Автор: Jay Yu

Компиляция: Jiahuan, ChainCatcher

Для самых быстрорастущих технологических компаний в мире публичные рынки уже не те, что были раньше. Тридцать лет назад Amazon провела IPO спустя три года после основания с оценкой в 438 миллионов долларов. Netscape провела первичное публичное размещение через восемнадцать месяцев после создания.

Но сегодня самые быстрорастущие компании (Stripe, SpaceX, OpenAI, Ramp) обычно остаются частными более десяти лет. Возможность доступа к этапу высокого роста, которым инвесторы когда-то могли легко воспользоваться на публичных рынках, теперь тихо перехвачена частным капиталом при постоянно растущих балансовых оценках.

«Если говорить цинично, [венчурный капитал] перехватил этап роста компаний, которые раньше рано выходили на IPO. Amazon вышел на биржу, когда его рыночная капитализация была меньше десяти миллиардов долларов. Сегодня это трудно представить». — Билл Герли

Рынок отреагировал на это некоторыми временными решениями: специальными целевыми компаниями (SPV), платформами вторичного рынка, тендерами и другими инструментами, призванными удовлетворить желание инвесторов иметь доступ к активам рискового роста. Но это лишь заплатки, а не фундаментальное решение.

То, чего действительно хотят инвесторы, возможно, и есть то самое видение, которое несли публичные размещения технологических компаний тридцать лет назад: получить широкий и ликвидный доступ к инвестициям в эпохальные компании, разделить огромную доходность венчурного уровня.

Токенизация рисковых активов может быть частью ответа. В этой статье рассматриваются три вопроса, исследующих, как токенизация стартапов может восстановить баланс на этих разрозненных рынках:

(1) Почему сейчас подходящее время для развития токенизированных стартапов

(2) Как выглядит ландшафт токенизированных стартапов

(3) Каковы ключевые возможности, вызовы и неразрешенные противоречия, препятствующие масштабированию этой области.

Часть первая: Почему токенизация стартапов наступает именно сейчас?

Токенизация стартапов находится на перекрестке трех основных тенденций:

(1) Взрывной рост временных инструментов, таких как SPV, в качестве фактического механизма ликвидности для эпохальных технологических компаний

(2) Быстрый рост токенизации реальных мировых активов (RWA), охватывающей денежные рынки, публичные акции, сырьевые товары и другие области

(3) Разрушение консенсуса «токен против акций», из-за которого токены проектов все больше становятся гражданами второго сорта по сравнению с венчурными инвестициями.

1.1 Восход SPV

Десять лет назад SPV были нишевым инструментом, способом агрегации капитала вне традиционных структур венчурного финансирования или публичных размещений. Но за последние два года они стали ключевой частью капитальной стратегии, а такие платформы, как AngelList, Carta и Assure, сделали создание SPV под конкретные возможности и компании как никогда простым.

Особенно SPV вторичного рынка выросли более чем на 545% за последние два года, привлекая в более чем 10 раз больше капитала. Эти временные рыночные структуры уловили значительный рыночный рост: взвешенная корзина 50 крупнейших активов вторичного рынка Hiive показала рост в 49,1% в 2025 году, значительно опередив индекс S&P 500.

Это указывает на то, что инвесторы используют временные структуры частного рынка, чтобы восстановить функции, которые публичные рынки когда-то выполняли более гладко: доступ, ликвидность и ценовое обнаружение. Поскольку компании остаются частными все дольше, SPV стали одним из основных альтернативных решений.

1.2 RWA, токенизация и перпетуализация всего

Вторая тенденция — это рост токенизации и перпетуальных (бессрочных) рынков в различных классах активов.

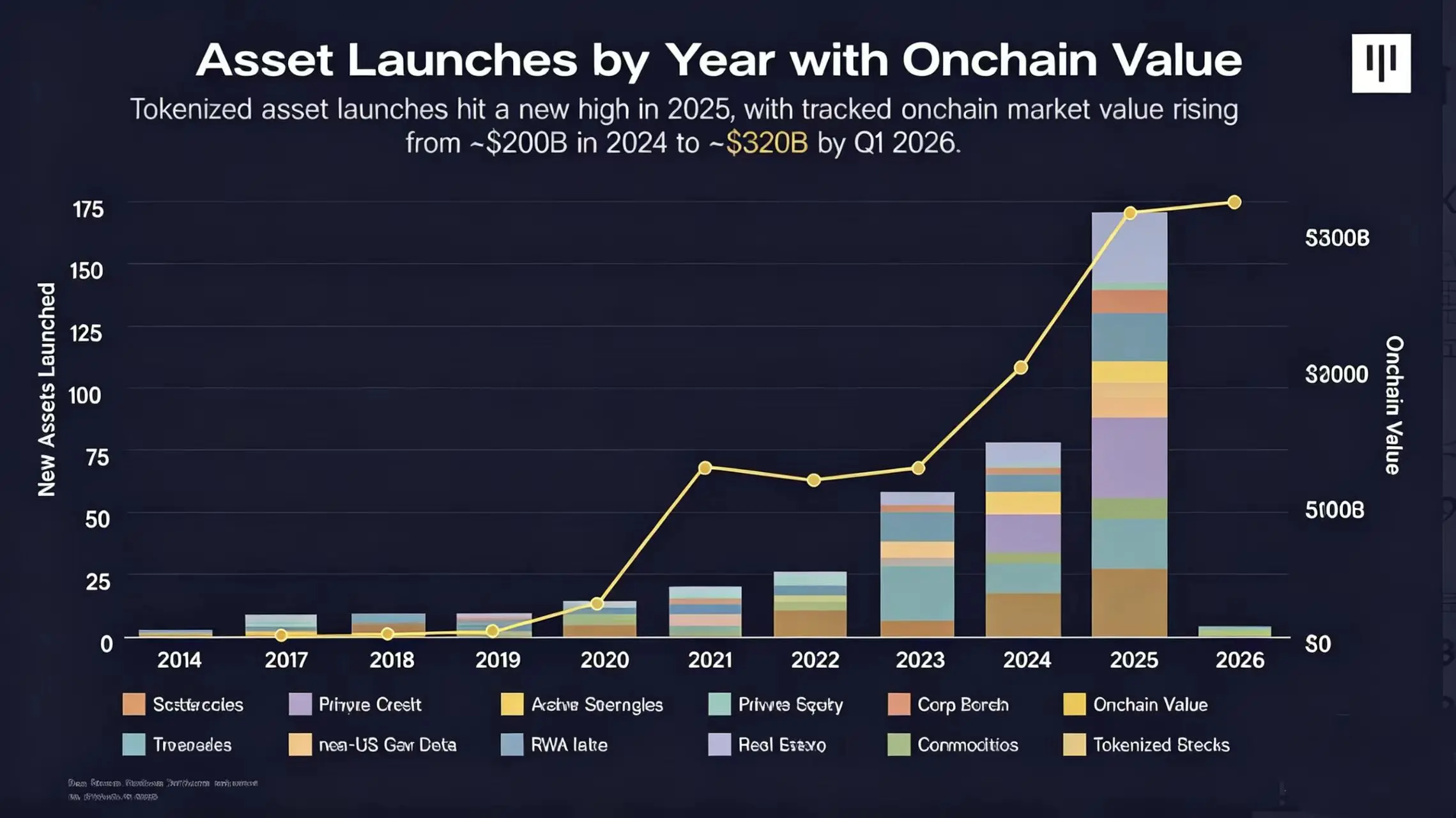

В первом квартале 2026 года стоимость RWA в ончейне достигла примерно 320 миллиардов долларов. Хотя крупнейшим классом активов RWA по-прежнему являются казначейские обязательства США (которые могут служить залогом для стейблкоинов), наблюдался значительный рост и в других классах активов, таких как сырьевые товары, акции, а также обеспеченные активами кредиты (например, кредиты под залог недвижимости от Figure).

По мере принятия RWA мы видим созревание цепочки поставок токенизации: от эмитентов и хранителей до нормативных рамок.

В то же время перпетуальные фьючерсы также получили огромное развитие за последние два года с появлением перпетуальных децентрализованных бирж (perp-DEX), таких как Hyperliquid. По сравнению с деривативами с датой истечения, перпетуальные фьючерсы не имеют срока действия, что дает преимущества на практике исполнения, их легче понять с точки зрения риска, и они изначально поддерживают круглосуточную торговлю.

Такие проекты, как TradeXYZ, также расширяют перпетуальные фьючерсы на другие классы активов, помимо чистых криптовалютных пар (например, BTC-USDC), включая акции США и Кореи, сырьевые товары и фондовые индексы, сочетая HIP-3 для предоставления стандартизированного метода создания новых перпетуальных рынков.

1.3 Разрушение консенсуса «токен против акций»

Третья растущая тенденция — это дилемма захвата стоимости между токенами и акциями.

Токены децентрализованных финансовых проектов, такие как UNI и AAVE, при выпуске четко заявляли, что не представляют собой акции, чтобы решить регуляторные проблемы. Это создало «консенсус токена против акций», согласно которому токены проекта должны служить синтетическими инструментами, дающими владельцам «право управления» частью протокола, с обещанием взимания комиссий как средства захвата стоимости.

Однако это создало двухуровневую систему, где захват стоимости стал игрой с нулевой суммой, и держатели токенов стали как бы гражданами второго сорта по сравнению с держателями акций.

Эта проблема стала очевидной в недавних событиях, таких как противостояние Aave DAO и Labs, а также спорное приобретение Axelar компанией Circle, где интересы держателей токенов были подчинены интересам акционеров.

Все это побуждает переосмыслить существующий «консенсус токена против акций»: как нам разработать токены, которые лучше отражают потенциал роста проекта?

Пересечение этих трех тенденций может проложить путь для подъема «токенизированных стартапов»: то есть предоставление токенизированного инвестиционного доступа к компаниям с потенциалом роста венчурного масштаба, позволяющего обычной публике, как раньше на публичных рынках, раньше знакомиться с эпохальными выдающимися компаниями.

Таким образом, токены становятся переосмыслением традиционного механизма первичного публичного размещения, предоставляя более широкой публике доступ к самым горячим компаниям-гигантам.

Часть вторая: Ландшафт токенизированных стартапов

2.1 Современные подходы к дизайну и объемы торгов

Сегодня токенизированные стартапы имеют разнообразные подходы и дизайн по двум основным измерениям: механизму инвестирования и стадии стартапа.

Инвестиционные механизмы токенизированных стартапов варьируются от инструментов SPV, владеющих акциями (например, PreStocks), закрытых фондов, предоставляющих доступ к акциям компании (например, Robinhood Ventures), до чистых перпетуальных фьючерсов (например, TradeXYZ и Ventuals), которые предоставляют только ценовой доступ без права собственности на базовые акции.

Стадии стартапов варьируются от ранних компаний (например, платформа MetaDAO) до активов стадии роста и широко известных компаний, готовящихся к IPO (например, SpaceX, Anthropic и OpenAI).

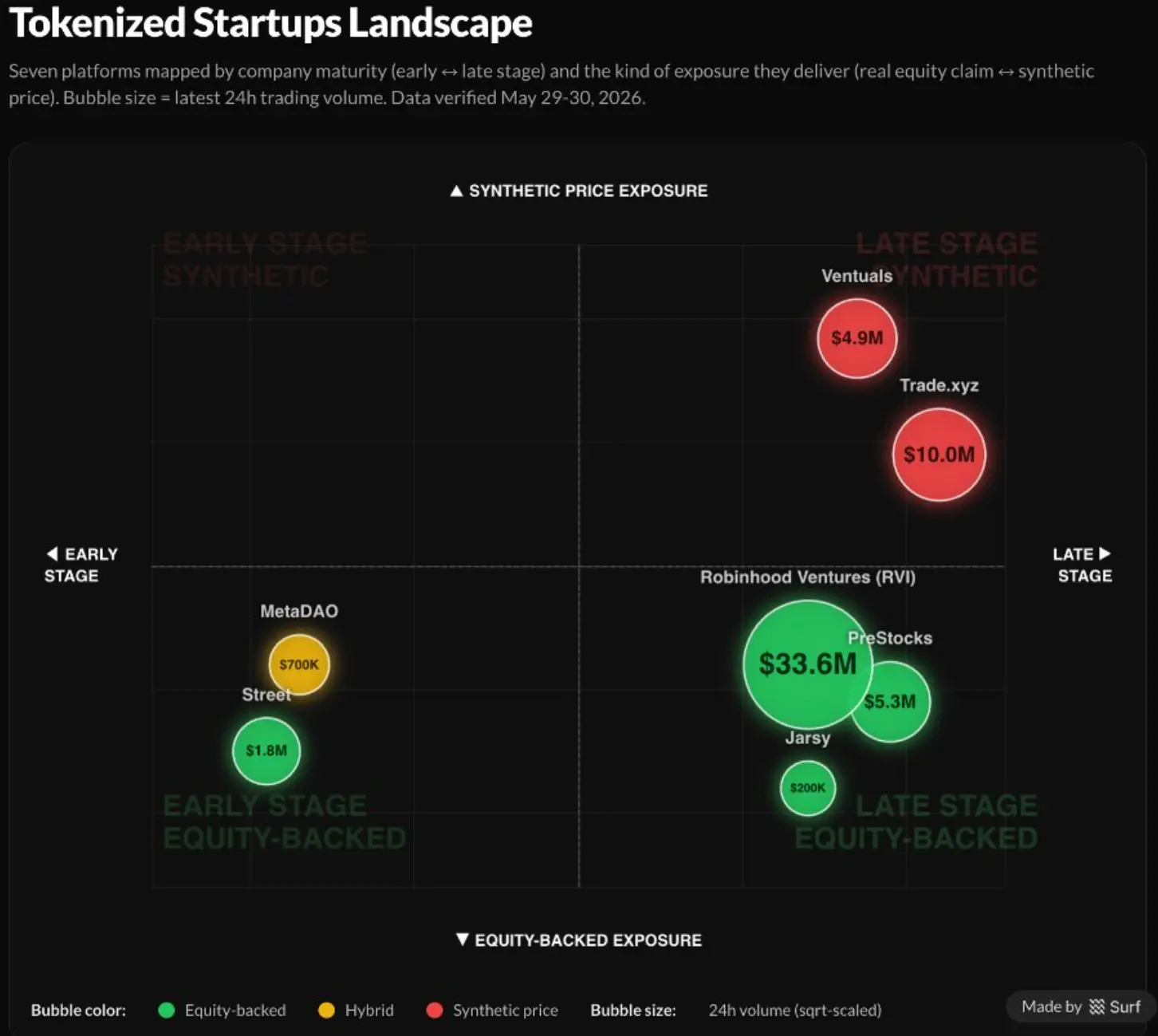

Разбирая основных игроков в этой области и их масштабы (24-часовой объем торгов по состоянию на 30 мая), мы отмечаем несколько очевидных моделей.

Во-первых, самая большая тенденция заключается в том, что объемы торгов на платформах для поздних стадий (особенно пред-IPO стартапов) более чем в 10 раз выше, чем на ранних стадиях. В частности, пользователи, кажется, предпочитают инвестировать в известные компании, такие как SpaceX, Anthropic, Anduril и OpenAI, независимо от того, на какой платформе представлены эти активы.

Во-вторых, объемы торгов токенизированных стартапов на основе акций (например, через Robinhood Ventures и PreStocks) обычно выше, чем на соответствующих платформах с перпетуальными контрактами. Отчасти это может быть связано просто с преимуществами дистрибуции Robinhood как платформы и консервативной стратегией TradeXYZ по выпуску перпетуальных контрактов по одному.

Стоит отметить, что перпетуальный контракт TradeXYZ для Cerebras Systems достиг огромного успеха, с дневным объемом торгов более 30 миллионов долларов и предоставлением точного ценового обнаружения с погрешностью менее 3% от цены размещения.

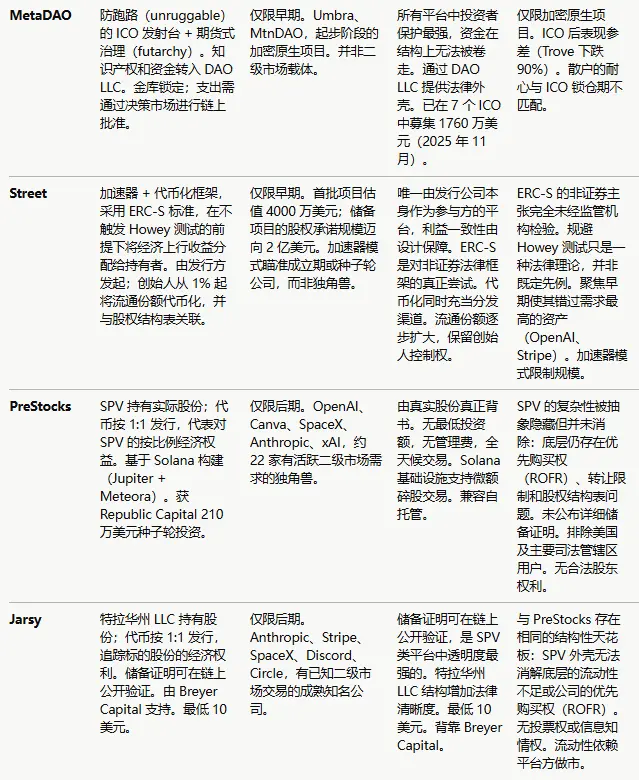

В-третьих, во всем этом ландшафте наблюдается сильный степенной закон концентрации, где объемы торгов платформы, как правило, определяются менее чем тремя активами. Например, объемы торгов MetaDAO определяются META, Avici и Umbra; объемы Street определяются KLED.

В настоящее время (по состоянию на 30 мая 2026 года) TradeXYZ предлагает только пары для торгов, связанные с SpaceX, а SpaceX также составляет около половины еженедельного объема торгов PreStock. Этот огромный степенной эффект может указывать на то, что для большинства платформ трейдеры более лояльны к высококачественным активам с высокой известностью, чем к самой базовой платформе.

2.2 Архитектура проектного дизайна

Мы также можем глубже изучить отдельные проекты на этой карте ландшафта, чтобы внимательно рассмотреть компромиссы различных схем дизайна в этой области, от перпетуального доступа до структур капитала, поддерживаемых SPV.

Примечание: Сравнение платформ и описание характеристик в этом анализе представляют точку зрения автора на основе общедоступной информации по состоянию на 30 мая 2026 года. Описание сильных и слабых сторон платформ не является инвестиционной рекомендацией.

Часть третья: Вызовы и возможности для токенизированных стартапов

Сегодня токенизированные стартапы все еще находятся в зачаточном состоянии, и их пространство дизайна полно возможностей и вызовов.

3.1 Согласие на передачу акций и выравнивание интересов команды

В настоящее время одним из самых насущных вопросов для платформ токенизированных стартапов на споте является то, соответствуют ли эти проекты интересам учредительских команд или противоречат им, особенно учитывая, что объемы торгов на платформах непропорционально сосредоточены на 1-3 качественных активах.

Это особенно верно для таких высокопрофильных пред-IPO компаний, как SpaceX, Anthropic и OpenAI, на которые приходится большая часть пред-рыночного спроса и объемов торгов.

Без согласия команды компания может публично выступить против токенизации, что приведет к аннулированию продаж и последующему резкому падению стоимости токена, как показали случаи с выступлением Anthropic против SPV вторичного рынка и OpenAI против сток-токенов Robinhood.

Обычно у компаний на стадии роста есть четыре явных мотива для выхода на публичный рынок: (1) доступ к капиталу на публичных рынках; (2) определение цены в реальном времени; (3) обеспечение ликвидного выхода для учредительской команды и инвесторов; (4) сигнал престижа.

Сегодня взрывной рост «мега-фондов» на стадии роста обеспечивает чрезвычайно устойчивую и обильную среду финансирования для самых горячих стартапов, обычно с очень высокими оценками. Этот ландшафт ослабил мотивы (1) и (2) для компаний на стадии роста для проведения публичного размещения: им больше не нужно обращаться к публичным рынкам для привлечения капитала, а определение цены в реальном времени несет в себе риск корректировки цены в сторону понижения.

Таким образом, в сегодняшней среде финансирования горячий стартап на стадии роста будет рассматривать выход на публичный рынок только в том случае, если большое количество ранних сотрудников и инвесторов стремится к немедленной ликвидности (например, как Facebook при выходе на IPO в 2012 году) или если это рассматривается как символ зрелости, представляющий престиж.

Для платформы токенизированных стартапов на споте, которая хочет получить одобрение совета директоров и предоставить канал прямого владения акциями в текущей среде финансирования, последние два мотива имеют гораздо больший вес.

Традиционные брокеры вторичного рынка, такие как Forge и Hiive, больше ориентированы на мотив ликвидности, тогда как высокопрофильные закрытые фонды, такие как Robinhood Ventures и USVC, можно сказать, ориентированы на мотив престижа.

Тем не менее, помимо традиционных мотивов для выхода на IPO, появился ряд новых конструкций, таких как корзины токенизированных стартапов, модель токенизированного акселератора и выпуск токенизированного сообщества, которые могут решить эту проблему выравнивания интересов основателей:

Корзины токенизированных стартапов относятся к торгуемому портфелю стартапов на стадии роста, а не к отдельной токенизированной компании.

Это путь, который предлагают такие закрытые фонды, как Robinhood Ventures. Этот механизм может удовлетворить мотивы ликвидности, престижа и даже привлечения капитала, одновременно смягчая давление на переоценку в сторону понижения из-за «ценообразования в реальном времени» за счет использования мультипликаторов чистой стоимости активов (NAV) (отчасти похоже на DAT).

Модель токенизированного акселератора применяет традиционную модель акселератора и инкубатора (например, YC, HF0, South Park Commons), помогая стартапам вырасти с 0 до 1 в обмен на их согласие на токенизацию акций.

Мы видим, что такие платформы для выпуска, как Street и MetaDAO, эффективно предоставляют эту модель; они решают проблему выравнивания интересов основателей, становясь на сторону основателей и фактически помогая им расти.

Выпуск токенизированного сообщества, возможно, является самой интересной и достойной исследования моделью токенизированных стартапов. Как показал эирдроп Uniswap в 2020 году, токены могут стать отличным стимулом для обычных пользователей, ежедневно использующих продукт.

При правильной реализации эирдроп токенов может снизить стоимость привлечения клиента (CAC) за счет субсидирования естественной пользовательской активности, содействия маркетингу проекта и повышения удовлетворенности пользователей, особенно для проектов, ориентированных на потребителя.

Например, Revolut провела раунд финансирования акционерного капитала сообщества, привлекая 1,3 миллиона долларов от ранних пользователей при оценке в 40 миллионов долларов. Это также выполняло маркетинговую функцию, превращая пользователей в владельцев и сторонников, при этом ранние сторонники получили 400-кратную отдачу.

Однако эирдроп токенов также может быть обоюдоострым оружием; многие эирдропы криптопроектов страдали от фарминга, обвинений во внутренних долях и мгновенного давления продаж.

3.2 Неамериканские юрисдикции

Другой путь обхода проблемы согласованности с основателями — это выход на глобальный уровень. Многие текущие дискуссии вокруг токенизированных стартапов (и их объемов торгов) принимают американоцентричную перспективу, фокусируясь на самых горячих американских компаниях и предполагая проведение публичного размещения на американском рынке.

Но американские публичные и частные рынки капитала уже отлично обслуживают компании на стадии роста, что затрудняет обоснование дополнительных преимуществ токенизированного выпуска для компаний.

Однако в других регионах это может быть не так, и местные рынки капитала могут быть неэффективными, не предлагая оптимальной ликвидности или ценообразования для самых быстрорастущих компаний. Например, Wise изначально была зарегистрирована на Лондонской фондовой бирже в 2021 году.

Но в мае 2026 года она перенесла основное место листинга на американский NASDAQ, полагая, что это привлечет более ликвидный рынок, обеспечит доступ к более широкому кругу розничных и институциональных инвесторов и даст более щедрые мультипликаторы оценки.

Это географическое расхождение в оценке и доступе к капиталу также очевидно в различиях мультипликаторов оценки между американскими и китайскими компаниями в области искусственного интеллекта.

Ведущие американские компании в области ИИ обычно имеют мультипликаторы цены к выручке от 15 до 40, в то время как китайские компании в области ИИ имеют гораздо более консервативные мультипликаторы, близкие к 5-15. Эта скидка частично может быть отнесена к способности привлечения капитала; доступ к китайским рынкам капитала обычно сложнее, чем к американским.

Это географическое арбитражное ценообразование становится особенно интересным по мере того, как различные части цепочек поставок в таких передовых областях, как искусственный интеллект, робототехника, полупроводники и биотехнологии, рассредоточены по всему миру, а соответствующие компании выходят на рынки Азии и Европы.

Несмотря на это структурное преимущество неамериканских юрисдикций в отношении токенизированных стартапов, текущие эмпирические эксперименты и объемы торгов по-прежнему ограничены. Возможно, это связано с трудностью найти стартапы с высоким спросом, готовые экспериментировать со своей таблицей капитализации, а также со сложной местной нормативной средой в отношении иностранных инвестиций и токенизации.

Южная Корея является особенно интересным неамериканским рынком для токенизированных стартапов.

Южная Корея имеет:

(1) Несколько национальных лидеров в цепочке поставок ИИ с глобальным спросом инвесторов, таких как Samsung и SK Hynix

(2) Новую правовую базу для «сток-токенов»;

(3) Брокеров, активно интересующихся пред-IPO инвестициями;

(4) Больше инвесторов в криптовалюты, чем в акции.

Возможно, это отчасти объясняет, почему TradeXYZ активно начал размещать перпетуальные контракты на корейских акциях.

Одним из самых больших преимуществ токенизации является ее способность к географическому арбитражу, предоставляя глобальной аудитории базовый канал для инвестиций в компании по всему миру.

Платформы токенизированных стартапов с их глобальной базой ликвидности и потенциалом открытия для более широкого круга розничных и институциональных инвесторов, скорее всего, станут частью стратегии выхода на следующий уровень для быстрорастущих компаний за пределами США, подобных Wise, у которых нет сильных местных рынков капитала.

3.3 Дизайн ценового обнаружения для перпетуальных контрактов

Другой путь для платформ токенизированных стартапов — это использование стратегии перпетуальных контрактов. Если у вас есть только синтетический инструмент, который не представляет собой базовые акции, то у совета директоров нечего аннулировать. Это обходит необходимость вмешательства команды и согласия совета директоров. Однако, избегая проблемы легитимности, синтетические активы сталкиваются с проблемой ценового обнаружения.

Существующие рынки перпетуальных контрактов (например, для криптотокенов, акций и сырьевых товаров) обычно полагаются на ликвидный спотовый рынок и надежные ценовые оракулы для управления ставками финансирования и синтетическими ценами. Однако, по определению, у частных стартапов нет ликвидного публичного рынка.

Ближайшим доступным рынком являются тендеры и покупки на вторичном рынке, которые такие платформы, как Ventuals, используют для привязки своих ставок финансирования. Но они обычно ненадежны и часто недооценивают цену базового актива.

Например, на Ventuals ставка финансирования в пределах 5% от цены оракула составляет около 15% годовых, за пределами этого диапазона она растет по экспоненциальной кривой, налагая карательные сборы на покупателей с длинной позицией.

TradeXYZ использует противоположный подход, полагаясь на механизм ценового обнаружения без оракулов. Например, при размещении Cerebras Systems, TradeXYZ просто установил механизм Hyperp, использующий последние рыночные котировки для выведения справочной цены, позволяя контракту самостоятельно обнаруживать цену в узком временном окне между подачей документа S-1 и фактическим листингом. Он показал себя лучше, чем любой другой механизм на рынке.

Перпетуальный контракт CBRS был запущен 1 мая со справочной ценой в 175 долларов, в течение двух недель торговался стабильно в диапазоне от 288 до 320 долларов, достигнув около 340 долларов за час до открытия, что было менее чем на 3% ниже фактической цены открытия NASDAQ в 350 долларов.

Эта оценочная цена была примерно на 84% выше цены размещения инвестиционных банков в 185 долларов и намного точнее, чем цены брокеров вторичного рынка, таких как Hiive (225 долларов) и Forge (113,50 долларов). Это ярко демонстрирует огромный успех перпетуального контракта как инструмента.

Однако этот процесс не обязательно масштабируем, поскольку четкое ценовое обнаружение зависит от предстоящего, проверяемого события конвергенции. Если бы Cerebras не завершила листинг в определенный период времени, контракт был бы рассчитан по взвешенному по времени среднему значению его собственной цены.

В этом смысле механизм «ценового обнаружения перпетуальных контрактов» в конечном итоге больше похож на традиционные фьючерсные контракты и не обязательно применим к ранним активам, которые не собираются проводить публичное размещение в ближайшее время.

Таким образом, пространство дизайна токенизированных стартапов на основе перпетуальных контрактов по-прежнему очень обширно. Масштабируемая модель еще не установлена, и она, вероятно, будет представлять собой гибрид крипто-перпетуальных контрактов с традиционными фьючерсами, рынками предсказаний, вторичными спотовыми рынками, контрактами на разницу цен (CFD) и другими примитивами.

С недавним выходом Kalshi на рынок перпетуальных контрактов и появлением Hyperliquid с HIP-4 на рынках предсказаний исходов, мы видим важное сближение между всеми этими различными инструментами ценообразования. Ценообразование пред-IPO стартапов, вероятно, станет катализатором для создания нового типа пространства деривативов, более эффективного и удобного для обычных пользователей.

3.4 Правовая структура и регулирование

С точки зрения правовой структуры, многие из этих инструментов токенизированных стартапов, такие как ERC-S от Street, DAO LLC от MetaDAO и токены, поддерживаемые SPV, все еще являются новыми, экспериментальными инструментами, которые не выдержали испытания временем со стороны регулирующих органов, имеющих строгие намерения по обеспечению соблюдения.

Даже недавний американский «Закон о ясности» в отношении цифровых товаров не решил эту проблему для токенизированных акций.

Судя по публичным заявлениям, Комиссия по ценным бумагам и биржам США, по-видимому, делит эти токенизированные стартапы на две разные категории в зависимости от того, выпущены ли токены непосредственно компанией или третьей стороной.

Токены, спонсируемые эмитентом, сами по себе являются ценными бумагами, просто в другой форме, и поэтому подпадают под действие традиционного законодательства о ценных бумагах. Независимо от того, находится ли официальный реестр в ончейне (передача токена означает передачу акции) или офчейне (токен запускает обновление реестра), с ним обращаются точно так же, как с обычными акциями: он должен быть зарегистрирован или соответствовать исключениям, со всеми стандартными обязательствами по раскрытию информации и отчетности.

Токены третьих сторон обрабатываются в зависимости от того, что они фактически передают. Кастодиальные токены — это права на ценные бумаги в соответствии со статьей 8 Единого торгового кодекса США, то есть реальная сделка с ценными бумагами, но это право требования на акции, находящиеся у кастодиана, а не сами акции, что означает, что вы также берете на себя риск банкротства кастодиана.

Синтетические токены — это полностью независимые ценные бумаги, выпущенные третьей стороной, не предоставляющие никаких прав в отношении референтной компании, и они требуют отдельной регистрации или получения исключения: привязанные ценные бумаги (ноты или SPV, отслеживающие стоимость цели) относятся к этой категории; а свопы на основе ценных бумаг (например, перпетуальные контракты в стиле Ventuals) наиболее ограничены, запрещая продажу обычным американским розничным инвесторам, если они не зарегистрированы и не торгуются на национальной бирже.

Заключение

Будь то пред-IPO перпетуальные контракты, SPV, закрытые фонды или тендеры вторичного рынка, каждый инструмент пытается вернуть возможность, которую публичные рынки когда-то давали массам бесплатно: возможность получить ранний, ликвидный доступ к инвестициям в период наивысшего роста компании, вместо того чтобы позволить его монополизировать фондам роста.

Сегодня мы знаем, что этот спрос реален, но инфраструктура все еще находится в стадии разработки. Для токенов значение еще глубже. Последние несколько лет стали кризисом идентичности: токены проектов стали гражданами второго сорта, управление превратилось в пустую формальность, а стоимость накапливалась в другом месте.

Переосмысление механизма выпуска, наделение токенов реальным правом требования на рост венчурного масштаба, возможно, является миссией эпохи, которая может их освободить. Обладая инфраструктурой, которой никогда не было у первой волны, токены, возможно, смогут выполнить свое основное видение, которое они обещали в свои ранние, полные энтузиазма дни.