Author: Prathik Desai

Original Title: The New ICO Test

Compiled and Edited by: BitpushNews

The new year kicked off with a series of major events. The rekindled tariff war between the United States and the European Union has once again brought uncertainty to the forefront. Following closely was a wave of high-volume liquidations in the crypto market within a week.

However, tariffs were not the only "discordant note" at the start of this year. Several Initial Coin Offering (ICO) events that occurred over the past week have given us ample reason to revisit this topic that the crypto community was once obsessed with nearly a decade ago.

Those who remember history might think that the crypto world has long moved beyond the ICO era of 2017. Although many aspects of ICOs have changed since then, the two ICO events last week still raised many key questions—some are old issues, while others are new.

Both the Trove and Ranger ICOs were oversubscribed, albeit without the frenzied aura of Telegram-style countdowns from 2017. However, the evolution of these events still serves as a reminder that the fairness of the community allocation process is crucial.

In today's article, I will delve into what the TROVE and RNGR issuance events tell us about how ICOs are evolving and the trust mechanisms for investors in the allocation process.

The Story Begins:

The more recent of the two, Trove's ICO, ran from January 8 to January 11, raising over $11.5 million upon conclusion. This exceeded the initial $2.5 million target by 4.5 times. The oversubscription clearly indicated investor support and belief in the project, which was positioned as a perpetual contract exchange.

Trove had promised to build on Hyperliquid, leveraging the ecosystem's perpetual contract infrastructure and community.

However, just days after raising funds and before the token generation event, Trove suddenly pivoted, announcing it would launch on Solana instead of the initially promised Hyperliquid. Participants who had invested based on trust in Hyperliquid instantly felt betrayed.

This pivot not only shook investor confidence but also caused widespread confusion. Chaos further escalated when another detail was dug up by investors: Trove stated it would retain approximately $9.4 million of the raised funds for the redesigned plan, refunding only the remaining few million. This undoubtedly raised another red flag.

Ultimately, Trove had to respond.

"We are not taking the money and running," it said in a statement on platform X.

The team insisted that the project remained focused on building, albeit with a changed approach.

Even without making any assumptions, one thing is crystal clear: it is hard to imagine that they were not framed in an unfair, retroactive manner. The funds were initially committed based on one ecosystem, one technical path, and one set of implied risk profiles. The modified plan now requires them to accept another set of assumptions without reopening the participation terms.

It is like changing the rules for one player alone after a game has started.

But by then, the damage was done, and the market voted with its feet, punishing this collapse of trust. The TROVE token plummeted over 75% within 24 hours of its listing, with its market capitalization expectations nearly zeroed out.

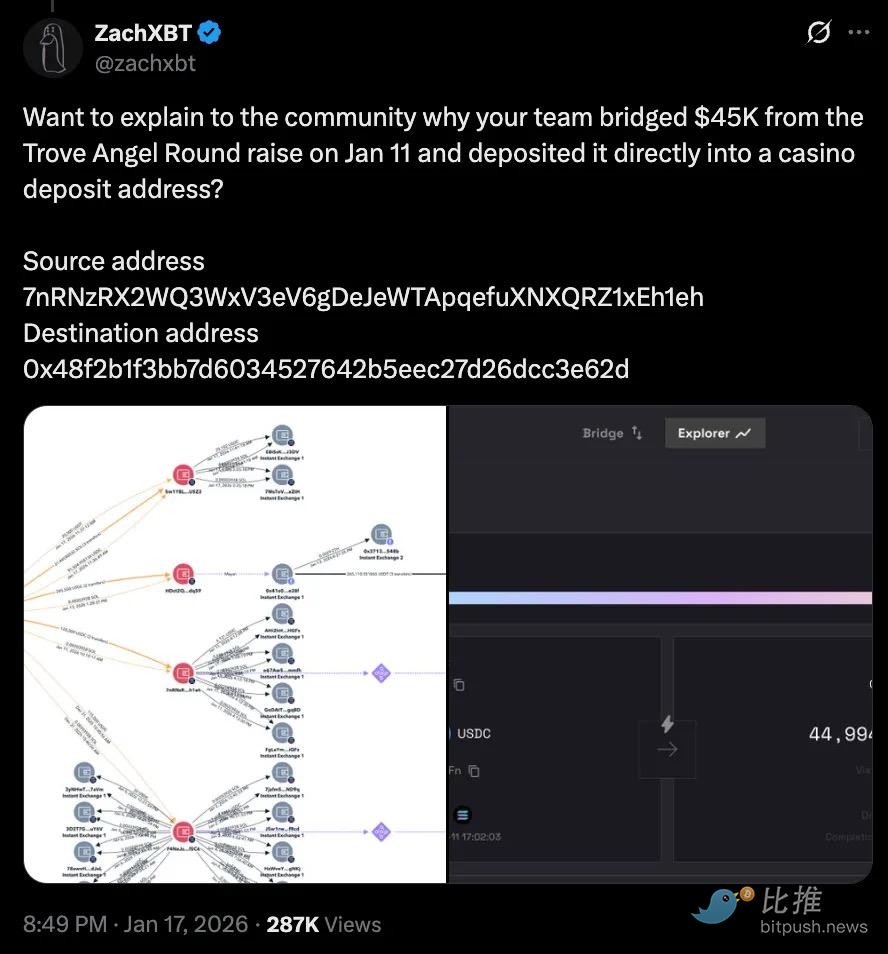

In the community, some moved beyond gut feelings and delved into on-chain fund movements. Crypto detective ZachXBT pointed out several suspicious transactions: approximately $45,000 in USDC from angel round funds eventually flowed into a prediction market platform and even to an address associated with a casino.

Whether this was a careless accounting error, poor fund management, or a genuine red flag remains debatable. Many users criticized the refund process, noting that only a few deserving refund recipients received their payments promptly.

Amid all this, Trove's statements failed to reassure investors who felt betrayed. Although it emphasized that the project would continue—a perpetual exchange on Solana—it did not adequately address the economic concerns arising from the pivot. It provided no detailed breakdown of the modified fund deployment and governance plan, nor did it offer more clarity on the refund roadmap.

Although there is no conclusive evidence linking this pivot to team misconduct, the incident shows that once trust in the fundraising process erodes, every data point is more likely to be viewed with suspicion.

What made this turmoil even more unstable was the way the team handled its discretion after the fundraising concluded.

Oversubscription effectively handed control of both capital and voice to the project team. Once the team changed direction, supporters had little recourse beyond selling on the secondary market or exerting public pressure.

To some extent, Trove's ICO still shares similarities with many projects from past cycles. Although the mechanisms are more standardized and the infrastructure more mature today, the core issue spanning both old and new cycles remains trust—investors still have to rely on the team's judgment rather than a clear set of rules as a backbone.

The Ranger ICO, conducted a few days earlier, provides an important contrast.

Ranger's token sale took place from January 6 to 10 on the MetaDAO platform, which requires teams to predefine key fundraising and allocation rules before the sale begins. Once started, these rules cannot be modified by the team.

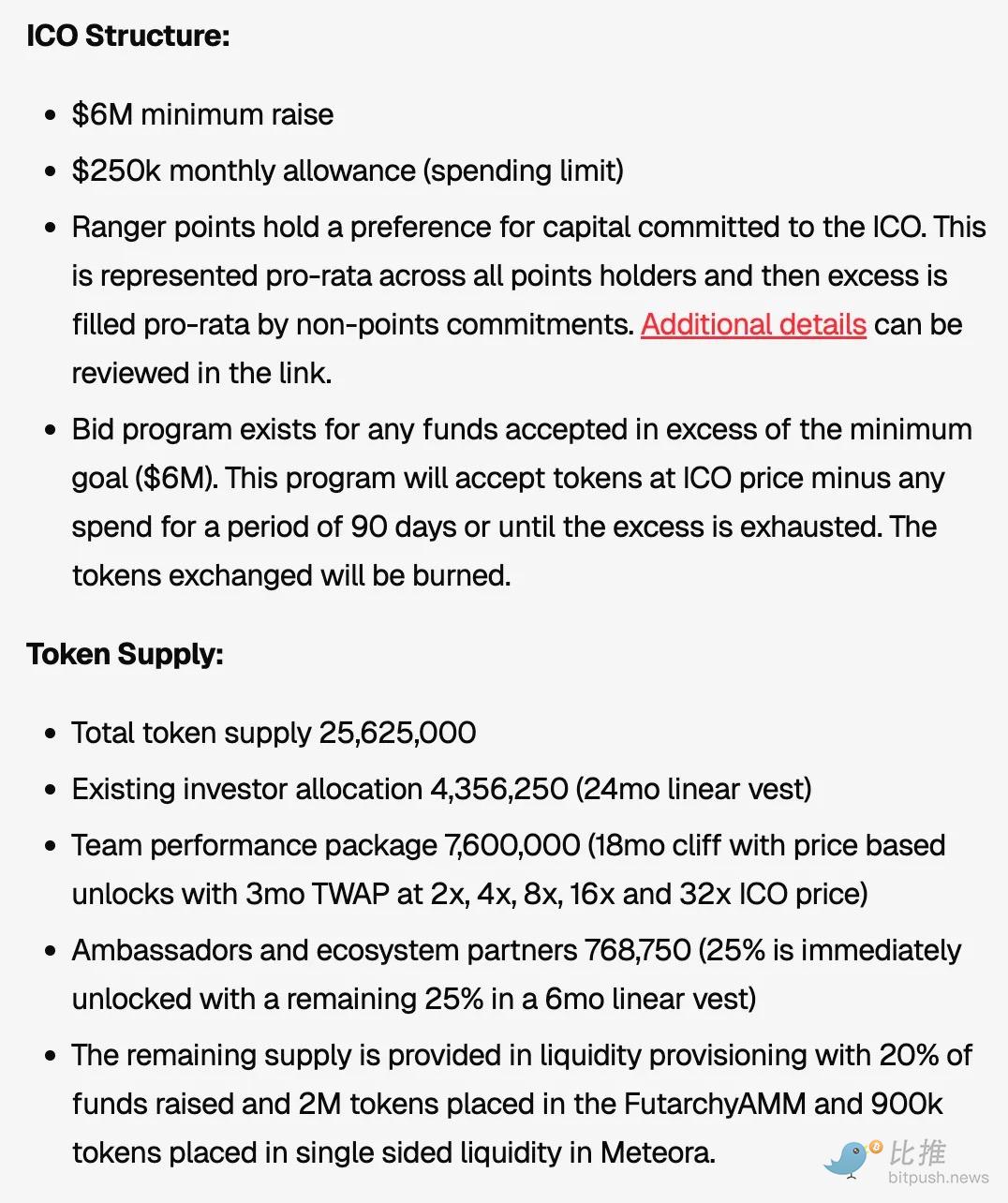

Ranger sought a minimum fundraising target of $6 million and sold approximately 39% of its total token supply through the public sale. Similar to Trove, its sale was oversubscribed. But MetaDAO's constraints meant the team had anticipated the possibility of oversubscription and made arrangements from the outset, unlike Trove's situation.

When the sale was oversubscribed, the proceeds were deposited into a treasury governed by token holders. MetaDAO's rules also restricted the team's access to the treasury to a fixed monthly allowance of $250,000.

Even the allocation structure was defined more clearly. Public sale participants received full liquidity at the token generation event, while presale investors faced a 24-month linear unlock period. The majority of tokens allocated to the team would only unlock upon reaching specific price milestones for the RNGR token. These milestones, such as reaching 2x, 4x, 8x, 16x, and 32x of the ICO price, would be measured using a three-month time-weighted average price, with at least an 18-month lock-up period before any unlocking occurs.

These measures show that the team embedded constraints into the fundraising structure itself, rather than expecting contributors to rely on post-fundraising discretion. Control over capital was partially ceded to governance rules, and any team gains were tied to long-term market performance, protecting contributors from the risk of a "rug pull" on launch day.

Nevertheless, concerns about fairness persist.

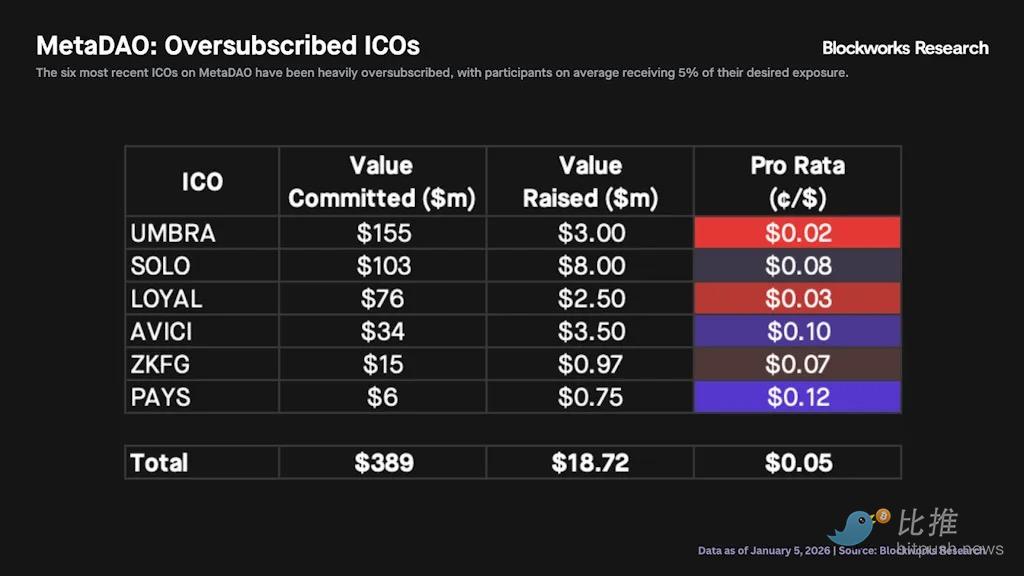

Like many modern ICOs, Ranger used a pro-rata allocation model to distribute tokens in its oversubscribed sale. In theory, this means everyone should receive tokens in proportion to their capital commitment. However, Blockworks Research pointed out that this model often favors participants who can over-commit capital. Smaller contributors typically receive disproportionately small allocations.

However, there is no simple solution to this problem.

Ranger attempted to address this by reserving separate token allocation pools specifically for users who had participated in the ecosystem before the public sale. While this practice alleviated some矛盾, it did not completely resolve a fundamental dilemma: how to balance allowing more people to obtain tokens with ensuring participants receive substantial shares.

Conclusion

The Trove and Ranger events show that nearly a decade after the initial explosion of ICOs, they are still subject to many constraints. The old ICO model heavily relied on Telegram announcements, narratives, and momentum.

The new model relies on structure—including unlock schedules, governance frameworks, treasury rules, and allocation formulas—to demonstrate restraint. These tools, often mandated by platforms like MetaDAO, help limit the discretionary power of launch teams. However, these tools can only reduce risks, not eliminate them entirely.

These events raise critical questions that every future ICO team needs to answer: "Who decides when a team can change plans?" "Who controls the funds after the fundraising is complete?" "What mechanisms do contributors have when expectations are not met?"

In any case, the issues that occurred in the Trove incident need to be corrected. Changing the chain on which a project launches cannot be a spur-of-the-moment decision. Here, the best way to remedy the damage is for Trove to treat its contributors properly. In this case, that might mean fully refunding the funds and re-conducting the sale under revised assumptions.

Although this is the most ideal path forward at the moment, it is not easy for Trove to actually achieve this. Funds may have already been deployed, operational costs may have been incurred, and partial refunds may have already been executed. Reversing course at this point could trigger multiple legal, procedural, and reputational complexities. But this is the price that must be paid to clean up the current mess.

How Trove chooses to proceed may set a precedent for ICOs in the year to come. Project launches now face a more cautious market environment—participants no longer equate oversubscription simply with consensus, nor do they confuse "being involved" with "being protected." Only a truly robust system can provide a fundraising experience that, while not foolproof, is trustworthy enough.

Twitter: https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group: https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush