Источник:Kalshi Research

Компиляция|Odaily Planet Daily(@OdailyChina); Переводчик|Azuma(@azuma_eth)

Примечание редактора: Ведущая платформа прогнозных рынков Kalshi вчера анонсировала запуск нового исследовательского раздела Kalshi Research, предназначенного для предоставления внутренних данных Kalshi ученым и исследователям, интересующимся темами, связанными с прогнозными рынками. Первый отчет этого раздела уже опубликован, оригинальное название — «Kalshi превосходит Уолл-стрит в прогнозировании инфляции» (Beyond Consensus: Prediction Markets and the Forecasting of Inflation Shocks).

Ниже приведено содержание оригинального отчета, скомпилированное Odaily Planet Daily.

Обзор

Обычно за неделю до публикации важных экономических статистических данных аналитики крупных финансовых институтов и старшие экономисты дают свои прогнозы ожидаемых значений. Эти прогнозы, собранные вместе, называются «консенсус-прогнозом» и широко рассматриваются как важный ориентир для понимания изменений на рынке и корректировки позиций.

В этом отчете мы сравниваем производительность консенсус-прогноза и подразумеваемых цен прогнозного рынка Kalshi (иногда сокращенно «рыночный прогноз» далее) в прогнозировании фактического значения ключевого макроэкономического показателя — годовой инфляции потребительских цен (ИПЦ г/г).

Ключевые моменты

- Общее превосходство в точности: При всех рыночных условиях (включая нормальные и шоковые) средняя абсолютная ошибка (SAO) прогнозов Kalshi на 40.1% ниже, чем у консенсус-прогноза.

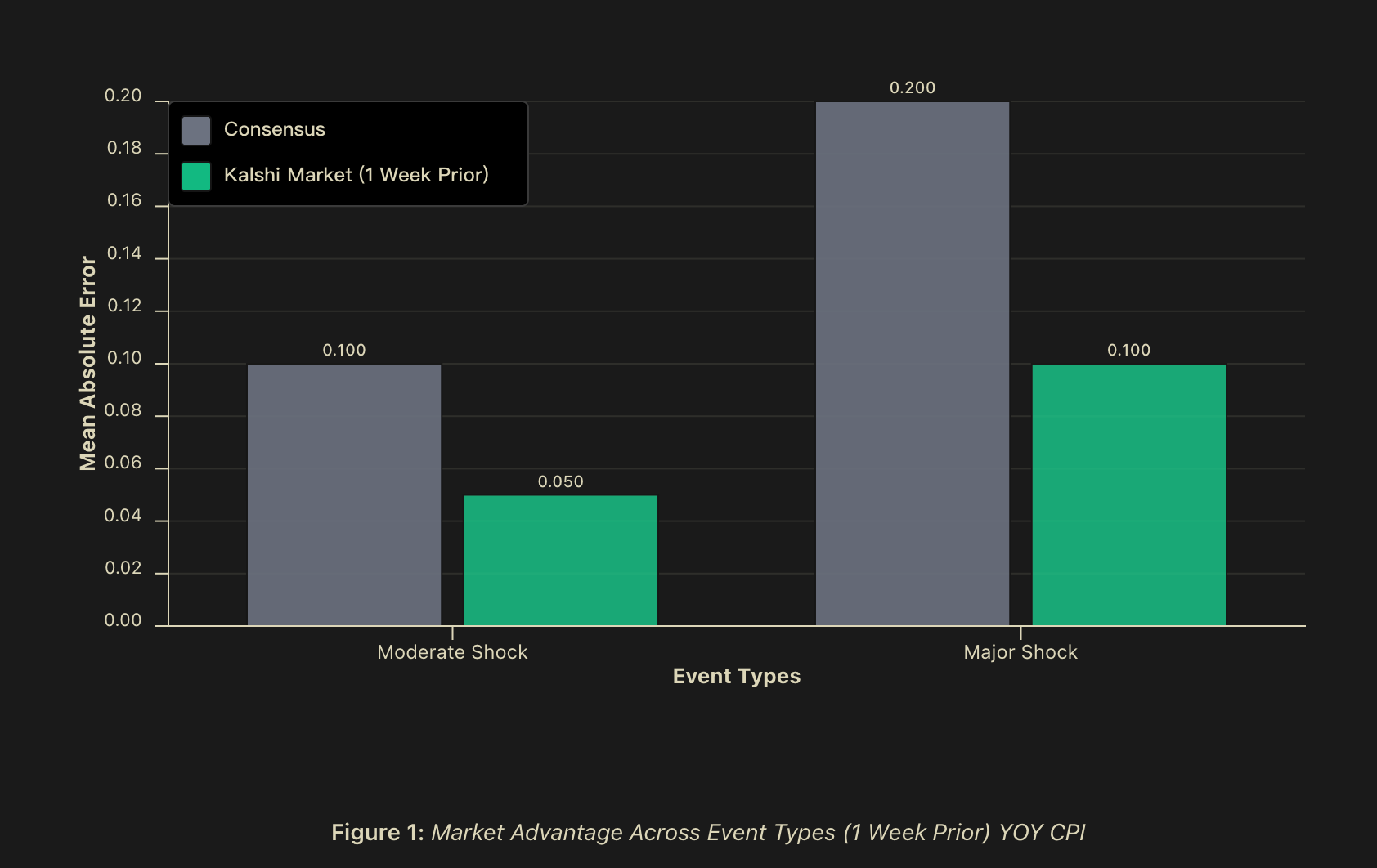

- «Шоковый альфа» (Shock Alpha): Во время значительных шоков (более 0.2 процентных пункта) SAO прогноза Kalshi за неделю до публикации данных на 50% ниже, чем у консенсус-прогноза, а за день до публикации это преимущество увеличивается до 60%; во время умеренных шоков (между 0.1 и 0.2 процентными пунктами) SAO прогноза Kalshi за неделю до публикации также на 50% ниже, чем у «консенсус-прогноза», а за день до публикации увеличивается до 56.2%.

- Прогнозный сигнал (Predictive Signal): Когда расхождение между рыночным прогнозом и консенсус-прогнозом превышает 0.1 процентный пункта, вероятность шока составляет около 81.2%, а за день до публикации данных возрастает примерно до 82.4%. В случаях, когда рыночный прогноз расходится с консенсус-прогнозом, рыночный прогноз оказывается точнее в 75% случаев.

Предыстория

Макроэкономические прогнозисты сталкиваются с внутренней проблемой: самые важные моменты для прогнозирования — периоды рыночных потрясений, изменений политики и структурных разрывов — это как раз те этапы, когда исторические модели чаще всего дают сбой. Участники финансовых рынков обычно публикуют консенсус-прогнозы за несколько дней до выхода ключевых экономических данных, объединяя мнения экспертов в рыночные ожидания. Однако эти консенсусные взгляды, хотя и ценны, часто разделяют схожие методологические подходы и источники информации.

Для институциональных инвесторов, риск-менеджеров и политиков ставки в точности прогнозов асимметричны. В спокойные времена немного лучший прогноз дает ограниченную ценность; но в периоды рыночной неразберихи — когда волатильность взлетает, корреляции рушатся или исторические взаимосвязи перестают работать — лучшее прогнозирование может принести значительную альфа-доходность и ограничить просадки.

Следовательно, понимание поведения параметров в периоды рыночной турбулентности крайне важно. Мы сосредоточимся на ключевом макроэкономическом показателе — годовом индексе потребительских цен (ИПЦ г/г) — основном ориентире для будущих решений по процентным ставкам и важном сигнале состояния экономики.

Мы сравнили и оценили точность прогнозов в нескольких временных окнах до официального релиза данных. Наше ключевое открытие заключается в том, что «шоковый альфа» действительно существует — то есть, в хвостовых событиях рыночные прогнозы могут обеспечить дополнительную точность по сравнению с консенсусным бенчмарком. Это превосходство означает не просто академический интерес, а значительное улучшение качества сигнала именно в те ключевые моменты, когда стоимость ошибки прогноза наиболее высока в экономическом плане. В этом контексте действительно важный вопрос не в том, всегда ли прогнозные рынки «правы», а в том, предоставляют ли они дифференцированный сигнал, который заслуживает включения в традиционные рамки принятия решений.

Методология

Данные

Мы проанализировали ежедневные подразумеваемые прогнозные значения трейдеров на платформе Kalshi за три момента времени: за неделю до публикации данных (совпадает со временем публикации консенсус-прогноза), за день до публикации и утром в день публикации. Каждый используемый рынок был (или является) реальным торгуемым рынком, отражающим реальные денежные позиции при разном уровне ликвидности. Для консенсус-прогноза мы собрали прогнозы консенсуса по ИПЦ г/г на институциональном уровне, которые обычно публикуются примерно за неделю до выхода официальных данных Бюро трудовой статистики США.

Выборка взята с февраля 2023 года до середины 2025 года, охватывая более 25 месячных циклов публикации ИПЦ в различных макроэкономических условиях.

Классификация шоков

Мы разделили события на три категории в зависимости от «величины неожиданности» относительно исторических уровней. «Шок» определялся как абсолютная разница между консенсус-прогнозом и фактически опубликованными данными:

- Нормальные события: ошибка прогноза ИПЦ г/г ниже 0.1 процентного пункта;

- Умеренный шок: ошибка прогноза ИПЦ г/г находится в диапазоне от 0.1 до 0.2 процентных пунктов;

- Значительный шок: ошибка прогноза ИПЦ г/г превышает 0.2 процентных пункта.

Этот метод классификации позволяет нам проверить: меняется ли систематически преимущество в прогнозировании по мере изменения сложности прогнозирования.

Показатели эффективности

Для оценки прогнозной производительности использовались следующие показатели:

- Средняя абсолютная ошибка (SAO): основной показатель точности, рассчитывается как среднее значение абсолютных разниц между прогнозируемым и фактическим значениями.

- Процент побед (Win Rate): когда разница между консенсус-прогнозом и рыночным прогнозом достигала или превышала 0.1 процентный пункта (округлено до одного знака после запятой), мы фиксировали, какой прогноз был ближе к конечному фактическому результату.

- Анализ временного горизонта прогноза: Мы отслеживали, как точность рыночных оценок развивается постепенно от недели до дня публикации, чтобы выявить ценность постоянного включения информации.

Результаты: Производительность прогнозирования ИПЦ

Общее превосходство в точности

При всех рыночных условиях рыночные прогнозы ИПЦ показали среднюю абсолютную ошибку (SAO) на 40.1% ниже, чем консенсус-прогнозы. На всех временных горизонтах SAO рыночных прогнозов ИПЦ была на 40.1% (за неделю) до 42.3% (за день) ниже, чем у консенсус-прогноза.

Кроме того, в случаях расхождений между консенсус-прогнозом и подразумеваемыми рыночными значениями, рыночные прогнозы Kalshi продемонстрировали статистически значимый процент побед, от 75.0% за неделю до 81.2% в день публикации. Если включить случаи ничьи с консенсус-прогнозом (с точностью до одного знака после запятой), рыночные прогнозы примерно в 85% случаев за неделю до публикации были наравне или лучше консенсуса.

Такой высокий показатель точности направления указывает на то, что: когда рыночный прогноз расходится с консенсус-прогнозом, само это расхождение имеет значительную информационную ценность относительно «вероятности наступления шокового события».

«Шоковый альфа» действительно существует

Различия в точности прогнозов особенно заметны в периоды шоковых событий. При умеренных шоках SAO рыночного прогноза в момент публикации была на 50% ниже, чем у консенсус-прогноза, а за день до публикации данных это преимущество увеличивалось до 56.2% и более; при значительных шоках SAO рыночного прогноза в момент публикации также была на 50% ниже, чем у консенсус-прогноза, а за день до публикации достигала 60% и более; а в нормальных условиях без шоков рыночные прогнозы и консенсус-прогнозы показали примерно одинаковые результаты.

Хотя количество шоковых событий в выборке невелико (что разумно в мире, где «шоки по определению высоко непредсказуемы»), общая картина весьма ясна: когда прогнозная среда наиболее сложна, преимущества агрегации информации на рынке оказываются наиболее ценными.

Однако, важно не только то, что прогнозы Kalshi работают лучше в шоковые периоды, но и то, что само расхождение между рыночным прогнозом и консенсус-прогнозом может быть сигналом надвигающегося шока. В случаях расхождений процент побед рыночного прогноза над консенсус-прогнозом составил 75% (в сопоставимых временных окнах). Кроме того, анализ пороговых значений дополнительно показывает: когда отклонение рынка от консенсуса превышает 0.1 процентный пункта, вероятность прогнозируемого шока составляет около 81.2%, а за день до публикации данных эта вероятность进一步 возрастает до примерно 84.2%.

Эта практически значимая разница указывает на то, что прогнозные рынки могут служить не только как конкурентный прогнозный инструмент наряду с консенсус-прогнозом, но и как «мета-сигнал» о неопределенности прогноза, превращая расхождения между рынком и консенсусом в количественный ранний индикатор для предупреждения о потенциальных неожиданных результатах.

Дополнительное обсуждение

Напрашивается очевидный вопрос: почему во время шоков рыночные прогнозы превосходят консенсус-прогнозы? Мы предлагаем три взаимодополняющих механизма для объяснения этого явления.

Разнородность участников рынка и «мудрость толпы»

Традиционные консенсус-прогнозы, хотя и объединяют точки зрения множества институтов, часто разделяют схожие методологические предположения и источники информации. Эконометрические модели, отчеты с Уолл-стрит и публикации государственных данных формируют сильно перекрывающуюся общую базу знаний.

В contrast, прогнозные рынки агрегируют позиции участников с разными информационными базами: включая проприетарные модели, отраслевую аналитику, альтернативные источники данных и интуитивные суждения, основанные на опыте. Это разнообразие участников имеет прочную теоретическую основу в теории «мудрости толпы» (wisdom of crowds). Эта теория предполагает, что когда участники обладают релевантной информацией и их ошибки прогнозирования не полностью коррелируют, агрегация независимых прогнозов из разнообразных источников часто позволяет получить более качественную оценку.

И эта ценность информационного разнообразия особенно突出 в моменты «смены состояния» макросреды — индивиды, обладающие разрозненной, локальной информацией, взаимодействуют на рынке, их информационные фрагменты комбинируются, формируя коллективный сигнал.

Различия в структуре стимулов участников

Прогнозисты на институциональном уровне часто находятся в сложных организационных и репутационных системах, которые систематически отклоняются от цели «чистого стремления к точности прогноза». Профессиональные риски, с которыми сталкиваются карьерные прогнозисты, создают асимметричную структуру выгод — крупные ошибки прогнозирования несут значительные репутационные издержки, в то время как даже чрезвычайно точные прогнозы, особенно достигнутые путем значительного отклонения от консенсуса коллег, не обязательно приносят пропорциональную карьерную отдачу.

Эта асимметрия провоцирует «стадное поведение» (herding), то есть тенденцию прогнозистов сближать свои прогнозы с консенсусным значением, даже если их частная информация или выводы моделей暗示 иные результаты. Причина в том, что в профессиональной системе цена «ошибиться в одиночку» часто выше, чем выгода от «быть правым в одиночку».

В резком contrast с этим, механизмы стимулирования участников прогнозных рынков обеспечивают прямое соответствие между точностью прогноза и экономическим результатом — точный прогноз означает прибыль, ошибочный прогноз означает убытки. В этой системе репутационные факторы практически отсутствуют, единственная цена отклонения от рыночного консенсуса — экономические потери, и она полностью зависит от правильности прогноза. Эта структура оказывает более сильное давление отбора в пользу точности прогноза — участники, способные систематически выявлять ошибки консенсус-прогноза, постоянно накапливают капитал и усиливают свое влияние на рынке через большие объемы позиций; те же, кто механически следует консенсусу,持续 несут убытки, когда консенсус оказывается ошибочным.

В периоды значительного роста неопределенности, когда профессиональные издержки отклонения институциональных прогнозистов от экспертного консенсуса достигают пика, это расхождение в структуре стимулов往往最为 заметно и наиболее важно в экономическом смысле.

Эффективность агрегации информации

Эмпирический факт, на который стоит обратить внимание: даже за неделю до публикации данных — этот момент времени совпадает с типичным окном публикации консенсус-прогноза — рыночные прогнозы все еще демонстрируют значительное преимущество в точности. Это указывает на то, что рыночное преимущество проистекает не только из часто упоминаемого «преимущества в скорости получения информации» участниками прогнозных рынков.

Напротив, рыночные прогнозы, возможно, более эффективно агрегируют те информационные фрагменты, которые слишком分散ны, слишком отраслевы или слишком模糊ды, чтобы быть формально включенными в традиционные эконометрические прогнозные框架. Относительное преимущество прогнозных рынков может заключаться не в более раннем доступе к публичной информации, а в их способности более эффективно синтезировать разнородную информацию в тех же временных масштабах — в то время как механизмы консенсуса на основе опросов, даже имея то же временное окно, часто struggle с эффективной обработкой этой информации.

Ограничения и предостережения

Наши результаты требуют важной оговорки. Поскольку общая выборка охватывает только около 30 месяцев, а значительные шоковые события по определению本就 редки, это означает, что статистическая мощность для крупных хвостовых событий все еще ограничена. Более длинные временные ряды усилят возможности выводов в будущем, хотя текущие результаты уже strongly указывают на превосходство рыночных прогнозов и дифференцированность сигнала.

Заключение

Мы зафиксировали систематическое и экономически значимое превосходство прогнозных рынков над экспертным консенсус-прогнозом, особенно в периоды шоковых событий, когда точность прогнозирования最为关键. Рыночные прогнозы ИПЦ в целом имеют ошибку примерно на 40% ниже, а в периоды значительных структурных изменений снижение ошибки может достигать около 60%.

Основываясь на этих выводах, несколько направлений для будущих исследований становятся особенно важными: во-первых, изучение того, можно ли сами события «шоковой альфы» прогнозировать с помощью показателей волатильности и расхождений в прогнозах, на большей выборке и для多种 макроэкономических показателей; во-вторых, определение порога ликвидности, выше которого прогнозные рынки могут стабильно превосходить традиционные методы прогнозирования; в-третьих, изучение взаимосвязи между прогнозными значениями на прогнозных рынках и значениями, подразумеваемыми инструментами высокочастотной торговли.

В среде, где консенсус-прогнозы в высокой степени зависят от коррелированных модельных предположений и общих наборов информации, прогнозные рынки предоставляют альтернативный механизм агрегации информации, способный раньше улавливать смену состояний и более эффективно обрабатывать разнородную информацию. Для субъектов, которым необходимо принимать решения в условиях растущей структурной неопределенности и учащения хвостовых событий, «шоковая альфа», возможно, представляет не просто постепенное улучшение прогнозных способностей, а должна стать基本组成部分 их надежной инфраструктуры управления рисками.