Автор: Frank, PANews

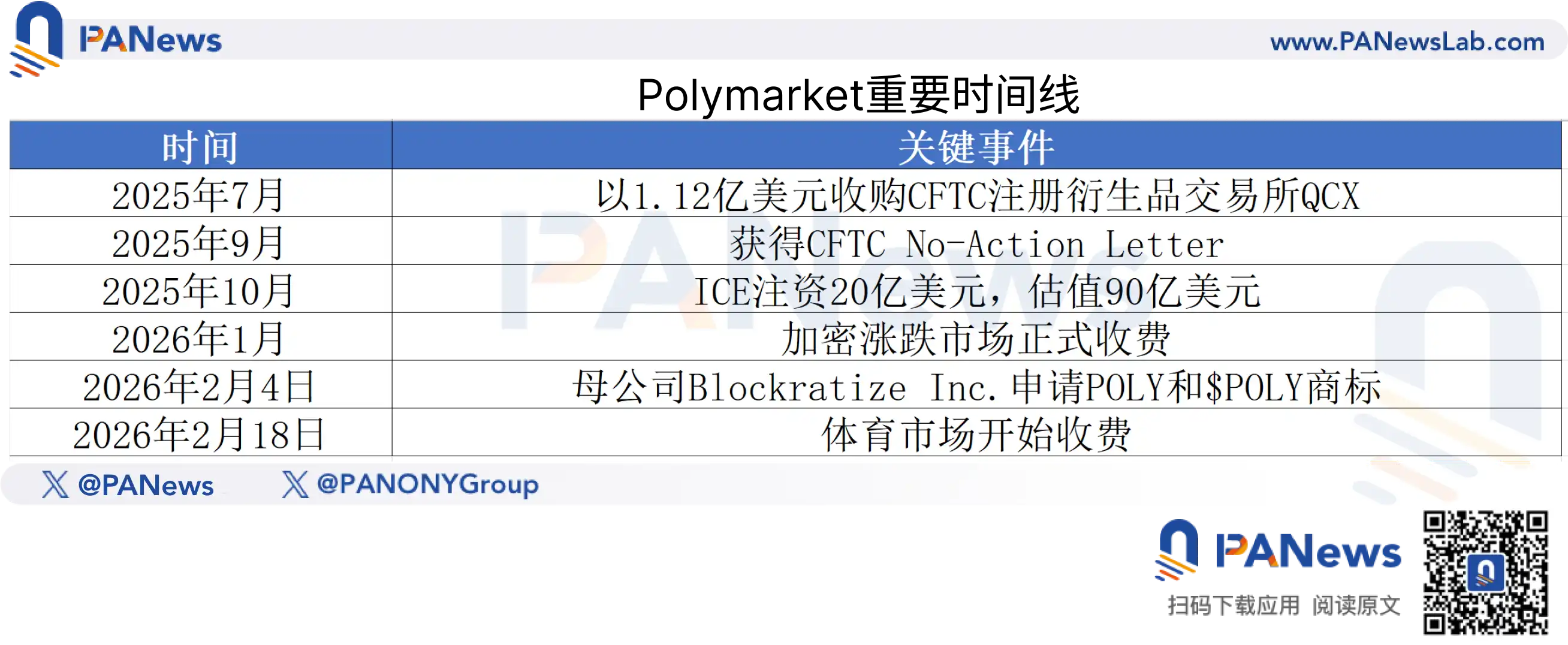

18 февраля 2026 года Polymarket объявил, что с этого дня платформа начнет взимать комиссию с рыночных ордеров в спортивных рынках в рамках пилотного проекта. Первыми охваченными событиями стали студенческий баскетбол в США (NCAA) и Серия А Италии, в будущем эта практика будет постепенно распространена на все спортивные события.

Ранее, только за счет комиссий с рынка 15-минутных колебаний криптовалют, недельный доход Polymarket недавно превысил 1,08 миллиона долларов. Согласно данным блокчейна, спортивные рынки составляют почти 40% от общей торговой активности платформы. Если пересчитать в годовой доход, то только收费 с крипторынка может обеспечить годовой доход около 56 миллионов долларов. Таким образом, когда начнут взимать плату с более крупной доли спортивного рынка, Polymarket, возможно, станет крупнейшим «печатным станком» в криптосфере.

PANews провел глубокий анализ механизма комиссий, модели выручки, сравнения с конкурентами и ожиданий по эирдропу токена Polymarket.

От «нулевого дохода» к миллиону в неделю: 90-миллиардный гигант начинает спешно зарабатывать

В течение длительного времени Polymarket работал практически с «нулевым доходом», на большинстве рынков не взимая никаких комиссий за сделки. Эта бесплатная стратегия принесла ему впечатляющий рост: совокупный объем торгов за 2025 год достиг 21,5 миллиарда долларов, что составляет почти половину от общего объема торгов на глобальном рынке прогнозов (44 миллиарда долларов); в январе 2026 года месячный объем торгов достиг рекордных 12 миллиардов долларов.

Однако с приближением листинга в этом году модель с нулевым доходом явно не соответствует его оценке. В последнем раунде финансирования его оценка достигла 9 миллиардов долларов. В октябре 2025 года Intercontinental Exchange (ICE), материнская компания Нью-Йоркской фондовой биржи, инвестировала в Polymarket колоссальные 2 миллиарда долларов. Согласно данным PM Insights, по состоянию на 19 января 2026 года подразумеваемая оценка акций Polymarket на внебиржевом рынке выросла до 11,6 миллиарда долларов, что на 29% больше, чем в предыдущем раунде финансирования. По слухам, оценка в последующих раундах финансирования может достичь 12-15 миллиардов долларов. Такая высокая оценка требует соответствующей выручки для ее поддержания.

Переломный момент произошел в январе 2026 года, и с начала года стало заметно, что Polymarket начал спешить.

В январе Polymarket официально ввел «Комиссию тейкера» (Taker Fee) для своего продукта для высокочастотной торговли — рынка 15-минутных колебаний криптовалют, максимальная ставка может достигать 3%. Данные сразу же показали результат: в начале февраля 2026 года недельный доход от комиссий превысил 1,08 миллиона долларов, причем в одну из недель января только рынок 15-минутных колебаний contributed 787 тысяч долларов, что составило 28,4% от общего дохода от комиссий на всех рынках прогнозов платформы (2,7 миллиона долларов) за тот же период. На сегодняшний день Polymarket уже заработал более 4,7 миллиона долларов комиссий, войдя в число лидеров по доходам.

Искусный дизайн behind 0.45%: Модель тарифов, созданная не только для заработка

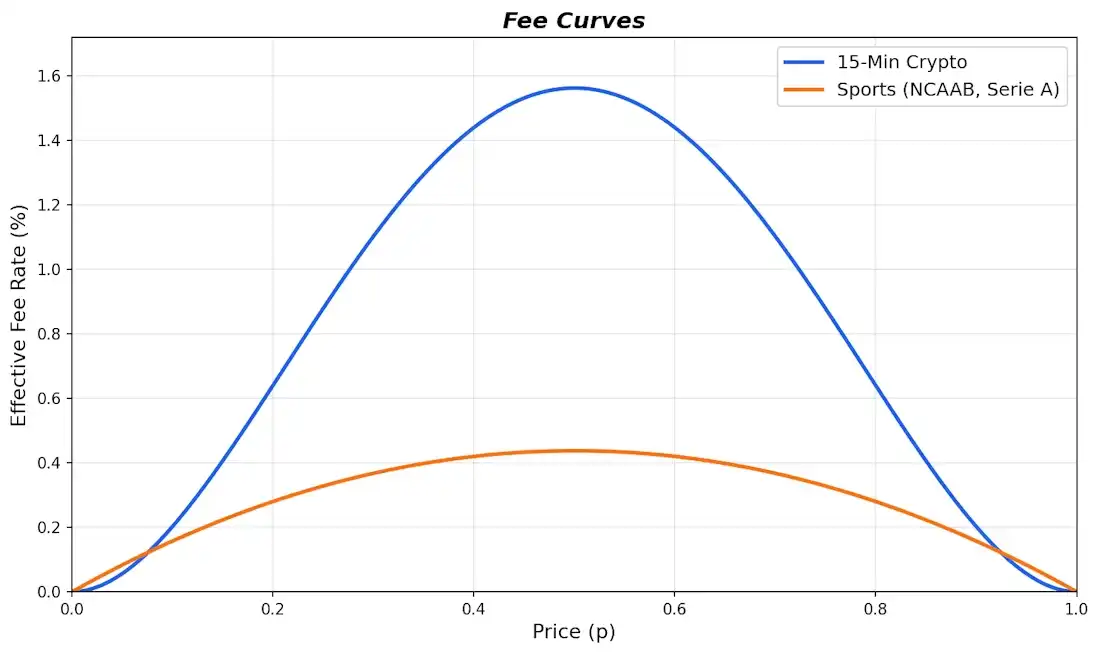

Введенная Polymarket комиссия для спортивных рынков представляет собой тщательно разработанную динамическую модель тарифов.

Согласно официальной документации Polymarket и анализу сообщества, комиссия на спортивных рынках взимается только с рыночных ордеров (Taker), лимитные ордера (Maker) не только бесплатны, но и получают 25% кэшбэк от комиссии тейкера. Как и в модели收费 на крипторынке, ставка не является фиксированной, а колеблется в зависимости от изменения вероятности события:

Проще говоря, чем более неопределенным является рынок, тем выше комиссия: при вероятности 50% комиссия достигает пика в 0,44%, а при вероятности 10% или 90% снижается до всего лишь 0,13%-0,16%.

Однако по стандартам тарифы на спортивных рынках значительно ниже, чем на крипторынке. Тем не менее, это не влияет на потенциал доходов спортивного рынка.

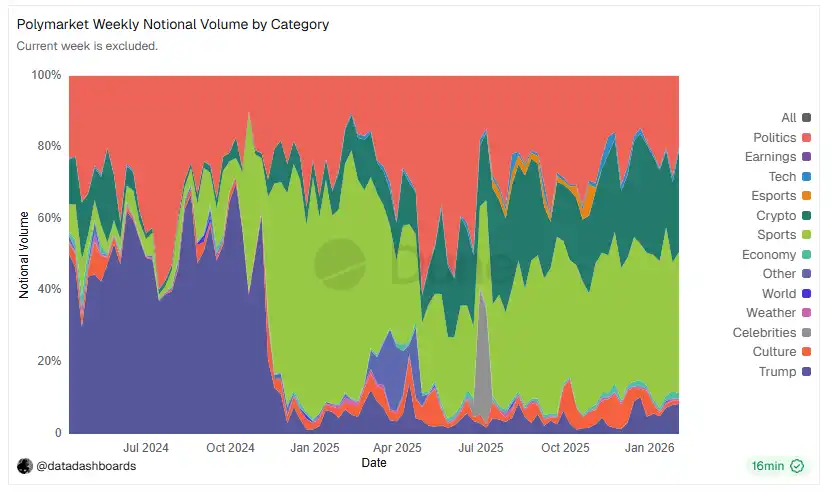

Согласно данным, в настоящее время спортивные рынки составляют 39% от общей торговой активности Polymarket, опережая политические (20%) и криптовалютные (28%). Что еще более важно, согласно предыдущему анализу PANews, средний объем торгов на краткосрочных спортивных рынках Polymarket (1,32 миллиона долларов) в 30 раз превышает средний объем торгов на краткосрочных крипторынках (44 тысячи долларов). Это означает, что при полном открытии收费 на спортивных рынках доходы значительно возрастут.

На примере Супербоула 2026 года: общий объем торгов на связанных с Супербоулом рынках Polymarket достиг approximately 795 миллионов долларов, охватывая несколько подрынков, включая прогнозы на исход матча, выступление игроков, шоу в перерыве и т.д. Недельный объем торгов на всех рынках прогнозов однажды достиг 6,3 миллиарда долларов благодаря спортивным событиям.

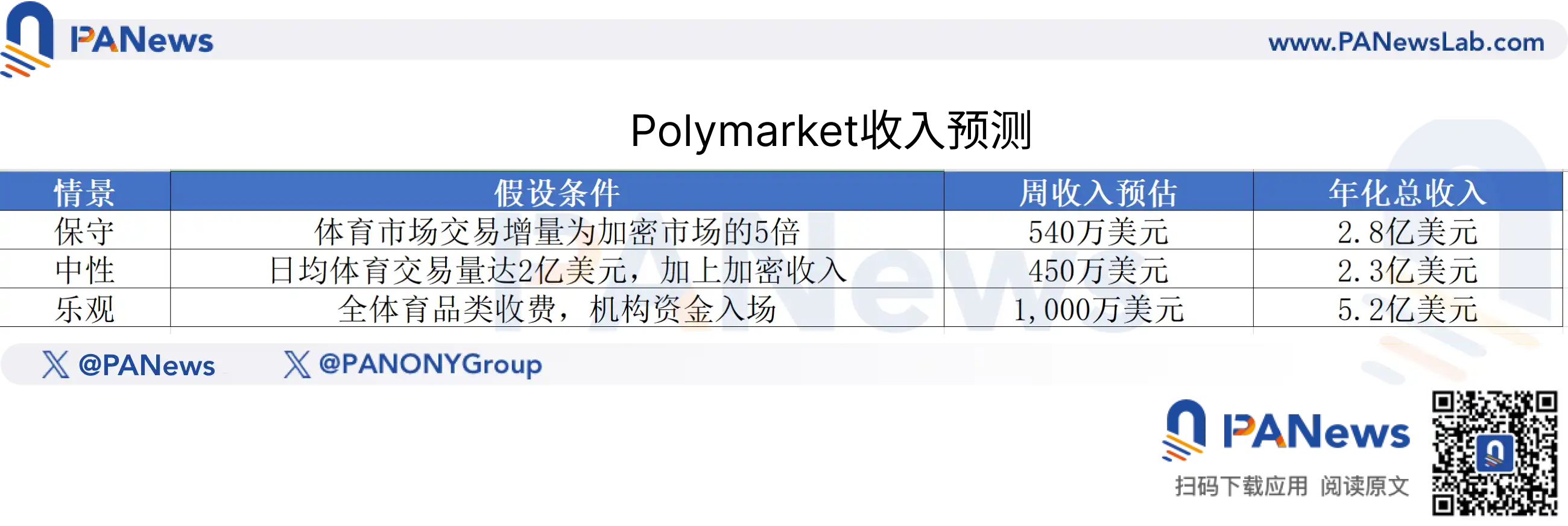

На основе имеющихся данных PANews построил три сценария прогноза прибыли (предполагая, что средняя эффективная ставка на спортивных рынках составляет 0,25%, с учетом распределения вероятностей и бесплатных лимитных ордеров):

Даже по самым консервативным оценкам, годовой доход Polymarket после полного введения платы превысит 200 миллионов долларов, что позволит ему войти в число протоколов с самыми высокими доходами в сфере Web3.

Хотя превзойти доход Tether от процентов по казначейским облигациям или комиссии за газ в сети Ethereum нереально, на уровне приложений Polymarket полностью имеет потенциал побороться за звание «самого прибыльного dApp». Особенно учитывая, что коэффициент удержания пользователей составляет 85%, что значительно превышает показатели обычных DeFi-протоколов, такая высокая вовлеченность означает более качественный доход.

Токен POLY и эирдроп: «Пиршество богатства» стоимостью в сотни миллионов долларов?

Высокая оценка Polymarket и庞大的用户基数 делают его эирдроп одним из самых ожидаемых событий 2026 года.

Главный маркетинговый директор Polymarket Мэтью Модаббер четко заявил: «Токен будет, эирдроп будет». Рынок прогнозирует, что вероятность выпуска токена Polymarket до 31 декабря 2026 года составляет 62%-70%, и, учитывая темпы возобновления бизнеса в США, TGE, вероятно, будет завершен в середине 2026 года.

4 февраля 2026 года его материнская компания Blockratize Inc. подала заявку на товарные знаки «POLY» и «$POLY», что также считается рынком важной вехой на пути к TGE. Согласно общей практике криптоиндустрии, от регистрации товарного знака до TGE обычно требуется 3-6 месяцев.

Масштаб эирдропа может превысить Hyperliquid, эпоха накрутки объема закончилась

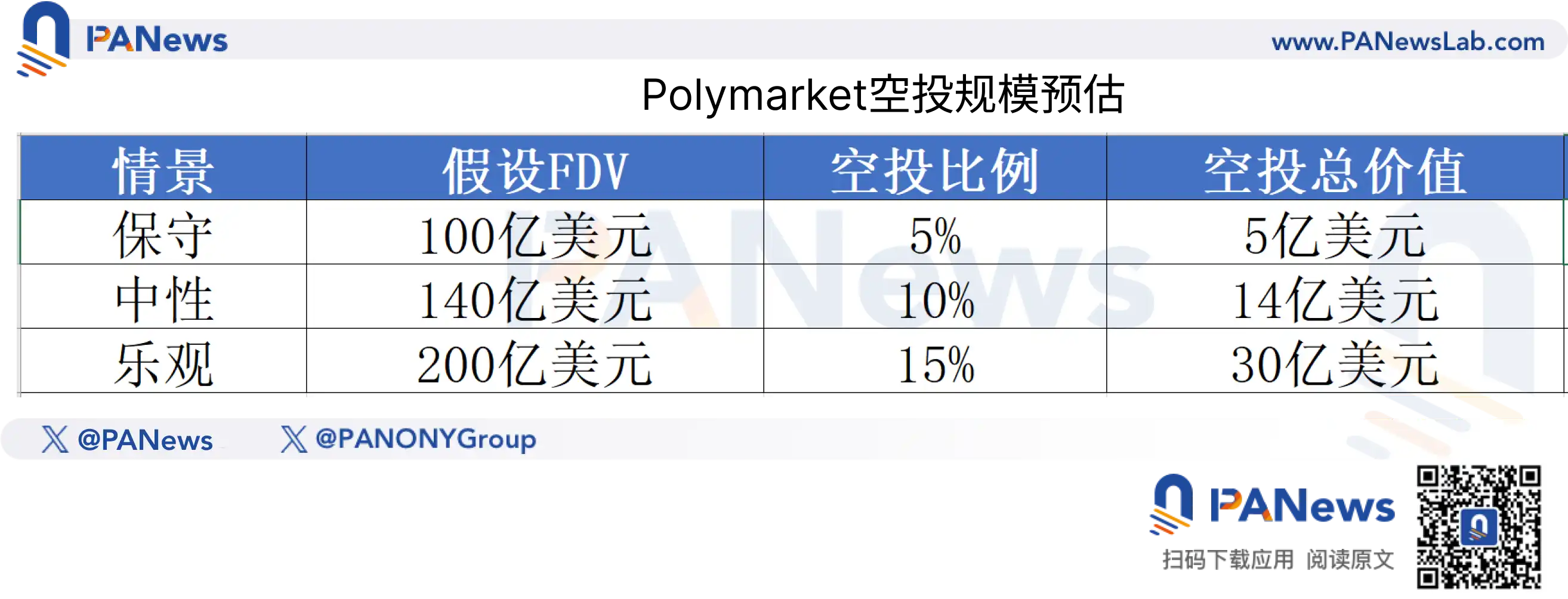

Ссылаясь на долю эирдропа недавних топовых проектов (Arbitrum, Jupiter, Hyperliquid), доля сообщества обычно составляет от 5% до 15% от общего предложения. PANews провел расчеты на основе различных предположений об оценке:

Если общая сумма эирдропа составит 1,4 миллиарда долларов, и предположить, что количество активных адресов, имеющих право на участие, составляет 500 000, средняя стоимость эирдропа на аккаунт может составить approximately 2800 долларов. Однако, согласно «принципу Парето», доходы топовых пользователей могут достигать сотен тысяч или даже миллионов долларов, поэтому обычным散户投资者 необходимо разумно управлять ожиданиями.

Особого внимания заслуживает то, что одновременно с началом взимания платы Polymarket推出了 годовая награда за хранение (Holding Rewards) в размере 4%, с ежечасными снепшотами и ежедневными выплатами. Этот механизм reveals явное предпочтение проектной команды: время удержания средств гораздо важнее частоты交易.

Ров с водой и скрытые тревоги: в чем риски этого «печатного станка»?

Взимание платы означает, что пользователям придется нести дополнительные издержки, так почему Polymarket сможет удержаться?

Три уровня рва с водой清晰可见: Во-первых, платформа обладает несравненной глубиной ликвидности в сфере рынков прогнозов, что крайне важно для крупных трейдеров. Во-вторых, по сравнению с традиционным отчислением в азартных играх в размере 5%-10% и 1%-3,5% у Kalshi, пиковая ставка в 0,45% по-прежнему обладает подавляющим преимуществом в стоимости. В-третьих, вход ICE принес не только资金, но и возможности распространения данных; ICE планирует подключить данные реального времени Polymarket к глобальным институциональным клиентам, что构成 вторую кривую роста помимо交易 комиссий.

Однако риски同样不容忽视:

Краткосрочные колебания объема торгов: месячный объем торгов Polymarket ранее снизился с пика в 1,026 миллиарда долларов в ноябре 2025 года до 543 миллионов долларов в декабре. Усилит ли введение платы эту тенденцию? Однако, учитывая положительный эффект увеличения глубины стакана и缩小 спреда после введения Maker Rebate, в долгосрочной перспективе объем торгов, вероятно, вырастет.

Конкурентная среда: Kalshi имеет преимущество первопроходца на регулируемом рынке США (выручка в 2025 году составила approximately 260 миллионов долларов), Hyperliquid пытается войти на рынок прогнозов через «Outcome Trading» (FDV approximately 16 миллиардов долларов), а Predict.fun привлекает пользователей с помощью叠加 DeFi-доходности.

Регуляторная неопределенность: Несмотря на получение Письма о неприменении мер (No-Action Letter) от CFTC и приобретение регулируемой биржи QCX, изменения в регуляторной среде США始终 являются дамокловым мечом, висящим над рынком прогнозов.

Послесловие

От бесплатного до платного, от рынка колебаний криптовалют до глобальных спортивных событий, Polymarket проводит тщательно спланированную модернизацию бизнес-модели. Только за счет крипторынка он уже зарабатывает миллионы в неделю, а спортивный рынок, этот колосс, занимающий почти 40% объема торгов платформы и имеющий ликвидность в 30 раз выше, чем у крипторынка, только начинает взимать плату. История Polymarket предоставляет вдохновляющую модель: истинная ценность платформы, возможно, заключается не в том, сколько она зарабатывает в данный момент, а в том, что она доказала свою уверенность в том, что «может взимать плату, когда захочет». Когда пирог достаточно велик, а ров с водой достаточно глубок, открытие шлюзов для взимания платы — это лишь вопрос времени.

И этот «печатный станок», который только разогревается, 18 февраля лишь нажал кнопку запуска.