Если бы нужно было выбрать самые ожидаемые TGE в начале 2026 года в криптосообществе, рынок прогнозов Opinion (OPN), скорее всего, был бы одним из главных претендентов.

Этот проект собрал практически все элементы, необходимые для того, чтобы стать топовым: поддержка ведущих VC, популярное направление, тесная связь с экосистемой Binance, а также нарратив рынка прогнозов, один из самых горячих в последние годы, что привлекло к нему всеобщее внимание еще до запуска.

Состав инвесторов можно назвать роскошным. Opinion Labs привлекла в общей сложности 25 миллионов долларов США в трех раундах: первый ангельский раунд в августе 2024 года, Seed-раунд на 5 миллионов долларов под руководством YZi Labs (бывшая Binance Labs) в марте 2025 года, и еще 20 миллионов долларов в Pre-Series A раунде в феврале этого года, с участием таких топовых фондов, как Hack VC, Jump Crypto, Primitive Ventures и других.

Hack VC — это известный фонд в криптосообществе, специализирующийся на AI и DeFi, ранее инвестировавший в Anthropic; Jump Crypto является важной опорой экосистемы Solana с активами под управлением на десятки миллиардов. Тот факт, что оба фонда сделали ставку одновременно, сам по себе является сильным рыночным сигналом. А YZi Labs (бывшая Binance Labs), участвовавшая в двух раундах подряд, от ангельского до Seed-раунда без пропусков, также напрямую открыла Opinion путь к листингу в экосистеме Binance.

Выбор ниши как нельзя кстати. Последовательные раунды финансирования Polymarket и Kalshi, партнерства с мейнстримными медиа и постоянно растущие объемы торгов сделали рынок прогнозов самым热门ным нарративом в криптосфере с 2025 года по настоящее время. Opinion,深耕щая в экосистеме BSC,长期 занимает третье место в мире по TVL на рынке прогнозов, став одним из первых проектов, вышедших в лидеры на этой волне.

Высокие рыночные ожидания от рынка прогнозов видны и по распределению ресурсов. Binance专门 запустила для OPN Launchpool, выделив 2% предложения для стейкинга BNB/USDC с целью майнинга. На предмаркете цена一度 взлетела более чем на 30%, достигнув максимума в $0.57. Поддержка Binance позволила OPN закрепить свой рыночный статус еще до запуска.

Наложение различных позитивных факторов сделало Opinion для многих обязательным проектом для получения эирдропа в Season 1. Множество пользователей вложили реальные деньги, ожидая получить солидную отдачу от этого проекта, заряженного по полной.

Однако, когда страница проверки эирдропа заработала, ожидания сообщества сменились разочарованием, которое быстро переросло в гнев.

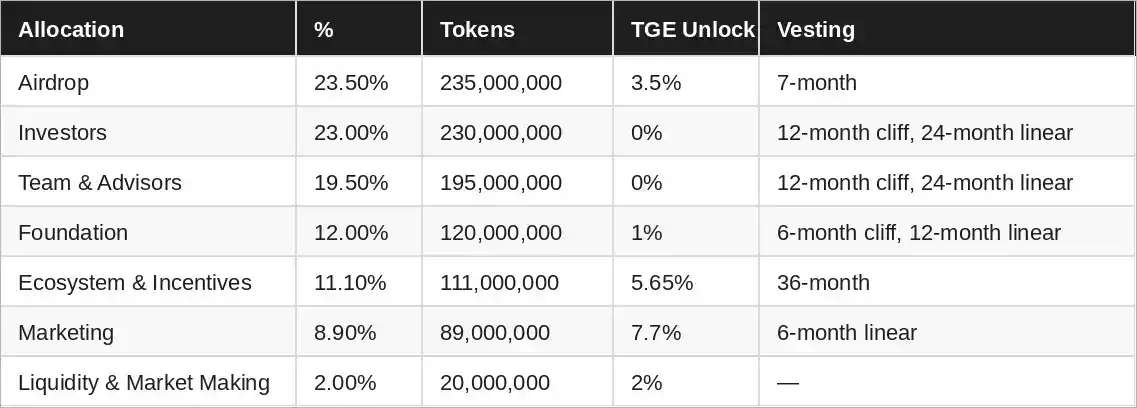

Общее предложение OPN составляет 1 миллиард токенов. На первый взгляд,分配 эирдропа выглядит высоким — 23.5% (235 миллионов токенов). Но проблема в том, что в день TGE было разблокировано лишь 3.5% (35 миллионов токенов), оставшаяся часть будет высвобождаться линейно в течение 7 месяцев. Для подавляющего большинства пользователей, накручивавших объемы, сумма, которую они получили сразу, оказалась значительно меньше ожидаемой.

В то же время,对比另一组 данных окончательно взорвал情绪 сообщества: команда и советники вместе владеют 19.5%, инвесторы — 23%, фонд — 12% — инсайдеры в сумме контролируют более 54% токенов, в то время как все активно участвовавшие пользователи сообщества получили лишь 3.5% в день TGE.

Фактическая отдача для пользователей оказалась плачевной. Несколько участников公开 поделились своими баллами и доходами. Блогер Со Ха (@WEB3_furture) подытожил: «Эирдроп 3%, один балл примерно 15 OPN, сейчас один балл стоит $8.5. На офчейне максимум был $45 за балл. Сейчас похоже, что всех обернули (反撸), у большинства成本 выше $10».

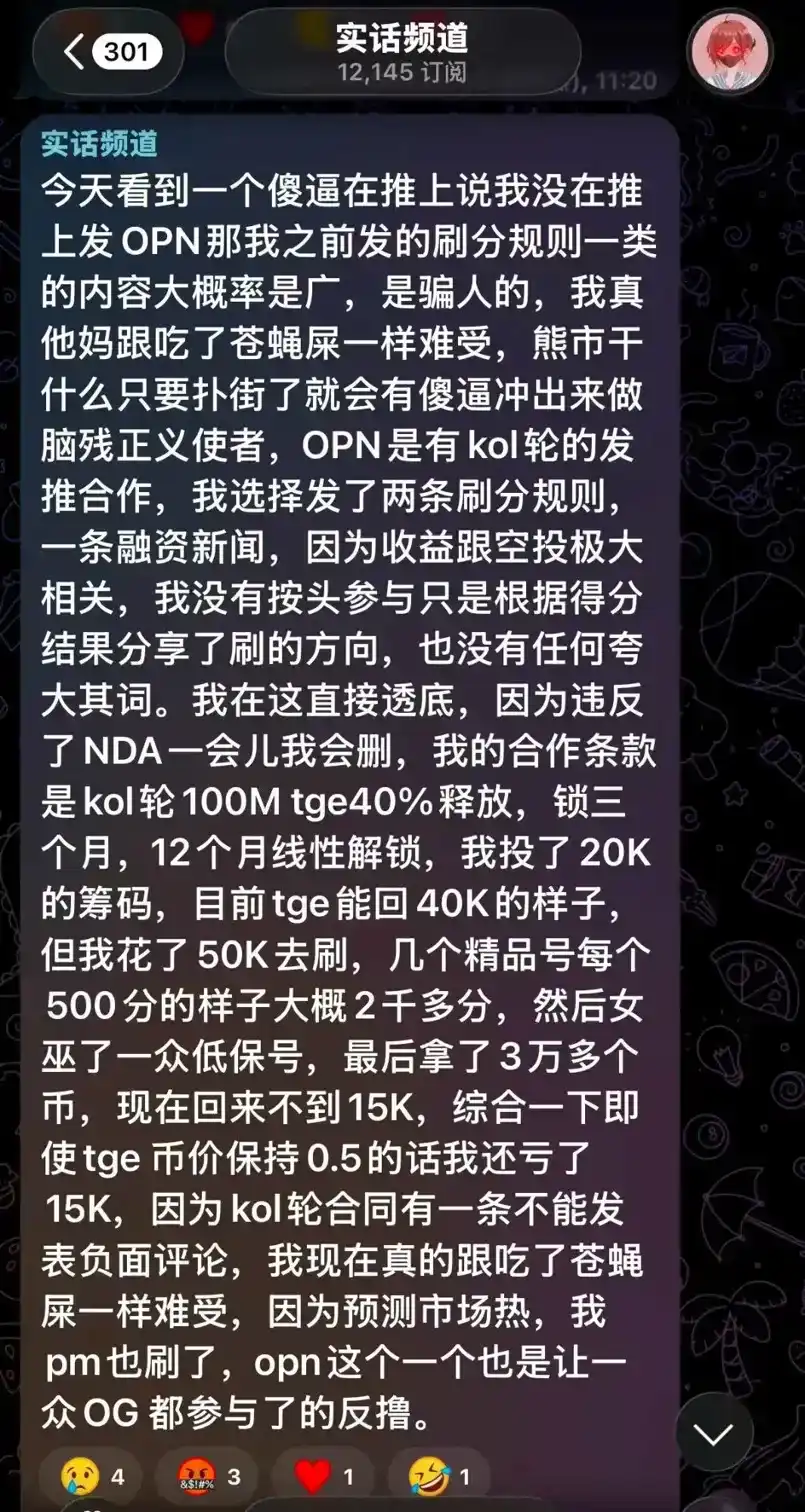

HongKongDoll (玩偶姐姐), участвовавшая во многих проектах в криптосфере, в своем Telegram-канале раскритиковала условия своего KOL-раунда и данные по накрутке баллов. Хотя доход от сотрудничества в KOL-раунде был гарантирован, она инвестировала $50 000 в накрутку баллов, примерно по 500 баллов на каждый качественный аккаунт, и в итоге получила чуть более 30 000 OPN. По цене TGE в $0.5 она отбила меньше $15 000, и даже с учетом回报 от разблокировки инвестиций整体仍然 в минусе на $15 000. Она直言: «Мне сейчас правда так противно, словно муху съела».

Другой KOL, Мати Цзюйцзы (@bitcoinzhang1), указал: «По ценам на Binance до открытия торгов, если бы比例 эирдропа была 5%, один балл оценивался бы в $11; если бы 10% — $22. И это лишь статическая оценка, а ведь еще есть более дешевые筹码 от Binance alpha и booster, которые обрушат цену... Похоже, всех обернули (集体反撸)».

Борьба с сибиллами (女巫) вызвала новую волну споров. Помимо самого распределения, масштабная проверка проектом сибил-аккаунтов и мультиаккаунтинга перед TGE привела к тому, что баллы множества пользователей, накручивавших объемы, были урезаны или дисквалифицированы. Сама по себе эта мера оправдана, но способ и время ее проведения вызвали недовольство сообщества: во время накрутки проект молчаливо允许甚至 поощрял активное участие, а集中ная проверка началась накануне TGE, что многие расценили как стратегию «использовал и выбросил», что углубило впечатление «反撸».

Перекос в распределении в пользу Binance стал мишенью для критики. По сравнению с仅有 3.5% разблокировки для сообщества в TGE, Binance Launchpool получила直接 2% предложения, при этом доля маркетинга была разблокирована на 7.7%, а ликвидность — на 100%. Это对比 привело многих к прямому выводу: «Opinion дала пользователям лишь 3% эирдропа, а Binance —大量筹码». В сообществе普遍认为, что это типичное распределение, «偏向 биржу, в ущерб сообществу».

В Discord и Twitter обсуждение Opinion一时间 было переполнено резкими выражениями вроде «scam», «rug», англоязычное сообщество также вскипело. KOLы公开 публиковали отчеты о убытках, негативные настроения продолжали нарастать.

Стоит отметить, что фундаментальные основы самого по себе проекта не пострадали — финансирование в $25 миллионов, поддержка Hack VC и Jump Crypto, лидирующие позиции на рынке прогнозов в BSC — все это объективные преимущества. Но даже самый сильный состав инвесторов едва ли сможет компенсировать урон, нанесенный подорванным доверием сообщества.

Когда консенсусом сообщества становится «при накрутке данных welcome, после запуска —反撸», самая большая проблема, с которой сталкивается Opinion, возможно, уже не в управлении рыночной капитализацией, а в том, как восстановить基本ное доверие с пользователями.