению лиги, легко манипулировать или которые могут быть связаны с инсайдерской информацией.

Это не первый случай сотрудничества спортивных лиг с рынками предсказаний. Еще в октябре прошлого года Национальная хоккейная лига (NHL) заключила многолетние лицензионные соглашения с Kalshi и Polymarket соответственно; затем в ноябре прошлого года Polymarket также заключил соглашение с Абсолютным бойцовским чемпионатом (UFC), став официальным эксклюзивным партнером UFC на рынке прогнозов.

Что означает «официальный эксклюзивный рынок прогнозов»? Означает ли это, что другие неавторизованные платформы в будущем не смогут открывать соответствующие рынки? И какое влияние это окажет на будущую конкуренцию в отрасли? Хотя на данный момент зрелых примеров сотрудничества рынков прогнозов со спортивными событиями ограничено и наблюдаемых образцов мало, на все эти вопросы можно найти похожие ответы на рынках спортивных ставок, чьи услуги极为相似.

- Прим. Odaily: О сходстве услуг рынков прогнозов и спортивных ставок, различиях в регулировании и регуляторной борьбе вокруг рынков прогнозов можно прочитать в нашей статье двухнедельной давности «Посягая на миллиардный пирог индустрии азартных игр, рынки прогнозов преследуются старым порядком».

Эксклюзивная лицензия ≠ Разрешение на рынки

Сначала ответим на самый ключевой вопрос — Означает ли наличие эксклюзивной лицензии, что другие неавторизованные платформы в будущем не смогут открывать соответствующие рынки?

Ситуация со спортивными ставками такова: с тех пор как Верховный суд США 14 мая 2018 года отменил федеральный закон «Акт о защите профессионального и любительского спорта» (PASPA), который запрещал коммерческие спортивные ставки, штаты США получили право самостоятельно решать, легализовывать ли спортивные ставки на своей территории. Другими словами, законность услуг по ставкам зависит от лицензирования на уровне штата, а не от коммерческого授权 лиги — в реальности букмекерским конторам не требуется получать коммерческое授权 от операторов лиг для открытия рынков или предоставления услуг по приему ставок на различные легальные спортивные события.

Однако в некоторых штатах, таких как Теннесси, регуляторы спортивных ставок на уровне штата требуют, чтобы букмекерские компании использовали официальные данные лиги при предоставлении услуг live-ставок (in-play), если только не будет доказано, что эти данные неприменимы или недоступны. Это делает официальное授权 фактором, влияющим на объем услуг букмекерских компаний на практике — только получив授权 на данные, можно предоставлять наиболее полный спектр услуг по ставкам.

Но эта логика пока не применима напрямую к рынкам прогнозов. Поскольку текущая регуляторная система рынков прогнозов еще не ясна (объективно более мягкая), для рынков прогнозов до тех пор, пока не будут определены результаты апелляционных судов и окончательное решение Верховного суда, у Polymarket и Kalshi нет обязанности следовать аналогичным требованиям законов о ставках.

Таким образом, хотя Polymarket в настоящее время получил эксклюзивную лицензию MLS, по крайней мере на данном этапе, это не означает, что другие платформы, такие как Kalshi, уже не могут открывать рынки, связанные с MLS.

Если не обязательно, то какой смысл в лицензии?

Хотя это и не «обязательное授权 для открытия рынков», в реальной коммерческой деятельности между крупными спортивными лигами и букмекерскими компаниями действительно существует множество коммерческих соглашений о сотрудничестве и лицензировании. Например, NFL заключила долгосрочное соглашение о сотрудничестве с Genius Sports, согласно которому Genius作为 единственный официальный поставщик данных授权 букмекерским компаниям данные о событиях в реальном времени, включая списки, отчеты о матчах, статистику и т.д.

Для букмекерских компаний основное значение授权 заключается в том, что они могут через коммерческие соглашения напрямую получать от операторов спортивных событий официальные данные, брендовые授权 для повышения качества услуг и пользовательского опыта. Если это эксклюзивная лицензия, то к этому можно добавить эффект исключительности.

Самое главное значение, естественно, заключается в качестве и полноте данных. По сравнению с сбором данных через сторонние каналы, официальные данные, полученные на основе лицензионного соглашения, обязательно будут более точными, своевременными и полными, что напрямую влияет на повышение точности коэффициентов ставок, ускорение эффективности расчетов и расширение ассортимента ставок. Что касается授权 на уровне бренда и товарных знаков, это позволяет букмекерским компаниям быть более гибкими в продвижении соответствующих рынков —可以使用 логотипы лиг, команд, игроков, избегая при этом риска нарушения прав.

Обратно для спортивных событий, прямое заключение лицензионных соглашений с букмекерскими компаниями также помогает снизить вероятность манипулирования рынком (звучит немного абстрактно...), стороны могут регулировать диапазон ставок и обмениваться данными о подозрительных ставках для своевременного выявления потенциальных возможностей манипулирования. Например, в сотрудничестве Polymarket с MLS четко указано, что запрещается открывать рынки на такие события, как назначение красных и желтых карточек, которые легко поддаются индивидуальному манипулированию, или увольнение главного тренера, трансферы игроков, которые могут быть связаны с инсайдерской информацией.

Учитывая высокую степень重叠ния в эффекте услуг между рынками прогнозов и спортивными ставками, значение лицензионных соглашений для рынка спортивных ставок будет同样 действовать и на рынках прогнозов.

Лобовое столкновение лидеров, обходной маневр второго эшелона

Спортивные ставки уже давно подтвердили себя как масштабный бизнес с определенным ростом, а на рынках прогнозов спортивные события也逐渐 стали категорией с самой высокой долей объема交易.

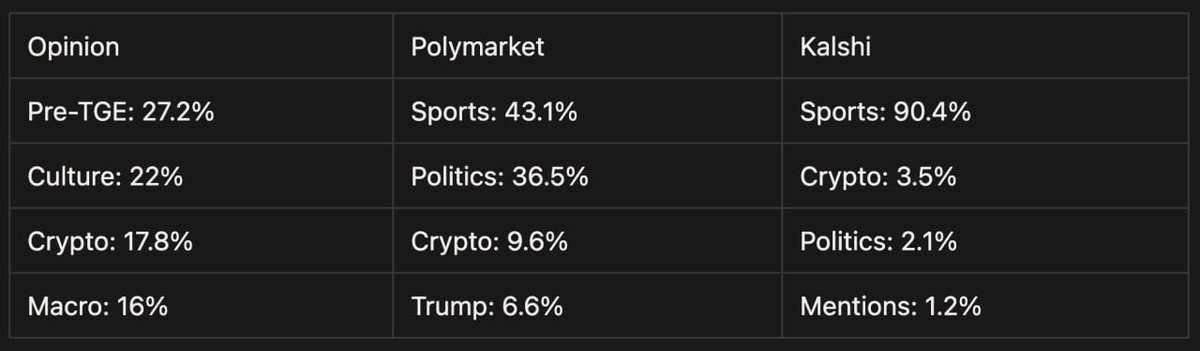

Основатель Primitive Ventures Dovey Wan(@DoveyWan) вчера опубликовала долю объемов различных типов событий на основных платформах прогнозных рынков. Среди них, доля объема ставок на спортивные события на Kalshi превышает 90%, на Polymarket доля объема ставок на спортивные события также достигла 43% — очевидно, что спортивные события стали основным источником трафика для этих двух ведущих рынков прогнозов.

Перед лицом庞大的 существующих масштабов и видимого пространства для роста, рыночная конкуренция была不可避免. В настоящее время из четырех крупных спортивных лиг США только NHL вышла на поле и подписала лицензионные соглашения с Kalshi и Polymarket соответственно, NFL, NBA, MLB все еще находятся в стадии наблюдения. Ожидается, что после того, как Polymarket последовательно захватил эксклюзивные права UFC и MLS, два лидера, Kalshi и Polymarket, обладающие преимуществами в соответствии и капитале, впоследствии, вероятно,展开更 ожесточенную конкуренцию за授权 различных топовых спортивных событий, и inevitably появятся更多的 соглашения об исключительности.

Но данные также揭示另一有趣现象 — возможно, из-за культурных различий и пользовательских привычек,新兴 рынки прогнозов на другом конце света идут по совершенно другому пути дифференциации. Как показано на предыдущем рисунке, доля объема событий, связанных с原生ным рынком криптовалют, на платформе Opinion значительно выше, чем на Kalshi и Polymarket. В то время как лидеры сталкиваются лоб в лоб за огромный пирог спортивных событий, выбор обходного пути, возможно, станет возможностью для проектов второго эшелона догнать на повороте.