Оригинал | Odaily Planet Daily (@OdailyChina)

Автор | Azuma (@azuma_eth)

Рынок продолжает оставаться в упадке, фонды бездействуют, протоколы закрываются, крупные игроки молчат, мелкие инвесторы теряют деньги... Кажется, что все в индустрии, сверху донизу, несут убытки. Но даже в таких холодных рыночных условиях печатные станки некоторых проектов продолжают гудеть.

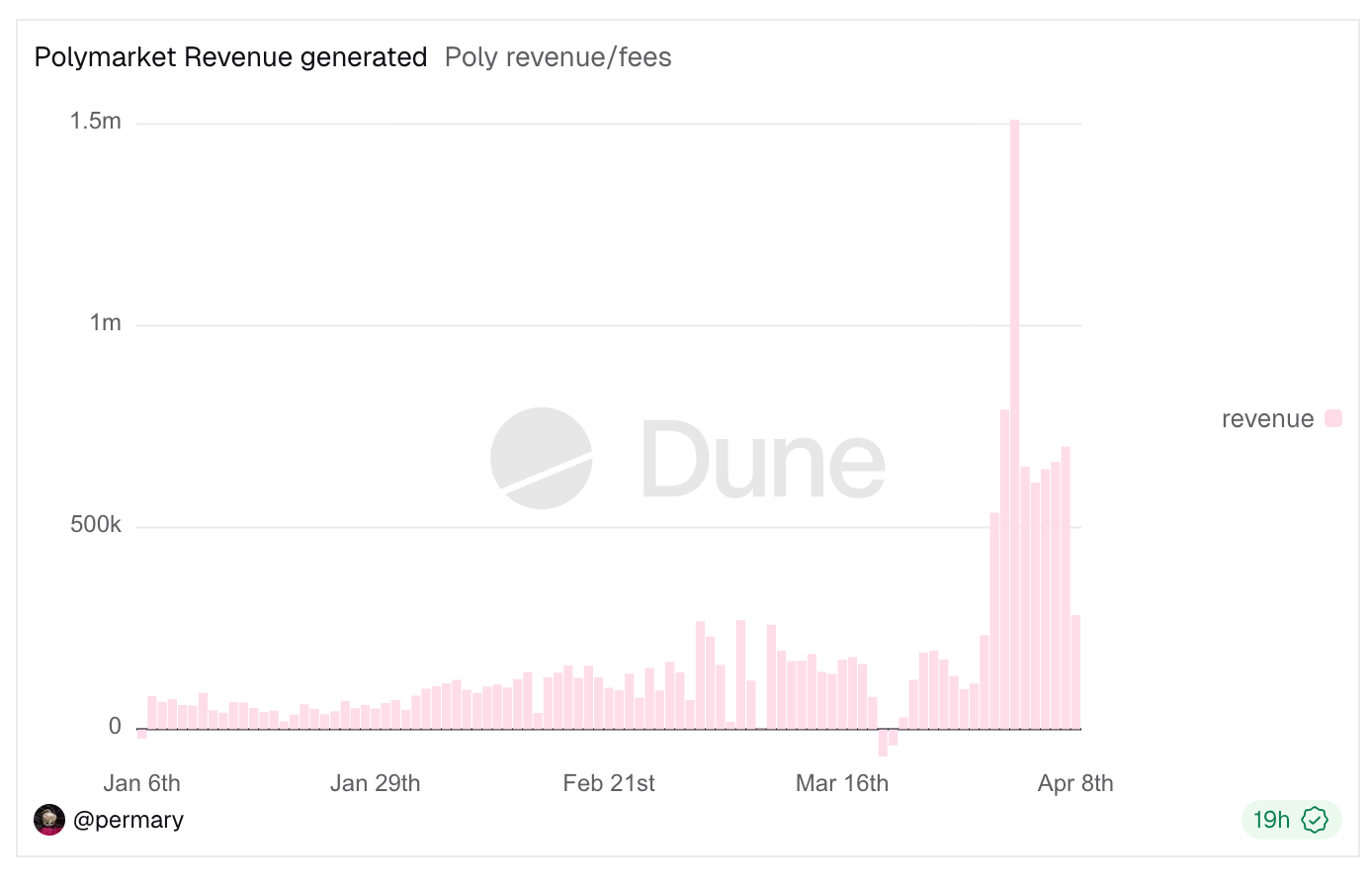

Свежий пример — Polymarket, который полностью открыл шлюзы для комиссий. После недавнего расширения диапазона комиссий и изменения формулы их расчета (рекомендуем прочитать: «Внутренний разбор формулы комиссий Polymarket: как появляется экстремальная ставка в 90+%?») доходность Polymarket значительно выросла; на момент публикации общий доход от комиссий Polymarket превысил 24 миллиона долларов, а 2 апреля был установлен рекорд дневного дохода в 1,5 миллиона долларов.

По этому поводу я заглянул в рейтинг доходности на Defillama, чтобы посмотреть, какие бизнесы продолжают стабильно зарабатывать на медвежьем рынке, и результат оказался довольно неожиданным: основной бизнес и источники дохода проектов в списке были довольно четкими и даже, можно сказать, «простыми».

Как показано на рисунках выше, я уверен, что большинство игроков, глубоко погруженных в крипторынок, даже не глядя на ответ, смогут угадать большинство этих названий и, вероятно, хорошо понимают, чем они занимаются. Но когда эти названия выстроились в аккуратный ряд, я внезапно осознал, что основные источники дохода этих прибыльных бизнесов高度 схожи, и их甚至可以 broadly概括为 две большие категории: маржа (spread) и транзакционный сбор (комиссия).

Во-первых, маржа (spread). По своей сути это «посредничество в капитале», основная логика которого заключается в привлечении средств по относительно низкой стоимости и размещении их с относительно высокой доходностью, используя время для постепенного накопления разницы между доходом и затратами — доходность такого бизнеса зависит от объема и продолжительности размещения средств: чем больше объем и дольше срок, тем выше доход.

К этой категории относятся такие эмитенты стейблкоинов, как Tether и Circle. Их основной доход поступает от процентов, полученных от размещения резервов в таких активах, как казначейские облигации США, а затраты в основном связаны с субсидиями, выплачиваемыми партнерам и пользователям; разница между ними составляет прибыль. Кредитные протоколы, такие как Aave, также относятся к этой категории — маржа представляет собой разницу между относительно высокой процентной ставкой по займам и относительно низкой ставкой по депозитам. Услуги ликвидностного стейкинга (LST), такие как Lido, не являются исключением — они удерживают определенный процент от native-вознаграждений за стейкинг ETH в качестве платы за услугу, что также является маржой.

Во-вторых, транзакционный сбор. Этот тип бизнеса проще для понимания: whenever происходит activity, связанная с транзакциями (включая создание токенов), бизнес-субъект может «взимать налог» в виде комиссии за каждую операцию — доходность такого бизнеса зависит от объема single операции и frequency операций: чем больше объем и выше частота, тем выше доход.

Будь то Hyperliquid и EdgeX, специализирующиеся на торговле фьючерсами, Polymarket, специализирующийся на торговле на событиях, pump.fun, GMGN, Axiom, four.meme, специализирующиеся на торговле мем-токенами, Aerodrome, Jupiter, Phantom (основной доход поступает от комиссий за своп во frontend кошелька), специализирующиеся на спотовой торговле, или же Courtyard, Fragment (то, что они все еще в списке, действительно неожиданно), специализирующиеся на торговле NFT, — их основной источник дохода — это транзакционный сбор.

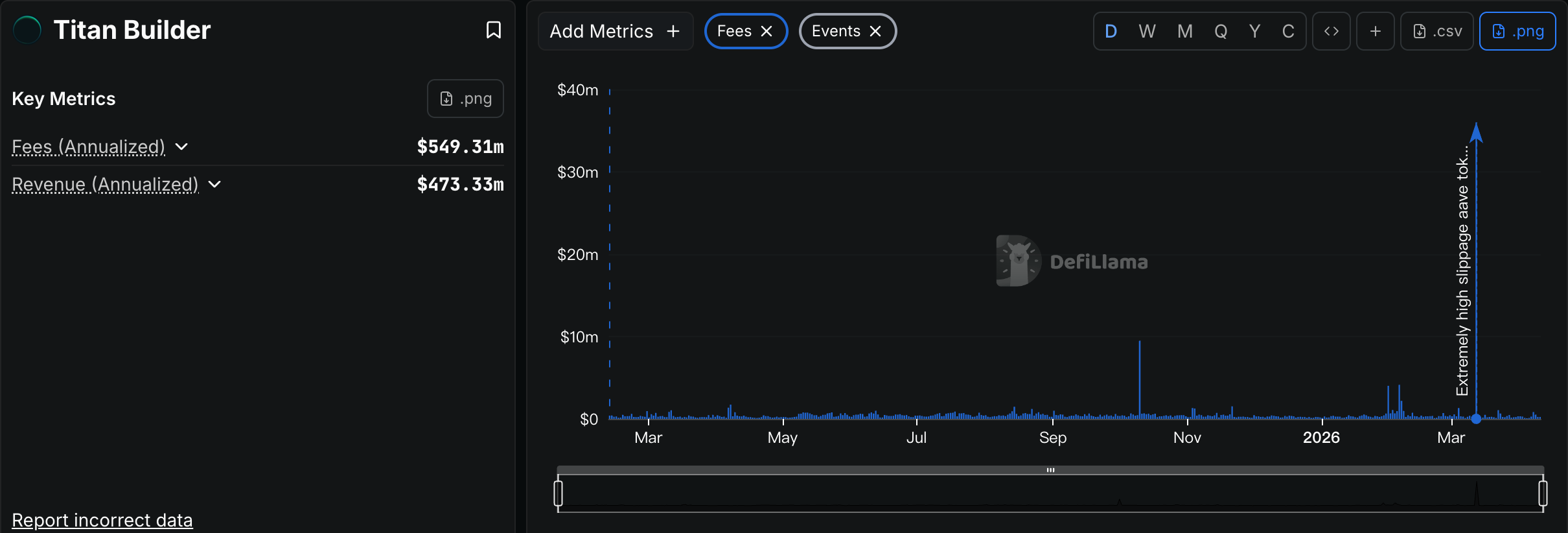

Единственными особыми случаями в рейтинге являются Grayscale, Chanilink и Titan Builder. Grayscale здесь выглядит somewhat странно — его основной доход поступает от управленческих сборов ETF и фондов, по сути, это традиционный бизнес по управлению активами, сфокусированный на криптовалютном рынке; Chanilink же определенно заслуживает упоминания — его основной доход поступает от платы за данные, выплачиваемой проектами за использование oracle-сервиса, это больше похоже на B2B SaaS-бизнес в blockchain, но, как видите, эффект Матфея на этом пути будет более выраженным, чем в других секторах; Titan Builder — чистая случайность. Это провайдер услуг по построению блоков (block builder), в нормальных условиях не считающийся сверхприбыльным бизнесом. Он попал в список потому, что Titan Builder получил самый большой кусок пирога в ходе инцидента с сэндвич-атакой на крупную сделку с AAVE в прошлом месяце (подробнее см. «50 миллионов USDT за 35 тысяч AAVE: как произошла катастрофа?»).

Прим. Odaily: вот что значит три года не открываешься, открылся — на три года хватит.

Таким образом, вывод уже ясен. Проекты, которые продолжают стабильно зарабатывать на медвежьем рынке, — это не те, которые ищут сложные механизмы и высокорискованные возможности, а те, которые могут продолжать работать благодаря простой и понятной модели дохода. На все еще нестабильном криптовалютном рынке более простая модель дохода продемонстрировала более высокую устойчивость, лучше выдерживая испытания рыночной волатильностью.

Однако более простая модель дохода отнюдь не означает, что сам бизнес «легче сделать»; напротив, за простой моделью дохода часто скрываются более сложные продукты и услуги, а также тонкое управление и операционная деятельность — именно в этом топ-игроки из списка по-настоящему «конкурируют» и создают различия. От дизайна взаимодействия (UX) до накопления ликвидности, управления рисками и обратной связи с пользователями... Чтобы выделиться в условиях激烈的 конкурентной борьбы на рынке существующих игроков, необходимо вкладывать больше усилий в продукт и сервис.

Зима на криптовалютном рынке еще не закончилась. Проекты, которые действительно могут выжить и даже быть прибыльными, — это often те, которые гибко сочетают простую модель дохода со сложным продуктом и сервисом. Возможно, в этом и заключается долгосрочный код для прохождения через бычьи и медвежьи рынки.