This article is from: Pine Analytics

Compiled by | Odaily Planet Daily (@OdailyChina); Translator | Ethan (@ethanzhang_web 3)

Editor's Note: In recent years, the crypto market once believed that the fee revenue of L1 public chains was the core cash flow supporting token valuations. However, this research uses on-chain data to reveal a different reality: whether it's Bitcoin's congestion cycles, Ethereum's DeFi and NFT peaks, or Solana's memecoin frenzy, all fee booms are ultimately compressed by innovation. Demand explosions lead to revenue peaks, peaks stimulate the emergence of alternatives, and profits are systematically squeezed out. The compression of L1 value capture is not a cyclical phenomenon but a structural outcome of open networks.

The market in 2026 has long stopped pricing L1s purely based on "fee capture." The price drivers for ETH and SOL are shifting from L1 fee logic to staking yields, ETF fund flows, RWA narratives, protocol upgrade expectations, and the macro liquidity environment. The compression trend continues, but the pricing anchors have migrated. What's truly worth pondering is not just whether fees will continue to decline, but: when the market stops pricing L1s based on "on-chain profits" and instead uses "asset narratives" and "structural fund flows," is this new logic equally fragile; and when narratives recede, what fundamental support will prices return to?

L1 blockchains find it difficult to earn fees sustainably and stably during their scaling development phase. Every major revenue source they once found—from transaction fees to MEV—is eventually eroded bit by bit by the users they serve through various arbitrage methods. This isn't a failure of any specific chain, but an inherent characteristic of open, permissionless networks: as soon as an L1 earns enough money from fees to reach a certain scale, transaction participants devise new ways to compress that revenue, or even reduce it to zero.

Bitcoin, Ethereum, and Solana are among the most successful networks in crypto. Yet, interestingly, although they process billions of dollars in value flow daily, all three have followed almost the same path: fee revenue spikes dramatically in the short term, capturing everyone's attention, only to soon have their business snatched away and revenue分流 (diverted) by L2s (Layer 2 networks), private order flow, MEV-aware routing tools, or new玩法 (play/innovations) at the application layer. This situation has occurred repeatedly in every fee model, every MEV wave, and every scaling solution in the crypto industry, with no signs of slowing down.

This article argues that L1 fee compression is a long-standing and accelerating phenomenon. This article will梳理 (outline) the specific innovative plays that compress profits at different stages and explore what this means for those L1 tokens that still factor "sustainable fee earnings" into their valuations.

Bitcoin

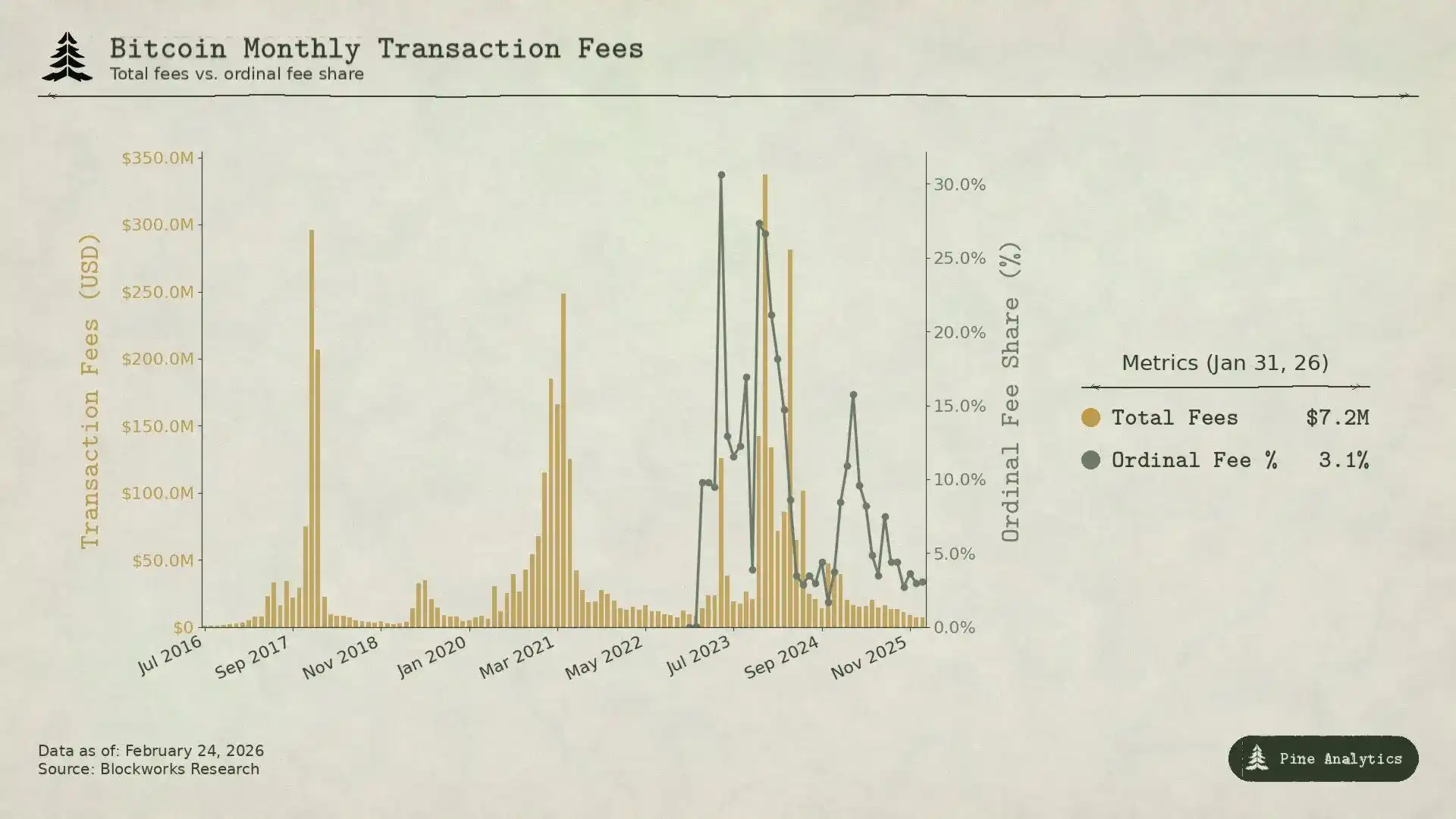

Bitcoin's fees are almost entirely earned from congestion during on-chain BTC movements—when everyone crowds in to transfer, fees naturally rise. And because Bitcoin lacks smart contracts, there's virtually no MEV in the network. The key issue is: each time a BTC price increase drives a fee surge, the magnitude of the fee increase is weaker compared to the scale of economic activity than in the previous cycle.

In 2017, BTC rose from $4,000 to $20,000. The average fee also surged from less than $0.40 to over $50. At the peak on December 22nd, fees constituted 78% of miner block rewards: fees alone amounted to approximately 7,268 BTC, nearly four times the block subsidy. But within just three months, fees fell by 97%, returning to their original state.

The market reacted very quickly, soon developing countermeasures. In early 2018, SegWit transactions accounted for only 9%; by mid-year, this had risen to 36%; although such transactions made up over one-third of the total transaction volume, they contributed only 16% of the fees. Exchanges also began adopting batching, combining hundreds of withdrawals into a single transaction, saving significant fees. These factors combined led to a 98% reduction in fees within six months. Additionally, the Lightning Network officially launched in early 2018, specifically addressing small transaction fees; Wrapped BTC on other chains also allowed users to gain BTC exposure without necessarily operating on the Bitcoin main chain.

By the 2021 BTC price peak, although the price reached $64,000, the monthly fee revenue was actually lower than in 2017. There were fewer on-chain transactions then, but the dollar-denominated transfer volume was 2.6 times higher than in 2017—simply put, the network transferred more value, but the fees captured did not keep up, and even decreased.

The current cycle illustrates this unstoppable trend even more clearly. BTC rose from $25,000 to over $100,000, an increase of roughly 3 times (the original text said 4x, adjusted slightly based on the actual price range without changing the meaning), but standard transfer fees never skyrocketed as in previous cycles. By late 2025, daily transaction fees were only about $300,000, less than 1% of miners' total income. Bitcoin's full-year 2024 fees were $922 million, but most came from the short-term hype of Ordinals and Runes, not stable income from traditional BTC transfers. By mid-2025, spot Bitcoin ETFs held over 1.29 million BTC, about 6% of the total supply, providing large-scale BTC exposure demand for the market without generating any on-chain fees. The on-chain interaction required to acquire Bitcoin assets has been largely engineered away.

Ordinals and Runes once pushed the fee share of miner income to 50% in April 2024, but as related tools matured, by mid-2025, this ratio fell back below 1%. This short-term spike was more like偶然 (fortuitous)收益 (income) from MEV, not stable income generated by congestion, stemming more from the immature tooling around new asset types rather than genuine demand for BTC settlement.

The pattern is quite clear: as soon as Bitcoin earns enough money from fees to be noticeable, cheaper alternatives emerge within the ecosystem. The L1 can only earn a short-term fee peak from each type of demand, after which that profit is gradually eaten away by continuous innovation.

Ethereum

Ethereum's fee story is even more dramatic. Because this chain truly captured massive value, only to watch it be systematically dismantled.

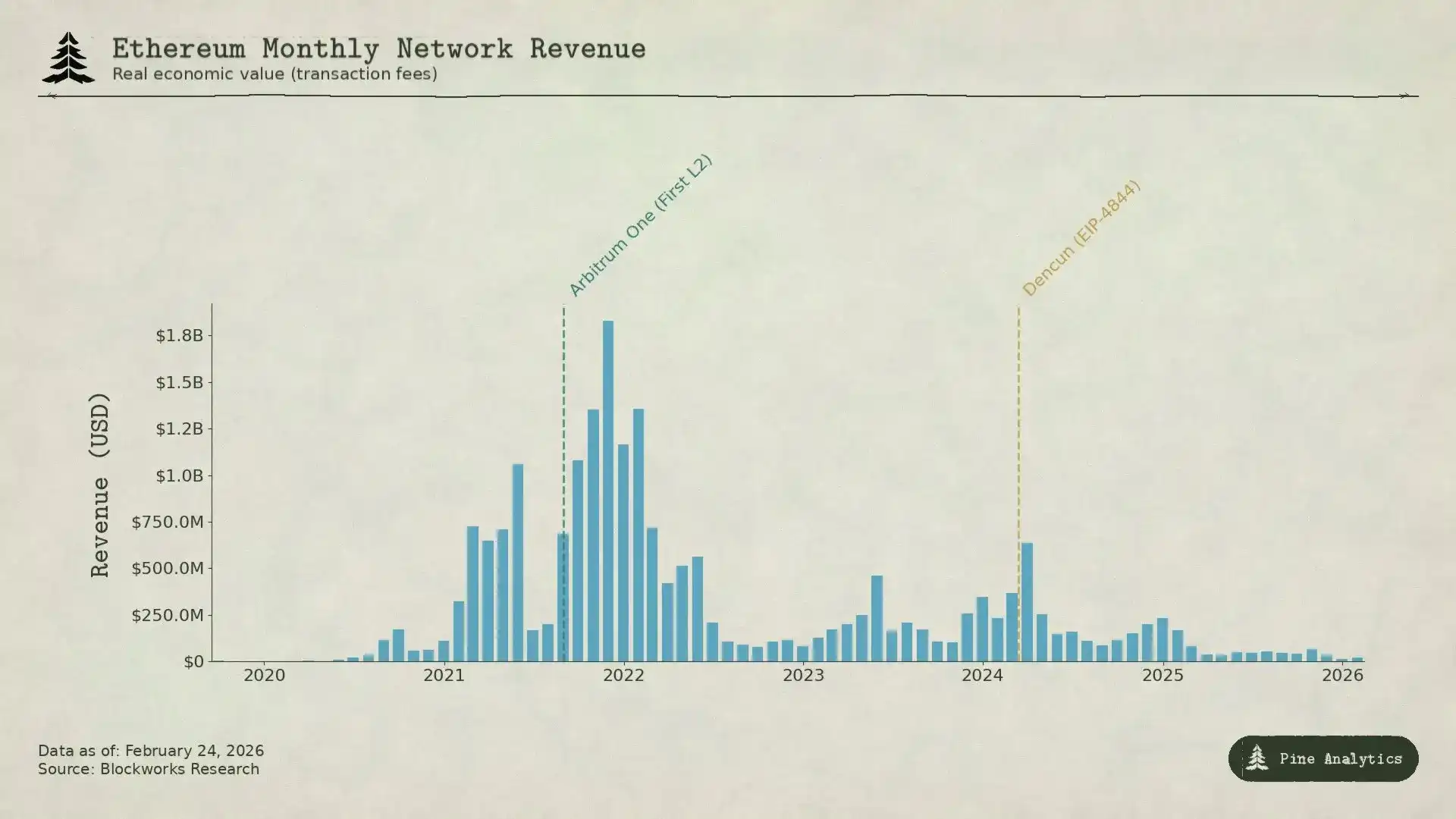

In mid-2020, "DeFi Summer" made Ethereum the center of a new financial system. Uniswap's monthly trading volume skyrocketed from $169 million in April to $15 billion in September. TVL grew from under $1 billion to $15 billion by year-end. In September 2020, Ethereum miner fee income hit a record $166 million, six times that of Bitcoin miners. This was the first time a smart contract platform earned substantial, sustained income from real economic activity.

In 2021, NFTs叠加 (stacked on top of) DeFi. The average transaction fee reached $53 during peaks. Quarterly fee income grew from $231 million in Q4 2020 to $4.3 billion in Q4 2021, an increase of 1,777%. The EIP-1559 implemented in August 2021 introduced a base fee burn mechanism, permanently removing a portion of fees from the market. At that time, it seemed Ethereum had truly solved the core problem of L1s not being able to earn money.

But in reality, these fees were essentially "congestion fees": users paid $20 to $50 not because the transaction was worth that much, but because everyone was trying to use the chain, exceeding Ethereum's processing capacity of about 15 transactions per second (15 TPS). This inherent shortcoming left ample room for cheaper alternatives.

Other L1s like Solana, Avalanche, and BNB Chain offered transactions for just a few cents; Ethereum's L2 Rollups, like Arbitrum and Optimism, snatched even more business—they process transactions on their own networks and then send compressed transaction batches back to the Ethereum mainnet for settlement, being both fast and cheap.

Subsequently, Ethereum performed a "self-weakening." The Dencun upgrade on March 13, 2024, introduced Blob transactions (EIP-4844), providing L2s with a cheaper data publishing path. Before this, L2s used calldata, costing about $1,000 per megabyte. After the upgrade, Arbitrum's per-transaction fee dropped from $0.37 to $0.012; Optimism from $0.32 to $0.009. The median Blob fee dropped to almost zero. Ethereum intended to retain users with this move, but instead weakened its last important source of fee income.

The data makes it even more直观 (intuitive). In 2024, L2s generated $277 million in revenue but paid only $113 million to Ethereum. By 2025, L2 revenue fell to $129 million, while the amount flowing back to Ethereum was only about $10 million, less than 10% of L2 revenue, a year-on-year decrease of over 90%. The once monthly L1 fee income exceeding $100 million had fallen below $15 million by Q4 2025. The chain that created $4.3 billion in revenue in a single quarter saw its income scale shrink by about 95% just four years later.

Bitcoin's revenue was compressed because people could get BTC without using the chain; Ethereum's revenue compression happened in two waves: The first wave was other alternative networks吸走 (siphoning off) users unwilling to pay high congestion fees; the second wave was Ethereum's own scaling plan, pushing the cost of L2 data transmission to almost zero, making it unable to earn money from settlement anymore. In either case, the L1 itself built, or allowed, the tools that snatched its revenue to appear.

Solana

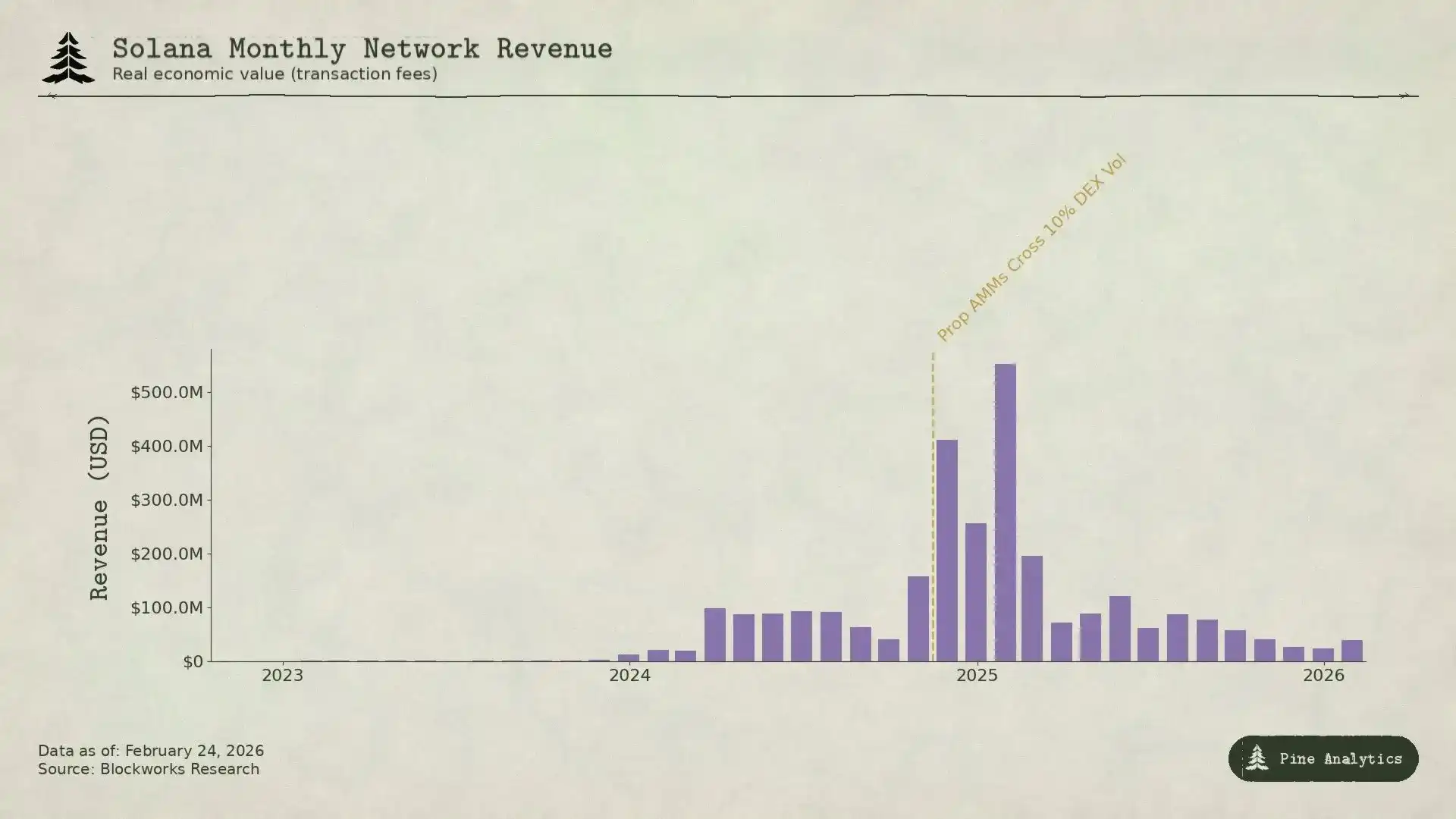

Solana's money-making logic is completely different from Bitcoin and Ethereum—it hardly relies on congestion for fees. The base fee is fixed at 0.000005 SOL per signature, cheap enough to be almost negligible. About 95% of fee income comes from priority fees and MEV tips paid through the Jito block engine. In Q1 2025, Solana's "Real Economic Value" (REV) reached $816 million, of which 55% came from MEV tips. In 2024, validators earned roughly $1.2 billion, while operating costs were only about $70 million, leaving a significant profit margin.

The key to Solana's fee explosion was memecoin trading. Pump.fun, launched in January 2024, earned over $600 million in protocol revenue in less than 18 months, contributing up to 99% of memecoin issuance at its peak. DEX daily trading volume once reached $38 billion. The launch of the TRUMP token in January 2025 drove single-day priority fees to 122,000 SOL and MEV tips to 98,120 SOL. In 2024, the top 1% of memecoin traders contributed $1.358 billion in fees, nearly 80% of total memecoin fees. Almost entirely driven by MEV.

Today, two types of innovation are compressing this income.

The first is proprietary AMMs. Protocols like HumidiFi, SolFi, Tessera, ZeroFi, and GoonFi use private vaults managed by professional market makers, quote internally, and update prices multiple times per second. Because liquidity is not公开 (publicly available), MEV bots cannot perform sandwich trades. More critically, proprietary AMMs route orders through aggregators like Jupiter, actively choosing counterparties, rather than passively exposing themselves to anyone willing to pay MEV tips as public pools do. By keeping pricing private and continuously refreshing, they eliminate the "stale quote" problem—the source of a large portion of Solana's MEV revenue. HumidiFi processed nearly $100 billion in trading volume in its first five months after launch. Today, proprietary AMMs account for over 50% of Solana DEX trading volume, with even higher shares in highly liquid pairs like SOL/USDC.

The second is Hyperliquid migrating the most profitable spot trading activity directly off Solana. Using its self-developed HyperCore technology, it built a set of native bridging tools, allowing tokens on Solana to be deposited onto Hyperliquid, withdrawn back, and traded on its spot order book. When Pump.fun launched the PUMP token in July 2025, price discovery happened on Hyperliquid, not Solana's DEXs, via the HyperCore cross-chain bridge. Before this, Hyperliquid had already tested this model with SOL itself and tokens like FARTCOIN—the phase with the largest spreads, highest volatility, and easiest MEV profits is gradually moving out of Solana.

These two approaches compress Solana's revenue from two directions: proprietary AMMs reduce the MEV trades remaining on Solana, while Hyperliquid directly migrates the spot trading most capable of generating MEV profits off-chain. By Q2 2025, Solana's REV had decreased 54% quarter-on-quarter to $272 million; daily MEV tips had fallen over 90% from the January peak to less than 10,000 SOL per day.

The pattern is actually the same as the previous two chains, just with a different way of making money: Solana's fees are essentially short-term money earned from MEV when new trading玩法 (plays/innovations) first emerge and are still chaotic. Once proprietary AMMs optimize trading efficiency and Hyperliquid siphons off high-value orders, these profits quickly shrink. The L1 can earn a large sum during market frenzies, but the market always quickly devises new ways to prevent such short-term gains from lasting.

Impact on Token Prices

The pattern demonstrated by the aforementioned three chains is not merely a retrospective description; it is also somewhat predictive to a certain extent. Every L1 fee mechanism follows the same trajectory: new demand brings an income peak, the peak attracts innovation, innovation compresses profits, and this compression, once it occurs, is difficult to reverse. Following this logic, we can make a rough judgment about the future of four tokens.

Ethereum: Persistent Fee "Collapse"

Ethereum's fees have not yet found a clear bottom. In 2024, L2s paid $113 million to the Ethereum mainnet; by 2025, this plummeted to roughly $10 million, a drop of over 90%. Each new L2 reduces the demand for Ethereum mainnet block space a little more, and Ethereum's own scaling plans continue to lower the cost of data transmission. EIP-4844 was not a one-time repricing but the starting point of a structural shift—Ethereum actively subsidizes infrastructure tools that route activity outside its fee market. Currently, monthly L1 fee income has fallen below $15 million, and the forces driving the decline are still strengthening. If Ethereum cannot create全新的 (brand new) sources of L1-native demand, the token price will continue to reflect this compression trend. ETH is increasingly resembling a low-yield infrastructure asset rather than the high-growth smart contract platform it once was.

Solana: Record High Activity, Not Necessarily Price

Solana will almost certainly achieve new highs in on-chain activity in the next cycle—its ecosystem is deep enough, developers numerous enough, and infrastructure mature enough—but fee revenue may not follow suit. The memecoin frenzy from late 2024 to early 2025 was, for Solana, equivalent to Bitcoin's "SegWit moment": a fee peak supported by new demand, quickly compressed thereafter by innovation.

Currently, proprietary AMMs already handle over 50% of DEX trading volume, significantly削弱 (weakening) MEV. Hyperliquid's HyperCore technology is still moving the most profitable price discovery环节 (aspects/segments) off-chain. Even if on-chain activity is 2 to 3 times higher than in January 2025, its fee system has matured to the point where it's difficult to convert this activity into corresponding validator income. Current daily MEV tips are down over 90% from the peak, but on-chain activity remains healthy. Without sufficient fee income to support valuation, even if Solana's usage hits new highs, the possibility of SOL breaking its all-time high in the next cycle is not great.

Hyperliquid: The Before and After of Boom and Compression

Hyperliquid is the most noteworthy case because it represents the next stage of this "earn-get compressed" cycle, and the market has not yet realized how the latter half of this cycle will play out.

Hyperliquid is now a leading decentralized exchange for traditional financial asset perpetual contracts (perps). During recent silver volatility peaks, markets deployed under HIP-3 captured about 2% of global silver trading volume, with median spreads for retail-sized trades even better than COMEX. At times, traditional financial instruments accounted for about 30% of the platform's volume, with daily notional trading exceeding $5 billion. Platform revenue in 2025 was approximately $600 million, of which 97% was used for HYPE buybacks and burns.

We expect Hyperliquid to continue dominating TradFi asset perpetual trading. Its product indeed has advantages: commodities and stocks can trade 24/7, even when traditional markets are closed; new markets can be added without approval via HIP-3 proposals; it offers up to 20x leverage on assets where the CME requires 18% initial margin. In the next bull run, if trading volume and fees keep rising, the HYPE token might be repriced similarly to Solana's rebound from bear market lows. If traditional financial asset trading volume continues to expand, HYPE will likely follow a similar path. Investors are likely to extrapolate future sustained high earnings based on one quarter's high revenue.

But Hyperliquid's fee model has already sown the seeds of compression. The platform charges takers a fee of 4.5 basis points of the notional value, offering up to 40% discounts based on trading volume and staking. This is截然不同 (completely different) from traditional financial derivatives pricing logic. On the CME, the exchange fee for one E-mini S&P 500 contract is about $1.33 per side, unrelated to the contract's notional value of over $275,000,折算 (converting to) less than 0.001 basis points. For a $10 million notional position: CME fees are about $2.50, while Hyperliquid charges $4,500, a difference of about 1,800 times.

This spread exists because Hyperliquid's current user base is primarily retail and crypto-native. But TradFi perpetual products will bring TradFi expectations. As trading volume expands and institutional participants enter, pressure to converge towards a CME-style economic model will significantly increase. Hyperliquid's own fee structure already hints at the direction: the HIP-3 growth model slashes taker fees for new markets by over 90%, down to a minimum of 0.0045%; top traders even get below 0.0015%. The protocol is actively推进 (advancing) fee compression. Competitive perpetual DEXs, and future traditional trading venues offering on-chain products, will further accelerate this process. Ultimately, there are two outcomes: either Hyperliquid loses volume because its fees are too high, or it changes its fee model to a fixed fee structure similar to the CME. Either way, the long-term high revenue currently anticipated by investors is difficult to achieve, and the HYPE token price could quickly readjust downward.

Bitcoin: Price Must Grow Before Fees

Among these four assets, Bitcoin is the most unique because the logical relationship between its fees and token price is reversed. For Ethereum, Solana, and Hyperliquid, the logic is: fees generate revenue, revenue supports valuation, fees get compressed, token price falls; but Bitcoin is different, the logic is reversed. Miners must rely on the continuous rise of the coin price to survive after each block reward halving—because fee income has proven unable to fill the gap left by the reduced block subsidy.

The 2024 halving reduced the block reward from 6.25 BTC to 3.125 BTC, daily issuance from 900 BTC to 450 BTC. By late 2025, average daily transaction fees were about $300,000, constituting less than 1% of miner total income. Although Bitcoin's full-year 2024 fee income reached $922 million, most of it came from the阶段性 (phase) peaks of Ordinals and Runes, not sustainable organic fee demand. Current fee contribution is almost negligible; miner income relies almost entirely on the block subsidy, which halves every four years and is denominated in BTC. The only way miners can remain profitable through halving cycles is for Bitcoin's dollar price to roughly double within a similar timeframe, offsetting the 50% reduction in BTC-denominated income. Historically, this condition has held. But this foundation is extremely fragile. The chain's security budget is not funded by usage but by the continuous appreciation of the asset price. If at some halving, the coin price doesn't rise, mining becomes unprofitable, hash rate drops, network security is affected, potentially陷入 (falling into) a vicious cycle of "price drop → hash rate drop → security worsens → price drops further".

This also makes Bitcoin's "sustainability" more fragile than it appears. The ability of the coin price to support network security with almost no fees is a mechanism other chains find difficult to replicate, because Bitcoin is first and foremost a monetary asset, not a smart contract platform.

People buy BTC to hold it, not to use its block space. This gives Bitcoin an advantage the other three chains lack: relying on monetary demand to drive price increases, it can maintain network security even with very low fees.

But this also means Bitcoin's long-term security relies entirely on one assumption—that the price keeps rising—and no one can guarantee that. Whether this chain can remain a secure settlement layer depends not on its ability to create fee-earning applications, but on its ability to maintain the narratives and market conditions that make people want to buy BTC. So far, this model is still functioning normally, but when the block subsidy drops further from 3.125 BTC to 1.5625 BTC, 0.78125 BTC, whether price increases can fill the gap in the next three to four halvings will be one of the most critical unknowns in the crypto space.