Author: Max.S

Original Title: Crisis or Feast? Unpacking JGB Risks Under Nikkei 57,000 and the New Logic of Global Asset Allocation

Just 24 hours ago, Japanese financial history was rewritten. The Nikkei 225 index surged violently by over 2,700 points, decisively breaking through the historic high of 57,000 points. This is not merely a numerical breakthrough; it is a direct pricing-in of the results of the House of Representatives election held after the shortest official campaign period (16 days) since the end of World War II — the ruling coalition of the Liberal Democratic Party (LDP) and Japan Innovation Party secured an absolute majority of two-thirds of the seats.

However, while equity traders were popping champagne corks, bond trading desks were on high alert. Japanese Government Bonds (JGBs) faced a fierce sell-off, with the yield on the 30-year bond soaring to 3.615%—a veritable tsunami in a country accustomed to low interest rates.

As financial professionals, we need to look beyond the surface of the price charts to decipher the logic behind this "Song of Ice and Fire": global markets are trading a new "Japan narrative," and this narrative is intertwining with the rebound in U.S. tech stocks, gold's push towards $5,000, and signals of China selling U.S. Treasuries to form a complex macroeconomic puzzle.

The core driver of the surge on February 9th was one thing only: expectations of fiscal expansion driven by political certainty.

According to the latest vote count, the LDP won 316 seats. Combined with the Innovation Party's 36 seats, the ruling coalition holds a dominant position within the 465-seat chamber. This grants the government unprecedented legislative power, including the ability to pass controversial constitutional amendments and, more importantly—aggressive fiscal stimulus policies.

The logic of this trade is very clear:

-

Political Backing: An absolute majority means the opposition's (e.g., the Constitutional Democratic Party) power to check the government is minimal.

-

Policy Expectations: While Finance Minister Takaichi Sanae explained the "temporary cut in food sales tax" as "limited to two years and not reliant on debt issuance," the market is clearly pricing in longer-term fiscal easing.

-

Industrial Policy: Defense and industry are at the core of the Takaichi policy. This explains why defense-related stocks like Mitsubishi Heavy Industries led the gains, while SoftBank Group's 8% surge was a direct reaction to expectations of liquidity easing and an improved environment for tech investment.

For quant funds, yesterday's strategy was simple: Long Nikkei, Short Yen, Short JGBs. This is a classic "Reflation" trade model.

If the stock market is trading "growth," then the bond market is trading the prelude to "default risk"—or at least a deterioration in fiscal sustainability.

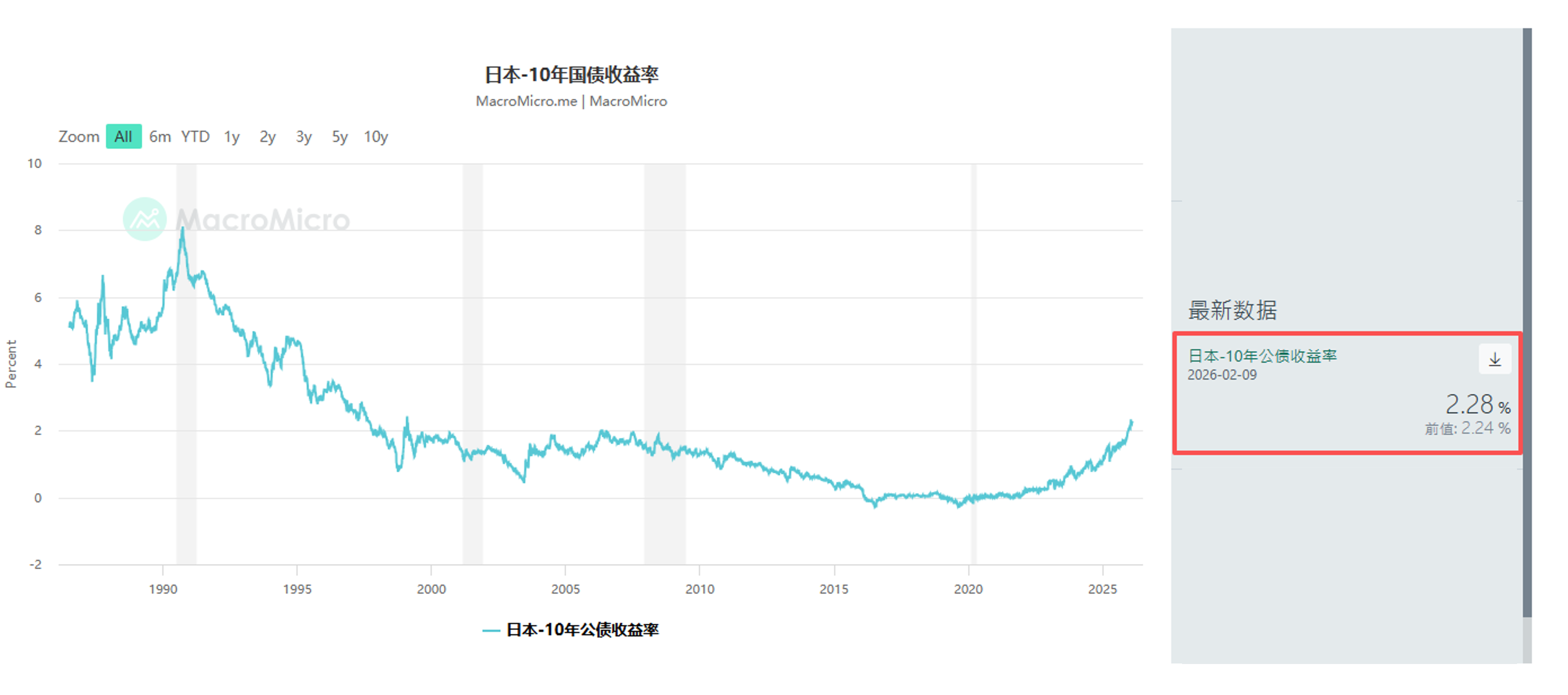

The sell-off in the JGB market was not sudden. As early as January, global macro funds, including Schroders Plc and JPMorgan Asset Management, had begun reducing their holdings of ultra-long-term Japanese government bonds. Yesterday, the 10-year bond yield rose 4.5 basis points to 2.28%, and the 30-year yield climbed 6.5 basis points to 3.615%.

This sends a dangerous signal: the Term Premium is returning.

Investors fear that tax cuts, combined with an already heavy debt burden, will force the Japanese government to increase JGB issuance. Although officials have tried to reassure markets that the tax cuts will not rely on deficit financing, in the illiquid JGB market, any hint of trouble is magnified.

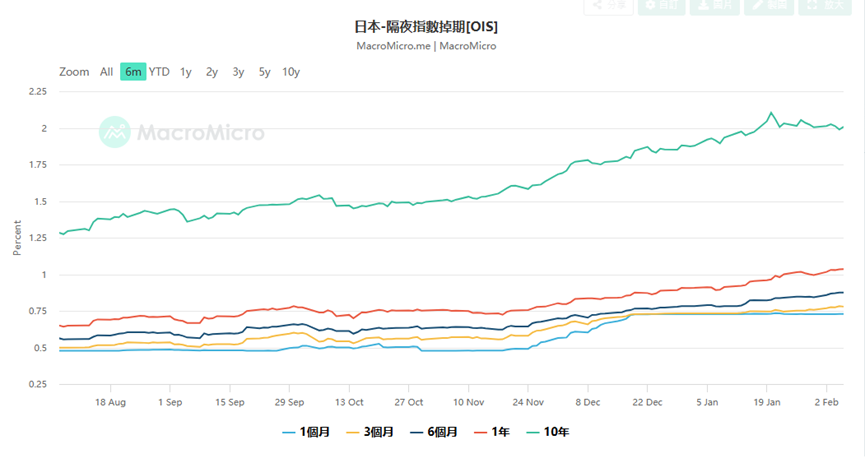

This also presents a huge dilemma for the Bank of Japan (BOJ). Overnight Index Swap (OIS) data shows the market is currently pricing in a 75% probability of a 25 basis point rate hike by the BOJ at its April meeting, with some traders even starting to bet on a March hike.

Why bet on a March hike? Because if the yen depreciates disorderly due to fiscal deterioration (yesterday it briefly broke through 157.76), the central bank must hike rates to defend the currency, even if this exacerbates debt servicing costs. This is a classic "fiscal dominance" dilemma. Yusuke Matsuo, senior market economist at Mizuho Bank, warned that we need to watch closely for hawkish comments from BOJ board members, as this could be verbal intervention to prevent a yen collapse.

The Japanese market is not an island. When we zoom out to a global perspective, we see that the February 9th market action is part of a broader return of risk appetite, but it also comes with deep structural fractures.

-

Chinese Market: This was one of the most intriguing macro news items yesterday: Chinese regulators advised financial institutions to control their holdings of U.S. Treasury bonds, citing "concentration risk and market volatility." Although the official wording was cautious, emphasizing this was not related to geopolitics, the move by the second-largest holder of U.S. debt undoubtedly puts upward pressure on U.S. Treasury yields (prices fall) amid global liquidity tightening. This is partly why U.S. Treasury yields rose in tandem with JGB yields yesterday. This essentially tells the market: the anchor of global sovereign credit is loosening.

-

U.S. Market: U.S. markets rebounded on Friday led by the semiconductor sector, with Nvidia, AMD, and Broadcom all gaining over 7%. This sentiment directly spilled over to Asia, where semiconductor equipment giants like Tokyo Electron and Advantest were the main drivers behind the Nikkei's charge. The capital expenditure (Capex) story for AI infrastructure continues, and although Amazon's massive spending raised profitability concerns, the logic of the hardware cycle remains intact as long as demand for Nvidia's GPUs persists.

-

Precious Metals Market: After experiencing sharp volatility, the gold price reclaimed the $5,000/oz level. This is not a safe-haven move; it's a "credit hedge." As Japan engages in fiscal expansion, U.S. debt ceiling issues persist, and China diversifies its reserves, gold becomes the only "supra-sovereign currency." U.S. Treasury Secretary Scott Bessent's accusation that Chinese traders are influencing gold price fluctuations itself exposes the U.S. Treasury's anxiety over dollar pricing power.

Faced with such a fragmented market—stock market狂欢 (狂欢,狂欢 means狂欢/carnival/celebration) vs. bond market暴跌 (暴跌 means暴跌/crash/plunge)—how should investors respond?

-

Equity Markets: Long Volatility. Even though the Nikkei hit a new high, the retreat in the VIX index might just be the calm before the storm. Key variables this week are Wednesday's U.S. labor market data and Friday's inflation data (CPI). If U.S. inflation rebounds, coupled with a hawkish pivot from the BOJ, global liquidity will face a double tightening.

In this environment, while holding core growth stocks (e.g., semiconductors, Japanese trading houses), it is wise to use put options for protection. Current Skew data shows put options are still expensive, indicating institutions are not completely off guard.

-

FX Market: Tactical Yen Rebound. The yen faces extremely high intervention risk around the 157 level. Finance Minister Takaichi Sanae explicitly stated she is in close contact with the U.S. Treasury Secretary, meaning the possibility of coordinated intervention cannot be ruled out. If the BOJ confirms a rate hike in March or April, the yen could see a rapid short squeeze. For carry traders, now is the time to gradually take profits.

-

Alternative Assets: Focus on "Hard Assets." In an era of shaky fiat currency credibility (be it concerns over Japan's fiscal health or U.S. debt worries), gold, silver, and some cryptocurrencies that have stabilized in this pullback (Bitcoin > $70k) possess long-term allocation value. Particularly silver, which, after a sharp 50% correction, could see a new short squeeze triggered by tight physical inventories.

February 9, 2026—Nikkei at 57,000 points is a milestone and a watershed. It marks Japan's complete departure from the deflationary era and its entry into a "new normal" of high growth, high inflation, and high interest rate volatility. Takaichi Sanae's supermajority is a double-edged sword: it can push stock prices higher through aggressive policies, but it can also destroy bond market confidence through runaway fiscal deficits.

For financial professionals, the gentle era of "stocks and bonds rising together" is over. We need to adapt to extreme scenarios where the negative stock-bond correlation breaks down, or even simultaneous stock and bond sell-offs. In this new era, watching central bank balance sheets might be more important than watching corporate income statements.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush