Written by: Wall Street Insights

This weekend is bound to be eventful.

The market is holding its breath for a true "major test." From the Supreme Court's "trillion-dollar tariff ruling" to the "tariff stick" targeting metals, and the "forced selling" by passive funds, the market is in the midst of multiple storm eyes this week.

The outcomes of these three key events, erupting in quick succession, will profoundly reshape market trends and directly impact the pricing logic of U.S. stocks, U.S. bonds, and precious metals markets.

Additionally, at 21:30 Beijing time on January 9 (Friday), the U.S. Bureau of Labor Statistics (BLS) will release the December non-farm payroll report.

After weeks of data vacuum caused by the government shutdown, this report will serve as a "reliable reading" for the economy's health and the most decisive reference before the Fed's January policy meeting, directly influencing its choice between "standing pat" or "continuing rate cuts."

At this "major test" juncture, fastening your seatbelt and guarding against volatility risks might be the best strategy.

Below, we break down these heavyweight changes one by one.

01 1,000 Companies "Besiege" the White House: Will the Trillion-Dollar Tariffs Be Refunded?

An unprecedented legal "siege" is underway in Washington.

According to the latest statistics, over 1,000 companies have officially filed lawsuits attempting to overturn the current tariff policies and demanding refunds totaling up to a hundred billion dollars in tariffs.

This includes listed giants like Costco and Goodyear Tire & Rubber Co. Dozens of entities joined the fray just in the first few days of 2026.

The focus of this lawsuit is the final ruling by the U.S. Supreme Court on the legality of the comprehensive tariff plan introduced by Trump.

According to CCTV News, the Supreme Court has set this Friday (U.S. Eastern Time) as the opinion release day. Although it is not yet confirmed whether it includes the tariff case, the market widely expects the ruling to be announced as early as this week.

What happens if the court rules the tariffs illegal?

- Bullish for U.S. Stocks: Wells Fargo chief equity strategist Ohsung Kwon estimates that if tariffs are overturned, the EBIT of S&P 500 component companies in 2026 could increase by about 2.4% compared to last year. Canceling tariffs would directly improve corporate profits, benefiting the stock market.

- Bearish for U.S. Bonds: The flip side of the coin is that canceling tariffs would削弱 an important source of government revenue, exacerbating federal deficit concerns and potentially triggering a sell-off in U.S. bonds.

- Policy Complication: If refunds form additional economic stimulus, the Fed's rate-cutting path will become more complex.

Even if the Supreme Court rules it illegal, the specific refund process (involving approximately $133 billion) may still need to be handled by lower courts, and the White House might invoke other laws to re-impose restrictions, meaning policy uncertainty will persist long-term.

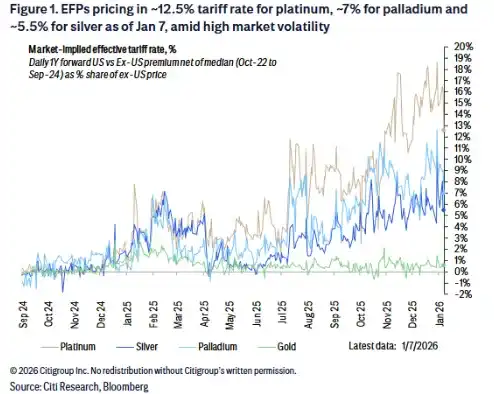

02 Critical Minerals Tariff Countdown: Silver, Platinum Face "Nerve-Wracking Moment"

Besides the comprehensive tariff case, the results of the U.S. "Section 232" investigation on critical minerals are expected to be announced this Saturday (January 10). This decision directly affects the fate of Comex silver and platinum group metals.

The Citi research team provided a detailed scenario analysis:

If tariffs are imposed: The market will have an implementation window of about 15 days, triggering a short-term "rush to ship to the U.S." behavior. This will push up domestic U.S. benchmark pricing and the Exchange for Physical (EFP) premium.

As of January 7, EFP pricing indicates the market expects a platinum tariff of about 12.5%, palladium about 7%, and silver about 5.5%. These implied tariff rates reflect market uncertainty amidst high volatility.

(Expected Tariff Rates from EFP Pricing)

If no tariffs are imposed: Metals will flow out of the U.S. to other global regions, easing pressure on London spot prices and potentially causing a price pullback.

What's the view on specific varieties?

- Silver (Likely Safe): Due to heavy U.S. reliance on silver imports, Citi believes no tariff is the base case, and even if imposed, Canada and Mexico might be exempt. However, in a "no tariff" scenario, silver prices could face temporary downward pressure.

- Palladium (High Risk): Most likely to face tariffs (e.g., 50%). If imposed, U.S. domestic import costs would rise sharply, pushing up futures prices.

- Platinum (A Coin Toss): Whether tariffs will be imposed is currently extremely uncertain.

The investigation results were originally due on October 12, 2025, and President Trump has 90 days to take action, meaning the deadline is around January 10 (this Saturday). However, Citi believes that given the large number of commodities involved, President Trump's action might be indefinitely delayed, in which case silver and PGM prices are likely to continue rising during this period.

03 Technical Sell-off Approaches: The "Bloody Week" of Commodity Index Rebalancing

Beyond fundamental news, a "passive storm" on the funding side has already begun.

The highly anticipated annual weight rebalancing of the Bloomberg Commodity Index (BCOM) started after the close on January 8 and will continue until January 14. To maintain the diversification rule that no single commodity weight exceeds 15%, this adjustment poses significant selling pressure on the precious metals sector.

Gold: Weight reduced from 20.4% to 14.9%, facing selling pressure equivalent to 3% of total holdings.

Silver: Faces particularly huge pressure! Weight will be drastically cut from 9.6% to 3.94%, with expected selling volume reaching up to 9% of total holdings.

This "non-fundamental" selling triggered by index rules forces speculative funds to stay on the sidelines, exacerbating short-term volatility.

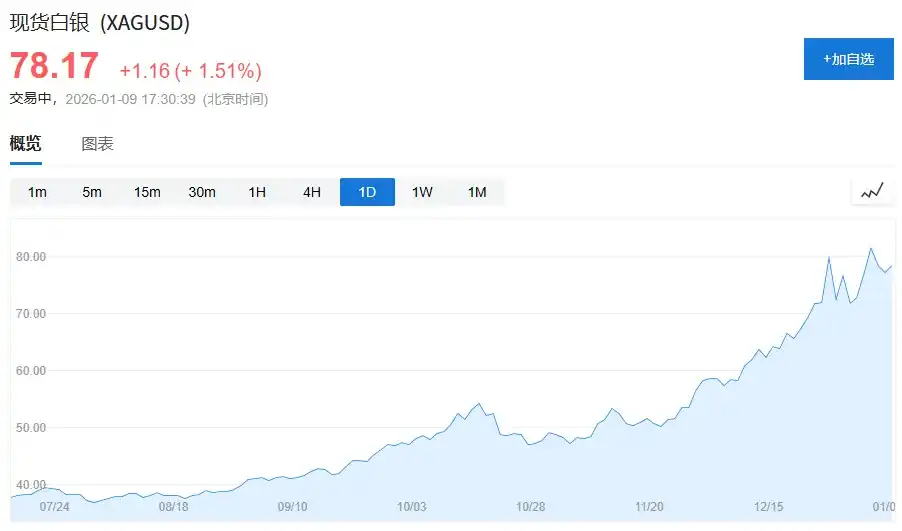

It's worth noting that the decline in gold, silver, and other precious metals comes after a rare epic rally. Spot gold surged over 70% throughout 2025, and silver gains once reached about 150%, entering a frenzy mode from December 23 last year and continuously hitting record highs. Such massive short-term profit accumulation makes the market extremely fragile when facing liquidity events.

Although Goldman Sachs analysts believe that as long as the tight London inventory situation persists, liquidity is the key determinant of prices, in the short term, investors' nerves must be strained in the face of such large-scale passive fund "repositioning."