Автор: Thejaswini M A

Оригинальное название: Coinbase's Walled Garden

Компиляция и редактирование: BitpushNews

В разных отраслях, в разные эпохи и на каждом существовавшем рынке наблюдается постоянно повторяющаяся модель. Сначала — взрывной рост: расцветает множество проектов, каждый участник заявляет, что может выполнить определенную работу лучше других. Растет число экспертов, множатся нишевые инструменты. Потребителям говорят: «Выбор — это свобода», «Кастомизация — это сила», будущее принадлежит тем, кто разбирает монолитных гигантов.

Затем, незаметно, маятник неизбежно качнется обратно.

Это происходит не потому, что эксперты ошибались, и не потому, что гиганты так уж хороши. А потому, что фрагментация имеет невидимую совокупную стоимость. Каждый новый инструмент — это еще один пароль, который нужно запомнить, еще один интерфейс, который нужно изучить, еще одна точка отказа в системе, за которую вы отвечаете. Суверенитет начинает ощущаться как «работа на износ», а свобода — как «административное бремя».

На этапе консолидации最后的赢家 — не те, кто делает каждое дело идеально. Это те, кто делает достаточно много вещей достаточно хорошо, чтобы стоимость перехода (и воссоздания всей системы в другом месте) стала непреодолимой. Они не удерживают вас контрактами или периодами блокировки. Они удерживают вас удобством. Через бесчисленные мелкие интеграции и накопления微小ой эффективности, эти капли, ни одна из которых не стоит того, чтобы из-за нее уходить, вместе образуют защитный ров.

Мы видели это в электронной коммерции. Это происходило в облачных вычислениях, в стриминге. И сейчас мы наблюдаем это в сфере финансов.

Coinbase только что сделала ставку на фазу цикла, в которую мы вступаем.

Исторический контекст

В течение большей части своего существования позиционирование Coinbase было четким. Это было место, где американцы могли купить биткоин, не беспокоясь, что совершают некое сомнительное преступление. У нее были регулируемые лицензии, чистый интерфейс, и, хотя часто критикуемая, но хотя бы теоретически существующая служба поддержки клиентов. В 2021 году компания вышла на биржу с оценкой в 65 миллиардов долларов, и логика заключалась в том, что она является «входом в криптовалюты». Какое-то время эта логика работала.

Но к 2025 году «быть входом в криптовалюты» начало выглядеть как плохой бизнес. Комиссии за спотовые торги сжимаются. Розничные объемы торгов носят резко циклический характер: взлетают на бычьем рынке, рушатся на медвежьем. Максималисты биткоина (Maxis) все чаще привыкают к использованию самодепозитных кошельков. Регуляторы по-прежнему подают на компанию в суд. Тем временем Robinhood, начавшая с торговли акциями и вышедшая на крипторынок, внезапно достигла рыночной капитализации в 1050 миллиардов долларов, что почти вдвое больше Coinbase.

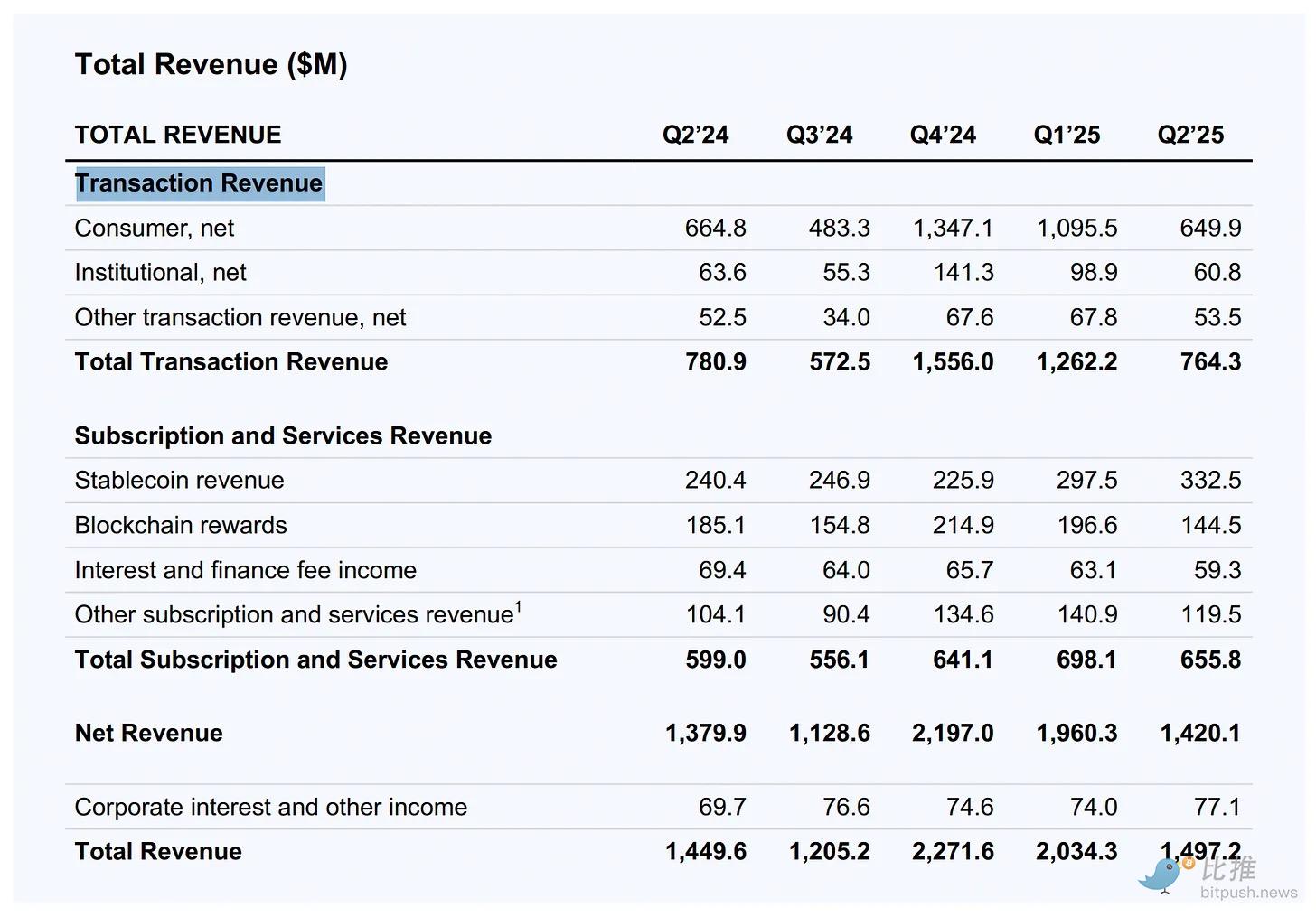

Более 90% выручки Coinbase в 2021 году приходилось на торговые комиссии. К второму кварталу 2025 года эта доля упала ниже 55%.

Поэтому Coinbase сделала то, что положено делать, когда основной продукт под давлением: она попыталась стать «всем остальным».

Гипотеза «Универсальной биржи»

Так называемая гипотеза «Универсальной биржи (Everything Exchange)» — это ставка на то, что агрегация побеждает специализацию.

-

Торговля акциями означает, что пользователи теперь могут реагировать на отчетность Apple в полночь с помощью USDC, не выходя из приложения.

-

Прогнозные рынки означают, что они могут проверить цену на вопрос «Снизит ли ФРС ставку?» во время обеда.

-

Бессрочные контракты означают, что они могут добавить 50-кратное плечо к своей позиции в Tesla в воскресенье.

Каждый новый функциональный модуль — это еще одна причина открыть приложение и еще одна возможность захватить спред, комиссию или проценты на闲置ный баланс стейблкоинов.

Эта стратегия — «давайте станем Robinhood» или «обеспечим, чтобы нашим пользователям никогда не понадобился Robinhood»?

В финтехе есть старое мнение: пользователи хотят специализированные приложения. Одно для инвестиций, одно для банкинга, одно для платежей, одно для криптовалют. Coinbase поставила на противоположное:一旦你完成了一次 KYC (верификацию личности) и привязали один банковский счет, вы не захотите делать то же самое еще девять раз в другом месте.

Это и есть тезис «агрегация побеждает специализацию». В мире, где базовые активы все чаще становятся токенами в блокчейне, это имеет большой смысл. Если акции — это токены, контракты预测市场 — это токены, мемные монеты — это токены, почему они не должны торговаться в одном месте?

Ее механическая логика такова: вы вносите доллары (или USDC), вы торгуете всем, вы выводите доллары (или USDC). Никаких межплатформенных кросс-чейн переводов, никаких требований к минимальному余额у на нескольких счетах. Только один пул средств,流动щий между классами активов.

Эффект маховика

Чем больше Coinbase становится похожей на традиционного брокера, тем больше ей нужно конкурировать на условиях традиционных брокеров. У Robinhood 27 миллионов фондируемых счетов, а у Coinbase около 9 миллионов月度 активных трейдеров. Конкурентное отличие не может быть просто «у нас тоже есть акции», оно должно заключаться в базовой инфраструктуре (Rails).

Ее обещание —提供 24/7 ликвидность для всего. Никаких времени закрытия рынков, никаких задержек расчетов. Когда рынок движется против вас, не нужно ждать одобрения маржинального запроса брокером.

Важно ли это для большинства пользователей? Пока probably нет. Большинству людей не нужно торговать акциями Apple в 3 часа ночи в субботу. Но некоторым — нужно. Если вы то место, где они могут это сделать, вы получаете их поток (Flow).一旦 у вас есть поток, у вас есть данные. Имея данные, вы можете создавать лучшие продукты. Имея лучшие продукты, вы получаете больше потока.

Это маховик, при условии, что он раскрутится.

Игра на预测市场ах

Прогнозные рынки — самая необычная часть этого «набора», и, возможно, самая важная. Это не «торговля» в традиционном смысле, а организованные пари на бинарные исходы: Победит ли Трамп? Повысит ли ФРС ставку? Попадут ли «Лейкерс» в плей-офф?

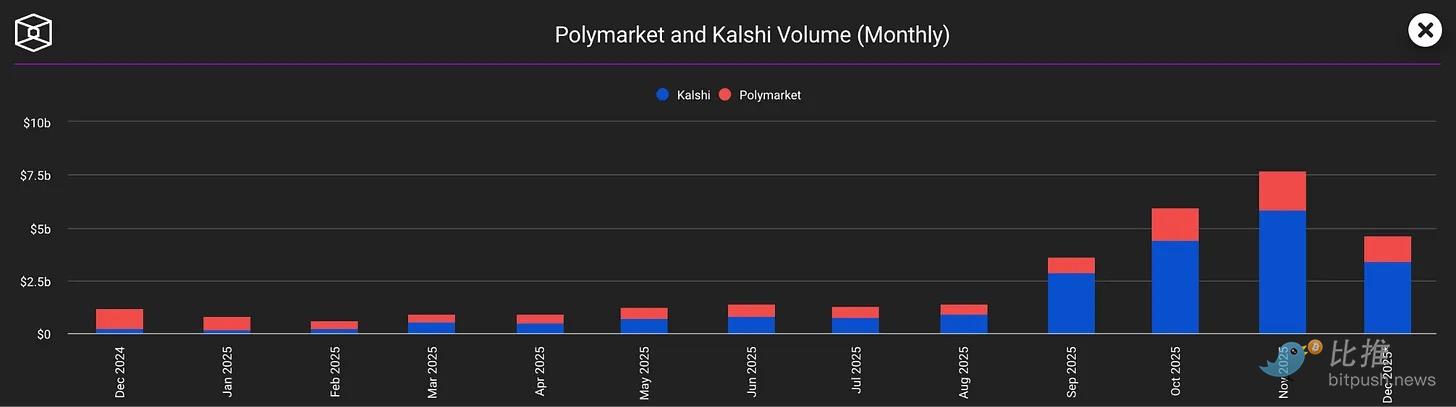

Контракты исчезают после расчета, поэтому нет долгосрочной базы держателей. Ликвидность зависит от событий, что означает ее взрывной и непредсказуемый характер. Тем не менее, такие платформы, как Kalshi и Polymarket, в ноябре saw monthly объем торгов взлетел до более than 7 миллиардов долларов.

Почему? Потому что预测市场 — это социальный инструмент. Это способ выразить мнение со ставками. Это причина проверить телефон в четвертой четверти игры или в ночь выборов.

Для Coinbase预测市场 решают конкретную проблему: вовлеченность (Engagement). Когда цена монеты стоит на месте, криптовалюты становятся скучными. Когда ваш инвестиционный портфель просто лежит, акции тоже становятся скучными. Но в мире всегда происходят события, которые волнуют людей. Интеграция Kalshi дает пользователям причину оставаться в приложении, даже когда биткоин не движется.

Ставка такова: пользователи, пришедшие ради рынков выборов, останутся торговать акциями, и наоборот. Большая площадь функциональности равна более высокой вовлеченности пользователей.

Суть бизнес-модели: Рентабельность

Отбросьте инновационный нарратив, и вы увидите компанию, пытающуюся монетизировать одного и того же пользователя большим количеством способов:

-

Торговые сборы за акции

-

Спреды на обменах DEX (децентрализованных биржах)

-

Проценты на стейблкоин-балансы

-

Плата за кредитование под залог криптоактивов

-

Подписной доход от Coinbase One

-

Инфраструктурные сборы от использования разработчиками блокчейна Base

Это не критика. Так работают биржи. Лучшие биржи — не те, у кого самые низкие комиссии, а те, которые пользователи не могут покинуть — потому что уход означает воссоздание всей системы в другом месте.

Coinbase строит walled garden, но стены построены из «удобства», а не принудительной блокировки. Вы по-прежнему можете вывести свои криптовалюты, вы по-прежнему можете перевести акции в Fidelity. Но, вероятно, вы не станете этого делать, потому что зачем麻烦ться?

Base: Настоящий козырь

Преимущество Coinbase должно было заключаться в ее «ончейн»-природе. Она может предложить токенизированные акции, мгновенные расчеты и программируемые деньги. Но в настоящее время ее торговля акциями выглядит примерно так же, как у Robinhood, только с延长交易时间; ее预测市场 выглядят примерно так же, как у Kalshi, только встроены в другое приложение.

Настоящее отличие должно исходить от Base — Level 2 блокчейна, который создала и контролирует Coinbase. Если акции действительно будут流动ть в ончейне, если платежи действительно будут использовать стейблкоины, если AI-агенты действительно начнут автономно торговать по протоколу x402, тогда Coinbase построила то, что Robinhood не сможет легко скопировать.

Но это долгосрочная история. В краткосрочной перспективе конкуренция сводится к тому, чье приложение наиболее sticky. А добавление большего количества функций не равно增加 stickiness. Оно также может сделать приложение загроможденным, запутанным и создать давление на новых пользователей, которые просто хотят купить немного биткоина.

Масштаб vs. Чистота

Часть криптопользователей будет ненавидеть все это: истинные верующие. Те, кто хотел, чтобы Coinbase была входом в децентрализованные финансы (DeFi), а не централизованным «супер-приложением», которое случайно закопalo несколько функций DeFi в подменю.

Coinbase явно выбрала масштаб, а не чистоту. Она хочет 1 миллиард пользователей, а не 1 миллион пуристов. Она хочет стать местом по умолчанию для обычных людей, а не предпочтительной биржей для тех, кто запускает собственные ноды.

Это может быть правильным бизнес-решением. Массовый рынок не заботится о децентрализации. Массовый рынок prioritizes удобство, скорость и избежание экономических потерь. Если Coinbase может提供 это, лежащая в основе философия не важна.

Но это создает peculiarное напряжение. Coinbase одновременно пытается быть инфраструктурой для ончейн-мира и централизованной биржей, конкурирующей с Charles Schwab; она пытается быть защитником криптовалют и компанией, стремящейся сделать криптовалюты «невидимыми». Она хочет казаться мятежной и при этом соответствовать требованиям регуляторов.

Возможно, это достижимо. Возможно, будущее — за регулируемой ончейн-биржей, которая ощущается как Venmo. Или, возможно, попытка быть всем для всех означает, что в конечном итоге вы не будете ни для кого особенным.

Это стратегия Amazon. Amazon не является лучшей ни в одной отдельной категории: это не лучший книжный магазин, не лучший бакалейный магазин, не лучший стриминг. Но она достаточно хороша во всех этих areas, так что большинству людей лень идти куда-то еще.

Однако многие компании пытались построить «универсальное приложение», и большинство из них просто построили загроможденное приложение.

Если Coinbase сможет захватить полный цикл «зарабатывать, торговать, хеджировать, занимать, платить,循环», то не имеет значения, slightly ли отдельные функции немного хуже, чем у специализированных конкурентов. Стоимость переключения и хлопоты управления несколькими счетами будут удерживать пользователей внутри экосистемы.

Вот и все, что касается «Универсальной биржи» Coinbase.

Twitter:https://twitter.com/BitpushNewsCN

Группа общения比推 TG:https://t.me/BitPushCommunity

Подписка比推 TG: https://t.me/bitpush