Редакционное примечание: Пока рынок продолжает волатильность цен на нефть как «результирующую переменную» войны, эта статья утверждает, что по-настоящему важно понять, как сама война оценивается через нефть.

Поскольку Ормузский пролив остается заблокированным, глобальная система поставок нефти вынуждена перестраиваться — азиатские покупатели массово переходят на американскую нефть, WTI опережает Brent, что свидетельствует о структурных изменениях в механизмах ценообразования и торговых потоках. Краткосрочные спреды можно объяснить контрактами, но на более глубоком уровне стоит вопрос: «Кто еще может поставлять?».

Автор далее указывает, что ключевая ошибка рынка сегодня заключается не в цене, а во времени. Кривая фьючерсов все еще подразумевает предпосылку: конфликт закончится в ближайшее время, поставки восстановятся. Но более вероятный путь — это затяжная война на истощение. Это означает, что высокие цены на нефть — это уже не временный шок, а превращающаяся в более устойчивое структурное состояние, с возможным смещением диапазона до 120–150 долларов.

В этой парадигме нефть перестает быть просто сырьевым товаром, становясь «восходящей переменной» для всех активов. Ее переоценка будет передаваться по цепочке через процентные ставки, валютные курсы, рынки акций и кредитные рынки.

Рынок уже оценил факт войны, но еще не оценил ее продолжение.

Далее следует оригинальный текст:

Трамп дал Ирану 10-дневный срок. Это было неделю назад. Вчера он снова всем напомнил: до обратного отсчета осталось 48 часов. Тегеран ответил: нет.

Пять недель назад, 28 февраля, когда американские и израильские самолеты нанесли удар по Ирану, рыночная логика ценообразования все еще предполагала «хирургический» авиаудар: две, максимум три недели; Ормузский пролив возобновляет судоходство; цены на нефть взлетают и затем отступают, все возвращается к норме.

Но наше суждение в то время было: нет.

С первого дня наша ключевая позиция заключалась в том, что эта война сначала эскалирует, и только потом, гораздо позже, возможно, сойдет на нет. Наиболее вероятный путь — ввод сухопутных войск с последующим переходом в затяжной и истощающий конфликт. Перерыв в работе Ормузского пролива значительно превысит те допущения, которые рынок готов закладывать в модели. Мы уже изложили полную логику в рамках анализа продолжительности, модели ценообразования для Ормуза и анализа переменных войны.

Ключевой вывод прост: Ирану не нужно побеждать, ему нужно лишь поднять стоимость войны до уровня, достаточного, чтобы заставить Вашингтон искать путь к выходу. И этот «выход» не будет сопровождаться беспрепятственным reopening пролива.

Спустя пять недель каждая ключевая часть этого прогноза постепенно подтверждается. Ормузский пролив все еще закрыт. Нефть Brent торгуется около 110 долларов. Пентагон готовится к неделям наземных операций. Военные цели Трампа также сместились с «денуклеаризации» к «отбросить противника в каменный век», но он по-прежнему не может четко определить, что такое «победа».

Ввод сухопутных войск — это точка эскалации, за которой мы следили все это время. Морская пехота и воздушно-десантные войска уже сосредоточены в регионе, этот момент приближается.

Но важнее, чем очередной авиаудар или следующий ультиматум, — это нефть.

Нефть не является побочным продуктом этой войны, нефть сама является ее核心. Фондовый рынок, рынок облигаций, криптовалюты, ФРС и даже ваши повседневные расходы на продукты — все это производные переменные. Если правильно оценить нефть, все остальное развернется accordingly; если ошибиться, все остальные решения потеряют смысл.

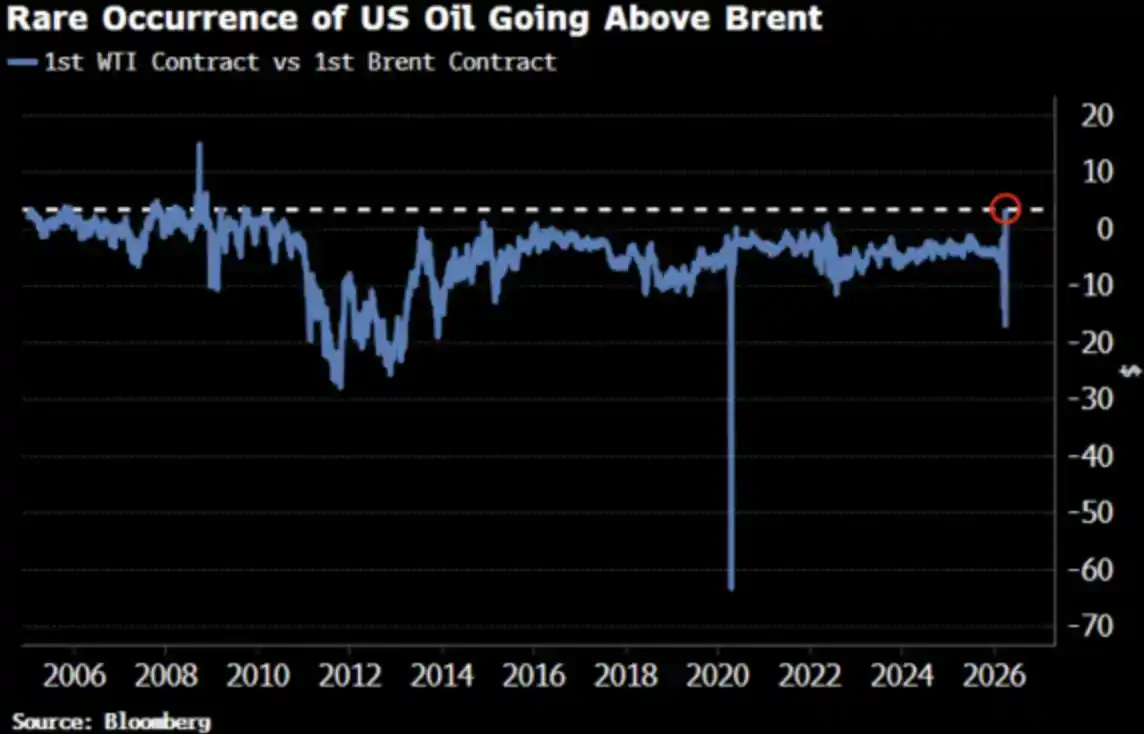

Цена на нефть WTI впервые с 2022 года превысила цену на Brent, и это изменение уже привлекло внимание рынка.

Отлично, так и должно быть.

WTI выше Brent: Все спрашивают, почему

2 апреля WTI закрылась на отметке 111,54 доллара, Brent — на 109,03 доллара. Премия WTI к Brent составила 2,51 доллара, что является наибольшим спредом с 2009 года. А всего две недели назад WTI все еще торговалась со значительным дисконтом к Brent.

Все спрашивают: что произошло? Вот краткая версия и версия, более близкая к реальности.

Краткая версия: Несовпадение сроков контрактов

Ближайший контракт WTI соответствует поставке в мае, в то время как ближайший контракт Brent уже перешел на июнь. В условиях столь напряженного предложения «поставка на месяц раньше» означает более высокую цену — WTI просто оказалась с более ранним сроком поставки.

Нефтяной трейдер с 35-летним стажем, ныне работающий в Оксфорде, Ади Имсирович заявил, что помимо исторически высоких фрахтовых и страховых расходов покупатели готовы платить почти на 30 долларов за баррель больше за нефть Brent, поставленную на месяц раньше. За свои 35 лет карьеры он никогда не видел ничего подобного.

Это объяснение на «механическом уровне» — оно верное, но неполное.

Реальная версия: Кривая цен смещается в целом

Сближение WTI и Brent — это не просто случайное несовпадение ближайших контрактов. Bloomberg отмечает, что это явление четко прослеживается в нескольких контрактных месяцах,贯穿 всей форвардной кривой. Другими словами, вся ценовая кривая переоценивается.

В чем причина? Смещение азиатского спроса. В конце марта азиатские НПЗ заблокировали около 10 млн баррелей американской нефти для отгрузки в мае; неделей ранее также было закуплено около 8 млн баррелей. Kpler прогнозирует, что экспорт нефти из США в Азию в апреле достигнет 1,7 млн баррелей в сутки, что выше мартовских 1,3 млн баррелей в сутки. Китай, Южная Корея, Япония и НПЗ ExxonMobil в Сингапуре покупают американскую нефть — потому что это «единственный товар, который еще можно получить».

Ормузский пролив все еще закрыт. Эталонная нефть Абу-Даби Murban — ближайший заменитель WTI — исчезла с мирового рынка. WTI становится «маржинальной定价 нефтью» для всего мира.

Это не панические закупки, а изменение структуры потоков.

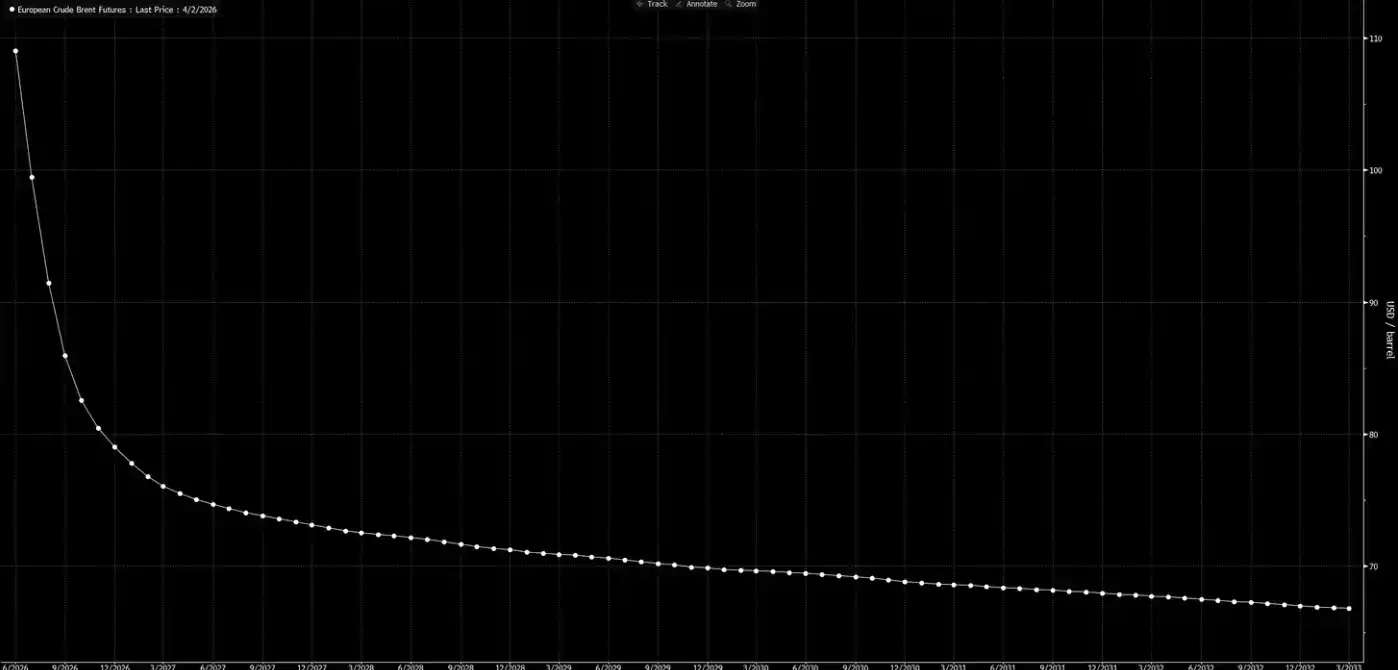

Теперь посмотрим на форвардную ценовую кривую.

Эта кривая передает сигнал: это всего лишь временный шок, и к Рождеству все вернется в норму.

Наше мнение: эта кривая «грезит».

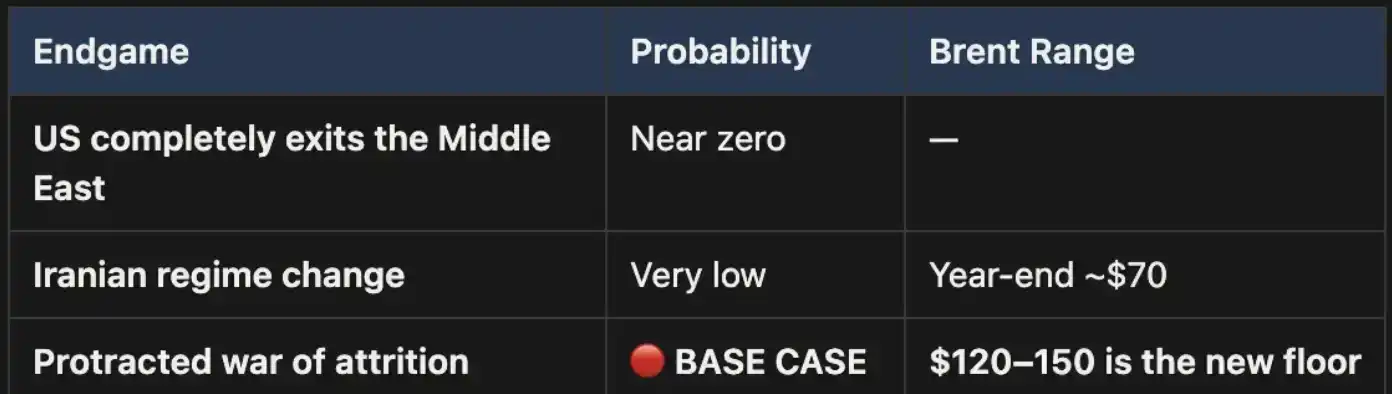

Три исхода, один базовый путь

Мы уже предлагали эту аналитическую структуру в «Weekly Signal Playbook». До сих пор ничего не изменилось; если и есть изменения, то только в сторону усиления вероятности базового сценария.

Эта война может закончиться только тремя способами:

Исход первый, политически почти невозможен.

Исход второй также несостоятелен: условия местности, потребности в войсках и логика развития партизанской войны указывают на то, что этот путь дорого обойдется и его будет трудно завершить. Территория Ирана в три раза больше Ирака, население почти в два раза больше, не говоря уже о горной местности, которая не оставляет захватчикам шансов. Это не 2003 год.

Исход третий является базовым сценарием, и его вероятность значительно выше. Если конфликт перерастет в затяжную войну на истощение, перерыв в работе Ормузского пролива сохранится, и цены на нефть останутся высокими. Эти высокие цены будут структурными, а не временными. Текущая форвардная ценовая кривая явно недостаточно это оценивает.

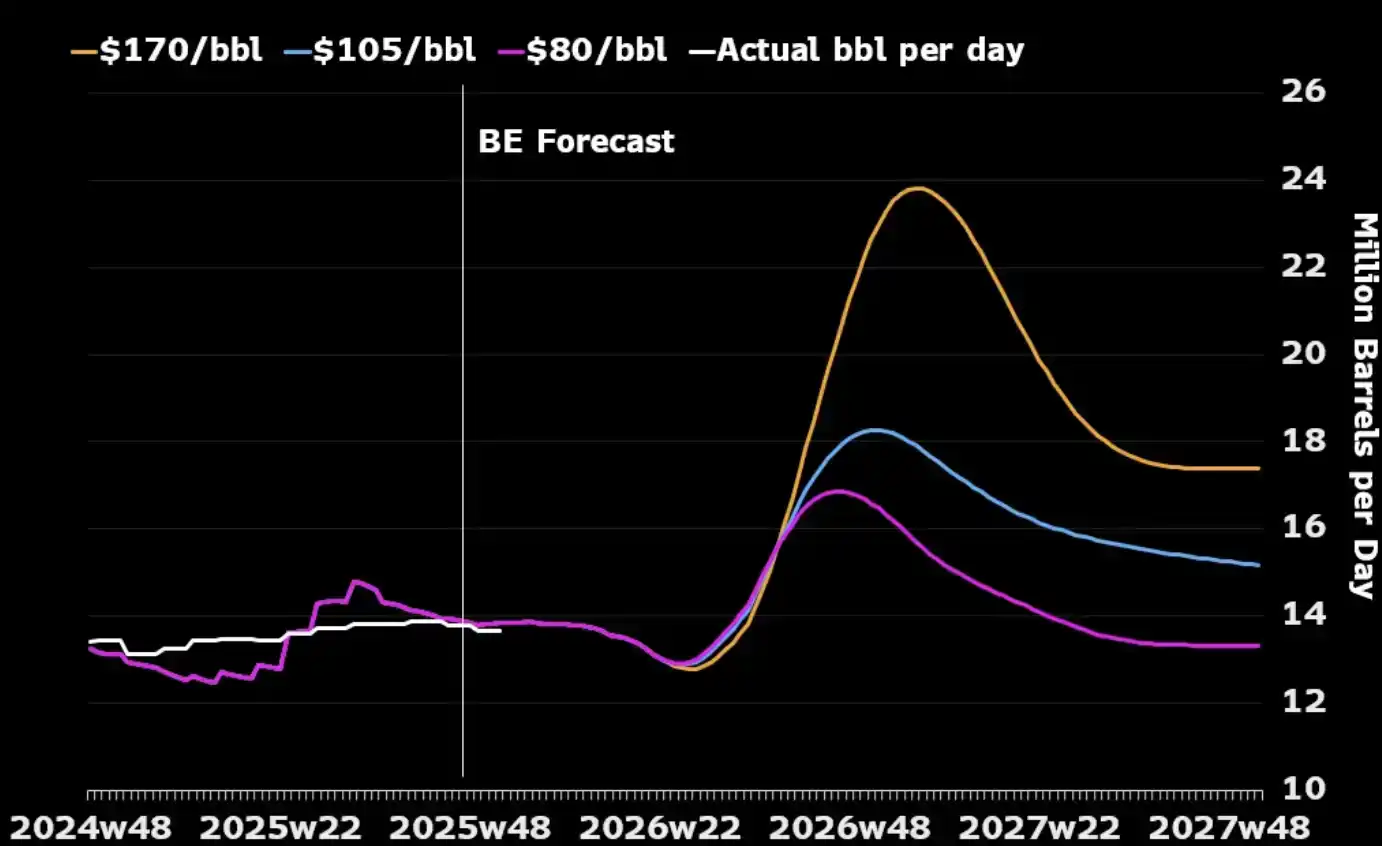

Что упускают из виду большинство: если смотреть только на саму нефтяную отрасль, то затяжная война может соответствовать стратегическим интересам США. Нефтяные мощности Ближнего Востока будут разрушены в ходе конфликта, глобальные покупатели будут вынуждены обратиться к североамериканской энергии, поскольку других альтернативных источников почти не осталось. А более высокие цены на нефть также будут стимулировать американских производителей наращивать добычу — увеличивать количество буровых установок, наращивать инвестиции в сланцевую нефть. Взгляните на график ниже, и вы увидите, что почти каждый значительный скачок цен на нефть в истории приводил к росту добычи в США в последующие 12–18 месяцев.

Единственные затраты, которыми США действительно need to manage, находятся на внутреннем уровне: как избежать долгосрочного удержания цен на бензин выше 4 долларов за галлон, чтобы не спровоцировать политическую реакцию. Это «порог боли», а не условие прекращения войны.

«Арифметика» цен

В условиях закрытия Ормузского пролива 110 долларов за Brent — это не потолок, а лишь отправная точка. В нашем базовом сценарии, пока пролив закрыт, цены на нефть будут сохраняться в диапазоне 120–150 долларов.

С каждой неделей запасы истощаются. Данные UBS показывают, что глобальные запасы упали до пятилетнего среднего уровня к концу марта — и это произошло до последнего раунда эскалации. Macquarie дает свою оценку: если война затянется beyond июня и пролив не откроется, вероятность того, что нефть достигнет 200 долларов, составляет 40%.

Спред между ближайшими месяцами (разница между двумя ближайшими контрактами на Brent) расширился до 8,59 доллара за баррель. Рынок платит премию около 8% за «поставку на месяц раньше» — это уровень напряженности 2008 года.

Но в 2008 году 15% мировых поставок не были физически заблокированы.

Сегодня почти все модели, все ценовые кривые, все годовые прогнозы Уолл-стрит построены на одной и той же предпосылке: этот конфликт закончится, Ормузский пролив вновь откроется, цены на нефть вернутся к норме, мир восстановится.

Наше мнение: нет.

Дальний конец форвардной кривой еще не поспевает за реальностью. Рынок уже оценил «факт войны», но еще не оценил «продолжение войны». До reopening Ормузского пролива любое отступление цен на нефть — это возможность. Это наша ключевая позиция, и мы не будем ее хеджировать.

Нефть — это первый узел. Когда «сухопутные войска вступят» и не будет быстрой победы — когда конфликт перерастет в ту затяжную войну на истощение, которую мы предсказывали с первого дня — переоценка не остановится на самой нефти, а будет передаваться по цепочке через процентные ставки, валютные курсы, рынки акций и кредитные рынки. Это то, что произойдет дальше.