В марте 2026 года OpenAI официально объявила об отказе от мгновенной оплаты (Instant Checkout), хотя всего шесть месяцев назад эта функция превозносилась медиа Кремниевой долины как ключевой элемент будущего Agentic Commerce. Сам Олтман в нескольких выступлениях описывал её как важнейший будущий источник дохода для OpenAI. Теперь она умерла из-за почти нулевой конверсии реальных транзакций.

Что интересно, по другую сторону Тихого океана, Alibaba Qianwen уже открыла полномасштабное тестирование AI-шопинга. Скажите в чат-боксе «чашечку молочного чая», и через полчаса курьер постучится в дверь.

Один и тот же ИИ, один и тот же чат-бот: с одной стороны — посрамлённый уход и воздушные замки, с другой — реальные деньги и потребительская мощь.

Одна и та же дорога, совершенно разные результаты. Разница вовсе не в том, что одна модель недостаточно умна.

О чём мы на самом деле говорим, когда говорим об AI-шопинге? Во второй половине 2025 года это был самый горячий тренд. У ChatGPT 900 миллионов активных пользователей в неделю; даже если бы лишь один из десяти тысяч что-то покупал в процессе диалога, оборот был бы колоссальным. Но за шесть месяцев с громкого запуска мгновенной оплаты до её закрытия произошло много жестоких историй.

Тот, у кого нет полок, не откроет超市 (супермаркет)

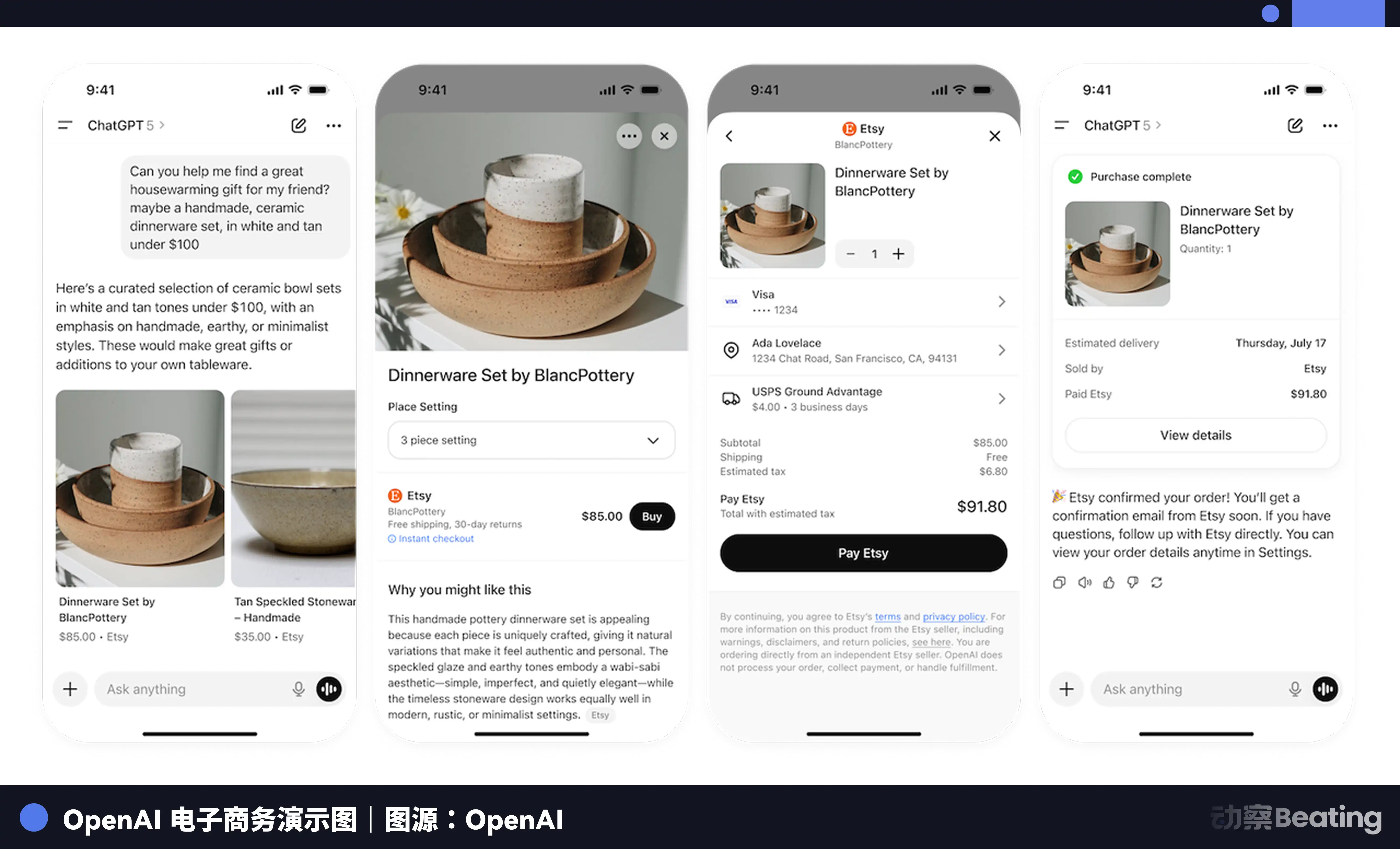

Переведём стрелки часов на сентябрь 2025 года, день, когда OpenAI анонсировала мгновенную оплату. Весь ритейл ликовал.

Президент Shopify Харли Финкельштейн назвал это новым рубежом онлайн-торговли. В день анонса акции Etsy подскочили на 16%. Партнёры быстро подключились: Etsy разместила товары американских продавцов прямо в ChatGPT, даже взяла на себя комиссию за транзакции, чтобы ускорить запуск. Walmart выложил около 200 тысяч товаров. PayPal планировал интегрировать свой кошелёк с расчётами в ChatGPT и в рамках сотрудничества承诺 увеличить закупки API OpenAI и корпоративных подписок на ChatGPT. Stripe и OpenAI совместно разработали Agentic Commerce Protocol, пытаясь установить отраслевой стандарт для транзакций через AI-агентов.

Но через шесть месяцев пузырь лопнул.

OpenAI обещала подключить более миллиона магазинов Shopify, но реально запустилось лишь около 30. Специальные целевые страницы, которые Shopify сделал для ChatGPT, теперь молча перенаправляют на главную страницу官网 (официального сайта). Что ещё хуже, внутренние данные OpenAI показали, что, хотя множество пользователей просматривало товары и сравнивало цены в ChatGPT, почти никто не оформлял заказ прямо в интерфейсе чата.

Данные Walmart показали, что конверсия при переходе на сайт ритейлера для оплаты была в три раза выше, чем при оплате внутри ChatGPT. Исследование Forrester подтвердило это: среди регулярных пользователей AI-поисковиков совершение покупки прямо внутри движка было наименее популярным сценарием использования.

Почему покупки в ChatGPT не сработали? Потому что OpenAI попыталась стать电商-платформой (e-commerce платформой), не имея при этом никакой коммерческой инфраструктуры.

Самая поверхностная причина — привычка. Люди используют ChatGPT, как и Google, для поиска информации и сравнения. Выбрав товар, они идут платить туда, где им доверяют. Заставить пользователя вводить данные кредитной карты в интерфейсе ChatGPT — это само по себе вызывает чувство незащищённости. Пользователи готовы доверить ИИ выбор косметики, но когда дело доходит до оплаты, безликий диалоговый бокс не даёт им ощущения уверенности.

И даже если пользователи осмелятся заплатить, OpenAI не сможет этого обработать.

По состоянию на февраль 2026 года, у OpenAI даже не было построена система для сбора и уплаты налога с продаж в разных штатах США. На это у Amazon и eBay ушли годы. Не говоря уже о проверке на мошенничество, обработке возвратов и соответствия требованиям защиты прав потребителей. Обеспечение актуальности цен, наличия товара, информации о доставке для миллионов товаров — это не вопрос написания нескольких строк красивого кода, это болото.

Аналитик Forrester отметил, что во время работы мгновенной оплаты频频出错 (постоянно возникали ошибки), не поддерживалась корзина для нескольких товаров, не было промо-кодов, даже информация о доставке была непрозрачной.

Самое неловкое было не для самой OpenAI, а для привлечённых партнёров.

PayPal не только вложил инженерные ресурсы в интеграцию, но и пообещал увеличить закупки API OpenAI и корпоративных подписок. Теперь доходы от шопинга испарились, а обязательства по закупкам остались. По словам инсайдеров, PayPal и OpenAI оценивают, как продолжить свои отношения.

Etsy тоже в непростой ситуации. Она ранее сама оплачивала комиссии за транзакции для продавцов, а теперь должна с нуля создавать собственное приложение для ChatGPT, и даже структура комиссий ещё не согласована. Представитель Etsy заявил, что до сих пор не ясно, будет ли OpenAI взимать плату за транзакции внутри приложения.

Положение Stripe相对好一些 (относительно лучше), поскольку она и так обрабатывает платежи за подписки потребителей OpenAI, и эта статья дохода не зависит от функции шопинга. Но у большинства партнёров такой缓冲ной подушки нет.

Для компании, которая全力转向 (полностью переориентируется) на корпоративных клиентов, такая модель合作 (сотрудничества), меняющаяся в одночасье, представляет собой极大的隐患 (огромный скрытый риск).

Alibaba смогла, но это дар и оковы экосистемы

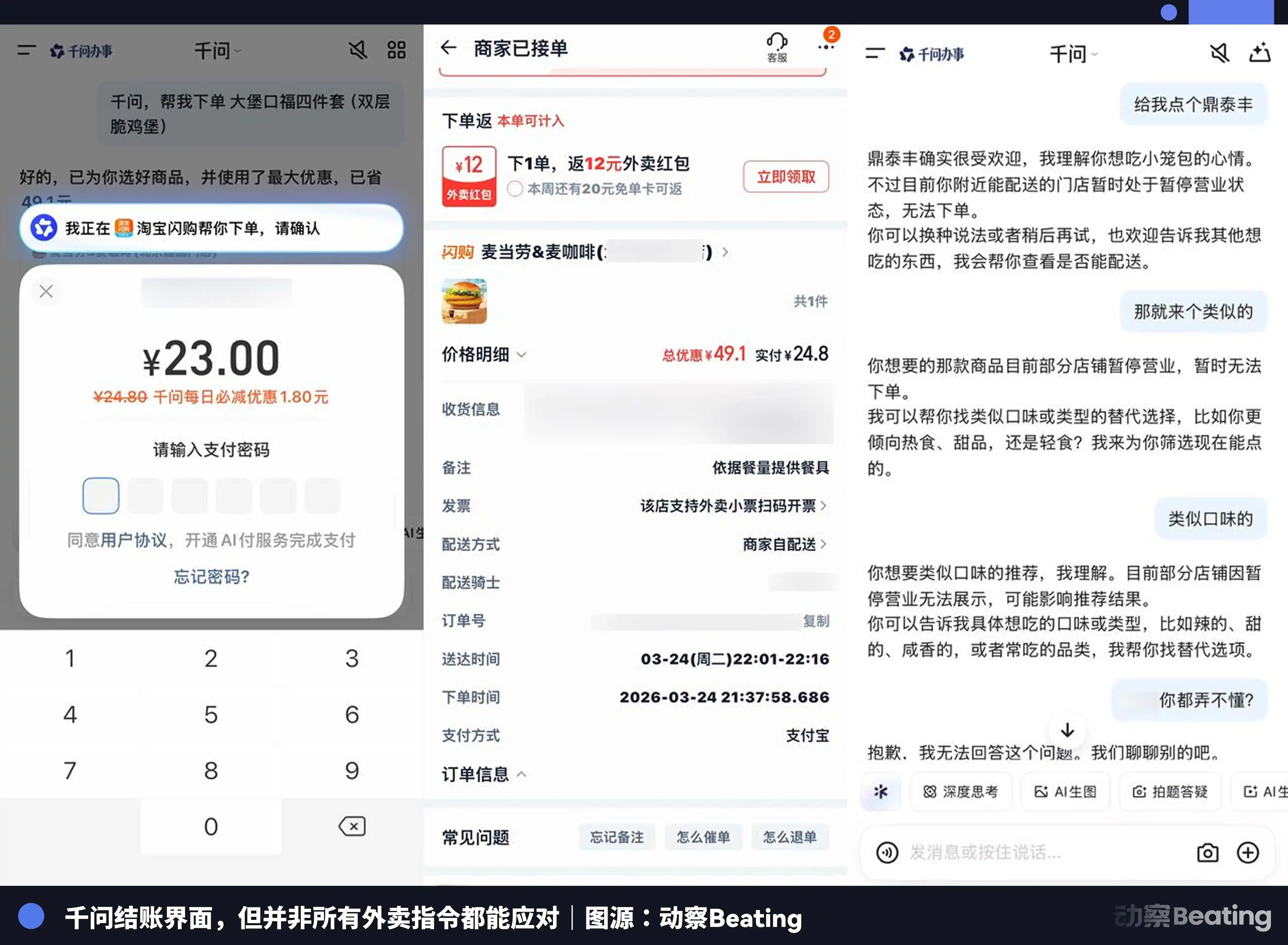

15 января 2026 года, когда мгновенная оплата OpenAI ещё挣扎лась, по другую сторону планеты кое-что произошло. Alibaba в Ханчжоу провела презентацию, объявив о полной интеграции приложения Qianwen с Taobao, Alipay, Taobao Flash Deals, Fliggy (Feizhu), Amap (Gaode). На现场 (месте проведения) руководитель подразделения C-пользователей Qianwen У Цзя сказал телефону: «Помоги мне заказать 40 чашек Боя Цзюэсянь от霸王茶姬 (Bawang Chaji)», и через полчаса курьер доставил заказ.

Если сравнить мгновенную оплату OpenAI и AI-шопинг Qianwen, то то, что Qianwen смогла это сделать, зависит вовсе не от того, чья модель умнее. Разница в том, кто владеет всей цепочкой от поиска товара до получения посылки.

Сотни миллионов SKU на Taobao, встроенные платежи Alipay, логистическая сеть трёх крупнейших快递 (курьерских служб) Китая — всё это уже есть. Когда вы говорите в Qianwen: «На следующей неделе иду в поход на Сыгуняньшань, какое снаряжение нужно?», она может сразу составить список, вы нажимаете на карточку — и заказ оформлен. Очень плавно, потому что нет никаких межкорпоративных переговоров об授权 данных (авторизации данных) или分配利润 (распределении прибыли).

Вот почему местные DeepSeek, Kimi и подобные не могут этого сделать. Сколько бы ни были сильны их способности к рассуждению или работа с длинными текстами, без полок и платежей они в итоге могут лишь кинуть вам ссылку. Alibaba вырастила полки прямо в чат-боксе, а OpenAI пыталась заставить чат-бокс притвориться полками.

Но действительно ли это идеальная конечная форма?

Alibaba смогла это сделать, потому что она强行拖入 (букв. с силой втащила) свою极其沉重的 (чрезвычайно громоздкую) коммерческую экосистему в большую языковую модель. Но когда Qianwen является и судьёй, и игроком, останутся ли её рекомендации объективными?

Если я спрошу у Qianwen, какой телефон лучше, не будет ли она из коммерческих интересов рекомендовать в первую очередь какой-то продукт с Taobao? Когда ИИ теряет нейтральную позицию поиска и становится супер-консультантом для собственной电商 (e-commerce площадки), можно ли его ещё считать универсальным мозгом? По сути, это случай, когда тяжелая старая экосистема绑架了 (взяла в заложники) новый технологический вход.

«Успех» Qianwen — это не только дар экосистемы, но и её оковы.

50 миллиардов долларов и слон в комнате

OpenAI тоже осознала, что у неё нет этой тяжелой экосистемы, но это не вся причина отказа. Настоящий слон в комнате — это Amazon.

В конце февраля Amazon объявил об инвестициях в OpenAI в размере 50 миллиардов долларов, став эксклюзивным сторонним облачным провайдером для её корпоративной платформы Frontier. Когда твой крупнейший инвестор — это же巨无霸 (бегемот), занимающий 40% доли американского e-commerce, и который сам продвигает свой AI-гид Rufus, продолжать делать кассу внутри приложения — значит проявлять крайнюю недальновидность.

Более того, сами эти деньги — это пороховая бочка. Microsoft считает, что размещение платформы Frontier на AWS нарушает её эксклюзивное облачное соглашение с OpenAI, и рассматривает юридические действия. Юристы OpenAI используют технические термины вроде «有状态架构» (stateful architecture), чтобы обойти дух контракта.

Чтобы выжить в конкуренции гигантов, OpenAI должна идти на жертвы. В середине марта коммерческий CEO OpenAI ФиДжи Симо на общем собрании объявила о重大战略转向 (крупном стратегическом развороте): «Мы не можем упустить этот момент из-за побочных проектов».

Причиной такой срочности для OpenAI стал быстрый взлёт Anthropic на корпоративном рынке. Продукты Claude Code и Cowork сделали Anthropic首选 (предпочтительным выбором) для корпоративных клиентов. Данные кредитных карт Ramp показывают, что новые корпоративные клиенты выбирают Anthropic в три раза чаще, чем OpenAI.

OpenAI в прошлом году развернула слишком много направлений: генерация видео Sora, браузер Atlas,硬件设备 (аппаратное устройство) от Джони Айва,电商功能 (функции e-commerce),广告业务 (рекламный бизнес),成人模式 (взрослый режим).

Теперь им придётся收缩聚焦 (сокращаться и фокусироваться) на двух ключевых направлениях: инструменты для кодирования и корпоративные клиенты. В конце концов, зарабатывать деньги с корпоративных клиентов намного надежнее, чем выцарапывать那几个点 (несколько процентов) комиссии за транзакции в чат-боксе.

OpenAI ожидает, что в этом году корпоративные клиенты обеспечат половину общего дохода, увеличившись с текущих ~40%. Для этого она планирует удвоить число сотрудников с 4500 до 8000 человек, новые сотрудники будут сосредоточены в инженерии, исследованиях, продажах и разработке продуктов.

В Сан-Франциско OpenAI подписала новый аренды (договор аренды), расширив办公面积 (офисную площадь) до более чем миллиона квадратных футов.

Настоящее поле битвы AI-шопинга не у кассы

Отступление OpenAI не означает, что AI-шопинг умер. Наоборот, верхняя часть воронки已经被彻底重塑 (была полностью преобразована).

Более половины американских потребителей уже привыкли позволять ИИ принимать решения за них. Люди больше не ищут «робот-пылесос» и не листают десять страниц с рекламой, они прямо спрашивают: «Какая модель самая性价比 (соотношение цена/качество)?». Обнаружение, исследование, сравнение — все эти действия смещаются вперед, ценность собственных каналов ритейлеров无情侵蚀 (безжалостно размывается).

Но для交易闭环 (замыкания цикла транзакции) на последней миле нужна не более умная модель, а более полная инфраструктура.

OpenAI уже чётко дала понять, что в дальнейшем будет优先做 (отдавать приоритет) поиску товаров и их обнаружению, а также добавит рекламу в ChatGPT. Это её способ монетизации на уровне обнаружения, гораздо более реалистичный, чем создание собственной кассы.

В конечном счёте, наиболее вероятный кандидат на повторение пути Alibaba в США — не OpenAI, а Amazon. У него есть пользовательские профили, карта товаров, платёжные шлюзы, инфраструктура исполнения заказов.

OpenAI попыталась создать собственную电商闭环 (e-commerce петлю) и потерпела неудачу, затем взяла деньги у крупнейшей电商平台 (e-commerce платформы) и в итоге может стать流量入口 (входом трафика) для этой платформы.

В Китае全栈优势 (преимущество полного стека) Alibaba позволило Qianwen пойти другим путём, но этот путь под силу только Alibaba. Руководитель подразделения C-пользователей Qianwen У Цзя сказал одну ключевую фразу: конкурентоспособность комплексного агента очень сильна, всё больше доказывается, что вертикальный агент — это阶段性产品 (временный продукт), в будущем独立作为入口的AI应用 (независимых AI-приложений, выступающих входом) будет не так много.

Если перевести это на язык бизнеса: в будущем замкнуть цикл AI-шопинга смогут те платформы, которые уже обладают полной экосистемой, а не AI-компании, которые начинают строить всё с нуля.

В чат-боксе не вырастет касса. Но если касса уже есть в твоём магазине, то поставить рядом чат-бота кажется совершенно естественным. Это самый важный урок AI-шопинга в 2026 году.