Автор: Гу Юй, ChainCatcher

Долгое время Paradigm была знаковой венчурной компанией в криптоиндустрии, олицетворяя высший стиль инвестирования и эстетику в отрасли, а её исследовательский подход к крипто-ВК высоко ценился. Однако под влиянием цикличности отрасли, в нынешний период всеобщего спада венчурного капитала, Paradigm также не избежала трудностей, одним из проявлений которых стала беспрецедентная волна уходов высшего руководства: с апреля этого года по крайней мере 7 сотрудников покинули компанию, включая нескольких партнёров.

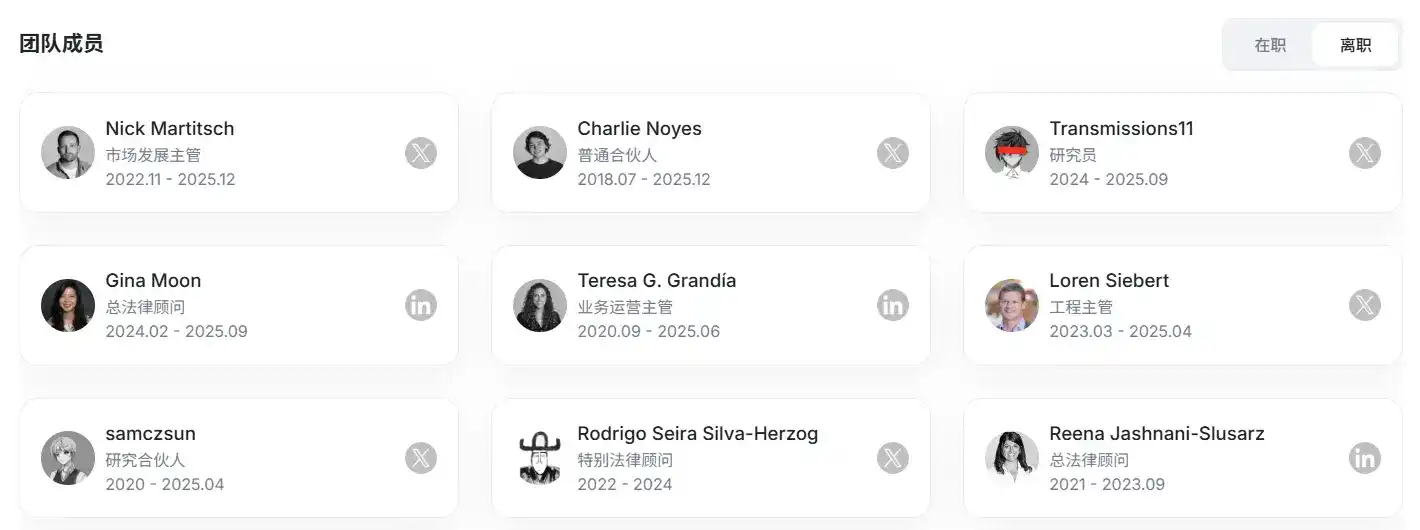

В декабре первый сотрудник Paradigm, генеральный партнёр Чарли Нойес, а также руководитель по развитию рынка Paradigm Ник Мартич подряд объявили об уходе.

В сентябре главный юрисконсульт Paradigm Джина Мун и исследователь Paradigm Transmissions11 уволились.

В июне руководитель операционной деятельности Paradigm Тереза Г. Грандиа уволилась.

В апреле инженерный руководитель Paradigm Лорен Зиберт и исследовательский партнёр samczsun подряд уволились.

Источник: RootData

Такая волна уходов крайне редка даже среди ведущих ВК, что отражает, что Paradigm переживает довольно трудный этап. Судя по публичному портфелю и частоте сделок, инвестиционная активность Paradigm за последние два-три года заметно снизилась, при этом не хватает «образцовых работ», получивших отраслевое признание, и упущено множество проектов с высокой доходностью, что, вероятно, является основным источником трудностей Paradigm.

Постоянные переплаты, упущенные звездные объекты

Золотой век Paradigm пришелся примерно на 2019-2021 годы. На этом этапе она завершила развертывание ключевых проектов, таких как Uniswap, Optimism, Lido, Flashbots, и благодаря этому создала яркий бренд: технологическая инфраструктура,核心 экосистема Ethereum, долгосрочный подход, что также принесло Paradigm немалую репутацию в кругах крипто-предпринимателей и инвесторов.

Эти типичные инвестиции имеют несколько общих характеристик: это не краткосрочные тренды, а базовые протоколы или ключевые промежуточные слои; точка инвестирования относительно ранняя, но не экстремально;高度 соответствует внутренним исследовательским направлениям Paradigm.

Именно на этом этапе Paradigm сформировала четкую и неоднократно подчеркиваемую инвестиционную стратегию: исследовательский подход. Но проблема в том, что эта методология в последующих циклах, столкнувшись с быстрыми изменениями отраслевой логики, постепенно показала недостаточную адаптивность, что также привело к заметному разрыву между инвестиционными показателями и влиянием Paradigm.

С 2022 года новые высокорослые проекты начали появляться больше на уровне приложений, финансовых структурных инноваций, дизайна механизмов и пользовательского опыта, например,预测 рынки, протоколы структуры доходности, протоколы perpetual контрактов. Эти проекты往往 быстро итератируют, более ориентированы на продукт, более терпимы к «технической корректности» и более чувствительны к «росту пользователей» и «эффективности механизмов».

В прошлом цикле Paradigm ярко поддержала и инвестировала в два хит-проекта, Blur и Friend.tech, став одним из главных двигателей их популярности, но оба после выпуска токенов быстро пришли в упадок, команды массово продавали токены и постепенно стали неактивны, что заставило рынок усомниться в инвестиционном чутье и стиле Paradigm.

В то же время Paradigm также переплатила за последующие раунды финансирования многих проектов с высокой оценкой. Хотя эта стратегия в условиях бычьего рынка ранее приносила Paradigm значительную прибыль, из-за持续低迷 рынка альткойнов, а также проблем самих инвестиционных объектов, ключевые проекты Paradigm почти все после выпуска токенов быстро падали ниже их себестоимости или развивались плохо, пытаясь转型.

В мае 2024 года Paradigm возглавила раунд A финансирования Farcaster на 150 миллионов долларов с оценкой в 1 миллиард долларов, а теперь Farcaster объявила об отказе от социального направления и переходе в сферу кошельков.

В мае 2024 года Paradigm возглавила финансирование Babylon на 70 миллионов долларов с оценкой в 800 миллионов долларов, а теперь FDV токена Babylon составляет всего 180 миллионов долларов.

В апреле 2024 года Paradigm возглавила финансирование Monad на 225 миллионов долларов с оценкой в 3 миллиарда долларов, а теперь FDV токена Monad составляет всего 1,7 миллиарда долларов.

В июне 2022 года Paradigm участвовала в финансировании Magic Eden на 130 миллионов долларов с оценкой в 1,6 миллиарда долларов, а теперь FDV токена Magic Eden составляет всего 200 миллионов долларов.

Для Paradigm еще более неприемлемо то, что она также упустила ранние инвестиции во многие проекты с высокой доходностью за последние годы, такие как Ethena, Pump.fun, Ondo Finance, MYX и другие. В热门 секторах деривативов и RWA за последние годы Paradigm не инвестировала ни в один объект.

А в预测 рынках, наиболее favored капиталом в криптоиндустрии за эти годы, хотя Paradigm еще в январе 2019 года инвестировала в预测 рынок проект Veil, тот проработал менее года и宣布 прекращение работы.

Модель预测 рынков теоретически не нова, техническая сложность также не высока, неудачный инвестиционный опыт привел к тому, что Paradigm не участвовала в первых пяти раундах финансирования Polymarket. Возможно, только в январе этого года, когда Polymarket с оценкой в 1,2 миллиарда долларов объявила о завершении финансирования на 150 миллионов долларов, Paradigm осознала ценность этого направления и转而 начала делать крупные ставки на конкурента Polymarket, Kalshi, сначала в июне возглавив его финансирование на 185 миллионов долларов с оценкой в 2 миллиарда долларов, а затем в течение полугода подряд участвуя в двух раундах финансирования с оценками в 5 миллиардов и 11 миллиардов долларов. Это также проект с самой высокой оценкой, в который Paradigm когда-либо инвестировала.

Из этого видно, что Paradigm уже решила не упускать ключевые инвестиционные объекты в самых热门 секторах, даже до степени наличия менталитета «fomo».

Инкубация搁浅

Глубокое участие в инкубации проектов长期以来 также является标志性 стилем Paradigm, Uniswap и Flashbots являются репрезентативными кейсами предыдущих циклов.

В ранее опубликованной Paradigm статье компания заявила, что Paradigm — это группа разработчиков, цель которой — поддерживать других разработчиков. Наиболее продуктивное сотрудничество часто заключается в тесной работе со стартап-командами для совместного решения важных бизнес- и исследовательских проблем.

Для ВК加入 на этапе, когда проект еще находится в стадии концепции, позволяет лучше влиять на дизайн продукта и стратегическое направление, высвобождая thus больший потенциал стоимости и получая более высокую переговорную силу и доходность на инвестиционном уровне.

Имея несколько успешных кейсов, Paradigm в последние годы продолжала探索 модель инкубации и даже推出了 институционализированную модель EIR (Entrepreneurs-in-Residence), то есть совместная работа в офисе, где ВК предоставляет предпринимателям существенную поддержку в стратегии, технологиях, найме и т.д. Но, судя по последним нескольким案例, эта модель Paradigm также столкнулась с трудностями.

В декабре 2023 года Paradigm через механизм EIR совместно разработала платформу для разработчиков на блокчейне Shadow и инвестировала 9 миллионов долларов, но в этом году проект прекратил разработку, а основатели转而推出 платформу деривативов на акции непубличных компаний Ventuals.

Децентрализованный протокол фиксированных процентных ставок Yield Protocol, в написании白皮书, разработке и инвестировании которого ранее участвовала Paradigm, также в октябре 2023 года宣布 прекращение работы.

Затем Paradigm переключила цель на инфраструктурные направления. В октябре 2024 года крипто-венчурная компания Paradigm объявила об инвестициях в 20 миллионов долларов в свой спин-офф Ithaca. Ithaca разрабатывает новый блокчейн Layer 2 под названием Odyssey, технический директор и генеральный партнер Paradigm Георгиос Константопулос занял пост генерального директора Ithaca, сохранив при этом должность в Paradigm. Соучредитель Paradigm Мэтт Хуан стал председателем правления Ithaca.

Эта структура команды показывает, что Ithaca полностью разрабатывается核心 командой Paradigm, что означает более глубокое участие, чем в предыдущих проектах, таких как Uniswap. Выбор направления Layer2 в этот момент времени,现在看来, нельзя назвать明智ным выбором. В последующий год Ithaca на рынке практически не имела каких-либо重大动态.

В начале этого года отраслевой тренд в криптоиндустрии полностью сместился в сторону стейблкоинов и платежей, и Paradigm снова «понеслась за трендом», совместно с интернет-платежным гигантом Stripe в августе推出 высокопроизводительный публичный блокчейн Layer1 Tempo, ориентированный на платежные сценарии, соучредитель Paradigm Мэтт Хуан занял пост генерального директора проекта. В октябре Tempo приобрела Ithaca, все члены后者 присоединились к Tempo.

К этому времени в платежном направлении уже активно действовали такие серьезные проекты, как Arc, RedotPay, Plasma, Stable, 1Money, BVNK. Tempo лидировала по объему привлеченного финансирования и имела поддержку ресурсов Stripe, заняв较为领先 позицию в激烈竞争.

Платежная битва Tempo станет решающим сражением для Paradigm, чтобы вновь доказать свои продуктовые и исследовательские способности.

Заключение

Сможет ли Paradigm снова найти свой ритм, ответ еще предстоит проверить временем. Но можно с уверенностью сказать, что она уже находится на позиции, где必须 меняться.

С января этого года инвестиционная частота Paradigm заметно выросла, с в среднем 1 сделки в месяц в 2023-2024 годах до в среднем 2 сделок в месяц, при этом明显提升 доля инвестиций на ранних стадиях. В июне прошлого года Paradigm также объявила о завершении сбора фонда в 850 миллионов долларов, оставаясь одной из ВК с самым большим объемом наличных средств на руках.

Смена команды и неудачи инвестиционной стратегии — это не уникальная трудность какой-то одной ВК, а неизбежный путь, который проходят почти все долгосрочные институты в процессе развития, пересекающем циклы. Если прошлая Paradigm представляла «эпоху инженеров» криптоиндустрии, то теперь ей предстоит столкнуться, возможно, с более прагматичным этапом, более ориентированным на рыночные результаты. И успех этой корректировки также определит, сможет ли она в следующем цикле продолжать играть роль определяющего, а не наблюдающего.