Автор: Яш Рой, Bloomberg

Компиляция: Saoirse, Foresight News

Реклама платформы прогнозных рынков Kalshi, размещенная на автобусной остановке в Вашингтоне в марте, с лозунгом «Мы не занимаемся рынками смерти», подчеркивает ее соответствие федеральному регулированию, атакуя конкурента Polymarket за офшорную деятельность без регулирования и чувствительные контракты, связанные с военными конфликтами. Фотограф: Дэниел Хойл / Bloomberg

По мере того как конкуренция в индустрии прогнозных рынков накаляется, а эта новая область подвергается пристальному вниманию регуляторов в Вашингтоне, компании Kalshi и Polymarket обмениваются серьезными обвинениями, ведя ожесточенную борьбу.

Платформы уже неоднократно сталкивались ранее, но в последнее время противоречия резко обострились — Kalshi начала целенаправленную рекламную кампанию, а ее сотрудники публично критиковали Polymarket, значительно усилив риторику.

Бенджамин Фриман, отвечающий за политические и избирательные рынки в Kalshi, в понедельник написал в социальных сетях: «Безответственное, опасное и потенциально незаконное поведение Polymarket угрожает существованию законных прогнозных рынков в США.»

Эти обвинения быстро спровоцировали острую перепалку между двумя компаниями.

Polymarket ответил в заявлении: «Мы приветствуем конкуренцию, но считаем, что дискуссия должна основываться на фактах. Введение общественности в заблуждение вредит всей отрасли и ее участникам.»

Представитель Kalshi Элизабет Диана парировала: «Смешно слышать это от компании, большая часть объема торгов которой приходится на нерегулируемую зарубежную платформу, где правила даже допускают существование "рынков смерти".»

(Прим.: Рынки смерти (Death Markets) — в индустрии прогнозных рынков общее название для торговых контрактов, прямо или косвенно связанных со ставками на смерть, военные конфликты, убийства и другие события, связанные с жизнью, также известны как "рынки assassination")

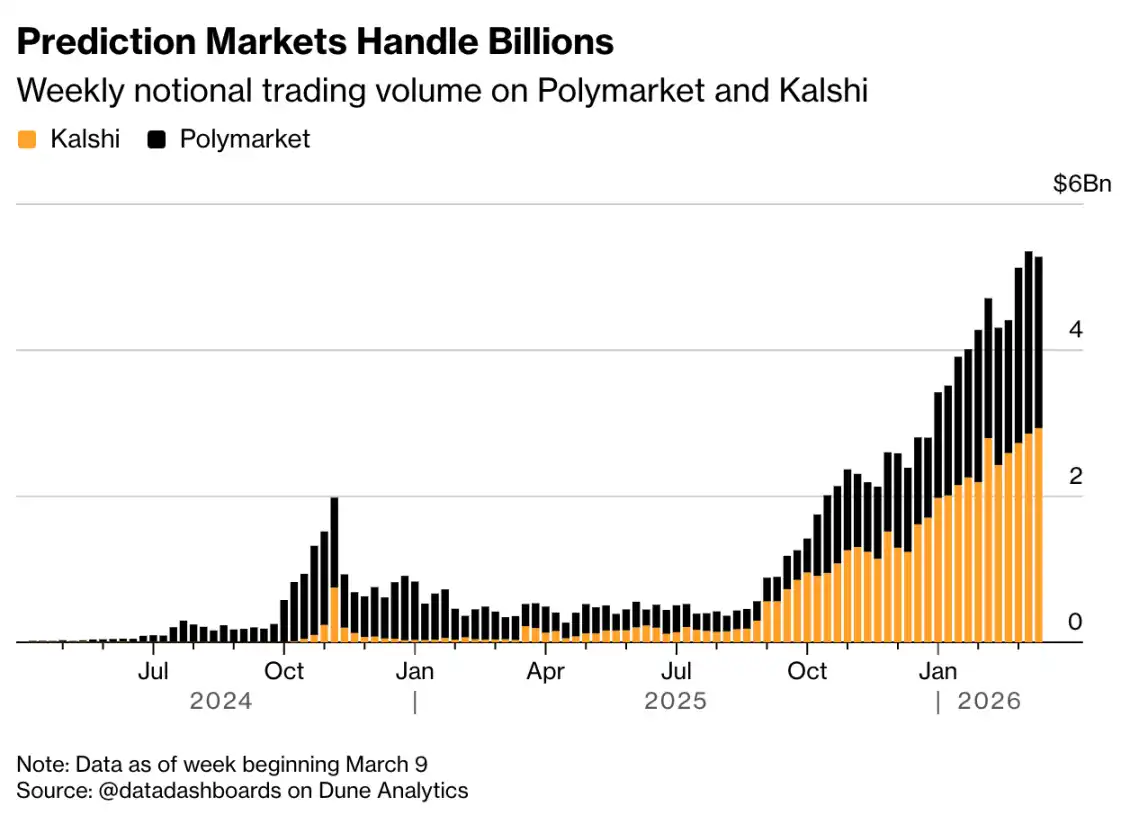

Эта внутренняя распря вспыхнула в ключевой момент, когда Polymarket и Kalshi борются за лидерство в быстрорастущей индустрии прогнозных рынков. Эта отрасль предлагает американцам новый способ делать ставки на различные события, от спортивных соревнований до результатов выборов. Согласно данным, собранным пользователями на Dune Analytics, недавно обе стартап-компании последовательно устанавливали новые рекорды недельного объема торгов, а их совокупный номинальный объем в последнее время приблизился к 60 миллиардам долларов.

Объем торгов на прогнозных рынках достигает миллиардов

Еженедельный номинальный объем торгов Polymarket и Kalshi. Примечание: данные по неделе, закончившейся 9 марта. Источник: @datadashboards на Dune Analytics

В основе спора лежат фундаментальные различия в моделях создания торговых платформ и правилах работы. Платформа Kalshi базируется в США и регулируется Комиссией по торговле товарными фьючерсами США (CFTC); основная же торговая платформа Polymarket расположена за рубежом.

Polymarket использует свое преимущество офшорной деятельности, предлагая контракты, связанные с военными конфликтами, включая боевые действия, связанные с Ираном, которые Kalshi называет аморальными и незаконными.

В одной из рекламных объявлений Kalshi прямо говорится: «Мы не занимаемся рынками смерти.»

В начале этой недели эти маркетинговые объявления от Kalshi в форме «списка правил платформы» начали появляться на автобусных остановках и станциях метро в Вашингтоне.

Одно из них гласит: «Правило первое: мы запрещаем инсайдерскую торговлю, потому что Kalshi — это федерально регулируемая американская биржа.» По мнению отраслевых наблюдателей, подтекст этих слов очевиден: основная платформа Polymarket не подпадает под юрисдикцию американских регуляторов.

Логотип законопроекта «BETS OFF». Конгрессмен Грег Касар и сенатор Крис Мерфи выступают на пресс-конференции, посвященной законопроекту «О запрете торговли, связанной с чувствительными операциями и деятельностью федеральных органов (BETS OFF)». Фотограф: Стефани Рейнольдс / Bloomberg

После обвинений в использовании инсайдерской информации для размещения неправомерных ставок на военные действия США в Иране и Венесуэле, Конгресс обратил внимание на проблему инсайдерской торговли на прогнозных рынках. В ответ Kalshi заняла более жесткую позицию, налагая штрафы и приостанавливая торговлю для пользователей, которых она признала нарушившими правила; Polymarket был более снисходителен, однако с ростом внимания регуляторов платформа недавно также опубликовала собственные правила по инсайдерской торговле.

Представитель Kalshi Диана заявила: «Мы хотим прояснить эти важные различия. Сейчас многие на рынке путают Kalshi и Polymarket, а также смешивают наши разные подходы к регуляторному соответствию.»

Помимо основной зарубежной платформы, у Polymarket также есть регулируемая платформа в США, которая в настоящее время находится на стадии тестирования. Компания заявила, что на обеих платформах действуют «одинаково строгие стандарты добросовестности рынка, включая запрет инсайдерской торговли и манипулирования рынком, активный мониторинг торговли и постоянное взаимодействие с регуляторами и правоохранительными органами».

На сайте Polymarket размещен контракт на тему, атакуют ли хуситы территорию Израиля. Фотограф: Габби Джонс / Bloomberg

Всего несколько месяцев назад соучредитель Kalshi Луана Лопес Лара еще пыталась смягчить напряженность между двумя конкурентами. В октябрьском посте в социальных сетях она выразила надежду, что отрасль выйдет из «разрушительной внутренней борьбы» и будет развиваться совместно.

Теперь看来, это видение в основном рухнуло.

Особенно после того, как в полемику вмешался советник Kalshi, бывший комиссар CFTC Брайан Квентинц, примирить противоречия стало еще сложнее. Комментируя сообщения о том, что прокуроры расследуют инсайдерскую торговлю, Брайан Квентинц на этой неделе в социальных сетях открыто намекнул, что расследование должно быть сосредоточено на Polymarket. Когда с ним связались Bloomberg News, он отказался от дальнейших комментариев.