Author: Claude, Shenchao TechFlow

Synopsis: The Wall Street Journal revealed the scale of wealth creation within OpenAI. In a staff stock sale last October, the company raised the personal cash-out limit from $10 million to $30 million. Over 600 current and former employees participated, cashing out a combined $6.6 billion, with approximately 75 individuals taking the full maximum amount. President Brockman confirmed in court this week that his stake is worth about $30 billion. Silicon Valley has never seen such a concentration of millionaires created by a private company before its IPO.

Image source: Wall Street Journal

In the past Silicon Valley, the typical path for ordinary employees to strike it rich was one: wait for the company to go public. OpenAI is rewriting that rule.

According to The Wall Street Journal, in an internal stock transaction completed last October, OpenAI allowed employees to sell up to $30 million in shares each. Over 600 current and former employees participated, cashing out approximately $6.6 billion in total. Informed sources revealed that about 75 of them took the full $30 million cap. This is the largest single employee stock sale event in the tech industry to date.

Cash-Out Cap Tripled, Driven by External Investor Demand

OpenAI originally set a single cash-out limit of $10 million for employees. However, due to external investor demand far exceeding expectations, the company tripled the cap to $30 million last fall.

The transaction was completed at a $500 billion valuation, with investors including Thrive Capital, SoftBank, Dragoneer Investment Group, Abu Dhabi's MGX, and T. Rowe Price. As previously reported by CNBC, OpenAI initially planned a sale of about $6 billion, later expanded to $10.3 billion, but the actual transaction ended up being around $6.6 billion. Internally, the lower participation rate was interpreted as a vote of confidence in the long-term prospects by employees.

According to OpenAI's rules, employees can sell shares after two years of service. This means many employees who joined after ChatGPT's launch at the end of 2022 had their first opportunity to cash in options in this transaction. The value of OpenAI's stock has increased over 100-fold in the past seven years.

Brockman Confirms $30 Billion Stake in Court, Musk's Lawyer Presses Relentlessly

The scale of wealth held by executives is even more staggering. According to NBC, OpenAI President and Co-founder Greg Brockman confirmed during testimony on May 4th that his current OpenAI equity is worth approximately $30 billion.

This figure was disclosed on the fourth day of the trial in Elon Musk's lawsuit against OpenAI. Musk's lawyer, Steven Molo, repeatedly referenced this number during over two hours of questioning, pressing Brockman on why he hadn't fulfilled a promised $100,000 donation while amassing a $30 billion fortune. According to CNBC, Brockman admitted, "It is true I ultimately did not make the donation."

As reported by Fortune, Musk's legal team also revealed multi-layered financial ties between Brockman and CEO Sam Altman: Altman provided Brockman with about $10 million in equity from his family office as early as 2017; Brockman also holds stakes in AI chip startup Cerebras and nuclear fusion company Helion Energy. OpenAI had previously discussed acquiring Cerebras, and Altman has invested hundreds of millions in Helion. Musk's side argues these cross-holdings compromised Brockman's independence as a fiduciary.

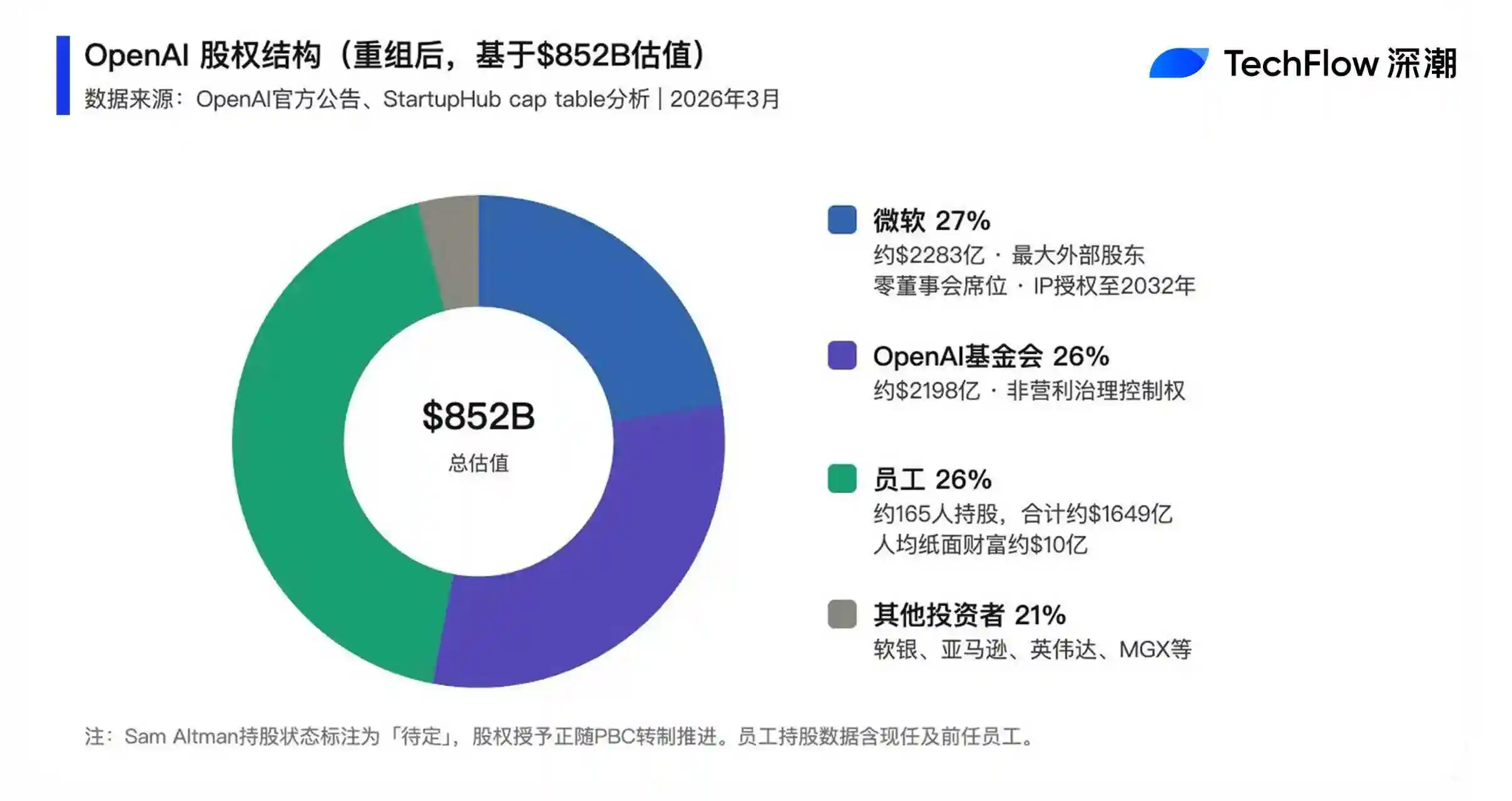

Employees Hold 26% Stake, Average Paper Wealth Exceeds Returns of Most VC Funds

Following the company restructuring completed last October, OpenAI employees collectively hold about 26% of the company's equity.

According to an analysis by StartupHub, approximately 165 current and former employees collectively hold equity worth about $164.9 billion, averaging nearly $1 billion in paper wealth per person. This exceeds the total lifetime returns of most venture capital funds.

According to an analysis by The Wall Street Journal and data firm Equilar, OpenAI's per capita stock-based compensation in 2025 is about $1.5 million. This is over 7 times the figure for Google before its 2004 IPO, and 34 times the average for 18 large tech companies in the year before their IPOs over the past 25 years.

The company's equity-based compensation expense constitutes nearly half of its projected revenue, far surpassing peers like Palantir, Meta, and Salesforce.

$852 Billion Valuation, Trillion-Dollar IPO on Horizon, Wealth Creation Far From Over

OpenAI completed a $122 billion financing round on March 31st this year at an $852 billion valuation, setting a new record for the largest single private funding round in Silicon Valley history. Amazon led the investment with $50 billion, while Nvidia and SoftBank each invested $30 billion. The company's current monthly revenue is $2 billion, with over 900 million weekly active ChatGPT users and more than 50 million paid subscribers.

According to multiple media reports, OpenAI is preparing for an IPO in the fourth quarter of 2026, with a target valuation potentially reaching $1 trillion. If successful, this would become one of the largest tech IPOs in history. CFO Sarah Friar previously stated at Davos that the company plans to allocate a portion of the IPO shares to retail investors.