Whether the United States has "invaded" Venezuela—this semantic judgment directly determines a bet worth over ten million dollars.

You might find this counterintuitive, as in the real world, the U.S. has indeed taken a series of measures against Venezuela, including military deployments and direct actions. In everyday language and media narratives, such actions are easily interpreted as an "invasion."

However, the final settlement result did not align with the expectations of some betting users—Polymarket ultimately did not recognize the U.S. military's actions as constituting an "invasion" within its rule context, thereby negating the validity of the "Yes" option and sparking protests from users.

This is actually a not-so-new but highly representative controversy, once again exposing a long-standing yet often overlooked structural issue in prediction markets: When it comes to complex real-world events, on what basis, and by whom, is "fact" defined in decentralized prediction markets?

I. Frequent "Semantic Traps" in Prediction Markets

The reason it is "not so new" is that similar semantic disputes have occurred multiple times in prediction markets.

Indeed, such situations on Polymarket are already commonplace, especially in predictions surrounding political figures and international situations. The platform has repeatedly produced adjudication results that users consider "counterintuitive." Some predictions, almost uncontroversial in reality, have fallen into repeated appeals and reversals on-chain; other events have seen final adjudication results that significantly deviate from most users' real-world judgments.

In more extreme cases, during the dispute adjudication phase, the oracle mechanism allows token holders to participate in voting, leading to situations where certain topical events can be "swayed by the voting power of major players"...

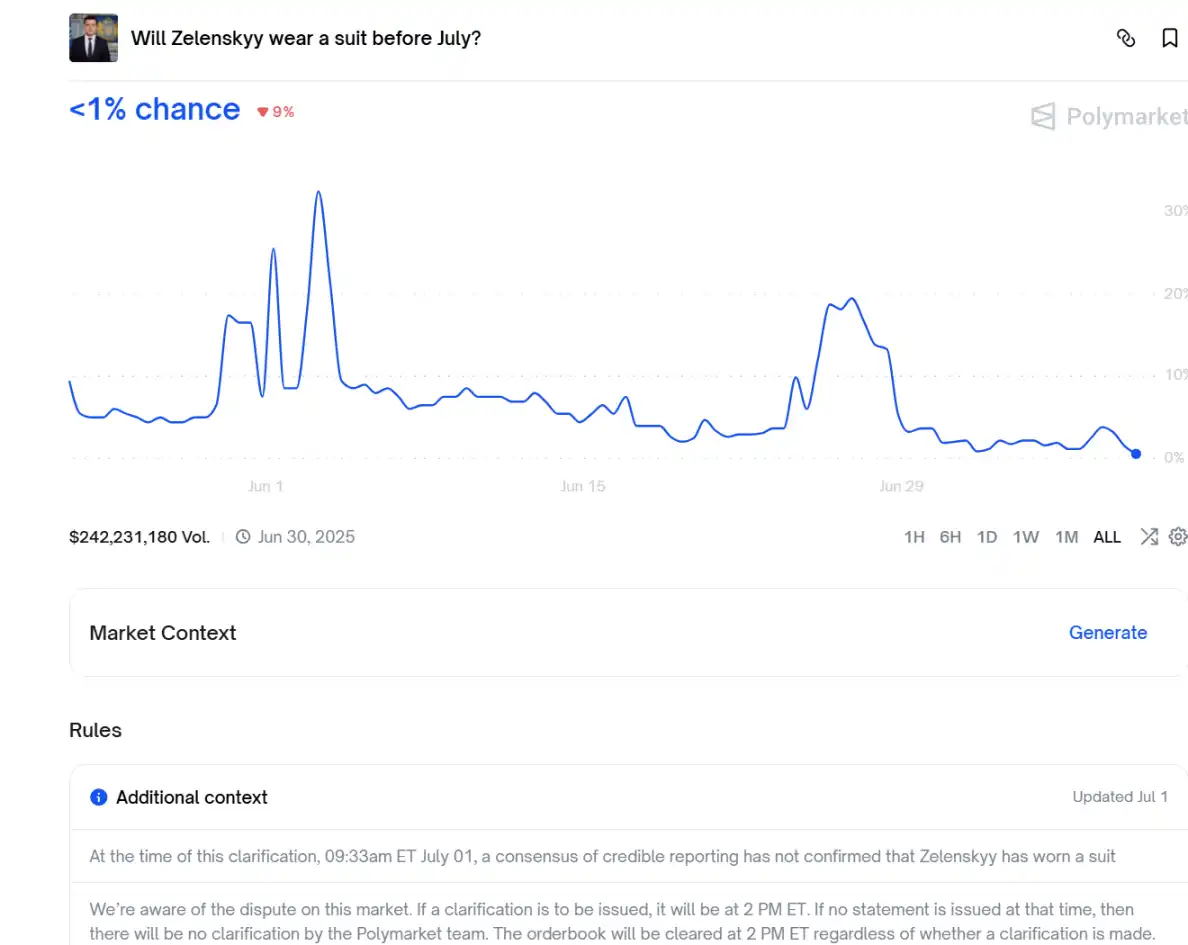

These controversies share a common characteristic: they are often not technical issues but social consensus problems. A widely discussed example is the prediction about whether Ukrainian President Zelensky "wore a suit" at a specific time:

In reality, Zelensky wore a formal suit to a public event last June. Interpretations from multiple sources, including the BBC and designers, confirmed it as a suit. By common sense, the result should have been settled. But on Polymarket, this seemingly clear fact turned into a tug-of-war involving hundreds of millions of dollars.

During this period, the probability of Yes and No fluctuated wildly, with high-risk arbitrage behaviors. Some achieved huge floating profits in a short time, while the final settlement was repeatedly delayed.

The key issue is that Polymarket relies on the decentralized oracle UMA for result adjudication. Its operating mechanism allows holders to participate in dispute resolution through voting, making it easy for major players to manipulate the outcome of certain topical events.

More controversially, the platform level does not deny that this mechanism could be exploited but insists on "rules are rules," refusing to adjust the adjudication logic afterward, ultimately allowing large funds to flip the outcome using the rules themselves.

It is precisely such cases that provide a highly representative and clear insight into the institutional boundaries of prediction markets.

II. The Failure Boundary of "Code is Law"

Objectively speaking, prediction markets are now considered one of the most imaginative applications of blockchain. They are no longer just a small tool for "betting" or "predicting the future" but have become outposts for institutions, analysts, and even central banks to observe market sentiment (Extended reading: "The Breakout Moment of 'Prediction Markets': ICE Enters, Hyperliquid Doubles Down, Why Are Giants Competing to 'Price Uncertainty'?").

But all of this has a prerequisite: prediction questions must be answerable clearly.

It is important to know that blockchain systems are naturally good at handling deterministic problems—such as whether assets have arrived, whether states have changed, whether conditions have been met. Once these results are written on-chain, there is almost no room for tampering.

However, prediction markets often face another type of object: whether a war has broken out, whether an election has ended, whether a certain political or military action constitutes a judgment of a particular nature. These problems are not inherently encodable; they highly depend on context, interpretation, and social consensus, rather than a single, verifiable objective signal.

This is why, no matter what kind of oracle or adjudication mechanism is adopted, subjectivity is almost unavoidable in the process of translating real-world events into settleable results.

This is also why, in multiple Polymarket controversies, the disagreement between users and the platform is not about whether the facts exist, but about which interpretation of reality is the one that can be settled.

Ultimately, when this power of interpretation cannot be completely formalized by code, the underlying logic of the grand vision that "code is law" inevitably hits its boundary in the face of complex social semantics.

III. The "Last Mile" of Truth is Hard to Decentralize

In many decentralized narratives, "centralization" is often seen as a system defect. But the author believes that in the specific context of prediction markets, the opposite is true.

Because prediction markets do not eliminate adjudication power; they merely transfer it from one position to another:

- Trading and settlement phase: Highly decentralized, automated execution;

- Definition and interpretation phase: Highly centralized, reliant on rules and adjudicators;

In other words, decentralization solves the credibility of execution but cannot avoid the reality of centralized interpretation power. This is why the concept of "code is law," which is highly attractive in the blockchain world, often seems inadequate in prediction markets—because code cannot generate social consensus on its own; it can only faithfully execute established rules.

And when the rules themselves cannot cover the full complexity of reality, adjudication power inevitably returns to the hands of "people." The only difference is that this power no longer appears as an explicit arbiter but is hidden within problem definition, rule interpretation, and adjudication processes.

Returning to the Polymarket controversy itself, it does not mean the failure of prediction markets, nor does it mean the decentralized narrative is a castle in the air. On the contrary, such controversies remind us to re-understand the applicable boundaries of prediction markets: They are very suitable for data/events with clear outcomes and definitions but are naturally not good at handling highly politicized, semantically ambiguous, value-judgment-intensive real-world problems.

From this perspective, prediction markets never solve "who is right or wrong" but rather how the market efficiently aggregates expectations under given rules. So once the rules themselves become the focus of controversy, the system exposes its institutional boundaries.

Like the latest controversy over whether Venezuela was "invaded," it essentially shows that when it comes to complex real-world events, decentralization does not mean there is no adjudicator, but that adjudication power exists in a more hidden way.

For ordinary users, what truly matters may not be whether the prediction market "is decentralized," but rather: when a dispute occurs, who has the power to define the problem? Who decides which version of reality can be settled? Are the rules clear and predictable enough?

In this sense, prediction markets are not only an experiment in collective wisdom but also a power game about "who has the right to define reality."

Understanding this, we can find a balance point closer to certainty amidst uncertain truths.