Оригинал | Odaily Planet Daily (@OdailyChina)

Автор | Azuma (@azuma_eth)

6 января этого года Polymarket официально отказался от модели «нулевых комиссий» и начал пробное введение комиссий за сделки на рынке «15-минутных взлетов и падений криптовалют». Размер комиссии меняется в реальном времени в зависимости от коэффициентов рынка — чем ближе коэффициент к 0% или 100%, тем ниже комиссия; и наоборот, чем ближе коэффициент к 50%, тем выше комиссия, достигая максимум 1,56%.

Позже, 28 января, примерно через три недели после начала взимания комиссий, мы опубликовали статью «По данным расчетов, Polymarket легко может получить годовой доход свыше 100 миллионов, при условии, что...». В статье на основе объема и структуры торговой активности Polymarket на тот момент был сделан статический расчет: в самом консервативном сценарии, если охват платных рынков не изменится,预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估预估极保守的情况下,若收费市场的范围不变,预估 Polymarket 每年可获取约 3800 万美元收入;而在最激进的情况下,若 Polymarket 将手续费扩展至全部市场,预估每年可获得 4.18 亿美元的手续费收入。

В прошлый раз, когда мы оценивали доходы Polymarket, мы также жаловались на слишком короткий период наблюдения и малое количество доступных для расчета образцов. А сегодня, почти через два месяца, мы использовали более обширные данные, чтобы заново оценить прогнозы по доходам Polymarket, и обнаружили, что所谓的“консервативный”действительно был слишком консервативным, а所谓的“агрессивный”прогноз не был слишком преувеличенным.

Изменения данных о доходах

Согласно данным, составленным Gate Research на Dune, с 6 января, когда началось взимание комиссий за сделки, Polymarket накопил свыше 11,2 миллиона долларов дохода от комиссий.

Повторив статическую оценку самым консервативным способом, при условии сохранения объема и структуры торговой активности на соответствующих рынках,预计 Polymarket 每年可获得约 5840 万美元的收入。

Однако такой метод оценки не может точно отразить потенциал доходов Polymarket.

Причина в том, что данные о доходах Polymarket находятся в состоянии видимого роста — за последние 10 недель доходы платформы от комиссий составили 560 000, 786 000, 633 000, 749 000, 1,08 миллиона, 1,28 миллиона, 1,35 миллиона, 1,29 миллиона, 1,63 миллиона и 1,84 миллиона долларов соответственно... наблюдается заметный рост почти каждую неделю.

Причины роста доходов

Рост доходов Polymarket от комиссий обусловлен двумя причинами. Во-первых, Polymarket расширил охват платных рынков; во-вторых, общий объем торгов на Polymarket, а также объем торгов на платных рынках продолжают расти.

Что касается охвата платных рынков, то 6 марта Polymarket распространил механизм комиссий на все рынки, связанные с криптовалютой, кроме того, ранее уже проводились пробные введения комиссий на спортивных рынках, таких как NCAA и Серия А, но первые (рынки, связанные с криптовалютой) в настоящее время仍然是手续费收入的主要来源。

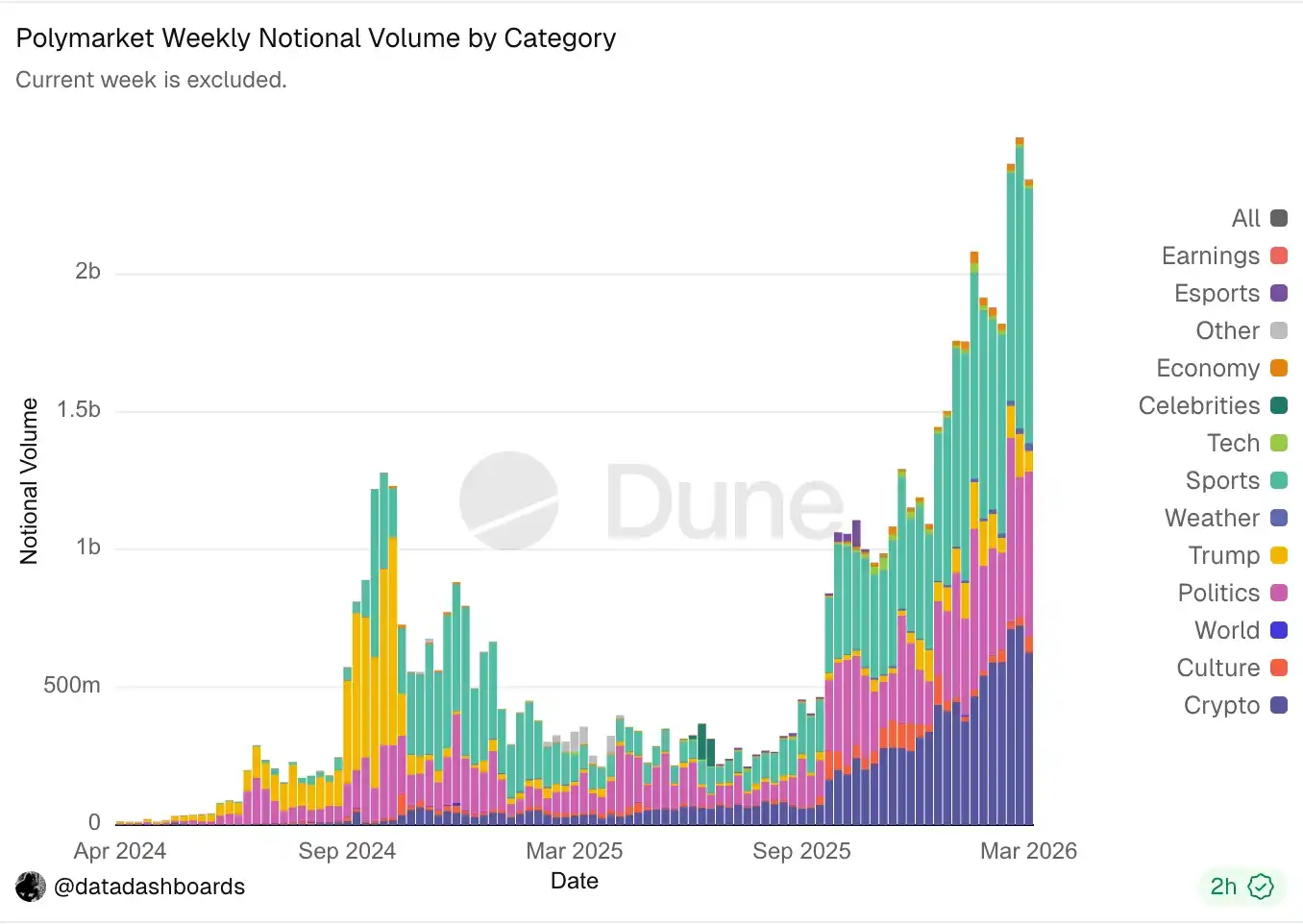

Что касается объема торгов, то панель данных, составленная Data Dashboards на Dune, показывает, что еженедельный общий объем торгов на Polymarket, а также объем торгов на криптовалютных рынках (фиолетовые столбцы внизу) продолжают расти.

Прогноз будущих доходов

В прошлый раз, когда мы делали прогноз доходов Polymarket, нам еще нужно было вручную выяснять долю объема торгов на рынках, связанных с «15-минутными взлетами и падениями криптовалют», во всем объеме торгов на рынках, связанных с криптовалютой. Но теперь, когда Polymarket 6 марта распространил комиссии на все рынки, связанные с криптовалютой, на этот раз оценка стала намного удобнее. Что касается NCAA и Серии А, возможно, потому что первые еще не вышли на正式赛段 «Безумного марта», а вторые не пользуются большой популярностью в американской культуре, объем торгов на соответствующих рынках очень мал по сравнению с криптовалютой, поэтому暂时忽略。

Взяв данные за единственную полную неделю после 6 марта (9.03-15.03), доля объема торгов на событиях, связанных с криптовалютой, в общем объеме торгов на платформе Polymarket на этой неделе составила 26,7%, а доход от комиссий Polymarket за ту же неделю составил около 1,84 миллиона долларов —基于该比例静态推算, при текущем уровне объема торгов и структуре торгов, если Polymarket введет аналогичную модель комиссий на всех рынках,预计可为该平台带来 3.6 亿美元的年收入。

Печатный станок уже запущен

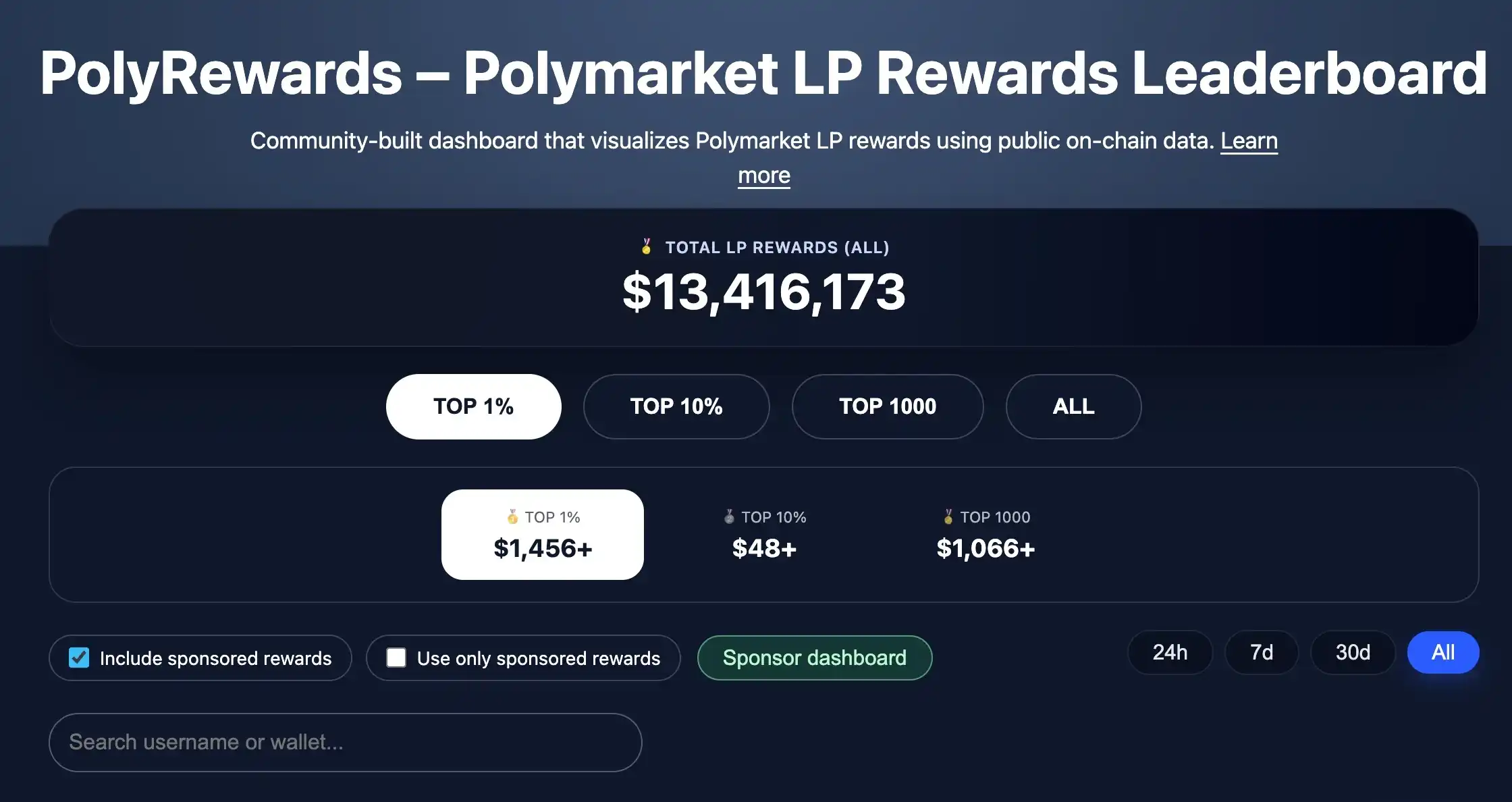

Стоит отметить, что в качестве ключевой меры по увеличению ликвидности Polymarket, платформа на сегодняшний день уже выплатила поставщикам ликвидности (LP) в общей сложности 13,41 миллиона долларов субсидий. Для сравнения, если данные за оставшиеся десять с лишним дней марта продолжат показывать результаты первой половины месяца, то доходы Polymarket от комиссий в течение этого месяца смогут покрыть общие расходы на субсидии ликвидности.

Polymarket в основном уже доказал потенциал доходов этой новой формы рынка прогнозов, и дальнейший рост доходов будет в основном зависеть от двух переменных — насколько еще может вырасти объем торгов и можно ли распространить комиссии на большее количество рынков.

Если эти две переменные продолжат расти, рынок прогнозов, возможно, станет самым простым и прямым «печатным станком» в криптовалютной индустрии.