Автор: RoboRhythms

Компиляция: Deep Tide TechFlow

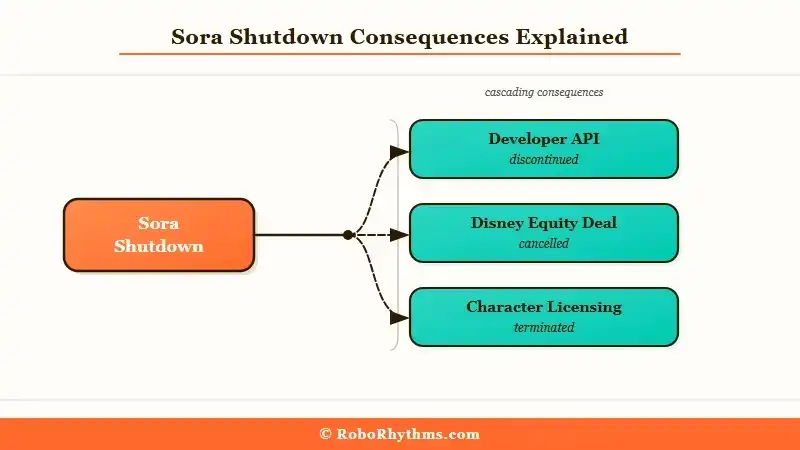

Введение от Deep Tide: 24 марта 2026 года OpenAI единовременно закрыл приложение Sora, его API и домен. Трехлетнее лицензионное соглашение с Disney и инвестиции в $1 млрд рухнули.

Первой реакцией технического сообщества была не скорбь, а вопрос: "А кто-нибудь вообще этим пользовался?" — эта фраза говорит больше любого официального заявления. Runway, Kling и Google Veo теперь остаются единственными реальными игроками на поле AI-видео.

Полный текст:

Продукт, который должен был вывести генерацию AI-видео в массы, исчез. OpenAI закрыл Sora 24 марта 2026 года, одновременно отключив самостоятельное приложение, API и домен sora.com, всего через примерно шесть месяцев после его громкого публичного анонса.

Момент выбран крайне неудачный. В декабре 2025 года Disney подписала трехлетнее лицензионное соглашение, предоставив OpenAI права на использование таких знаковых персонажей, как Микки Маус и Золушка, для генерации контента в Sora, и планировала инвестировать в OpenAI $1 млрд.

Теперь все это отменено.

Мне кажется, наиболее показательной была реакция tech-сообщества: основным настроением была не скорбь, а вопрос: "А кто-нибудь вообще этим пользовался?" Эта фраза правдивее любого официального заявления раскрывает реальное положение дел с продуктом.

Если вы использовали Sora или планировали создавать продукты на основе его API, вот что вам нужно знать.

Что именно произошло

Закрытие Sora — это полное прекращение продукта, затрагивающее приложение, API для разработчиков и домен sora.com.

OpenAI подтвердил 24 марта, что вся продуктовая линейка Sora будет полностью закрыта. Это не трансформация, не ребрендинг и не поглощение другим продуктом.

Приложения больше нет, API отключается, домен sora.com снимается с обслуживания.

Вот что было прекращено полностью:

- Потребительское приложение Sora (генерация видео из текста)

- Sora API (доступ для разработчиков и предприятий)

- Веб-сайт sora.com

Планировавшиеся инвестиции Disney в акционерный капитал OpenAI на $1 млрд

Объявленное в декабре 2025 года трехлетнее соглашение Disney о лицензировании персонажей

История с Disney — не просто сноска. Сделка в $1 млрд, рухнувшая в течение трех месяцев после анонса, говорит о том, что отношения усложнились еще до официального объявления о закрытии.

Variety и Bloomberg подтвердили, что сделка была напрямую отменена в связи с прекращением работы Sora.

От Sora осталась лишь часть: внутренняя исследовательская команда продолжает работу над тем, что OpenAI называет исследованием "симуляции мира", в направлении применения в робототехнике.

Этот проект не имеет ничего общего с видеопродуктом, которым вы, возможно, пользовались. OpenAI четко позиционирует это как инфраструктурное исследование, а не будущий потребительский продукт.

Это также соответствует закономерности, о которой я ранее сообщал. OpenAI имеет историю прекращения продуктов, которые больше не соответствуют его доходной дорожной карте, и этот временной узел — перед планируемым IPO — следует той же логике.

Почему это серьезнее, чем кажется

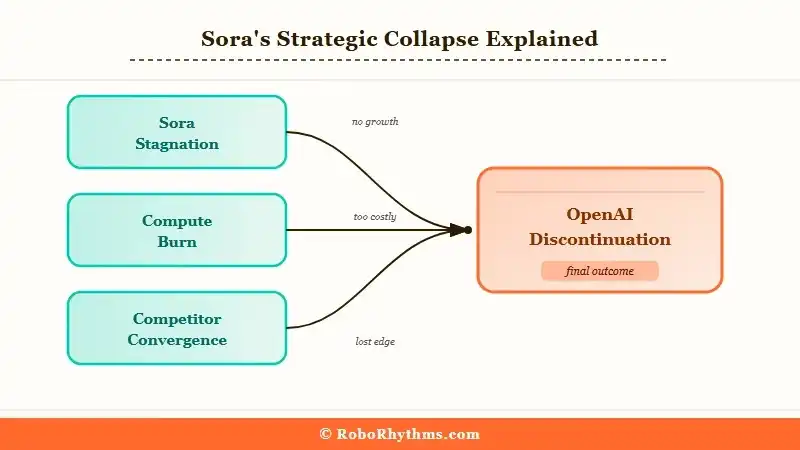

Закрытие Sora — это не просто провал продукта, а публичное признание OpenAI, что оно уступает целую категорию AI тем конкурентам, которых оно презирало при запуске.

Когда Sora впервые появился в 2024 году, демо было ошеломляющим. Посты на r/singularity набирали сотни тысяч просмотров, и普遍 считалось, что OpenAI снова в одночасье обошел всех конкурентов.

Runway, Pika и Kling должны были стать неактуальными.

Но затем публично запущенный продукт застопорился. Runway Gen-4 продолжал итеративно поставлять обновления, Kling 3.0 от Kuaishou сокращал разрыв в качестве быстрее, чем ожидало большинство аналитиков.

Google Veo накопил преимущество в вычислительной мощности, с которым OpenAI на этом непрофильном доходном направлении было трудно соперничать.

Затраты на вычисления — самая шокирующая цифра. По оценкам аналитиков, Sora в пиковые периоды использования потреблял около $15 млн в день на вычисления.

Для компании, сфокусированной на предIPO финансовом состоянии, эту статью расходов было крайне сложно оправдать, когда модели, реально приносящие доход (серия GPT-5, API оператора, корпоративные контракты), сами требуют больше инвестиций.

Была и проблема дипфейков. TechCrunch в своем репортаже о закрытии назвал Sora "самым тревожным приложением на вашем телефоне", ссылаясь на функцию камео, позволявшую пользователям помещать реальных людей в AI-генерируемые сцены.

Вызванный этой функцией backlash был достаточно серьезным, и, на мой взгляд, созданная ею репутационная нагрузка сделала решение о закрытии более легким, чем оно могло бы быть.

Отраслевое влияние теперь очевидно: Runway, Kling и Google Veo — настоящие игроки в сфере AI-видео. Неопределенность стратегии, которую присутствие OpenAI создавало для каждого конкурента, теперь устранена.

Что это значит для вас

Если вы использовали Sora или подключались к его API, вам нужно действовать немедленно. Временные рамки закрытия — мгновенные.

Три инструмента, которые сейчас лучше всего могут принять исходную пользовательскую базу Sora:

Runway Gen-4 — наиболее близок по техническим характеристикам к кинематографическим quality-целям Sora, имеет зрелый API и активное сообщество разработчиков. Наиболее подходит для профессионального производства длинных видео.

Kling 3.0 — модель от Kuaishou стала фаворитом сообщества по реалистичности движений и наиболее рекомендуемым инструментом в дискуссиях о миграции бывших пользователей Sora. Доступен API для разработчиков.

Pika 2.0 — быстрее, дешевле и проще в использовании, чем два вышеупомянутых. Тарифы начинаются примерно с $8 в месяц. Наиболее подходит для создателей контента, prioritizing скорость над кинематографическим quality.

Если ваш основной сценарий использования — это видео с виртуальными аватарами или говорящими головами, а не чисто генеративная графика, выбор инструментов будет другим.

Что произойдет дальше

Рынок AI-видео ждет консолидация, и цены вырастут.

С уходом OpenAI, Runway, Kling и Google Veo больше не сталкиваются с рынком, где хорошо финансируемый новичок в любой момент может颠覆ить ценовые ожидания всех.

Это меняет бизнес-динамику для всех оставшихся игроков.

Мой прогноз на ближайшие шесть месяцев:

Runway повысит цены на подписки. С наплывом пользователей Sora спрос резко возрастет, а цены Runway всегда были ниже уровня, который могла бы поддерживать его конкурентная позиция. Ослабление угрозы со стороны OpenAI дает им четкое пространство для пересмотра цен.

Google Veo будет активнее продвигать потребительский продукт. Google до этого намеренно держал публичный запуск Veo в тени, теперь адресуемый рынок стал более четким. Ожидайте более заметного потребительского продукта к концу 2026 года.

Kling будет瞄准овать корпоративные контракты, освободившиеся после ухода Disney. Kuaishou一直将Kling打造为专业级产品。 Сделка OpenAI-Disney фактически блокировала некоторые корпоративные отношения, которые теперь вновь открыты.

Результат, который, я считаю, не произойдет: возвращение OpenAI в AI-видео в форме потребительского продукта. Внутренние сигналы указывают на то, что видео переклассифицировано как исследование инфраструктуры для робототехники, а окно для возвращения на рынок короче обычного цикла разработки компании.

Исходя из моего опыта наблюдения за каждой категорией AI, компания, которая в конечном итоге побеждает, — это та, которая со временем накапливает итерации, а не та, которая выпустила лучшее демо. Sora достиг пика на демо, Runway итерировала уже три года.

Часто задаваемые вопросы

Вопрос: Можно ли еще использовать приложение Sora по состоянию на март 2026 года?

С 24 марта 2026 года Sora начался процесс прекращения обслуживания. OpenAI не объявил конкретные окончательные даты доступа для всех пользователей, но процесс закрытия уже запущен. Не полагайтесь на его continued доступность для любой production-среды.

Вопрос: Какая лучшая замена Sora для разработчиков API?

Runway Gen-4 в настоящее время имеет самый зрелый и стабильный API для разработчиков среди инструментов AI-видео. Kling 3.0 также предоставляет доступ к API и широко рекомендуется в дискуссиях о миграции разработчиков. Рекомендуется протестировать оба, прежде чем полностью мигрировать.

Вопрос: Почему Disney отменила инвестиции в $1 млрд в OpenAI?

Инвестиции Disney и трехлетнее лицензионное соглашение были напрямую привязаны к продуктовой линейке Sora и включали права на использование персонажей Disney в AI-генерируемом видео. После прекращения работы Sora лицензионные условия потеряли основу. Обе стороны аннулировали сделку, согласно Bloomberg и Variety.

Вопрос: Что будет с внутренней исследовательской командой Sora в OpenAI?

Команда продолжает заниматься исследованием симуляции мира для робототехники. Эта работа не будет производить каких-либо видеопродуктов для потребителей или разработчиков. OpenAI позиционирует это как инфраструктурное исследование, а не часть продуктовой дорожной карты.

Вопрос: Означает ли это, что OpenAI сворачивает потребительские продукты в целом?

OpenAI четко дал понять, что ресурсы перед IPO будут сконцентрированы на корпоративном ПО, инструментах программирования и продуктах-агентах. Закрытие Sora напрямую соответствует этому направлению.

Вопрос: Является ли Google Veo теперь лучшей заменой Sora?

Veo технически силен, но для разработчиков и создателей контента Runway Gen-4 и Kling 3.0 в настоящее время более доступны и лучше поддерживаются. Для большинства пользователей, которым нужно мигрировать сегодня, Runway или Kling являются более практичным выбором.