Author: Claude, Deep Tide TechFlow

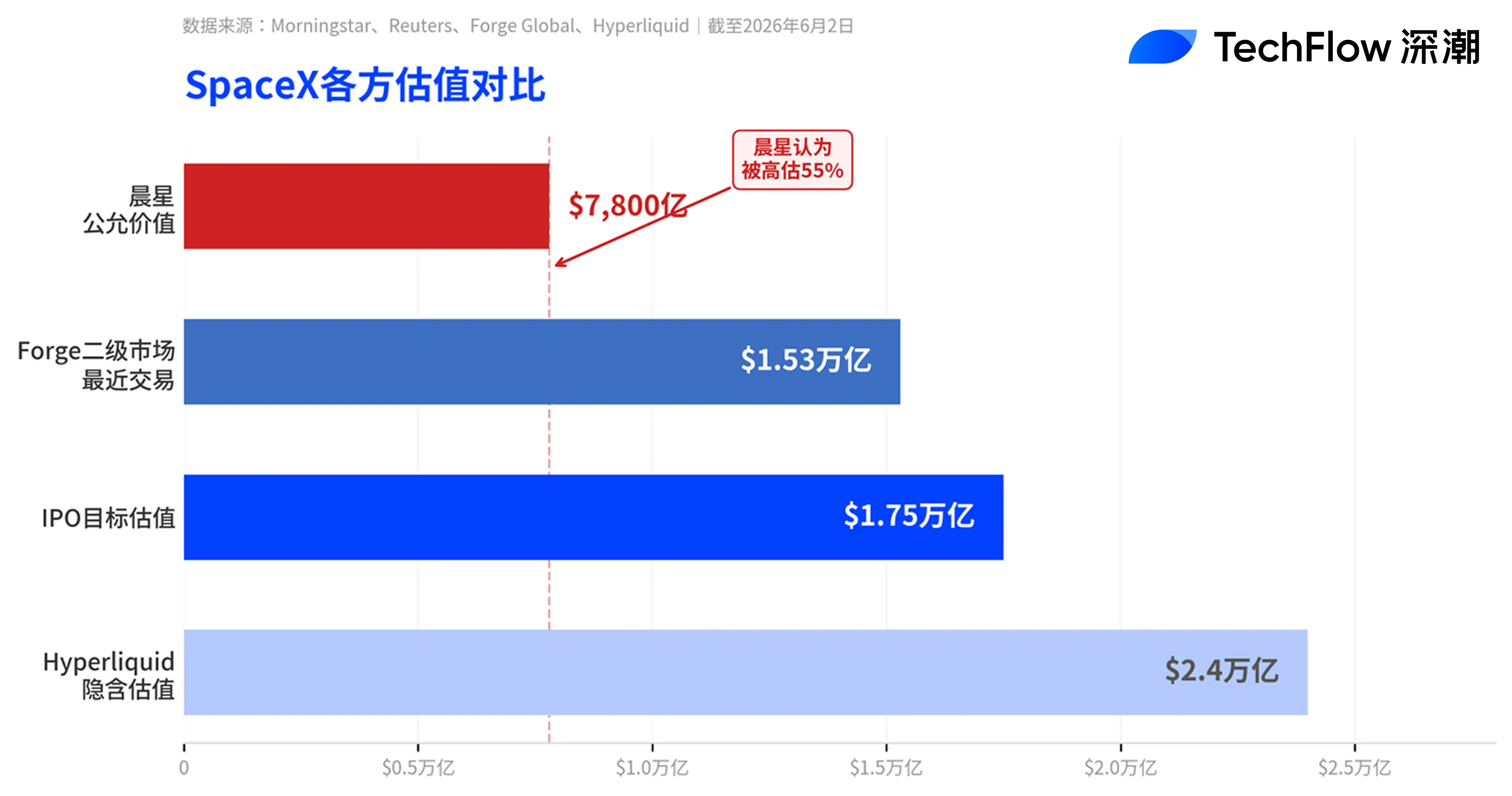

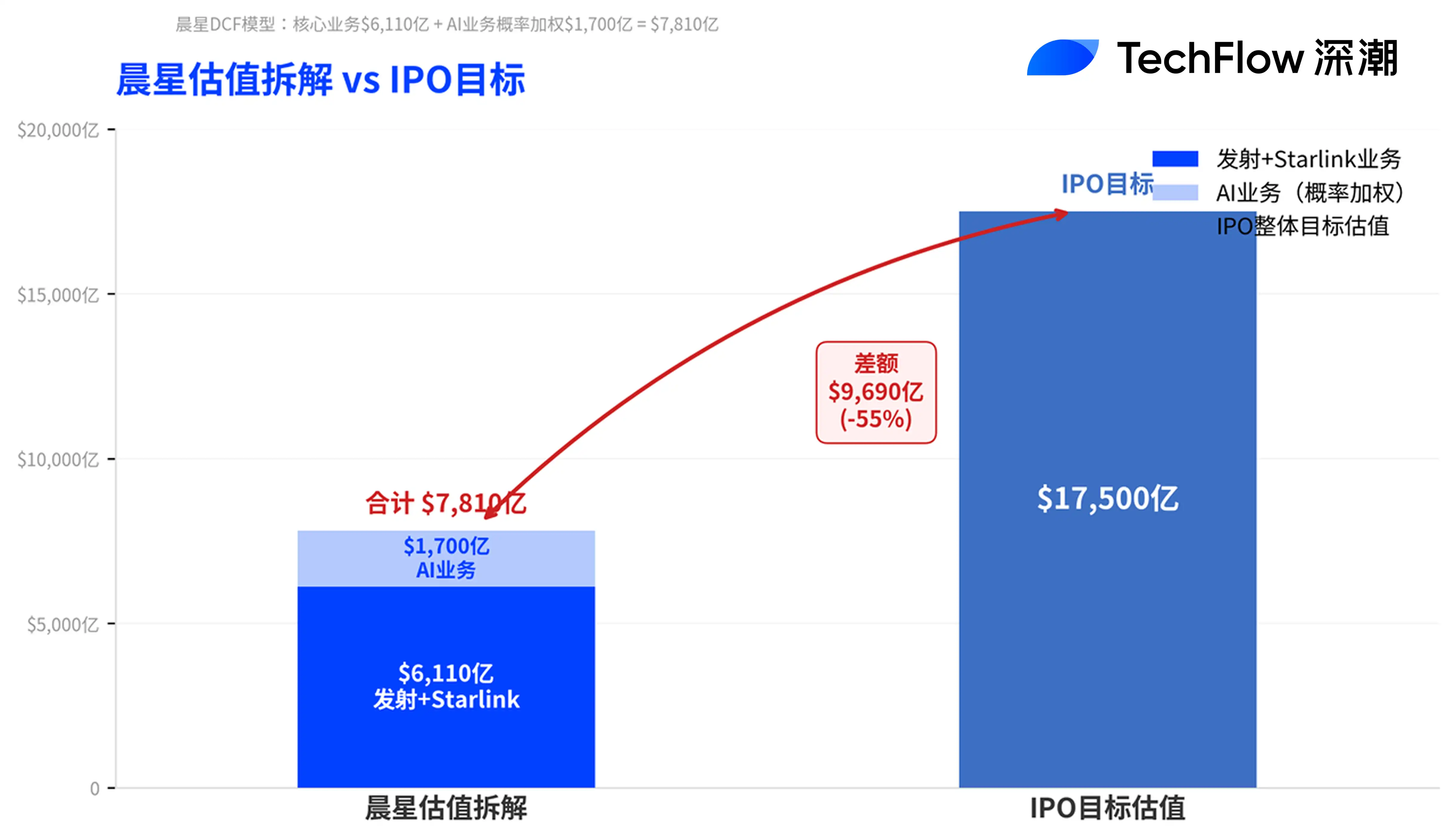

Deep Tide Guide:SpaceX's roadshow kicks off this week, but Morningstar has already poured cold water. The research firm values it at a fair value of $780 billion using a DCF model, only 45% of SpaceX's target valuation of $1.75 trillion, with the analyst bluntly stating "the company is severely overvalued." Morningstar values the core launch and Starlink businesses at $611 billion, with xAI-related AI business receiving only a $170 billion probability-weighted valuation. However, Morningstar also admits that with extremely low float and the Nasdaq 100's rapid inclusion mechanism, SpaceX's stock price may still rise in the short term.

SpaceX is about to welcome what could be the largest IPO ever, and one of Wall Street's most well-known independent research firms just threw a bucket of cold water on it.

According to a Reuters report on June 2, Morningstar, just before SpaceX's planned roadshow launch this week, initiated research coverage on the company for the first time, providing a fair value estimate of $780 billion. This is nearly a 50% discount to SpaceX's most recent secondary market valuation of $1.53 trillion on the Forge Global platform and only about 45% of its $1.75 trillion IPO target valuation.

Morningstar equity analyst Nicolas Owens's judgment was unequivocal: "We believe the company is severely overvalued, and investors will have the opportunity to buy at a more attractive price after the IPO."

Where Does $780B Come From: Launch+Starlink Worth $611B, AI Worth Only $170B

Morningstar's valuation breakdown reveals the core of the disagreement.

Owens's DCF model values SpaceX's core launch business and Starlink satellite broadband business together at approximately $611 billion in enterprise value, with an additional probability-weighted valuation of about $170 billion for the AI business (including xAI and social media platform X). Morningstar gives SpaceX a "Narrow Moat" rating, citing its cost advantage in reusable rockets and Starlink's scale effects, but believes the recently acquired AI business drags down the overall rating.

Regarding the AI business specifically, Morningstar modeled three scenarios: the most optimistic "moonshot" scenario values it at $1.3 trillion but is assigned only a 7% probability; the most pessimistic "unviable" scenario would destroy over $81 billion in value and is assigned a 43% probability. Owens wrote: "We do not regard Grok as one of today's leading AI labs." He also warned that the future prospects of SpaceX's AI business rely on unproven technologies like orbital data centers.

Starlink's fundamentals are relatively solid. According to S-1 filing disclosures, Starlink's 2025 revenue grew 50% year-over-year to $11.3 billion, with operating profit exceeding $4.4 billion. The user base has surpassed 10 million, making it SpaceX's only profitable business segment currently. Yet, even with that, based on the $1.75 trillion valuation, SpaceX's estimated total 2025 revenue of around $18.7 billion implies a price-to-sales ratio nearing 100.

Musk's Retort from Afar: 'You shall see'

Faced with valuation doubts, Musk chose to respond with Tesla's history. He posted on platform X early Tuesday: "Tesla's IPO market cap was only 0.1% of its current value." When a user pressed him on how to defend a valuation with over 50x price-to-sales, Musk replied with just three words: "You shall see."

But the validity of the analogy is questionable. According to Yahoo Finance, Tesla's current market cap is about $1.3 trillion, with a price-to-sales ratio of about 15.7x and a P/E nearing 400. Even by Tesla's already expensive valuation standards, SpaceX seeking a higher market cap with significantly lower revenue presents a much higher pricing hurdle.

NYU Stern professor Scott Galloway's podcast co-host Ed Elson used sharper language. As cited by Motley Fool, he described SpaceX's IPO filing documents in an article as "non-serious, empty, full of illusions, bordering on dishonest."

Staged Unlock + Nasdaq Rapid Inclusion: Short-term Rise Followed by Potential Decline

Despite its bearish valuation, Morningstar also acknowledged that SpaceX's stock price may still rise in the short term after the IPO. The logic is threefold: extremely low initial float (only about 3% of shares publicly offered), robust investor demand for AI infrastructure plays, and the Nasdaq 100 index's fast-track inclusion mechanism.

According to CNBC, new Nasdaq rules introduced on May 1 allow mega-cap new listings to be included in the Nasdaq 100 index after just 15 trading days post-IPO, a condition SpaceX fully meets based on its expected valuation. Upon inclusion, all passive funds tracking the index will be forced to buy, creating a wave of short-term index inclusion buying pressure.

However, mid-term selling pressure is also a concern. SpaceX has adopted an unconventional staged lock-up release structure: after the company releases its first quarterly report post-IPO (covering April to June), insiders can sell up to 20% of their locked shares; if the stock price has risen over 30% from the IPO price by then, an additional 10% can be unlocked. Subsequently, at days 70, 90, 105, 120, and 135, an additional 7% unlocks each time. After the Q3 earnings release, another 28% unlocks, with the remainder fully unlocked 180 days after the IPO. Musk himself is subject to a 366-day lock-up.

According to the S-1/A filing, SpaceX has also reserved up to 5% of IPO shares for designated employees and executives, and these holders are not subject to standard lock-up restrictions. Motley Fool analysis suggests investors need not rush to buy on the first IPO day; waiting until all unlock provisions expire and index inclusion is complete might be wiser.

$20B Bridge Loan and Governance Risks

Morningstar also flagged two structural risks.

First, debt accumulated by SpaceX in recent years is mainly related to AI infrastructure investments, with $20 billion in the form of a bridge loan maturing 15 months after the IPO, posing refinancing risk. Morningstar expects the company to raise $50-$80 billion through the IPO, with part of the proceeds used to repay this loan.

Second is corporate governance issues. Musk holds about 85% of voting rights through a dual-class share structure. Additionally, the $250 billion acquisition of xAI earlier this year was not an arm's-length transaction. This related-party deal boosted SpaceX's valuation from around $1.5 trillion to the IPO target level, but the AI business itself has not yet proven its economic viability.

SpaceX plans to launch its roadshow during the week of June 8, price on June 11, and list on Nasdaq under the ticker SPCX on June 12. This will be the largest IPO in history and could also be one with the most significant bullish-bearish divergence in recent years.